Global Non Ferrous Foundry Chemicals Market

Market Size in USD Billion

USD

2.79 Billion

USD

3.86 Billion

2025

2033

USD

2.79 Billion

USD

3.86 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.79 Billion | |

| USD 3.86 Billion | |

| % | |

|

Non-ferrous foundry Chemicals Market Size

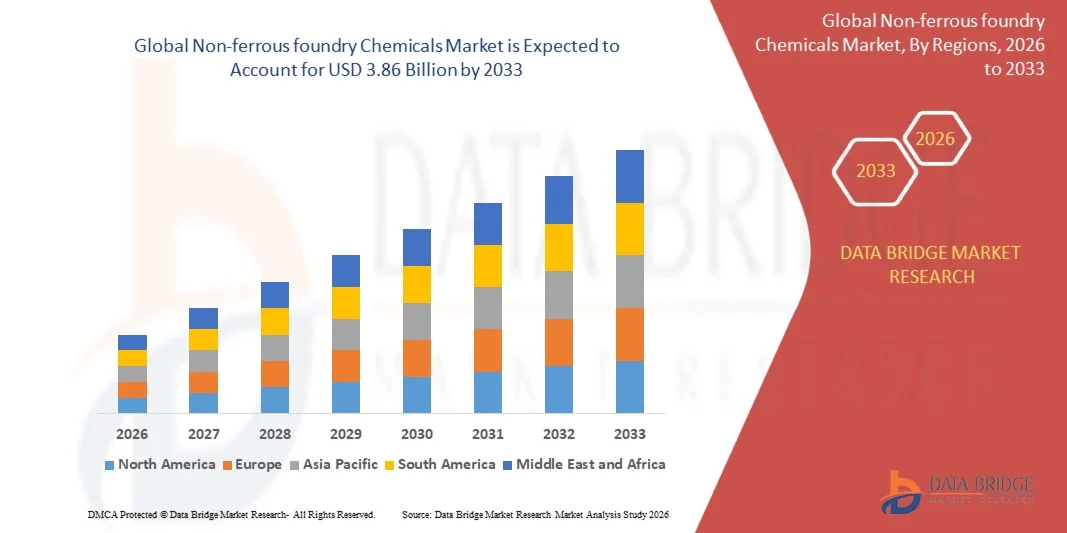

- The global non-ferrous foundry chemicals market size was valued at USD 2.79 billion in 2025 and is expected to reach USD 3.86 billion by 2033, at a CAGR of 4.17% during the forecast period

- The market growth is largely fuelled by the rising demand for high-quality non-ferrous metal castings in automotive, aerospace, and construction industries, increasing adoption of advanced casting processes, and growing focus on improving mold performance and surface finish

- Growing environmental regulations and the shift toward eco-friendly and efficient foundry chemicals also support market expansion

Non-ferrous foundry Chemicals Market Analysis

- The market is witnessing increasing demand for binders, coatings, and release agents to enhance the quality, precision, and efficiency of non-ferrous metal casting processes

- Automotive and aerospace industries are driving the adoption of advanced chemicals due to stringent requirements for lightweight, durable, and high-performance components

- North America dominated the non-ferrous foundry chemicals market with the largest revenue share of 38.75% in 2025, driven by the presence of major automotive, aerospace, and industrial manufacturers, as well as increasing adoption of advanced casting processes

- Asia-Pacific region is expected to witness the highest growth rate in the global non-ferrous foundry chemicals market, driven by rising industrial production, increasing investments in aerospace and automotive manufacturing, and government initiatives supporting advanced foundry technologies

- The Aluminum segment held the largest market revenue share in 2025, driven by its extensive use in automotive and aerospace components due to its lightweight and corrosion-resistant properties. Aluminum casting requires specialized binders, coatings, and release agents to ensure high-quality surface finish and dimensional accuracy, making chemicals for aluminum castings a key focus for foundries

