Global Non Radiographic Axial Spondyloarthritis Therapeutics Market

Market Size in USD Billion

USD

7.80 Billion

USD

12.41 Billion

2025

2033

USD

7.80 Billion

USD

12.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.80 Billion | |

| USD 12.41 Billion | |

| % | |

|

Non-Radiographic Axial Spondyloarthritis Therapeutics Market Size

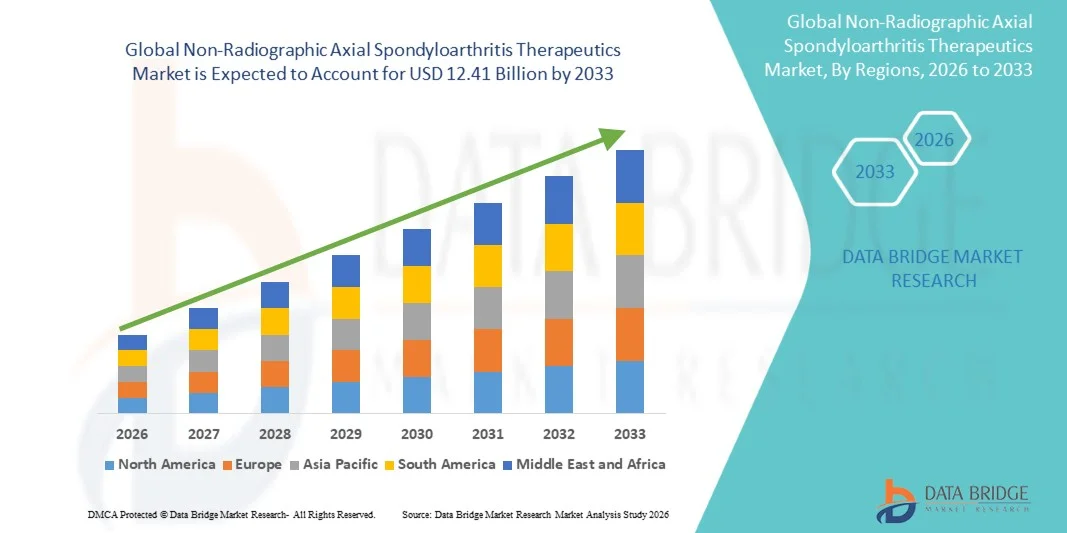

- The Non-Radiographic Axial Spondyloarthritis Therapeutics Market size was valued at USD 7.8 Billion in 2025and is expected to reach USD 12.41 Billion by 2033, at a CAGR of 7.2% during the forecast period

- The market growth is primarily driven by the rising prevalence and improved diagnosis of non-radiographic axial spondyloarthritis, supported by increased awareness among clinicians and patients. Advances in imaging techniques such as MRI have enabled earlier detection of inflammatory back pain, expanding the diagnosed patient pool eligible for treatment.

- Strong expansion of biologic and targeted therapies is significantly accelerating market development. The increasing adoption of TNF inhibitors, IL-17 inhibitors, and emerging JAK inhibitors has improved treatment outcomes, particularly for patients who do not respond adequately to conventional NSAIDs.

Non-Radiographic Axial Spondyloarthritis Therapeutics Market Analysis

- The Global Non-Radiographic Axial Spondyloarthritis (nr-axSpA) Therapeutics market is witnessing steady growth as increasing disease awareness, improved diagnostic practices, and earlier detection of inflammatory back pain are expanding the treated patient population. Rising prevalence of nr-axSpA and growing clinical recognition of non-radiographic cases are driving higher demand for effective long-term treatment options. The increasing adoption of advanced biologics and targeted therapies is further strengthening market expansion.

- These advancements are reshaping the treatment landscape through rapid development of novel immunomodulatory drugs, including TNF inhibitors, IL-17 inhibitors, and emerging JAK inhibitors. Strong investment in clinical research, coupled with expanding drug pipelines and improved patient access to advanced therapies, is enhancing treatment outcomes and supporting more personalized disease management strategies across healthcare systems.

- North America is expected to dominate the Global nr-axSpA Therapeutics market with the largest revenue share of 41.79% in 2026, supported by strong healthcare infrastructure, early adoption of advanced biologics, and high diagnosis rates. The presence of leading pharmaceutical companies and increased access to innovative therapies continue to reinforce the region’s market leadership.

- Asia-Pacific is projected to be the fastest-growing market, registering a CAGR of 8.5%, driven by improving healthcare infrastructure, rising awareness of inflammatory rheumatic diseases, and increasing access to biologic therapies. Expanding healthcare investments and government initiatives to enhance chronic disease management in countries such as Brazil and Argentina are further accelerating regional growth.

- In 2025, the Medication segment dominated the market with a 78.65% share, reflecting strong demand for biologic therapies and targeted treatment options such as TNF inhibitors, IL-17 inhibitors, and JAK inhibitors. These medications play a critical role in reducing inflammation, managing disease progression, and improving long-term patient outcomes in non-radiographic axial spondyloarthritis care.

Report Scope and Non-Radiographic Axial Spondyloarthritis Therapeutics Market Segmentation

|

Attributes |

Non-Radiographic Axial Spondyloarthritis Therapeutics Market Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Global North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novartis AG (Switzerland) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · UCB Group (Belgium) · Eli Lilly and Company (U.S.) · Biogen (U.S.) · Johnson & Johnson (U.S.) · Amgen Inc. (U.S.) · Bristol-Myers Squibb (U.S.) · Merck KGaA (Germany) · Sanofi (France) · F. Hoffmann-La Roche Ltd (Switzerland) · Boehringer Ingelheim (Germany) · Astellas Pharma Inc. (Japan) · Gedeon Richter Plc. (Hungary) · Sun Pharmaceutical Industries Ltd (India) · Lupin Limited (India) · Dr. Reddy’s Laboratories Limited (India) · Teva Pharmaceutical Industries Ltd (Israel) · Zydus Group (India) · Viatris Inc. (U.S.) · Fresenius Kabi (Germany) · Kyowa Kirin Co., Ltd (Japan) · Celltrion Inc. (South Korea) · Torrent Pharmaceuticals Ltd (India) · Samsung Bioepis (South Korea) · Alkem Laboratories (India) · Cipla (India) · Sandoz (Switzerland) · Takeda Pharmaceutical Company Limited (Japan) · Biocad (Russia) |

|

Market Opportunities |

· Development of targeted therapies and novel biologics with improved efficacy and safety profiles · Expansion of biosimilars market reducing treatment costs and improving accessibility · Growing focus on personalized medicine and precision therapeutics |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Non-Radiographic Axial Spondyloarthritis Therapeutics MarketTrends

“Rising demand for advanced and targeted therapeutic solutions for inflammatory spine disorders”

- The demand for advanced therapeutic options for non-radiographic axial spondyloarthritis is increasing globally as patients, physicians, and healthcare systems seek more effective long-term disease control beyond conventional NSAIDs. The introduction and growing adoption of biologics, including TNF inhibitors and IL-17 inhibitors, along with targeted synthetic DMARDs, is significantly improving pain management, inflammation control, and overall quality of life in patients with nr-axSpA.

- Factors such as rising disease awareness, improved diagnostic capabilities (including MRI-based detection of early sacroiliitis), evolving clinical guidelines, and increasing recognition of axial spondyloarthritis as a spectrum disorder are driving earlier diagnosis and wider treatment adoption across both developed and emerging healthcare markets.

- As patients with nr-axSpA face chronic pain, mobility limitations, and risk of disease progression, the demand for long-term, safe, and effective treatment regimens has grown substantially. This has encouraged the use of advanced biologic therapies that not only reduce symptoms but also help prevent structural damage and improve functional outcomes.

