Global Non Cardioselective Beta Blockers Market

Market Size in USD Billion

USD

3.50 Billion

USD

5.09 Billion

2025

2033

USD

3.50 Billion

USD

5.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.50 Billion | |

| USD 5.09 Billion | |

| % | |

|

Non-Cardioselective Beta Blockers Market Size

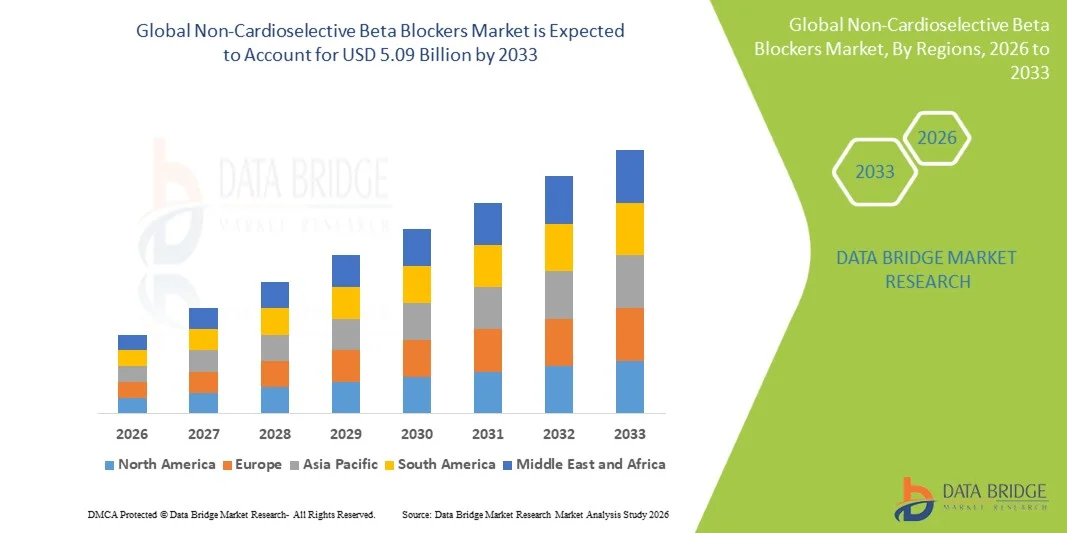

- The global non-cardioselective beta blockers market size was valued at USD 3.50 billion in 2025 and is expected to reach USD 5.09 billion by 2033, at a CAGR of4.80% during the forecast period

- The Non-Cardioselective Beta Blockers market is witnessing steady growth, driven by the rising prevalence of cardiovascular diseases, hypertension, and anxiety-related disorders, along with the increasing use of beta-blockers in the management of conditions such as angina, arrhythmias, and migraine prevention

- Furthermore, growing awareness of effective long-term cardiac management therapies, expanding access to generic formulations, and continuous advancements in pharmaceutical manufacturing are accelerating the adoption of non-cardioselective beta blockers, thereby significantly supporting the growth of the market

Non-Cardioselective Beta Blockers Market Analysis

- Non-cardioselective beta blockers, a class of cardiovascular drugs that block both β1 and β2 adrenergic receptors, are widely used in the management of hypertension, angina pectoris, arrhythmias, and other cardiovascular disorders due to their proven efficacy in reducing heart rate, myocardial oxygen demand, and blood pressure

- The market growth is primarily driven by the rising global burden of cardiovascular diseases, increasing prevalence of hypertension and stress-related conditions, and growing adoption of cost-effective generic beta blocker therapies across both developed and emerging healthcare markets

- North America dominated the non-cardioselective beta blockers market with the largest revenue share of 38.6% in 2025, supported by high disease prevalence, advanced healthcare infrastructure, strong prescription rates, and widespread availability of branded and generic cardiovascular drugs

- Asia-Pacific is expected to be the fastest growing region in the non-cardioselective beta blockers market during the forecast period, driven by increasing cardiovascular disease burden, rising geriatric population, improving healthcare access, and expanding generic drug manufacturing capabilities

- The oral segment dominated the largest market revenue share of 74.5% in 2025, driven by widespread use of tablet-based beta blockers for long-term cardiovascular management

Report Scope and Non-Cardioselective Beta Blockers Market Segmentation

|

Attributes |

Non-Cardioselective Beta Blockers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Non-Cardioselective Beta Blockers Market Trends

“Advancements in Therapeutic Applications and Clinical Optimization of Non-Cardioselective Beta Blockers”

