Global Non Animal Stabilized Hyaluronic Acid Fillers Market

Market Size in USD Billion

USD

1.25 Billion

USD

3.17 Billion

2024

2032

USD

1.25 Billion

USD

3.17 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.25 Billion | |

| USD 3.17 Billion | |

| % | |

|

Non-Animal Stabilized Hyaluronic Acid Fillers Market Size

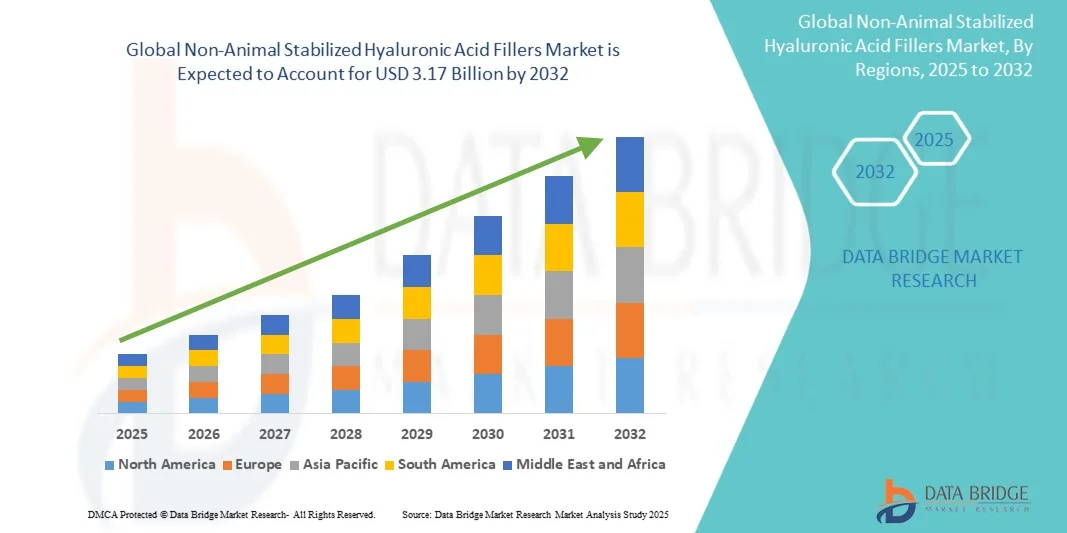

- The global non-animal stabilized hyaluronic acid fillers market size was valued at USD 1.25 billion in 2024 and is expected to reach USD 3.17 billion by 2032, at a CAGR of 12.37% during the forecast period

- The market growth is largely driven by the increasing demand for aesthetic and dermatological treatments, with rising awareness of non-animal stabilized hyaluronic acid fillers as a safer and biocompatible option

- Technological advancements in formulation and delivery methods are enhancing product efficacy, safety, and longevity, making these fillers more attractive to both clinicians and patients

Non-Animal Stabilized Hyaluronic Acid Fillers Market Analysis

- Non-Animal Stabilized Hyaluronic Acid Fillers, widely used in aesthetic and dermatological procedures, are increasingly important due to their safety, biocompatibility, and ability to provide natural-looking facial rejuvenation and wrinkle correction

- The growing demand for these fillers is primarily driven by rising awareness of minimally invasive cosmetic treatments, increasing focus on anti-aging procedures, and consumer preference for non-animal-derived, safe, and effective products

- North America dominated the non-animal stabilized hyaluronic acid fillers market with the largest revenue share of 38.5% in 2024, driven by high disposable incomes, well-established aesthetic clinics, and strong adoption of advanced filler technologies by key market players

- Asia-Pacific is expected to be the fastest-growing region in the non-animal stabilized hyaluronic acid fillers market during the forecast period due to increasing urbanization, growing beauty and wellness awareness, and rising disposable incomes in countries such as China, India, and Japan

- The Single-phase NASHA fillers segment dominated the non-animal stabilized hyaluronic acid fillers market with the largest market revenue share of 52.4% in 2024, attributed to its ease of injection, smooth consistency, and suitability for superficial dermal corrections

Report Scope and Non-Animal Stabilized Hyaluronic Acid Fillers Market Segmentation

|

Attributes |

Non-Animal Stabilized Hyaluronic Acid Fillers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Non-Animal Stabilized Hyaluronic Acid Fillers Market Trends