- Increasing burden of autoimmune and inflammatory diseases, along with genetic predisposition factors such as HLA-B27 association, is contributing to a growing patient pool requiring continuous management. Coupled with delayed diagnosis in many regions, this is further increasing the need for advanced and accessible therapeutic options.

- Additionally, the growing adoption of biosimilars and next-generation biologic therapies represents a major opportunity for the Non-Radiographic Axial Spondyloarthritis Therapeutics Market. As healthcare systems aim to improve affordability and expand patient access to high-cost biologics, the availability of cost-effective biosimilars, combined with advancements in precision medicine and immunology research, is expected to further accelerate market growth

Non-Radiographic Axial Spondyloarthritis Therapeutics Market trends

Driver

“Increasing prevalence of non-radiographic axial spondyloarthritis and improved disease awareness”

- The expansion of the Global Non-Radiographic Axial Spondyloarthritis (nr-axSpA) Therapeutics Market is strongly driven by the increasing recognition of disease prevalence and a substantial rise in awareness among healthcare providers and patients.

- Historically underdiagnosed due to the absence of definitive radiographic damage, nr-axSpA is now being increasingly identified through improved clinical classification frameworks and the broader adoption of advanced imaging techniques. International rheumatology bodies and public health organizations have intensified efforts to promote early identification of inflammatory back pain and axial spondyloarthritis spectrum disorders, thereby reducing diagnostic delays.

- Concurrently, patient advocacy initiatives and educational campaigns have enhanced disease visibility, encouraging earlier healthcare-seeking behavior and physician intervention. These developments are expanding the diagnosed patient pool and accelerating the uptake of targeted therapies, positioning disease awareness and prevalence growth as a fundamental driver of market demand.

- In May 2023, the European Alliance of Associations for Rheumatology highlighted new research and clinical insights on axial spondyloarthritis at its annual congress, emphasizing improved disease understanding and the importance of early identification strategies, which support increased diagnosis of non-radiographic cases.

- In 2023, the Assessment of SpondyloArthritis international Society in collaboration with EULAR released updated management recommendations for axial spondyloarthritis, reinforcing structured diagnostic and treatment pathways that enhance early detection and awareness among clinicians.

- Growing awareness of non-radiographic axial spondyloarthritis (nr-axSpA), supported by updated clinical guidelines, educational initiatives, and enhanced physician training, is leading to earlier diagnosis and expanding the eligible treatment population worldwide.

- Increasing recognition of disease prevalence, combined with improved diagnostic frameworks and greater adoption of advanced imaging technologies, is driving demand for targeted therapeutics and contributing significantly to the growth of the Global Non-Radiographic Axial Spondyloarthritis (nr-axSpA) Therapeutics Market.

Restraint/Challenge

“High cost of biologic therapies limiting patient access in low- and middle-income regions”

- The Global Non-Radiographic Axial Spondyloarthritis (nr-axSpA) Therapeutics Market is significantly constrained by the high cost of biologic therapies, which continues to limit patient access, particularly across low- and middle-income regions. Biologic agents, including tumor necrosis factor inhibitors and interleukin-17 inhibitors, involve complex development and manufacturing processes that contribute to elevated pricing structures.

- This cost burden poses a substantial challenge for healthcare systems with limited financial resources and for patients lacking comprehensive reimbursement coverage. In many emerging economies, constrained healthcare budgets and fragmented insurance frameworks further restrict access to these advanced therapies, resulting in delayed treatment initiation and suboptimal disease management.

- Despite their proven clinical efficacy, affordability barriers remain a critical impediment to widespread adoption, thereby moderating the overall growth potential of the nr-axSpA therapeutics market.

- In February 2025, the World Health Organization reported that biologic medicines, although highly effective for chronic diseases, remain inaccessible to many patients globally due to their high costs, particularly in low- and middle-income countries with constrained healthcare budgets.

- In November 2024, the Access to Medicine Foundation highlighted that significant gaps persist in access to essential medicines in low-income countries, noting that affordability and limited coverage of advanced therapies continue to restrict patient reach despite industry initiatives

- The high cost of biologic therapies and limited reimbursement coverage continue to restrict patient access, particularly in emerging and resource-constrained healthcare markets, thereby hindering treatment adoption.

- Persistent affordability challenges and disparities in healthcare funding are expected to remain key barriers to the widespread utilization of advanced nr-axSpA therapies, moderating overall market growth.

Non-Radiographic Axial Spondyloarthritis Therapeutics Market Scope

Non-Radiographic Axial Spondyloarthritis Therapeutics Market is categorized into five notable segments which are based on treatment type, drug, route of administration, end user, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Non-Radiographic Axial Spondyloarthritis Therapeutics Market is segmented into Medication, Surgery, Physical Therapy, and Others. In 2026, Medication is anticipated to dominate the market with 78.77% market share, driven by its critical role in providing first-line disease control, reducing inflammation, managing chronic pain, and its widespread use of biologics and targeted DMARD therapies as standard care for nr-axSpA patients.

The Medication segment in the market is expected to grow the fastest with a CAGR of 7.4% from 2026 to 2033, supported by increasing adoption of biologic therapies such as TNF and IL-17 inhibitors, rising diagnosis rates, and continuous advancements in targeted treatment options that improve long-term patient outcomes and delay disease progression.

- By drug type

On the basis of drug type, the Non-Radiographic Axial Spondyloarthritis Therapeutics Market is segmented into Adalimumab, Secukinumab, Etanercept, Ixekizumab, Upadacitinib, Certolizumab Pegol, Golimumab, Infliximab, Tofacitinib, and Others. In 2026, Adalimumab is anticipated to dominate the market with 27.34% market share, driven by its strong clinical efficacy, widespread physician preference as a first-line biologic TNF inhibitor, and extensive real-world evidence supporting its long-term effectiveness in reducing inflammation and disease progression in nr-axSpA patients.

The Upadacitinib segment in the market is expected to grow the fastest with a CAGR of 8.6% from 2026 to 2033, driven by increasing adoption of oral targeted synthetic DMARDs, strong efficacy in JAK pathway inhibition, improved patient convenience compared to injectable biologics, and rising preference for advanced therapies offering rapid symptom relief and flexible administration.

- By Route of Administration

On the basis of route of administration, the Non-Radiographic Axial Spondyloarthritis Therapeutics Market is segmented into Subcutaneous, Oral, Intravenous, and Others. In 2026, the Subcutaneous segment is anticipated to dominate the market with 48.02% market share, driven by its widespread use in biologic therapies, improved patient compliance through self-administration, and its effectiveness in delivering long-acting targeted treatments for chronic inflammatory conditions like nr-axSpA.

The Oral segment in the market is expected to grow the fastest with a CAGR of 8.2% from 2026 to 2033, supported by increasing adoption of oral targeted synthetic DMARDs such as JAK inhibitors, growing patient preference for non-invasive treatment options, and advancements in oral drug formulations that offer greater convenience, faster onset of action, and improved long-term adherence.

- By End User

On the basis of end user, the Non-Radiographic Axial Spondyloarthritis Therapeutics Market is segmented into Specialty Clinics, Homecare, Hospitals, Pharmacy & Retailers, and Others. In 2026, Specialty Clinics are anticipated to dominate the market with 31.72% market share, driven by the growing preference for specialized rheumatology care, improved access to expert diagnosis and biologic therapy management, and the rising role of these clinics in providing targeted, long-term treatment for chronic inflammatory conditions like nr-axSpA.

