Global Non Thermal Pasteurization In Dairy Industry Market

Market Size in USD Billion

USD

1.25 Billion

USD

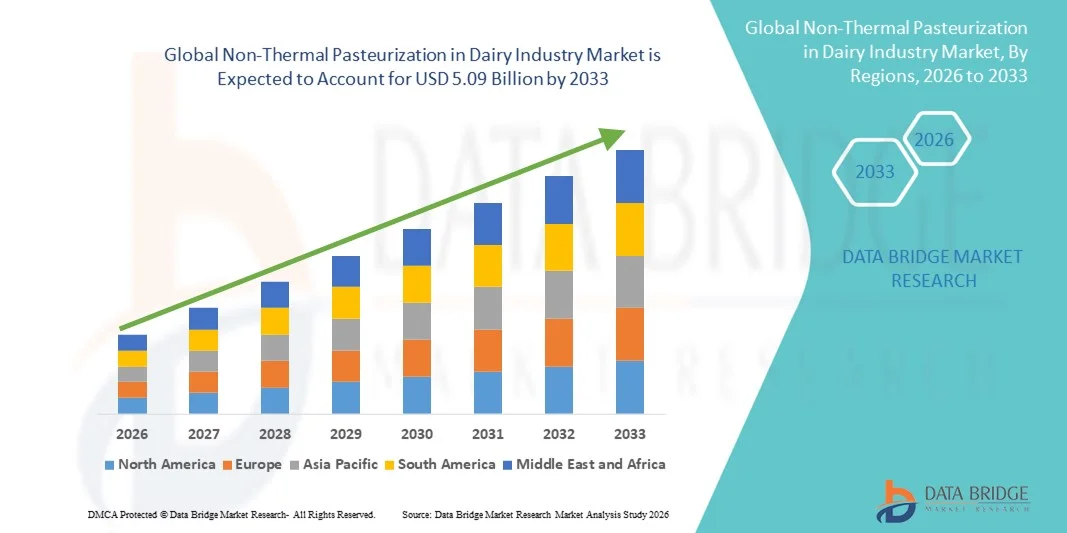

5.09 Billion

2025

2033

USD

1.25 Billion

USD

5.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.25 Billion | |

| USD 5.09 Billion | |

| % | |

|

What is the Non-Thermal Pasteurization in Dairy Industry Market Size and Growth Rate?

- As per Data Bridge Market Research Analysis the global non-thermal pasteurization in dairy industry market size was valued at USD 1.25 billion in 2025 and is expected to reach USD 5.09 billion by 2033, at a CAGR of 19.20% during the forecast period

- The market growth is largely fueled by the increasing demand for safe, high-quality dairy products combined with technological advancements in non-thermal processing methods, enabling improved microbial inactivation while preserving nutritional value, taste, and freshness

- Furthermore, rising consumer preference for minimally processed, clean-label, and extended-shelf-life dairy products, along with stringent food safety regulations and sustainability goals, is accelerating the uptake of Non-Thermal Pasteurization solutions in the dairy industry, thereby significantly boosting the overall growth of the Non-Thermal Pasteurization in Dairy Industry Market

Market Size & Forecast

Global Market Value (2025): USD 1.25 billion

Expected Market Value (2033): USD 5.09 billion

Forecast CAGR (2026–2033): 19.20%

Non-Thermal Pasteurization in Dairy Industry Market Analysis

- Non-Thermal Pasteurization technologies, such as High-Pressure Processing (HPP), Pulsed Electric Field (PEF), and Ultraviolet (UV) treatment, are increasingly vital in the dairy industry as they ensure microbial safety while preserving nutritional value, sensory quality, and freshness of dairy products

- The market growth is primarily driven by rising consumer demand for clean-label and minimally processed dairy products, stringent food safety regulations, and technological advancements that extend shelf life without heat damage, encouraging dairy processors to adopt non-thermal solutions

- North America dominated the non-thermal pasteurization in dairy industry market with an estimated revenue share of around 36.9% in 2025, supported by advanced dairy processing infrastructure, high adoption of HPP technology, and strong presence of key technology providers, particularly in the U.S. and Canada

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, driven by expanding dairy consumption, increasing food safety awareness, rapid industrialization of dairy processing, and rising investments in advanced preservation technologies across countries such as China and India

- The Liquid segment accounted for the largest market revenue share of 64.8% in 2025, driven by the extensive consumption of liquid dairy products such as milk, flavored milk, dairy drinks, cream, and whey-based beverages

Report Scope and Non-Thermal Pasteurization in Dairy Industry Market Segmentation

|

Attributes |

Non-Thermal Pasteurization in Dairy Industry Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Hiperbaric S.A. (Spain) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Non-Thermal Pasteurization in Dairy Industry Market?