Report Scope and Non-ferrous foundry Chemicals Market Segmentation

|

Attributes |

Non-ferrous foundry Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• H.C. Starck (Germany) |

|

Market Opportunities |

• Growing Demand For Lightweight And High-Performance Non-Ferrous Castings In Automotive And Aerospace Industries |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Non-ferrous foundry Chemicals Market Trends

“Rising Demand for High-Performance and Eco-Friendly Foundry Chemicals”

• The growing focus on high-quality castings and sustainable manufacturing is significantly shaping the non-ferrous foundry chemicals market, as foundries increasingly prefer chemicals that enhance mold performance, surface finish, and casting precision while being environmentally responsible. Non-ferrous foundry chemicals are gaining traction due to their ability to improve productivity, reduce defects, and support lightweight, high-performance metal components across automotive, aerospace, and industrial applications

• Increasing awareness around operational efficiency, cost reduction, and regulatory compliance has accelerated the demand for advanced binders, coatings, and release agents. Manufacturers are actively seeking chemicals that ensure consistent quality, minimize scrap, and reduce energy consumption, prompting suppliers to innovate with environmentally friendly formulations and multifunctional solutions

• Sustainability trends are influencing procurement decisions, with manufacturers emphasizing low-emission, eco-certified products and transparent sourcing. These factors help foundries differentiate their offerings, reduce environmental footprint, and comply with stringent safety and emissions regulations, thereby driving adoption of advanced non-ferrous foundry chemicals

• For instance, in 2025, H.C. Starck in Germany and Chem-Trend in the U.S. expanded their product portfolios by introducing low-emission, high-performance coatings and binders for non-ferrous metal casting. These launches addressed growing demand for precision casting in aerospace and automotive sectors, while also supporting eco-friendly operations

• While demand for non-ferrous foundry chemicals is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining functional performance for diverse casting applications. Manufacturers are also focusing on improving scalability, supply chain reliability, and developing innovative solutions that balance cost, quality, and sustainability for broader industrial adoption

Non-ferrous foundry Chemicals Market Dynamics

Driver

“Growing Demand for High-Quality and Eco-Friendly Casting Solutions”

• Rising industrialization and the increasing use of non-ferrous metals in automotive, aerospace, and construction applications are major drivers for the non-ferrous foundry chemicals market. Manufacturers are adopting advanced binders, coatings, and release agents to improve mold quality, reduce defects, and enhance the mechanical properties of cast components

• Expanding applications in die casting, sand casting, and investment casting are influencing market growth. Non-ferrous foundry chemicals help optimize mold preparation, improve surface finish, and enhance productivity while meeting environmental and regulatory requirements, enabling foundries to produce high-performance, lightweight components

• Industry players are actively promoting eco-friendly and multifunctional chemicals through product innovation, marketing campaigns, and industry certifications. These efforts are supported by increasing awareness of sustainability, efficiency, and cost reduction in casting operations, and encourage partnerships between suppliers and foundries for better performance and environmental compliance

• For instance, in 2024, Chem-Trend in the U.S. and H.C. Starck in Germany reported higher adoption of low-emission coatings and binders in automotive and aerospace foundries. This expansion followed growing demand for precision, lightweight, and environmentally responsible castings, strengthening long-term supplier relationships and market presence

• Although growing demand and sustainability trends support market growth, wider adoption depends on cost optimization, raw material availability, and consistent quality across applications. Investment in R&D, supply chain efficiency, and eco-friendly formulations will be critical for meeting global demand and maintaining a competitive edge

Restraint/Challenge

“Higher Costs and Technical Complexity Compared to Conventional Chemicals”

• The relatively higher cost of advanced and eco-friendly non-ferrous foundry chemicals compared to conventional solutions remains a key challenge, limiting adoption among price-sensitive foundries. Costs are influenced by complex production methods, high-quality raw materials, and certification compliance

• Awareness and technical know-how remain uneven, particularly in developing markets where advanced casting techniques are still emerging. Limited understanding of chemical benefits restricts adoption across certain industries, slowing market growth