The Homecare segment in the market is expected to grow the fastest with a CAGR of 8.0% from 2026 to 2033, supported by increasing adoption of self-administered biologic therapies, rising demand for patient-centric and convenient treatment settings, and advancements in home-based monitoring and telehealth services that enable continuous disease management outside traditional healthcare facilities.

- By Distribution Channel

On the basis of distribution channel, the Non-Radiographic Axial Spondyloarthritis Therapeutics Market is segmented into Hospital Pharmacy, Retail Pharmacy, Direct Tender, Online Pharmacy, and Others. In 2026, the Hospital Pharmacy segment is anticipated to dominate the market with 35.73% market share, driven by the high reliance on hospital-based dispensing for biologics and advanced therapies, physician-led treatment initiation, and the strong role of hospitals in managing moderate to severe nr-axSpA cases requiring specialized care and monitoring.

The Online Pharmacy segment in the market is expected to grow the fastest with a CAGR of 8.0% from 2026 to 2033, supported by increasing digitalization of healthcare services, rising adoption of e-pharmacy platforms for medication access, improved convenience for chronic disease patients requiring long-term therapy, and growing integration of telemedicine with prescription fulfillment systems.

Global Non-Radiographic Axial Spondyloarthritis Therapeutics Market Regional Analysis

- North America dominated the Non-Radiographic Axial Spondyloarthritis Therapeutics Market with the largest revenue share of 41.88% in 2025.

- The region is supported by a well-established healthcare infrastructure, high disease awareness, and early adoption of advanced biologic therapies and targeted synthetic DMARDs. Strong presence of leading pharmaceutical companies, favorable reimbursement frameworks, and extensive clinical research activities in autoimmune and inflammatory diseases are further strengthening market penetration and improving patient access to innovative treatment options.

- Additionally, the region benefits from increasing diagnosis rates of nr-axSpA, widespread availability of rheumatology specialists, and continuous introduction of novel biologics, which collectively enhance treatment outcomes and support sustained market growth..

U.S. Non-Radiographic Axial Spondyloarthritis therapeutics Insight

The U.S. Non-Radiographic Axial Spondyloarthritis therapeutics market accounted for the largest revenue share in 2025, driven by strong disease awareness, early diagnosis rates, and widespread adoption of advanced biologic therapies and targeted synthetic DMARDs. Increasing utilization of TNF inhibitors and IL-17 inhibitors across rheumatology clinics, along with strong reimbursement support and established healthcare infrastructure, is further fueling market growth. In addition, the presence of leading pharmaceutical companies, robust clinical trial activity, and advanced research capabilities in autoimmune disorders is supporting continuous innovation and expanding treatment access across diverse patient populations.

Europe Non-Radiographic Axial Spondyloarthritis Therapeutics Market Insight

The Europe Non-Radiographic Axial Spondyloarthritis therapeutics market is projected to expand at a substantial CAGR throughout the forecast period, driven by rising prevalence of autoimmune disorders, increasing awareness of early-stage axial spondyloarthritis, and growing adoption of biologic and biosimilar therapies. Investments in healthcare modernization, digital diagnostics, and value-based care frameworks are further supporting market growth. The region is witnessing increased use of advanced biologics, improved MRI-based diagnosis, and expanding access to rheumatology care, with healthcare systems emphasizing cost-effective treatment strategies and improved long-term disease management.

Germany Non-Radiographic Axial Spondyloarthritis Therapeutics Market Insight

The Germany Non-Radiographic Axial Spondyloarthritis therapeutics market is expected to grow at a notable CAGR during the forecast period, driven by strong demand from specialized rheumatology centers, increasing diagnosis rates, and rising adoption of advanced biologic therapies. Growing investments in healthcare infrastructure modernization and clinical research activities are further supporting market expansion. Major hospitals and specialty clinics are increasingly utilizing targeted biologics and precision medicine approaches, encouraging pharmaceutical companies to strengthen local partnerships and expand access to innovative treatment options.

Asia Pacific Non-Radiographic Axial Spondyloarthritis Therapeutics Market Insight

The Asia Pacific Non-Radiographic Axial Spondyloarthritis therapeutics market is expected to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of autoimmune diseases, improving diagnostic capabilities, and expanding access to advanced biologic therapies across emerging economies. Increasing healthcare investments, growing patient pool, and gradual adoption of biosimilars are accelerating market penetration. In addition, expanding healthcare infrastructure, rising rheumatology specialization, and increasing affordability of targeted therapies are supporting wider treatment adoption across both urban and semi-urban populations.

China Non-Radiographic Axial Spondyloarthritis Therapeutics Market Insight

The China Non-Radiographic Axial Spondyloarthritis therapeutics market is experiencing steady growth due to increasing healthcare modernization, rising awareness of inflammatory spine disorders, and expanding adoption of biologics and biosimilars. Growing investment in domestic pharmaceutical development, improved diagnostic infrastructure, and supportive government healthcare initiatives are driving market expansion. Increasing availability of advanced treatment options across hospitals and specialty clinics, along with a strong focus on early diagnosis and chronic disease management, continues to support widespread adoption of nr-axSpA therapeutics across the country.

Non-Radiographic Axial Spondyloarthritis Therapeutics Market Share

The non-radiographic axial spondyloarthritis therapeutics market is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- UCB Group (Belgium)

- Eli Lilly and Company (U.S.)

- Biogen (U.S.)

- Johnson & Johnson (U.S.)

- Amgen Inc. (U.S.)

- Bristol-Myers Squibb (U.S.)

- Merck KGaA (Germany)

- Sanofi (France)

- Hoffmann-La Roche Ltd (Switzerland)

- Boehringer Ingelheim (Germany)

- Astellas Pharma Inc. (Japan)

- Gedeon Richter Plc. (Hungary)

- Sun Pharmaceutical Industries Ltd (India)

- Lupin Limited (India)

- Reddy’s Laboratories Limited (India)

- Teva Pharmaceutical Industries Ltd (Israel)

- Zydus Group (India)

- Viatris Inc. (U.S.)

- Fresenius Kabi (Germany)

- Kyowa Kirin Co., Ltd (Japan)

- Celltrion Inc. (South Korea)

- Torrent Pharmaceuticals Ltd (India)

- Samsung Bioepis (South Korea)

- Alkem Laboratories (India)

- Cipla (India)

- Sandoz (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Biocad (Russia)

Latest Developments in Non-Radiographic Axial Spondyloarthritis Therapeutics Market

- In April 2026 – The company received European Commission approval for Rhapsido, the first oral targeted treatment for chronic spontaneous urticaria, marking a major dermatology innovation.

- In November 2025, Pfizer shareholders approved the acquisition of Metsera, giving Pfizer access to a pipeline of 2026 Acquisition next-generation obesity and cardiometabolic therapies. This strengthens its long term growth by diversifying beyond declining COVID related revenues and addressing upcoming patent expiries The deal is expected to boost Pfizer’s competitive position in the rapidly expanding global obesity drug market (projected to reach ~USD150B), intensifying competition with players like Novo Nordisk and Eli Lilly while potentially driving future revenue and market share gains if pipeline drugs succeed.

- In April 2026 – AbbVie announced an update on its Biologics License Application (BLA) for TrenibotulinumtoxinE (TrenibotE) in the U.S. The FDA issued a Complete Response Letter due to manufacturing-related issues, but did not raise concerns about safety or effectiveness. AbbVie stated it will address the FDA’s feedback and resubmit the application for review.

- In April 2026: UCB partnered with a UK university to develop “digital antibodies” using artificial intelligence, aiming to 2026 2025 Partnership Expansion accelerate drug discovery and improve treatment precision. This collaboration reflects the company’s growing focus on advanced technologies in biopharma innovation.