Rising Adoption of Advanced Non-Thermal Processing Technologies

- A significant and accelerating trend in the global non-thermal pasteurization in dairy industry market is the increasing adoption of advanced processing technologies such as high-pressure processing (HPP), pulsed electric fields (PEF), and ultraviolet (UV) treatment to ensure food safety while preserving nutritional quality and sensory attributes

- For instance, in 2024, a leading European dairy processor expanded the use of high-pressure processing (HPP) for extended-shelf-life milk and yogurt products to meet growing consumer demand for minimally processed dairy products

- Non-thermal pasteurization methods are gaining traction as they effectively inactivate pathogens without exposing dairy products to high temperatures, thereby maintaining protein integrity, vitamins, and natural flavors

- The growing preference for clean-label and premium dairy products is encouraging manufacturers to shift away from conventional thermal pasteurization toward innovative non-thermal alternatives

- This trend toward advanced, quality-preserving pasteurization technologies is reshaping dairy processing standards and positioning non-thermal methods as a key differentiator in competitive global dairy markets

- As a result, dairy producers across North America, Europe, and Asia-Pacific are increasingly investing in non-thermal processing equipment to enhance product value and meet evolving consumer expectations

Non-Thermal Pasteurization in Dairy Industry Market Dynamics

Driver

Growing Demand for Safe, High-Quality, and Extended Shelf-Life Dairy Products

- The rising global demand for safe, nutritious, and extended shelf-life dairy products is a major driver fueling the adoption of non-thermal pasteurization technologies across the dairy industry

- For instance, in June 2025, a major dairy cooperative in the United States implemented pulsed electric field (PEF) technology for liquid milk processing to improve microbial safety while extending shelf life without altering taste or nutritional value

- Increasing urbanization and changing consumer lifestyles are driving demand for convenient dairy products with longer shelf stability and minimal preservatives

- Stringent food safety regulations and quality standards imposed by regulatory authorities in regions such as Europe and North America further encourage dairy manufacturers to adopt advanced pasteurization methods

- The expansion of international dairy trade also necessitates improved preservation techniques to maintain product quality during long-distance transportation

- Together, these factors are significantly accelerating global investment in non-thermal pasteurization technologies within the dairy sector

Restraint/Challenge

High Capital Investment and Limited Technical Expertise

- The high initial capital investment required for installing non-thermal pasteurization systems remains a significant challenge, particularly for small and mid-sized dairy processors

- For instance, in early 2025, several dairy producers in Southeast Asia postponed the adoption of UV and HPP-based pasteurization systems due to high equipment costs and limited access to skilled technical personnel

- Non-thermal technologies often require specialized infrastructure, maintenance, and process optimization, increasing operational complexity

- Limited awareness and technical know-how regarding the scalability and performance of non-thermal methods can further hinder adoption, especially in developing regions

- Regulatory approval processes for newer pasteurization technologies can also be time-consuming, delaying commercialization and market penetration

- Overcoming these challenges through cost-effective technology solutions, workforce training programs, and supportive regulatory frameworks will be crucial for sustained growth in the Non-Thermal Pasteurization in Dairy Industry market

Non-Thermal Pasteurization in Dairy Industry Market Scope

The market is segmented on the basis of technique and food form.

- By Technique

On the basis of technique, the Global Non-Thermal Pasteurization in Dairy Industry market is segmented into High Pressure Processing (HPP), Pulsed Electric Field (PEF), Microwave Volumetric Heating (MVH), Irradiation, Ultrasonic, and Others. The High Pressure Processing (HPP) segment dominated the largest market revenue share of 38.6% in 2025, owing to its proven effectiveness in microbial inactivation while preserving the nutritional value, taste, and texture of dairy products. HPP is widely adopted for milk, yogurt, cheese, and functional dairy beverages due to its ability to extend shelf life without heat damage. Major dairy producers in Europe and North America increasingly rely on HPP to meet clean-label and preservative-free product demands. The technology is compatible with packaged products, reducing contamination risks. Regulatory acceptance of HPP across developed markets further supports its dominance. In addition, growing consumer preference for minimally processed dairy continues to reinforce adoption. The segment benefits from continuous technological improvements that enhance throughput and reduce processing costs, strengthening its leadership position through 2033.