- A significant and accelerating trend in the global non-cardioselective beta blockers market is the increasing clinical use of these agents in managing cardiovascular conditions such as hypertension, arrhythmias, angina, and heart failure. These drugs work by blocking both β1 and β2 adrenergic receptors, providing broad therapeutic effects in cardiac and non-cardiac conditions

- Non-cardioselective beta blockers such as propranolol and nadolol are widely integrated into treatment protocols for conditions including portal hypertension, migraine prophylaxis, and essential tremor

- For instance, propranolol is commonly prescribed for migraine prevention in neurology clinics and is also frequently used in patients with performance anxiety in pre-surgical or high-stress clinical settings, demonstrating its expanding therapeutic versatility

- The growing emphasis on personalized medicine is improving patient-specific drug selection and dosage optimization, enhancing treatment outcomes

- In addition, increasing clinical research on expanding therapeutic indications is broadening the use of these drugs beyond traditional cardiovascular applications

- Improved formulation strategies, including extended-release variants, are further enhancing patient adherence and treatment efficacy

- This increasing focus on optimized cardiovascular and systemic disease management is shaping the evolution of the non-cardioselective beta blockers market

Non-Cardioselective Beta Blockers Market Dynamics

Driver

“Rising Prevalence of Cardiovascular and Related Chronic Diseases”

- The increasing global burden of cardiovascular diseases is a major driver for the Non-Cardioselective Beta Blockers market

- Rising incidence of hypertension, arrhythmias, coronary artery disease, and heart failure is significantly increasing demand for effective beta-blocker therapies

- For instance, propranolol is routinely used in emergency departments and cardiology wards for acute symptom control in tachycardia and hypertension-related complications, supporting its strong clinical relevance in acute care settings

- The growing aging population, which is more susceptible to cardiac disorders, is further supporting market growth

- In addition, increasing awareness regarding early diagnosis and chronic disease management is driving higher adoption of beta-blocker therapies

- Clinical guidelines recommending beta blockers as part of combination therapy for cardiovascular conditions are further boosting demand

- Rising healthcare access in developing regions is expanding treatment uptake

- Improved diagnostic rates for hypertension and cardiac arrhythmias are also contributing to market growth

Restraint/Challenge

“Adverse Effects and Contraindications Limiting Patient Adoption”

- One of the key challenges in the Non-Cardioselective Beta Blockers market is the occurrence of adverse effects such as bronchospasm, fatigue, hypotension, and bradycardia, which can limit long-term use

- Because these drugs block β2 receptors, they may worsen conditions such as asthma and chronic obstructive pulmonary disease (COPD), restricting their use in certain patient populations

- For instance, propranolol is generally avoided in patients with asthma in respiratory clinics due to its potential to induce bronchoconstriction, leading physicians to prefer cardioselective alternatives in such cases

- The need for careful patient selection and monitoring increases treatment complexity in clinical practice

- In addition, contraindications in patients with severe peripheral vascular disease or diabetes-related complications further limit usage

- Availability of alternative cardioselective beta blockers and newer antihypertensive drug classes also creates substitution pressure

- Addressing these challenges requires improved patient stratification, safer dosing strategies, and continued development of next-generation beta-blocker therapies

Non-Cardioselective Beta Blockers Market Scope

The market is segmented on the basis of indication, target, drugs, route of administration, end-users, and distribution channel.

• By Indication

On the basis of indication, the Non-Cardioselective Beta Blockers market is segmented into angina, hypertension, heart failure, arrhythmias, and others. The hypertension segment dominated the largest market revenue share of 41.8% in 2025, driven by the rising global burden of high blood pressure linked to sedentary lifestyles, obesity, and aging populations. Non-cardioselective beta blockers are widely used in hypertension management due to their effectiveness in reducing cardiac output and controlling sympathetic activity. Increasing awareness of cardiovascular risks and routine screening programs further support early diagnosis and treatment adoption. Strong physician preference for established therapies also reinforces market dominance. In addition, growing healthcare access in emerging economies continues to expand patient reach and treatment uptake.

The heart failure segment is anticipated to witness the fastest growth rate of 8.9% from 2026 to 2033, driven by increasing prevalence of chronic heart conditions and rising hospital admissions. Non-cardioselective beta blockers such as carvedilol are widely used to improve survival rates and reduce disease progression. Expanding geriatric population and lifestyle-related cardiovascular disorders are major growth drivers. Advancements in heart failure management guidelines are further supporting adoption. Increasing use of combination therapies is also enhancing treatment effectiveness. Improved diagnostic capabilities are enabling earlier intervention. The segment is expected to grow steadily as cardiovascular disease burden continues to rise globally.