• Supply chain and distribution challenges also impact market growth, as specialized chemicals require certified suppliers, proper storage, and adherence to stringent quality standards. Logistical complexities and shorter shelf life of some environmentally friendly chemicals increase operational costs

• For instance, in 2024, distributors in Southeast Asia supplying automotive and aerospace foundries reported slower uptake due to higher prices and limited awareness of functional and environmental advantages. Handling and storage requirements further restricted availability and adoption in smaller foundries

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and technical training for foundries. Collaboration with industry associations, OEMs, and certification bodies can help unlock long-term growth potential. Developing cost-competitive, multifunctional, and environmentally responsible solutions will be essential for wider adoption of non-ferrous foundry chemicals

Non-ferrous foundry Chemicals Market Scope

The market is segmented on the basis of metal type, casting process, application, and distribution channel.

• By Metal Type

On the basis of metal type, the non-ferrous foundry chemicals market is segmented into Aluminum, Copper, Zinc, Magnesium, Titanium, Nickel, Lead, and Bronze & Brass. The Aluminum segment held the largest market revenue share in 2025, driven by its extensive use in automotive and aerospace components due to its lightweight and corrosion-resistant properties. Aluminum casting requires specialized binders, coatings, and release agents to ensure high-quality surface finish and dimensional accuracy, making chemicals for aluminum castings a key focus for foundries.

The Copper segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for electrical and electronic components and industrial machinery. Copper casting chemicals enhance mold performance and reduce defects, supporting efficient manufacturing of high-conductivity components in both residential and industrial applications.

• By Casting Process

On the basis of casting process, the market is segmented into Sand Casting, Investment Casting, Die Casting, Centrifugal Casting, Permanent Mold Casting, and Continuous Casting. Sand Casting held the largest revenue share in 2025 due to its versatility, low cost, and widespread use across automotive, industrial, and construction applications. Chemicals used in sand casting improve mold strength, reduce metal penetration, and enhance surface finish, making them essential for high-quality production.

The Investment Casting segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand in aerospace, defense, and medical equipment sectors. Investment casting requires high-performance coatings and binders to achieve precise geometries and defect-free castings, increasing the adoption of specialized foundry chemicals.

• By Application

On the basis of application, the market is segmented into Automotive & Transportation, Aerospace & Defense, Industrial Machinery, Construction & Infrastructure, Electrical & Electronics, Marine & Shipbuilding, Medical Equipment, Consumer Goods, and Energy. The Automotive & Transportation segment held the largest market share in 2025, fueled by rising demand for lightweight, durable, and high-performance non-ferrous components. Chemicals in automotive casting improve surface finish, dimensional accuracy, and mold efficiency.

The Aerospace & Defense segment is expected to witness the fastest growth from 2026 to 2033, driven by stringent quality requirements and the growing use of advanced alloys. High-performance coatings, binders, and release agents are critical for producing lightweight, precise, and durable aerospace components, increasing adoption of advanced foundry chemicals.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Sales, Distributors & Suppliers, and Online Marketplaces. The Direct Sales segment held the largest revenue share in 2025, as major manufacturers prefer procuring chemicals directly from suppliers to ensure product quality, consistency, and technical support for large-scale foundry operations.

The Online Marketplaces segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing digitalization of procurement, ease of access to specialty chemicals, and the expanding presence of B2B e-commerce platforms catering to small and medium-sized foundries.

Non-ferrous foundry Chemicals Market Regional Analysis

• North America dominated the non-ferrous foundry chemicals market with the largest revenue share of 38.75% in 2025, driven by the presence of major automotive, aerospace, and industrial manufacturers, as well as increasing adoption of advanced casting processes

• Foundries in the region highly value high-performance binders, coatings, and release agents that improve mold efficiency, surface finish, and dimensional accuracy while supporting sustainable operations

• This widespread adoption is further supported by strong industrial infrastructure, high technological capabilities, and stringent regulatory standards, establishing non-ferrous foundry chemicals as a preferred solution for high-quality casting applications

U.S. Non-Ferrous Foundry Chemicals Market Insight

The U.S. non-ferrous foundry chemicals market captured the largest revenue share in 2025 within North America, fueled by extensive demand from automotive, aerospace, and electrical & electronics industries. Foundries are increasingly prioritizing the use of chemicals that enhance casting precision, reduce defects, and optimize operational efficiency. The rising trend of lightweight, high-performance alloy components, coupled with advanced mold technologies, further propels market growth. Moreover, sustainability initiatives and environmental compliance are driving adoption of eco-friendly, low-emission chemicals across the country.