“Rising Demand and Innovation in Non-Animal Stabilized Hyaluronic Acid Fillers”

- A significant and accelerating trend in the global Non-Animal Stabilized Hyaluronic Acid Fillers market is the growing innovation in formulation and delivery methods, aimed at improving efficacy, safety, and patient satisfaction

- For instance, new injectable fillers with enhanced cross-linking and longer-lasting effects are allowing clinicians to achieve more natural facial contouring, wrinkle reduction, and volume restoration with fewer sessions

- Advanced techniques in filler administration, such as microcannula delivery and combination therapies, are improving patient comfort, minimizing side effects, and optimizing treatment outcomes

- The rise in aesthetic clinics, medispas, and dermatology centers worldwide has made these treatments increasingly accessible, catering to a broadening consumer base seeking minimally invasive cosmetic solutions

- Increasing awareness of non-animal-derived fillers, driven by marketing campaigns, social media influence, and celebrity endorsements, is reshaping consumer expectations for safe and biocompatible anti-aging treatments

- Companies are developing new products that offer longer-lasting results, reduced recovery time, and more versatile applications, meeting the evolving demands of both clinicians and patients

- The global trend towards personalized beauty and wellness is further accelerating market adoption, as patients seek tailored treatment plans and safer, effective alternatives to traditional cosmetic procedures

- Overall, this combination of product innovation, growing accessibility, and rising consumer awareness is driving robust growth and transforming the Non-Animal Stabilized Hyaluronic Acid Fillers market

Non-Animal Stabilized Hyaluronic Acid Fillers Market Dynamics

Driver

“Increasing Demand for Minimally Invasive Aesthetic Procedures and Facial Rejuvenation”

- The global Non-Animal Stabilized Hyaluronic Acid Fillers market is largely driven by the rising preference for minimally invasive cosmetic treatments, as consumers increasingly seek effective alternatives to surgical procedures

- For instance, in March 2024, Allergan Aesthetics expanded its NASHA filler portfolio by launching a new formulation targeting mid-face volumization, enhancing treatment versatility and patient outcomes. Such strategic launches by leading companies are expected to significantly drive market growth during the forecast period

- Growing awareness of aesthetic enhancements, including wrinkle reduction, lip augmentation, and facial contouring, is encouraging more individuals to opt for NASHA fillers over traditional surgical interventions

- The convenience of in-office procedures, shorter recovery times, and reduced procedural risks are key factors propelling adoption among both first-time and repeat patients

- The increasing influence of social media, beauty trends, and celebrity endorsements further stimulates demand for facial aesthetic treatments using NASHA fillers

- Rising disposable incomes and improved affordability of filler treatments in both developed and emerging markets contribute to a wider patient base and higher treatment volumes

- Medical professionals are adopting NASHA fillers due to their proven safety profile, predictable results, and ability to offer natural-looking outcomes, strengthening clinical confidence in these products

- The trend toward personalized aesthetic solutions and tailored facial rejuvenation plans enhances the appeal of NASHA fillers, supporting long-term market expansion

Restraint/Challenge

“Concerns Over Adverse Reactions and High Treatment Costs”

- Despite their popularity, NASHA fillers face challenges related to potential side effects, such as swelling, bruising, or allergic reactions, which can make some consumers hesitant to pursue treatment

- For instance, isolated reports of injection-site complications or overcorrection in certain facial areas have prompted providers to emphasize proper training and post-treatment care

- Addressing these concerns through comprehensive patient education, improved formulation safety, and advanced injection techniques is crucial for building consumer confidence

- In addition, the relatively high cost of NASHA filler treatments compared to other non-surgical cosmetic options can be a barrier for price-sensitive patients, particularly in developing regions

- While treatment affordability is gradually improving through the introduction of smaller-volume syringes and competitive pricing, premium formulations with enhanced longevity or specialized applications still carry a higher price tag

- Ensuring accessibility through broader distribution channels, promotional offers, and bundled aesthetic packages can help overcome cost-related hesitancy

- Regulatory guidelines and safety compliance are critical for sustaining market growth, as strict adherence ensures consumer trust and mitigates risk concerns

- Continued innovation in product development, alongside patient-focused marketing and education campaigns, will be essential to drive widespread adoption of NASHA fillers globally

Non-Animal Stabilized Hyaluronic Acid Fillers Market Scope

The market is segmented on the basis of type, application, end-users, and distribution channel.