• By Target

On the basis of target, the Non-Cardioselective Beta Blockers market is segmented into beta-1 receptors, beta-2 receptors, and others. The beta-1 receptors segment dominated the largest market revenue share of 57.3% in 2025, driven by its central role in controlling heart rate and myocardial contractility. Drugs targeting beta-1 receptors are widely prescribed for cardiovascular conditions due to their proven clinical efficacy and safety profile. Strong inclusion in treatment guidelines for hypertension and arrhythmias further supports dominance. Increasing cardiovascular disease prevalence continues to drive demand for beta-1 selective and non-selective therapies. In addition, physician preference for predictable therapeutic outcomes strengthens this segment’s leadership.

The beta-2 receptors segment is expected to witness the fastest growth rate of 7.4% from 2026 to 2033, driven by expanding research into respiratory and vascular applications. Beta-2 receptor modulation is increasingly being studied for broader therapeutic benefits beyond traditional cardiovascular use. Rising interest in multi-target drug mechanisms is also supporting growth. Pharmaceutical innovation in receptor-specific modulation is improving treatment precision. Increasing clinical trials exploring novel indications are further boosting adoption. The segment is expected to expand gradually as research advances continue.

• By Drugs

On the basis of drugs, the Non-Cardioselective Beta Blockers market is segmented into propranolol, nadolol, labetalol, carvedilol, sotalol, timolol, pindolol, and others. The propranolol segment dominated the largest market revenue share of 29.6% in 2025, driven by its wide therapeutic use across hypertension, arrhythmias, anxiety, and migraine prophylaxis. Its long-standing clinical history and proven effectiveness make it a widely preferred beta blocker. Strong global availability and low cost further enhance accessibility. Increasing cardiovascular and neurological disorder prevalence continues to drive demand. In addition, inclusion in essential medicine lists supports consistent utilization across healthcare systems.

The carvedilol segment is expected to witness the fastest growth rate of 9.2% from 2026 to 2033, driven by its strong efficacy in heart failure and hypertension management. Carvedilol’s dual beta and alpha blocking action provides enhanced cardiovascular protection. Rising adoption in chronic heart failure treatment guidelines is supporting growth. Increasing geriatric population and lifestyle-related cardiac disorders are further boosting demand. Strong clinical evidence supporting mortality reduction is enhancing physician preference. Expanding hospital use and improved treatment protocols are also contributing to growth. The segment is expected to expand steadily as advanced cardiac therapies gain traction.

• By Route of Administration

On the basis of route of administration, the Non-Cardioselective Beta Blockers market is segmented into oral, parenteral, and others. The oral segment dominated the largest market revenue share of 74.5% in 2025, driven by widespread use of tablet-based beta blockers for long-term cardiovascular management. Oral administration is preferred due to convenience, affordability, and high patient compliance. Most beta blocker therapies are designed for chronic outpatient treatment, further strengthening dominance. Strong prescription rates in primary care settings support consistent demand. In addition, availability of generic oral formulations enhances accessibility across regions.

The parenteral segment is expected to witness the fastest growth rate of 8.1% from 2026 to 2033, driven by increasing use in emergency and hospital-based care settings. Injectable beta blockers are critical for acute arrhythmias and hypertensive emergencies. Rising hospitalization rates for cardiovascular complications are supporting demand. Improved critical care infrastructure is further enhancing adoption. Clinician preference for rapid-acting therapies in acute settings is boosting usage. The segment is expected to expand steadily as emergency cardiovascular care becomes more advanced.

• By End-Users

On the basis of end-users, the Non-Cardioselective Beta Blockers market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the largest market revenue share of 53.9% in 2025, driven by high patient inflow for cardiovascular emergencies and chronic disease management. Hospitals provide advanced diagnostic and monitoring facilities essential for beta blocker therapy initiation. Strong presence of cardiology departments supports treatment adoption. Government healthcare funding and reimbursement policies further reinforce hospital dominance. In addition, critical care requirements in severe cases boost hospital-based utilization.

The homecare segment is expected to witness the fastest growth rate of 8.6% from 2026 to 2033, driven by increasing preference for long-term oral therapy management outside hospital settings. Patients with chronic cardiovascular conditions increasingly prefer home-based treatment for convenience and cost savings. Growing telemedicine adoption is enabling remote monitoring of therapy. Expanding elderly population is also contributing to demand. Improved awareness of medication adherence is further supporting growth. The segment is expected to expand steadily as healthcare shifts toward decentralized care models.

• By Distribution Channel

On the basis of distribution channel, the Non-Cardioselective Beta Blockers market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 48.7% in 2025, driven by strong institutional prescribing and inpatient treatment demand. Hospitals ensure immediate availability of cardiovascular drugs for emergency and chronic care. Integration with hospital treatment protocols supports consistent usage. Government procurement systems and bulk purchasing further reinforce dominance.