Europe Non-Ferrous Foundry Chemicals Market Insight

The Europe non-ferrous foundry chemicals market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing automation in foundries, growing aerospace and defense manufacturing, and strict environmental regulations. The region’s emphasis on energy efficiency and eco-friendly production processes is encouraging adoption of advanced binders, coatings, and release agents. European foundries are integrating these chemicals into both new production lines and refurbishment projects, supporting high-quality casting outcomes.

U.K. Non-Ferrous Foundry Chemicals Market Insight

The U.K. non-ferrous foundry chemicals market is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising demand for precision cast components in automotive and aerospace sectors. In addition, regulatory compliance and sustainability considerations are encouraging foundries to use environmentally responsible chemicals. The U.K.’s strong industrial base and adoption of connected foundry technologies are expected to continue supporting market expansion.

Germany Non-Ferrous Foundry Chemicals Market Insight

The Germany non-ferrous foundry chemicals market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing focus on lightweight alloys, digitalized foundry operations, and eco-conscious manufacturing practices. Germany’s advanced industrial infrastructure, combined with its emphasis on innovation and sustainability, promotes adoption of high-performance binders, coatings, and release agents. Integration with automated and precision casting systems is becoming increasingly prevalent, aligning with local industry standards and quality expectations.

Asia-Pacific Non-Ferrous Foundry Chemicals Market Insight

The Asia-Pacific non-ferrous foundry chemicals market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, urbanization, and growing demand for automotive, aerospace, and construction components in countries such as China, Japan, and India. Government initiatives promoting advanced manufacturing and eco-friendly production are supporting adoption of high-performance foundry chemicals. Furthermore, as APAC emerges as a manufacturing hub for alloys and casting systems, accessibility and affordability of non-ferrous foundry chemicals are increasing for small and medium-sized foundries.

Japan Non-Ferrous Foundry Chemicals Market Insight

The Japan non-ferrous foundry chemicals market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced industrial technology, focus on precision engineering, and strong aerospace and automotive sectors. Japanese foundries are increasingly adopting high-performance binders, coatings, and release agents to improve mold quality and casting efficiency. In addition, automation and integration with digital foundry technologies are boosting market growth, while sustainability initiatives drive demand for eco-friendly chemical solutions.

China Non-Ferrous Foundry Chemicals Market Insight

The China non-ferrous foundry chemicals market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive, aerospace, and industrial manufacturing sectors. Rapid urbanization, increasing adoption of lightweight alloys, and high rates of technological integration are key drivers. The push towards smart factories, coupled with availability of affordable and high-quality chemicals from domestic manufacturers, is propelling growth in both small-scale and large industrial foundries.

Non-ferrous foundry Chemicals Market Share

The Non-ferrous foundry Chemicals industry is primarily led by well-established companies, including:

• H.C. Starck (Germany)

• Chem-Trend (U.S.)

• ASK Chemicals (Germany)

• BASF SE (Germany)

• Clariant AG (Switzerland)

• Nouryon (Netherlands)

• Zibo Hengtong Chemical Co., Ltd. (China)

• Foseco International Ltd. (U.K.)

• Fushun Jinlong Foundry Chemicals Co., Ltd. (China)

• Hangzhou Newtech Foundry Materials Co., Ltd. (China)

• Imerys Group (France)

• Solvay S.A. (Belgium)

• Chryso Group (France)

• Schenck Process (Germany)

• Dongyue Chemical Co., Ltd. (China)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Non Ferrous Foundry Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Non Ferrous Foundry Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Non Ferrous Foundry Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.