- In April 2026 – Eli Lilly announced the acquisition of Ajax Therapeutics for up to USD2.3 billion, strengthening its oncology pipeline with a novel treatment for blood cancer (myelofibrosis)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET END USER COVERAGE GRID

2.1 VENDOR SHARE ANALYSIS

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES

4.1.1 THREAT OF NEW ENTRANTS

4.1.2 THREAT OF SUBSTITUTES

4.1.3 BARGAINING POWER OF BUYERS

4.1.4 BARGAINING POWER OF SUPPLIERS

4.1.5 INDUSTRY RIVALRY

4.2 BRAND OUTLOOK

4.3 COST ANALYSIS BREAKDOWN

4.3.1 DRUG ACQUISITION COSTS AND PRICING DYNAMICS

4.3.2 MANUFACTURING AND BIOLOGICS PRODUCTION COSTS

4.3.3 RESEARCH AND DEVELOPMENT EXPENDITURE

4.3.4 DISTRIBUTION, LOGISTICS, AND COLD CHAIN MANAGEMENT

4.3.5 ADMINISTRATION AND HEALTHCARE SYSTEM COSTS

4.3.6 IMPACT OF BIOSIMILARS AND COMPETITIVE PRICING

4.3.7 REIMBURSEMENT FRAMEWORKS AND PATIENT ACCESS

4.3.8 MARKET DEVELOPMENTS INFLUENCING COST STRUCTURES

4.3.9 CONCLUSION

4.4 INDUSTRY ECOSYSTEM ANALYSIS

4.4.1 OVERVIEW OF THE INDUSTRY ECOSYSTEM STRUCTURE

4.4.2 DRUG DISCOVERY AND TRANSLATIONAL RESEARCH ECOSYSTEM

4.4.3 CLINICAL DEVELOPMENT AND TRIAL INFRASTRUCTURE

4.4.4 MANUFACTURING AND BIOPHARMACEUTICAL SUPPLY CHAIN ECOSYSTEM

4.4.5 REGULATORY AND HEALTH AUTHORITY ECOSYSTEM

4.4.6 HEALTHCARE DELIVERY AND PRESCRIBING ECOSYSTEM

4.4.7 DISTRIBUTION AND PHARMACEUTICAL ACCESS CHANNELS

4.4.8 PATIENT ADVOCACY AND DISEASE AWARENESS ECOSYSTEM

4.4.9 PRICING AND MARKET ACCESS ECOSYSTEM

4.5 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.5.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.5.1.1 JOINT VENTURES

4.5.1.2 MERGERS AND ACQUISITIONS

4.5.1.3 LICENSING AND PARTNERSHIP

4.5.1.4 TECHNOLOGY COLLABORATIONS

4.5.1.5 STRATEGIC DIVESTMENTS

4.5.2 NUMBER OF PRODUCTS IN DEVELOPMENT

4.5.3 STAGE OF DEVELOPMENT

4.5.4 TIMELINES AND MILESTONES

4.5.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.5.6 RISK ASSESSMENT AND MITIGATION

4.5.7 FUTURE OUTLOOK

4.6 PATENT ANALYSIS

4.6.1 PATENT QUALITY AND STRENGTH

4.6.2 COUNTRY PATENT LANDSCAPE.

4.6.3 IP STRATEGY AND MANAGEMENT

4.6.4 LICENSING AND COLLABORATION

4.7 PRICING ANALYSIS

4.7.1 PREMIUM PRICING STRUCTURE DOMINATED BY BIOLOGICS AND TARGETED THERAPIES

4.7.2 BIOLOGICS AS THE KEY REVENUE AND PRICE REALIZATION SEGMENT

4.7.3 LOW-COST VOLUME SEGMENT LED BY NSAIDS AND CONVENTIONAL THERAPIES

4.7.4 REGIONAL PRICING DISPARITY ACROSS GLOBAL MARKETS

4.7.5 BIOSIMILARS DRIVING DOWNWARD PRICE CORRECTION

4.7.6 HEALTH ECONOMIC BURDEN AND PAYER-DRIVEN PRICING PRESSURE

4.8 PROFIT MARGINS SCENARIO

4.8.1 OVERVIEW OF PROFIT MARGIN DYNAMICS

4.8.2 REVENUE STRUCTURE AND PRICING POWER IN BIOLOGIC THERAPIES

4.8.3 COST STRUCTURE AND MANUFACTURING ECONOMICS

4.8.4 IMPACT OF BIOSIMILARS AND COMPETITIVE EROSION

4.8.5 REGIONAL REIMBURSEMENT AND MARKET ACCESS INFLUENCE

4.8.6 PIPELINE INNOVATION AND MARGIN EXPANSION POTENTIAL

4.8.7 REGULATORY APPROVALS AND MARKET EXPANSION CONTEXT

4.8.8 COMPETITIVE AND CLINICAL ADOPTION DYNAMICS

4.8.9 INNOVATION-DRIVEN MARGIN SUSTAINABILITY

4.8.10 CONCLUSION

4.9 RAW MATERIAL COVERAGE

4.9.1 OVERVIEW OF RAW MATERIAL LANDSCAPE

4.9.2 BIOLOGIC ACTIVE INGREDIENT PRODUCTION INPUTS

4.9.3 CELL CULTURE MEDIA AND UPSTREAM PROCESSING MATERIALS

4.9.4 CHROMATOGRAPHY AND PURIFICATION MATERIALS

4.9.5 FORMULATION EXCIPIENTS AND STABILIZATION AGENTS

4.9.6 PRIMARY PACKAGING MATERIALS

4.9.7 SECONDARY PACKAGING AND COLD CHAIN LOGISTICS MATERIALS

4.9.8 QUALITY STANDARDS AND REGULATORY MATERIAL COMPLIANCE

4.9.9 SUPPLY CHAIN CONSTRAINTS AND RISK FACTORS

4.9.10 EMERGING TRENDS IN RAW MATERIAL INNOVATION

4.1 TECHNOLOGICAL ADVANCEMENTS

4.10.1 EVOLUTION OF TARGETED BIOLOGIC THERAPIES

4.10.2 EMERGENCE OF IL-17 INHIBITORS AND NOVEL MECHANISTIC PATHWAYS

4.10.3 ADVANCEMENT OF ORAL SMALL MOLECULE THERAPIES

4.10.4 BIOMARKER-DRIVEN DIAGNOSIS AND TREATMENT OPTIMIZATION

4.10.5 DIGITAL HEALTH INTEGRATION AND REMOTE MONITORING

4.10.6 ADVANCES IN DRUG DELIVERY SYSTEMS

4.10.7 ONGOING RESEARCH IN NEXT-GENERATION THERAPEUTICS

4.10.8 INTEGRATION OF PRECISION MEDICINE APPROACHES

4.10.9 CONCLUSION

4.11 VALUE CHAIN ANALYSIS

4.11.1 RAW MATERIALS AND ACTIVE PHARMACEUTICAL INGREDIENTS

4.11.2 DRUG DISCOVERY AND PRECLINICAL DEVELOPMENT

4.11.3 MANUFACTURING AND BIOPROCESSING

4.11.4 PROCESSING, FILL-FINISH AND STERILIZATION

4.11.5 PACKAGING AND LABELING

4.11.6 DISTRIBUTION AND LOGISTICS

4.11.7 CONCLUSION

4.12 VENDOR SELECTION CRITERIA

4.12.1 CLINICAL EFFICACY AND EVIDENCE-BASED DIFFERENTIATION

4.12.2 MECHANISM OF ACTION AND PORTFOLIO BREADTH

4.12.3 REGULATORY COMPLIANCE AND GLOBAL MARKET ACCESS

4.12.4 PRICING STRATEGY AND REIMBURSEMENT LANDSCAPE

4.12.5 MANUFACTURING CAPABILITIES AND SUPPLY CHAIN RELIABILITY

4.12.6 STRATEGIC COLLABORATIONS AND INNOVATION CAPACITY

4.12.7 REAL-WORLD EVIDENCE AND POST-MARKETING SURVEILLANCE

4.12.8 MARKET PRESENCE AND PHYSICIAN ENGAGEMENT

4.12.9 CONCLUSION

5 TARIFFS & IMPACT ON THE MARKET

5.1 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION VERSUS IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL PROCUREMENT