The online pharmacy segment is expected to witness the fastest growth rate of 9.5% from 2026 to 2033, driven by increasing digitalization of healthcare and rising demand for convenient drug access. Online platforms enable easy prescription refills for chronic cardiovascular patients. Growing smartphone penetration and internet access are key drivers. Expansion of e-prescription systems is further supporting adoption. Post-pandemic shifts toward digital healthcare services are sustaining momentum. Improved logistics and delivery infrastructure are also enhancing accessibility. The segment is expected to expand rapidly as digital pharmacy ecosystems continue to evolve.

Non-Cardioselective Beta Blockers Market Regional Analysis

- North America dominated the non-cardioselective beta blockers market with the largest revenue share of 38.6% in 2025, supported by high disease prevalence, advanced healthcare infrastructure, strong prescription rates, and widespread availability of branded and generic cardiovascular drugs. The region benefits from well-established clinical guidelines for cardiovascular disease management, ensuring consistent adoption of beta blocker therapies across hospital and outpatient settings. In addition, strong awareness of hypertension, arrhythmias, and heart failure leads to early diagnosis and timely treatment initiation

- Patients and healthcare systems in the region benefit from broad access to affordable generic drugs, strong insurance coverage, and efficient drug distribution networks that ensure uninterrupted availability of essential cardiovascular medications. For instance, propranolol and other non-cardioselective beta blockers are routinely prescribed in both emergency and long-term care settings for managing arrhythmias and hypertension, particularly in large tertiary hospitals across the United States, reflecting their deep integration into standard treatment protocols

- This widespread adoption is further supported by high healthcare spending, strong pharmaceutical presence of both global and domestic players, and a highly developed regulatory framework that accelerates drug approval and availability, establishing non-cardioselective beta blockers as a cornerstone therapy in cardiovascular disease management

U.S. Non-Cardioselective Beta Blockers Market Insight

The U.S. non-cardioselective beta blockers market captured the largest revenue share in North America in 2025, driven by a high burden of cardiovascular diseases, advanced healthcare infrastructure, and strong adherence to evidence-based treatment guidelines. Patients increasingly rely on beta blockers as part of combination therapy for managing hypertension, arrhythmias, and post-myocardial infarction care. For instance, propranolol is commonly used in clinical practice for arrhythmia management in emergency departments and cardiology units, where rapid heart rate control is critical, reinforcing its strong clinical utility. The country also benefits from strong pharmaceutical manufacturing and distribution networks, ensuring consistent availability of both branded and generic formulations. In addition, widespread insurance coverage and structured healthcare reimbursement systems support high treatment accessibility.

Europe Non-Cardioselective Beta Blockers Market Insight

The Europe non-cardioselective beta blockers market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing prevalence of cardiovascular diseases, strong public healthcare systems, and standardized treatment protocols across countries. The region benefits from coordinated regulatory frameworks and widespread implementation of clinical guidelines for hypertension and cardiac disorder management.

Patients across Europe benefit from structured healthcare access and reimbursement systems that support affordability of essential cardiovascular drugs. For instance, non-cardioselective beta blockers such as propranolol are widely prescribed in hospital cardiology departments across countries like Germany and France for long-term management of hypertension and arrhythmias, demonstrating consistent clinical adoption. Urbanization, aging populations, and rising awareness of cardiovascular health are further contributing to steady market expansion across both Western and Eastern Europe.

U.K. Non-Cardioselective Beta Blockers Market Insight

The U.K. non-cardioselective beta blockers market is anticipated to grow at a steady CAGR during the forecast period, supported by the National Health Service (NHS), which ensures structured and universal access to cardiovascular therapies. Increasing cases of hypertension and heart disease are driving demand for beta blockers as first-line or adjunct therapies. For instance, propranolol is frequently prescribed within NHS cardiology and general practice settings for managing hypertension and anxiety-related tachycardia, reflecting its dual clinical utility in routine care pathways. Strong public healthcare funding, standardized prescribing protocols, and growing awareness of preventive cardiovascular care continue to support market growth.

Germany Non-Cardioselective Beta Blockers Market Insight

The Germany non-cardioselective beta blockers market is expected to expand at a considerable CAGR during the forecast period, driven by strong healthcare infrastructure, high cardiovascular disease burden, and emphasis on evidence-based clinical practice. Germany’s well-developed hospital systems ensure consistent adoption of beta blocker therapies for chronic disease management. For instance, propranolol and similar agents are widely used in German hospitals for long-term management of hypertension and cardiac arrhythmias, particularly in elderly patients with multiple comorbidities, highlighting their established role in cardiovascular treatment protocols. The presence of strong pharmaceutical manufacturing capabilities and widespread availability of generic formulations further supports market stability and growth.