• By Type

On the basis of type, the non-animal stabilized hyaluronic acid fillers market is segmented into Single-phase NASHA fillers and Biphasic NASHA fillers. The Single-phase NASHA fillers segment dominated the largest market revenue share of 52.4% in 2024, attributed to its ease of injection, smooth consistency, and suitability for superficial dermal corrections. Clinicians prefer single-phase fillers for wrinkle reduction and subtle facial enhancements due to their predictable spread and uniform results. The segment benefits from wide adoption in dermatology and cosmetic clinics, supported by extensive clinical studies validating safety and efficacy. Availability of a broad range of viscosities and formulations further strengthens market leadership. Patient demand for natural-looking outcomes and minimal downtime also contributes to dominance. Global awareness campaigns and social media influence on cosmetic procedures drive consistent adoption. The segment’s robust presence across developed and emerging markets ensures continued growth.

The Biphasic NASHA fillers segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032. This growth is driven by increasing demand for volumizing procedures, deep tissue augmentation, and enhanced facial contouring. Biphasic fillers offer versatility in treating deeper folds and restoring facial volume, making them ideal for advanced aesthetic applications. Rising adoption in specialty clinics and medical spas supports segment growth. Technological improvements in gel cohesion and longevity increase patient satisfaction and repeat treatments. Clinicians favor biphasic formulations for sculpting and volumetric corrections in the mid-face and cheek areas. The market for biphasic fillers is expanding rapidly in regions with rising disposable incomes and awareness of anti-aging solutions. Strategic product launches and marketing campaigns further accelerate adoption globally.

• By Application

On the basis of application, the non-animal stabilized hyaluronic acid fillers market is segmented into wrinkle reduction, facial line correction, lip enhancement, restoration of facial volume, and others. The wrinkle reduction segment dominated with a revenue share of 45.7% in 2024, driven by the increasing preference for non-surgical aesthetic solutions to treat fine lines and prevent early signs of aging. Patients favor wrinkle reduction procedures due to minimal invasiveness, shorter recovery times, and natural outcomes. Clinics and dermatology centers widely recommend NASHA fillers for forehead, crow’s feet, and periorbital wrinkles. Awareness campaigns, social media trends, and celebrity endorsements contribute to the segment’s popularity. Insurance coverage for cosmetic procedures in certain regions encourages adoption. Ease of combination with other aesthetic treatments, such as Botox, strengthens the segment’s market position. Continuous product innovations, such as longer-lasting formulations, support sustained dominance.

The facial volume restoration segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032. This growth is fueled by increasing demand for mid-face and cheek augmentation, especially among aging populations seeking natural-looking rejuvenation. Patients are increasingly opting for volumizing fillers to correct age-related tissue loss and enhance facial contours. Clinicians prefer NASHA fillers for safe, predictable volumization with minimal downtime. Awareness of non-surgical alternatives to facelifts and growing disposable incomes drive adoption. Marketing campaigns and influencer endorsements highlighting youthful outcomes boost patient interest. The segment is rapidly gaining traction in specialty aesthetic clinics and medical spas. Technological advancements, including enhanced gel cohesivity and extended longevity, contribute to accelerated growth.

• By End-Users

On the basis of end-users, the non-animal stabilized hyaluronic acid fillers market is segmented into hospitals, specialty & dermatology clinics, medical spas, and others. The specialty & dermatology clinics segment dominated the largest revenue share of 50.6% in 2024. This dominance is due to their established expertise, availability of trained professionals, and ability to offer customized treatment plans. Clinics provide both consultation and post-treatment follow-up, enhancing patient confidence. The segment benefits from a concentrated patient base seeking aesthetic enhancements. Advanced equipment and technology adoption in these clinics ensures high-quality procedures. Continuous training programs and clinical certifications strengthen trust in outcomes. Partnerships with product manufacturers enhance accessibility to new NASHA filler formulations. Clinics also attract repeat patients due to convenience, safety, and predictable results.