5.4.2 MANUFACTURING AND PRODUCTION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICE PITCHING AND MARKET POSITION

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

6 REGULATORY FRAMEWORK AND APPROVAL PATHWAYS

6.1 OVERVIEW

6.2 REGIONAL REGULATORY AND REIMBURSEMENT LANDSCAPES

6.3 PRICING, HEALTH TECHNOLOGY ASSESSMENT AND COVERAGE

6.4 POST-MARKETING SURVEILLANCE AND PHARMACOVIGILANCE

7 MARKET OVERVIEW

7.1 DRIVER

7.1.1 INCREASING PREVALENCE OF NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS AND IMPROVED DISEASE AWARENESS

7.1.2 GROWING ADOPTION OF BIOLOGICS SUCH AS TNF INHIBITORS AND IL-17 INHIBITORS FOR EARLY-STAGE TREATMENT

7.1.3 ADVANCEMENTS IN DIAGNOSTIC TECHNIQUES ENABLING EARLIER AND MORE ACCURATE DETECTION

7.1.4 RISING HEALTHCARE EXPENDITURE AND IMPROVED ACCESS TO SPECIALTY CARE IN EMERGING MARKETS

7.2 RESTRAINT

7.2.1 HIGH COST OF BIOLOGIC THERAPIES LIMITING PATIENT ACCESS IN LOW- AND MIDDLE-INCOME REGIONS

7.2.2 STRINGENT REGULATORY APPROVAL PROCESSES FOR NOVEL THERAPEUTICS DELAYING MARKET ENTRY

7.3 OPPORTUNITIES

7.3.1 DEVELOPMENT OF TARGETED THERAPIES AND NOVEL BIOLOGICS WITH IMPROVED EFFICACY AND SAFETY PROFILES

7.3.2 EXPANSION OF BIOSIMILARS MARKET REDUCING TREATMENT COSTS AND IMPROVING ACCESSIBILITY

7.3.3 GROWING FOCUS ON PERSONALIZED MEDICINE AND PRECISION THERAPEUTICS

7.4 CHALLENGES

7.4.1 COMPLEXITY IN DISEASE DIAGNOSIS DUE TO LACK OF RADIOGRAPHIC EVIDENCE IN EARLY STAGES

7.4.2 PATIENT ADHERENCE ISSUES DUE TO CHRONIC NATURE OF TREATMENT

8 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE

8.1 OVERVIEW

8.2 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.2.1 NORTH AMERICA

8.2.2 EUROPE

8.2.3 ASIA-PACIFIC

8.2.4 SOUTH AMERICA

8.2.5 MIDDLE EAST & AFRICA

8.3 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

8.3.1 MEDICATION

8.3.2 SURGERY

8.3.3 PHYSICAL THERAPY

8.3.4 OTHERS

8.4 GLOBAL MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.4.1 BIOLOGICS

8.4.2 NSAIDS

8.4.3 ANALGESICS

8.4.4 DISEASE-MODIFYING ANTIRHEUMATIC DRUGS (DMARDS)

8.4.5 OTHERS

8.5 GLOBAL BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.5.1 TNF INHIBITORS

8.5.2 INTERLEUKIN (IL-17) INHIBITORS

8.5.3 JAK INHIBITORS

8.5.4 OTHERS

8.6 GLOBAL TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.6.1 ADALIMUMAB

8.6.2 ETANERCEPT

8.6.3 CERTOLIZUMAB PEGOL

8.6.4 INFLIXIMAB

8.6.5 OTHERS

8.7 GLOBAL INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.7.1 SECUKINUMAB

8.7.2 IXEKIZUMAB

8.7.3 OTHERS

8.8 GLOBAL JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.8.1 UPADACITINIB

8.8.2 TOFACITINIB

8.8.3 OTHERS

8.9 GLOBAL NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.9.1 TRADITIONAL NSAIDS

8.9.2 SELECTIVE COX-2 INHIBITORS

8.9.3 OTHERS

8.1 GLOBAL MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.10.1 NORTH AMERICA

8.10.2 EUROPE

8.10.3 ASIA-PACIFIC

8.10.4 SOUTH AMERICA

8.10.5 MIDDLE EAST AND AFRICA

8.11 GLOBAL SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.11.1 JOINT REPLACEMENT

8.11.2 SPINAL FUSION

8.11.3 OTHERS

8.12 GLOBAL SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.12.1 NORTH AMERICA

8.12.2 EUROPE

8.12.3 ASIA-PACIFIC

8.12.4 SOUTH AMERICA

8.12.5 MIDDLE EAST AND AFRICA

8.13 GLOBAL PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.13.1 EXERCISE-BASED APPROACHES

8.13.2 HYDROTHERAPY

8.13.3 OTHERS

8.14 GLOBAL PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.14.1 NORTH AMERICA

8.14.2 EUROPE

8.14.3 ASIA-PACIFIC

8.14.4 SOUTH AMERICA

8.14.5 MIDDLE EAST AND AFRICA

8.15 GLOBAL OTHER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.15.1 NORTH AMERICA

8.15.2 EUROPE

8.15.3 ASIA-PACIFIC

8.15.4 SOUTH AMERICA

8.15.5 MIDDLE EAST AND AFRICA

9 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG

9.1 OVERVIEW

9.2 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

9.2.1 ADALIMUMAB

9.2.2 SECUKINUMAB

9.2.3 ETANERCEPT

9.2.4 IXEKIZUMAB

9.2.5 UPADACITINIB

9.2.6 CERTOLIZUMAB PEGOL

9.2.7 GOLIMUMAB

9.2.8 INFLIXIMAB

9.2.9 TOFACITINIB

9.2.10 OTHERS

9.3 GLOBAL ADALIMUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.3.1 NORTH AMERICA

9.3.2 EUROPE

9.3.3 ASIA-PACIFIC

9.3.4 SOUTH AMERICA

9.3.5 MIDDLE EAST AND AFRICA

9.4 GLOBAL SECUKINUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.4.1 NORTH AMERICA

9.4.2 EUROPE

9.4.3 ASIA-PACIFIC

9.4.4 SOUTH AMERICA

9.4.5 MIDDLE EAST AND AFRICA

9.5 GLOBAL ETANERCEPT IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.5.1 NORTH AMERICA

9.5.2 EUROPE

9.5.3 ASIA-PACIFIC

9.5.4 SOUTH AMERICA

9.5.5 MIDDLE EAST AND AFRICA

9.6 GLOBAL IXEKIZUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.6.1 NORTH AMERICA

9.6.2 EUROPE

9.6.3 ASIA-PACIFIC

9.6.4 SOUTH AMERICA

9.6.5 MIDDLE EAST AND AFRICA

9.7 GLOBAL UPADACITINIB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.7.1 NORTH AMERICA

9.7.2 EUROPE

9.7.3 ASIA-PACIFIC

9.7.4 SOUTH AMERICA

9.7.5 MIDDLE EAST AND AFRICA

9.8 GLOBAL CERTOLIZUMAB PEGOL IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.8.1 NORTH AMERICA

9.8.2 EUROPE

9.8.3 ASIA-PACIFIC

9.8.4 SOUTH AMERICA

9.8.5 MIDDLE EAST AND AFRICA