Asia-Pacific Non-Cardioselective Beta Blockers Market Insight

The Asia-Pacific non-cardioselective beta blockers market is expected to be the fastest-growing region during the forecast period, driven by rising cardiovascular disease burden, increasing geriatric population, improving healthcare access, and expanding availability of generic drugs. Rapid urbanization and lifestyle changes are contributing to a sharp increase in hypertension and heart disease cases across the region. Patients in emerging economies are increasingly gaining access to affordable cardiovascular therapies through expanding healthcare infrastructure and government-supported programs. For instance, propranolol is increasingly used in urban tertiary hospitals across India and China for managing hypertension and tachycardia, reflecting growing adoption in both emergency and chronic care settings. In addition, growth in domestic pharmaceutical manufacturing is improving affordability and accessibility of essential beta blocker medications.

Japan Non-Cardioselective Beta Blockers Market Insight

The Japan non-cardioselective beta blockers market is gaining steady traction due to a rapidly aging population, high prevalence of cardiovascular diseases, and strong healthcare infrastructure. Japan’s healthcare system emphasizes early diagnosis and effective long-term management of chronic conditions, supporting consistent use of beta blocker therapies. For instance, non-cardioselective beta blockers such as propranolol are commonly prescribed in Japanese hospitals for arrhythmia control and hypertension management in elderly patients, reflecting their importance in geriatric cardiovascular care. Integration of advanced diagnostic systems and structured treatment pathways further enhances clinical outcomes across the country.

China Non-Cardioselective Beta Blockers Market Insight

The China non-cardioselective beta blockers market accounted for the largest market revenue share in Asia Pacific in 2025, driven by a large patient population, rising cardiovascular disease prevalence, rapid urbanization, and strong expansion of healthcare infrastructure. Government initiatives aimed at improving chronic disease management are also supporting market growth. For instance, propranolol and other beta blockers are widely used in Chinese hospitals for treating hypertension and arrhythmias, particularly in large urban healthcare centers where cardiovascular cases are rising rapidly, demonstrating strong clinical adoption. The expansion of domestic pharmaceutical manufacturing and increasing availability of low-cost generics are further strengthening market accessibility across both urban and rural regions.

Non-Cardioselective Beta Blockers Market Share

The Non-Cardioselective Beta Blockers industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- Novartis (Switzerland)

- Pfizer (U.S.)

- Merck & Co. (U.S.)

- Teva Pharmaceutical Industries (Israel)

- Viatris (U.S.)

- Sandoz (Switzerland)

- Sun Pharmaceutical Industries (India)

- Cipla (India)

- Dr. Reddy’s Laboratories (India)

- Lupin Pharmaceuticals (India)

- Aurobindo Pharma (India)

- Zydus Lifesciences (India)

- Hetero Labs (India)

- Torrent Pharmaceuticals (India)

- Glenmark Pharmaceuticals (India)

- Hikma Pharmaceuticals (U.K.)

- Fresenius Kabi (Germany)

- Apotex Inc. (Canada)

- Intas Pharmaceuticals (India)

Latest Developments in Global Non-Cardioselective Beta Blockers Market

- In March 2021, industry reports highlighted that the global non-cardioselective beta blockers market continued to grow due to rising cases of hypertension and cardiovascular diseases, with key products like propranolol and nadolol remaining widely used in clinical practice. This growth was supported by increased awareness and treatment of conditions such as angina, arrhythmias, and heart failure

- In January 2023, broader beta-blocker market analyses showed sustained demand for non-cardioselective agents, driven by their established role in treating essential tremor and migraine prophylaxis, in addition to cardiovascular indications, even as newer selective agents gained preference in some regions

- In February 2024, updated global market forecasts projected that the overall beta-blocker market (including non-cardioselective segments) would be valued at approximately USD 9.6 billion in 2023 and continue growing toward 2030, reflecting steady usage across multiple indications and broad geographic demand

- In October 2025, the World Health Organization (WHO) Model List of Essential Medicines reaffirmed the inclusion of propranolol, a first-generation non-cardioselective beta blocker, for migraine prophylaxis and cardiovascular indications, underscoring its continued global therapeutic importance

- In November 2025, market insights confirmed that propranolol remained a cornerstone non-cardioselective beta blocker with broad clinical applications and a mature lifecycle, continuing to be positioned as a cost-effective therapy for hypertension, arrhythmia, and other indications, despite limited patent-driven innovation in this segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.