The medical spas segment is expected to witness the fastest CAGR of 20.3% from 2025 to 2032. This growth is driven by the increasing popularity of wellness-oriented aesthetic services and non-invasive cosmetic procedures. Medical spas offer combined services, such as skincare treatments alongside NASHA filler injections, appealing to younger, beauty-conscious demographics. Rising consumer awareness, social media trends, and convenience encourage adoption. The segment is particularly expanding in urban centers and high-income regions. Innovative marketing, package deals, and flexible treatment options contribute to rapid market expansion. Advancements in minimally invasive techniques and shorter recovery periods further accelerate growth. Strategic collaborations with product manufacturers enhance access to advanced formulations, driving segment adoption.

• By Distribution Channel

On the basis of distribution channel, the non-animal stabilized hyaluronic acid fillers market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated with a revenue share of 48.2% in 2024, supported by direct supply to clinics and hospitals, regulatory compliance, and assurance of genuine product quality. Hospitals and clinics often prefer sourcing from established pharmacies to ensure consistent stock availability and adherence to safety standards. Strong partnerships with leading NASHA filler manufacturers and centralized procurement systems further reinforce dominance. Post-treatment follow-up and professional guidance available at hospitals add to patient trust. Educational campaigns and awareness programs conducted through hospital channels strengthen market penetration.

The online pharmacy segment is expected to witness the fastest CAGR of 21.1% from 2025 to 2032. Growth is fueled by the increasing adoption of e-commerce and digital health platforms facilitating convenient access to NASHA fillers. Online channels offer a broader reach, allowing smaller clinics and individual practitioners to procure products efficiently. Consumers are increasingly comfortable purchasing medical-grade fillers through verified online portals. Promotional discounts, subscription models, and faster delivery services enhance adoption. The expansion of reliable logistics and adherence to storage standards ensures product safety. Increasing awareness campaigns and digital marketing efforts further accelerate segment growth globally.

Non-Animal Stabilized Hyaluronic Acid Fillers Market Regional Analysis

- North America dominated the non-animal stabilized hyaluronic acid fillers market with the largest revenue share of 38.5% in 2024, driven by high disposable incomes, a well-established network of aesthetic and dermatology clinics, and strong adoption of advanced filler technologies by key market players

- The market captured the largest share within the region, fueled by rising consumer awareness of minimally invasive cosmetic procedures and growing demand for anti-aging and facial rejuvenation treatments

- Increasing investment in research and development, coupled with a growing number of trained aesthetic professionals, is further supporting market expansion

U.S. Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The U.S. non-animal stabilized hyaluronic acid fillers market captured the largest revenue share within North America, in 2024. Growth is fueled by increasing awareness and adoption of aesthetic treatments, rising investment in dermatology and medispas, and strong demand for non-animal-derived fillers. The presence of leading manufacturers, coupled with ongoing innovations in filler formulations and delivery methods, is further driving market expansion. Consumers are increasingly prioritizing safe, effective, and minimally invasive treatments for wrinkle reduction, facial contouring, and volume restoration.

Europe Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The Europe non-animal stabilized hyaluronic acid fillers market is projected to expand at a significant CAGR during the forecast period. Growth is primarily driven by rising consumer awareness of aesthetic treatments, increasing disposable incomes, and a growing preference for minimally invasive cosmetic solutions. The region is witnessing higher adoption in both established urban centers and emerging markets, supported by the presence of leading cosmetic product manufacturers and dermatology specialists. France, Germany, and the U.K. are key contributors to market growth due to their advanced healthcare infrastructure and strong focus on beauty and wellness.

U.K. Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The U.K. non-animal stabilized hyaluronic acid fillers market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising consumer interest in anti-aging procedures and facial rejuvenation treatments. An increase in aesthetic clinics, medispas, and dermatology centers, along with strong social media influence and beauty trends, is driving demand. Personalized treatment plans and growing awareness about non-animal-derived fillers further contribute to the market’s expansion.

Germany Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The Germany non-animal stabilized hyaluronic acid fillers market is expected to expand steadily, driven by high healthcare standards, advanced cosmetic infrastructure, and increasing focus on minimally invasive aesthetic procedures. The presence of skilled dermatologists and growing consumer preference for natural-looking results are supporting market growth. Additionally, rising interest in wellness and beauty, along with government support for innovation, is fostering the adoption of non-animal-derived fillers across residential and commercial aesthetic practices.