9.9 GLOBAL GOLIMUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.9.1 NORTH AMERICA

9.9.2 EUROPE

9.9.3 ASIA-PACIFIC

9.9.4 SOUTH AMERICA

9.9.5 MIDDLE EAST AND AFRICA

9.1 GLOBAL INFLIXIMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 NORTH AMERICA

9.10.2 EUROPE

9.10.3 ASIA-PACIFIC

9.10.4 SOUTH AMERICA

9.10.5 MIDDLE EAST AND AFRICA

9.11 GLOBAL TOFACITINIB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 NORTH AMERICA

9.11.2 EUROPE

9.11.3 ASIA-PACIFIC

9.11.4 SOUTH AMERICA

9.11.5 MIDDLE EAST AND AFRICA

9.12 GLOBAL OTHER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.12.1 NORTH AMERICA

9.12.2 EUROPE

9.12.3 ASIA-PACIFIC

9.12.4 SOUTH AMERICA

9.12.5 MIDDLE EAST AND AFRICA

10 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION

10.1 OVERVIEW

10.2 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

10.2.1 SUBCUTANEOUS

10.2.2 ORAL

10.2.3 INTRAVENOUS

10.2.4 OTHERS

10.3 GLOBAL SUBCUTANEOUS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.3.1 NORTH AMERICA

10.3.2 EUROPE

10.3.3 ASIA-PACIFIC

10.3.4 SOUTH AMERICA

10.3.5 MIDDLE EAST AND AFRICA

10.4 GLOBAL ORAL IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.4.1 NORTH AMERICA

10.4.2 EUROPE

10.4.3 ASIA-PACIFIC

10.4.4 SOUTH AMERICA

10.4.5 MIDDLE EAST AND AFRICA

10.5 GLOBAL INTRAVENOUS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.5.1 NORTH AMERICA

10.5.2 EUROPE

10.5.3 ASIA-PACIFIC

10.5.4 SOUTH AMERICA

10.5.5 MIDDLE EAST AND AFRICA

10.6 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 NORTH AMERICA

10.6.2 EUROPE

10.6.3 ASIA-PACIFIC

10.6.4 SOUTH AMERICA

10.6.5 MIDDLE EAST AND AFRICA

11 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER

11.1 OVERVIEW

11.2 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

11.2.1 SPECIALTY CLINICS

11.2.2 HOMECARE

11.2.3 HOSPITALS

11.2.4 PHARMACY & RETAILERS

11.2.5 OTHERS

11.3 GLOBAL SPECIALTY CLINICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.3.1 NORTH AMERICA

11.3.2 EUROPE

11.3.3 ASIA-PACIFIC

11.3.4 SOUTH AMERICA

11.3.5 MIDDLE EAST AND AFRICA

11.4 GLOBAL HOMECARE IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.4.1 NORTH AMERICA

11.4.2 EUROPE

11.4.3 ASIA-PACIFIC

11.4.4 SOUTH AMERICA

11.4.5 MIDDLE EAST AND AFRICA

11.5 GLOBAL HOSPITALS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.5.1 NORTH AMERICA

11.5.2 EUROPE

11.5.3 ASIA-PACIFIC

11.5.4 SOUTH AMERICA

11.5.5 MIDDLE EAST AND AFRICA

11.6 GLOBAL PHARMACY & RETAILERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.6.1 NORTH AMERICA

11.6.2 EUROPE

11.6.3 ASIA-PACIFIC

11.6.4 SOUTH AMERICA

11.6.5 MIDDLE EAST AND AFRICA

11.7 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.7.1 NORTH AMERICA

11.7.2 EUROPE

11.7.3 ASIA-PACIFIC

11.7.4 SOUTH AMERICA

11.7.5 MIDDLE EAST AND AFRICA

12 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

12.2.1 HOSPITAL PHARMACY

12.2.2 RETAIL PHARMACY

12.2.3 DIRECT TENDER

12.2.4 ONLINE PHARMACY

12.2.5 OTHERS

12.3 GLOBAL HOSPITAL PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.3.1 NORTH AMERICA

12.3.2 EUROPE

12.3.3 ASIA-PACIFIC

12.3.4 SOUTH AMERICA

12.3.5 MIDDLE EAST AND AFRICA

12.4 GLOBAL RETAIL PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.4.1 NORTH AMERICA

12.4.2 EUROPE

12.4.3 ASIA-PACIFIC

12.4.4 SOUTH AMERICA

12.4.5 MIDDLE EAST AND AFRICA

12.5 GLOBAL DIRECT TENDER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.5.1 NORTH AMERICA

12.5.2 EUROPE

12.5.3 ASIA-PACIFIC

12.5.4 SOUTH AMERICA

12.5.5 MIDDLE EAST AND AFRICA

12.6 GLOBAL ONLINE PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.6.1 NORTH AMERICA

12.6.2 EUROPE

12.6.3 ASIA-PACIFIC

12.6.4 SOUTH AMERICA

12.6.5 MIDDLE EAST AND AFRICA

12.7 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.7.1 NORTH AMERICA

12.7.2 EUROPE

12.7.3 ASIA-PACIFIC

12.7.4 SOUTH AMERICA

12.7.5 MIDDLE EAST AND AFRICA

13 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION

13.1 OVERVIEW

13.2 NORTH AMERICA

13.2.1 U.S.

13.2.2 CANADA

13.2.3 MEXICO

13.3 EUROPE

13.3.1 GERMANY

13.3.2 U.K.

13.3.3 FRANCE

13.3.4 ITALY

13.3.5 SPAIN

13.3.6 SWITZERLAND

13.3.7 NETHERLANDS

13.3.8 SWEDEN

13.3.9 RUSSIA

13.3.10 BELGIUM

13.3.11 TURKEY

13.3.12 NORWAY

13.3.13 DENMARK

13.3.14 FINLAND

13.3.15 REST OF EUROPE

13.4 ASIA-PACIFIC

13.4.1 CHINA

13.4.2 JAPAN

13.4.3 INDIA

13.4.4 AUSTRALIA

13.4.5 SOUTH KOREA

13.4.6 TAIWAN

13.4.7 THAILAND

13.4.8 INDONESIA

13.4.9 MALAYSIA

13.4.10 SINGAPORE

13.4.11 PHILIPPINES

13.4.12 HONG KONG

13.4.13 NEW ZEALAND

13.4.14 REST OF ASIA-PACIFIC

13.5 SOUTH AMERICA

13.5.1 BRAZIL

13.5.2 ARGENTINA

13.5.3 COLOMBIA

13.5.4 CHILE

13.5.5 PERU

13.5.6 ECUADOR

13.5.7 URUGUAY

13.5.8 VENEZUELA

13.5.9 BOLIVIA

13.5.10 PARAGUAY

13.5.11 REST OF SOUTH AMERICA

13.6 MIDDLE EAST AND AFRICA

13.6.1 SAUDI ARABIA

13.6.2 SOUTH AFRICA

13.6.3 U.A.E

13.6.4 ISRAEL

13.6.5 EGYPT

13.6.6 KUWAIT

13.6.7 QATAR

13.6.8 OMAN

13.6.9 BAHRAIN

13.6.10 REST OF MIDDLE EAST & AFRICA

14 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET: COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: GLOBAL

14.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

14.3 COMPANY SHARE ANALYSIS: EUROPE

14.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

15 SWOT ANALYSIS

16 COMPANY PROFILE MANUFRACTURER

16.1 NOVARTIS AG

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 COMPANY SHARE ANALYSIS

16.1.4 PRODUCT PORTFOLIO

16.1.5 RECENT DEVELOPMENT

16.2 PFIZER INC.

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 COMPANY SHARE ANALYSIS

16.2.4 PRODUCT PORTFOLIO

16.2.5 RECENT DEVELOPMENT

16.3 ABBVIE INC.

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 COMPANY SHARE ANALYSIS

16.3.4 PRODUCT PORTFOLIO

16.3.5 RECENT DEVELOPMENT

16.4 UCB S.A.

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 COMPANY SHARE ANALYSIS

16.4.4 PRODUCT PORTFOLIO

16.4.5 RECENT DEVELOPMENT

16.5 LILLY

16.5.1 COMPANY SNAPSHOT

16.5.2 REVENUE ANALYSIS

16.5.3 COMPANY SHARE ANALYSIS

16.5.4 PRODUCT PORTFOLIO

16.5.5 RECENT DEVELOPMENT

16.6 BIOGEN

16.6.1 COMPANY SNAPSHOT

16.6.2 REVENUE ANALYSIS

16.6.3 PRODUCT PORTFOLIO

16.6.4 RECENT DEVELOPMENT

16.7 ALKEM

16.7.1 COMPANY SNAPSHOT

16.7.2 REVENUE ANALYSIS

16.7.3 PRODUCT PORTFOLIO

16.7.4 RECENT DEVELOPMENT

16.8 AMGEN INC.

16.8.1 COMPANY SNAPSHOT

16.8.2 REVENUE ANALYSIS

16.8.3 PRODUCT PORTFOLIO

16.8.4 RECENT DEVELOPMENT

16.9 ASTELLAS PHARMA INC

16.9.1 COMPANY SNAPSHOT

16.9.2 REVENUE ANALYSIS

16.9.3 PRODUCT PORTFOLIO

16.9.4 RECENT DEVELOPMENT

16.1 BIOCAD

16.10.1 COMPANY SNAPSHOT

16.10.2 PRODUCT PORTFOLIO

16.10.3 RECENT DEVELOPMENT

16.11 BOEHRINGER INGELHEIM INTERNATIONAL GMBH.

16.11.1 COMPANY SNAPSHOT

16.11.2 PRODUCT PORTFOLIO

16.11.3 RECENT DEVELOPMENT

16.12 BRISTOL-MYERS SQUIBB (BMS)

16.12.1 COMPANY SNAPSHOT

16.12.2 REVENUE ANALYSIS

16.12.3 PRODUCT PORTFOLIO

16.12.4 RECENT DEVELOPMENT

16.13 CELLTRION INC.

16.13.1 COMPANY SNAPSHOT

16.13.2 REVENUE ANALYSIS

16.13.3 PRODUCT PORTFOLIO

16.13.4 RECENT DEVELOPMENTS

16.14 CIPLA

16.14.1 COMPANY SNAPSHOT

16.14.2 REVENUE ANALYSIS

16.14.3 PRODUCT PORTFOLIO

16.14.4 RECENT DEVELOPMENTS

16.15 DR.REDDY’S LABORATORIES LTD.

16.15.1 COMPANY SNAPSHOT

16.15.2 REVENUE ANALYSIS

16.15.3 PRODUCT PORTFOLIO

16.15.4 RECENT DEVELOPMENTS

16.16 F. HOFFMANN-LA ROCHE LTD

16.16.1 COMPANY SNAPSHOT

16.16.2 REVENUE ANALYSIS

16.16.3 PRODUCT PORTFOLIO

16.16.4 RECENT DEVELOPMENT

16.17 FRESENIUS SE & CO. KGAA

16.17.1 COMPANY SNAPSHOT

16.17.2 REVENUE ANALYSIS

16.17.3 PRODUCT PORTFOLIO

16.17.4 RECENT DEVELOPMENT

16.18 GEDEON RICHTER PLC.

16.18.1 COMPANY SNAPSHOT

16.18.2 REVENUE ANALYSIS

16.18.3 PRODUCT PORTFOLIO

16.18.4 RECENT DEVELOPMENTS

16.19 JOHNSON & JOHNSON AND ITS AFFILIATES

16.19.1 COMPANY SNAPSHOT

16.19.2 REVENUE ANALYSIS

16.19.3 PRODUCT PORTFOLIO

16.19.4 RECENT DEVELOPMENT

16.2 KYOWA KIRIN CO., LTD.

16.20.1 COMPANY SNAPSHOT

16.20.2 REVENUE ANALYSIS

16.20.3 PRODUCT PORTFOLIO

16.20.4 RECENT DEVELOPMENT

16.21 LUPIN

16.21.1 COMPANY SNAPSHOT

16.21.2 REVENUE ANALYSIS

16.21.3 PRODUCT PORTFOLIO

16.21.4 RECENT DEVELOPMENTS

16.22 MERCK KGAA

16.22.1 COMPANY SNAPSHOT

16.22.2 REVENUE ANALYSIS

16.22.3 PRODUCT PORTFOLIO

16.22.4 RECENT DEVELOPMENT

16.23 SAMSUNG BIOEPIS

16.23.1 COMPANY SNAPSHOT

16.23.2 PRODUCT PORTFOLIO

16.23.3 RECENT DEVELOPMENT

16.24 SANDOZ.INC

16.24.1 COMPANY SNAPSHOT

16.24.2 REVENUE ANALYSIS

16.24.3 PRODUCT PORTFOLIO

16.24.4 RECENT DEVELOPMENT

16.25 SANOFI

16.25.1 COMPANY SNAPSHOT

16.25.2 REVENUE ANALYSIS

16.25.3 PRODUCT PORTFOLIO

16.25.4 RECENT DEVELOPMENT

16.26 SUN PHARMACEUTICAL INDUSTRIES LTD.

16.26.1 COMPANY SNAPSHOT

16.26.2 REVENUE ANALYSIS

16.26.3 PRODUCT PORTFOLIO

16.26.4 RECENT DEVELOPMENTS

16.27 TAKEDA PHARMACEUTICAL COMPANY LIMITED.

16.27.1 COMPANY SNAPSHOT

16.27.2 REVENUE ANALYSIS

16.27.3 PRODUCT PORTFOLIO

16.27.4 RECENT DEVELOPMENT

16.28 TEVA PHARMACEUTICAL INDUSTRIES LTD.

16.28.1 COMPANY SNAPSHOT

16.28.2 REVENUE ANALYSIS

16.28.3 PRODUCT PORTFOLIO

16.28.4 RECENT DEVELOPMENT

16.29 TORRENT PHARMACEUTICALS LTD.

16.29.1 COMPANY SNAPSHOT

16.29.2 REVENUE ANALYSIS

16.29.3 PRODUCT PORTFOLIO

16.29.4 RECENT DEVELOPMENTS

16.3 VIATRIS INC.

16.30.1 COMPANY SNAPSHOT

16.30.2 REVENUE ANALYSIS

16.30.3 PRODUCT PORTFOLIO

16.30.4 RECENT DEVELOPMENTS

16.31 ZYDUS GROUP

16.31.1 COMPANY SNAPSHOT

16.31.2 REVENUE ANALYSIS

16.31.3 PRODUCT PORTFOLIO

16.31.4 RECENT DEVELOPMENT

17 COMPANY PROFILE DISTRIBUTOR

17.1 ALFRESA PHARMA CORPORATION

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 PRODUCT PORTFOLIO

17.1.4 RECENT DEVELOPMENT

17.2 ASTUTE HEALTHCARE LTD.

17.2.1 COMPANY SNAPSHOT

17.2.2 PRODUCT PORTFOLIO

17.2.3 RECENT DEVELOPMENT

17.3 CARDINAL HEALTH

17.3.1 COMPANY SNAPSHOT

17.3.2 REVENUE ANALYSIS

17.3.3 PRODUCT PORTFOLIO

17.3.4 RECENT DEVELOPMENT

17.4 CENCORA, INC.

17.4.1 COMPANY SNAPSHOT

17.4.2 REVENUE ANALYSIS

17.4.3 PRODUCT PORTFOLIO

17.4.4 RECENT DEVELOPMENT

17.5 MCKESSON CORPORATION

17.5.1 COMPANY SNAPSHOT

17.5.2 REVENUE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 RECENT DEVELOPMENT

17.6 MEDIPAL HOLDINGS CORPORATION

17.6.1 COMPANY SNAPSHOT

17.6.2 REVENUE ANALYSIS

17.6.3 PRODUCT PORTFOLIO

17.6.4 RECENT DEVELOPMENT

17.7 PHOENIX PHARMA SE

17.7.1 COMPANY SNAPSHOT

17.7.2 PRODUCT PORTFOLIO

17.7.3 RECENT DEVELOPMENT

17.8 SMITH DRUG COMPANY

17.8.1 COMPANY SNAPSHOT

17.8.2 PRODUCT PORTFOLIO

17.8.3 RECENT DEVELOPMENT

17.9 ZUELLIG PHARMA

17.9.1 COMPANY SNAPSHOT

17.9.2 PRODUCT PORTFOLIO

17.9.3 RECENT DEVELOPMENT

18 QUESTIONNAIRE

19 RELATED REPORTS

List of Table

TABLE 1 COST BREAKDOWN (BIOLOGIC VS NON-BIOLOGIC THERAPY)

TABLE 2 DRUG COST BENCHMARKS (GLOBAL PRICING PERSPECTIVE)

TABLE 3 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 4 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 5 GLOBAL MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 6 GLOBAL BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 7 GLOBAL TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 8 GLOBAL INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 GLOBAL JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 10 GLOBAL NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 11 GLOBAL MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 12 GLOBAL SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 13 GLOBAL SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 14 GLOBAL PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 15 GLOBAL PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 16 GLOBAL OTHER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 17 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 18 GLOBAL ADALIMUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 19 GLOBAL SECUKINUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 20 GLOBAL ETANERCEPT IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 21 GLOBAL IXEKIZUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 22 GLOBAL UPADACITINIB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 23 GLOBAL CERTOLIZUMAB PEGOL IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 24 GLOBAL GOLIMUMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 25 GLOBAL INFLIXIMAB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 26 GLOBAL TOFACITINIB IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 27 GLOBAL OTHER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 28 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 29 GLOBAL SUBCUTANEOUS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 GLOBAL ORAL IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 GLOBAL INTRAVENOUS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 32 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 33 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 34 GLOBAL SPECIALTY CLINICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 35 GLOBAL HOMECARE IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 36 GLOBAL HOSPITALS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 37 GLOBAL PHARMACY & RETAILERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 38 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 39 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 40 GLOBAL HOSPITAL PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 41 GLOBAL RETAIL PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 42 GLOBAL DIRECT TENDER IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 43 GLOBAL ONLINE PHARMACY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 44 GLOBAL OTHERS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 45 GLOBAL NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 46 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 47 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 48 NORTH AMERICA MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 49 NORTH AMERICA BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 50 NORTH AMERICA TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 51 NORTH AMERICA INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 52 NORTH AMERICA JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 53 NORTH AMERICA NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 54 NORTH AMERICA SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 55 NORTH AMERICA PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 56 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 57 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 58 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 59 NORTH AMERICA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 60 U.S. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 61 U.S. MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 62 U.S. BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 63 U.S. TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 64 U.S. INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 U.S. JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 66 U.S. NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 U.S. SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 U.S. PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 69 U.S. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 70 U.S. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 71 U.S. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 72 U.S. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 73 CANADA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 74 CANADA MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 75 CANADA BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 76 CANADA TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 77 CANADA INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 78 CANADA JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 79 CANADA NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 80 CANADA SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 81 CANADA PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 82 CANADA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 83 CANADA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 84 CANADA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 85 CANADA NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 86 MEXICO NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 87 MEXICO MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 88 MEXICO BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 89 MEXICO TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 90 MEXICO INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 91 MEXICO JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 92 MEXICO NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 93 MEXICO SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 94 MEXICO PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 95 MEXICO NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 96 MEXICO NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 97 MEXICO NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 98 MEXICO NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 99 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 100 EUROPE

TABLE 101 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 102 EUROPE MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 103 EUROPE BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 104 EUROPE TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 105 EUROPE INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 106 EUROPE JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 107 EUROPE NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 108 EUROPE SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 109 EUROPE PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 110 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 111 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 112 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 113 EUROPE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 114 GERMANY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 115 GERMANY MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 116 GERMANY BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 117 GERMANY TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 118 GERMANY INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 119 GERMANY JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 120 GERMANY NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 121 GERMANY SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 122 GERMANY PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 123 GERMANY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 124 GERMANY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 125 GERMANY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 126 GERMANY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 127 U.K. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 128 U.K. MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 129 U.K. BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 130 U.K. TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 131 U.K. INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 132 U.K. JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 133 U.K. NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 134 U.K. SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 135 U.K. PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 136 U.K. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 137 U.K. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 138 U.K. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 139 U.K. NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 140 FRANCE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 141 FRANCE MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 142 FRANCE BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 143 FRANCE TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 144 FRANCE INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 145 FRANCE JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 146 FRANCE NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 147 FRANCE SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 148 FRANCE PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 149 FRANCE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 150 FRANCE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 151 FRANCE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 152 FRANCE NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 153 ITALY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 154 ITALY MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 155 ITALY BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 156 ITALY TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 157 ITALY INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 158 ITALY JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 159 ITALY NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 160 ITALY SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 161 ITALY PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 162 ITALY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 163 ITALY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 164 ITALY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 165 ITALY NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 166 SPAIN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 167 SPAIN MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 168 SPAIN BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 169 SPAIN TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 170 SPAIN INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 171 SPAIN JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 172 SPAIN NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 173 SPAIN SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 174 SPAIN PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 175 SPAIN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 176 SPAIN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 177 SPAIN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 178 SPAIN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 179 SWITZERLAND NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 180 SWITZERLAND MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 181 SWITZERLAND BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 182 SWITZERLAND TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 183 SWITZERLAND INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 184 SWITZERLAND JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 185 SWITZERLAND NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 186 SWITZERLAND SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 187 SWITZERLAND PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 188 SWITZERLAND NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DRUG, 2018-2033 (USD THOUSAND)

TABLE 189 SWITZERLAND NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY ROUTE OF ADMINISTRATION, 2018-2033 (USD THOUSAND)

TABLE 190 SWITZERLAND NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 191 SWITZERLAND NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 192 NETHERLANDS NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TREATMENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 193 NETHERLANDS MEDICATION IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 194 NETHERLANDS BIOLOGICS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 195 NETHERLANDS TNF INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 196 NETHERLANDS INTERLEUKIN (IL-17) INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 197 NETHERLANDS JAK INHIBITORS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 198 NETHERLANDS NSAIDS IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 199 NETHERLANDS SURGERY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 200 NETHERLANDS PHYSICAL THERAPY IN NON-RADIOGRAPHIC AXIAL SPONDYLOARTHRITIS THERAPEUTICS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)