Asia-Pacific Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The Asia-Pacific non-animal stabilized hyaluronic acid fillers market is expected to be the fastest-growing region in the Non-Animal Stabilized Hyaluronic Acid Fillers market during the forecast period, driven by increasing urbanization, growing beauty and wellness awareness, and rising disposable incomes in countries such as China, India, and Japan. Rapid development of aesthetic clinics, increasing awareness of minimally invasive cosmetic procedures, and the expanding middle-class population are major growth factors. Additionally, innovations in product formulations and delivery methods are further enhancing adoption rates in the region.

Japan Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The Japan non-animal stabilized hyaluronic acid fillers market is gaining momentum due to high consumer awareness of aesthetic treatments, an aging population, and growing demand for safe, effective, and convenient anti-aging solutions. Increasing availability of non-animal stabilized fillers, combined with a strong network of dermatology clinics and medispas, is driving the adoption of these products. Cultural emphasis on beauty and wellness, along with technological innovations in aesthetic treatments, further supports market growth.

China Non-Animal Stabilized Hyaluronic Acid Fillers Market Insight

The China non-animal stabilized hyaluronic acid fillers market accounted for the largest market revenue share in Asia-Pacific in 2024, fueled by a rising middle class, rapid urbanization, and increasing disposable incomes. Strong consumer preference for minimally invasive aesthetic procedures and growing awareness of non-animal-derived fillers are key factors propelling the market. The expanding network of aesthetic clinics, combined with innovative product launches and effective marketing strategies, is contributing to China’s robust market growth.

Non-Animal Stabilized Hyaluronic Acid Fillers Market Share

The non-animal stabilized hyaluronic acid fillers industry is primarily led by well-established companies, including:

- Galderma (Switzerland)

- Hugel, Inc. (South Korea)

- Croma-Pharma GmbH (Austria)

- Revance Therapeutics (U.S.)

- LG Chem Life Sciences (South Korea)

- Mentor Worldwide LLC (U.S.)

- Teoxane SA (Switzerland)

- Suneva Medical, Inc. (U.S.)

- Prollenium Medical Technologies Inc. (Canada)

- BioScience GmbH (Germany)

- Hyamira AG (Switzerland)

- MediBeauty Co., Ltd. (South Korea)

Latest Developments in Non-Animal Stabilized Hyaluronic Acid Fillers Market

- In September 2025, Allergan Aesthetics, an AbbVie company, launched the "Naturally You with Injectable Hyaluronic Acid Fillers" campaign. This initiative aims to educate consumers about the benefits and safety of hyaluronic acid injectable fillers, providing clear, factual information to correct misinformation and promote natural-looking outcomes. The campaign includes partnerships with healthcare providers and consumer influencers to support education and healthy, natural-looking results

- In February 2025, Evolus announced the FDA approval of Evolysse Form and Evolysse Smooth injectable hyaluronic acid gels. These products utilize Cold-X technology, which preserves the natural structure of the hyaluronic acid molecule, leading to more natural-looking and longer-lasting outcomes. The company plans to launch these products in the U.S. market in the second quarter of 2025

- In January 2025, at the International Master Course on Aging Science (IMCAS) conference, Galderma presented new data on its recently launched products, Restylane SHAYPE and Relfydess. These presentations reaffirmed Galderma's leadership in the NASHA filler category, showcasing the company's commitment to innovation and product development in the aesthetic dermatology field

- In May 2023, Allergan Aesthetics announced the U.S. FDA approval of Skinvive by JUVÉDERM to improve skin smoothness of the cheeks in adults over the age of 21. Skinvive is the first and only hyaluronic acid intradermal microdroplet injection for skin smoothness available in the U.S., with results lasting through six months with optimal treatment

- In September 2021, Galderma celebrated the 25th anniversary of Restylane®, the original non-animal stabilized hyaluronic acid filler. With over 50 million treatments worldwide, Restylane® continues to be a leading product in the NASHA filler market, demonstrating its enduring popularity and effectiveness in aesthetic treatments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.