The Pulsed Electric Field (PEF) segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by rising demand for energy-efficient and continuous-flow pasteurization methods. PEF is increasingly used in liquid dairy applications such as milk, whey, and dairy-based beverages due to its low thermal impact and high processing speed. Growing investments in pilot-scale and industrial-scale PEF systems across Asia-Pacific and Latin America are accelerating adoption. The technique supports superior retention of vitamins and bioactive compounds, aligning with premium dairy trends. Lower operational energy consumption compared to conventional methods also supports market expansion. Furthermore, increasing R&D collaborations between equipment manufacturers and dairy processors are enhancing commercial viability. These factors collectively position PEF as the fastest-growing technology segment.

- By Food Form

On the basis of food form, the Global Non-Thermal Pasteurization in Dairy Industry market is segmented into Liquid and Solid. The Liquid segment accounted for the largest market revenue share of 64.8% in 2025, driven by the extensive consumption of liquid dairy products such as milk, flavored milk, dairy drinks, cream, and whey-based beverages. Non-thermal technologies like HPP and PEF are highly compatible with liquid dairy, enabling efficient microbial control without altering sensory properties. Rising demand for extended shelf-life milk products in urban and export markets supports segment dominance. Liquid dairy producers increasingly adopt non-thermal processing to meet cold-chain distribution requirements. In addition, growing health awareness and demand for fortified liquid dairy beverages contribute to higher adoption. The segment benefits from ease of scalability and integration with existing processing lines. These advantages ensure continued leadership of the liquid food form segment through the forecast period.

The Solid segment is projected to register the fastest CAGR of 19.6% from 2026 to 2033, driven by increasing application of non-thermal technologies in cheese, butter, paneer, and fermented dairy products. HPP is gaining traction in solid dairy to enhance safety and shelf life without affecting texture and flavor. Premium and artisanal cheese manufacturers are adopting non-thermal pasteurization to preserve product authenticity. Growth in packaged and export-oriented cheese products across Europe and Asia-Pacific further fuels expansion. Technological advancements now allow better penetration of pressure and ultrasonic waves in solid matrices. In addition, rising demand for minimally processed solid dairy products supports rapid growth. These factors collectively drive the strong CAGR of the solid food form segment.

Non-Thermal Pasteurization in Dairy Industry Market Regional Analysis

- North America dominated the non-thermal pasteurization in dairy industry market with an estimated revenue share of around 36.9% in 2025, supported by advanced dairy processing infrastructure, high adoption of high-pressure processing (HPP) and other non-thermal technologies, and the strong presence of key technology providers in the U.S. and Canada

- Dairy producers in the region emphasize food safety, extended shelf life, and preservation of nutritional quality, which has accelerated the adoption of non-thermal pasteurization methods across milk, cheese, yogurt, and value-added dairy products

- This widespread adoption is further supported by stringent food safety regulations, high consumer demand for clean-label and minimally processed dairy products, and substantial investments in advanced dairy processing technologies, strengthening North America’s leadership in the market

U.S. Non-Thermal Pasteurization in Dairy Industry Market Insight

The U.S. non-thermal pasteurization in dairy industry market accounted for the largest revenue share within North America in 2025, driven by the strong penetration of high-pressure processing (HPP), pulsed electric field (PEF), and ultraviolet (UV) technologies in commercial dairy operations. U.S. dairy manufacturers are increasingly adopting non-thermal pasteurization to meet regulatory compliance, enhance product safety, and respond to growing consumer demand for fresh-tasting, preservative-free dairy products. In addition, continuous R&D investments and the presence of established food processing technology providers further support market expansion in the country.

Europe Non-Thermal Pasteurization in Dairy Industry Market Insight

The Europe non-thermal pasteurization in dairy industry market is projected to expand at a steady CAGR during the forecast period, primarily driven by strict food safety standards and rising demand for high-quality dairy products with extended shelf life. Increasing consumer awareness regarding nutritional retention and sustainable food processing is fostering the adoption of non-thermal pasteurization technologies across European dairy processors. Growth is evident across both industrial-scale dairy plants and specialty dairy producers focusing on premium and organic products.

U.K. Non-Thermal Pasteurization in Dairy Industry Market Insight

The U.K. non-thermal pasteurization in dairy industry market is expected to grow at a notable CAGR over the forecast period, supported by rising demand for minimally processed dairy products and increasing investments in advanced food processing technologies. Dairy manufacturers in the U.K. are increasingly adopting non-thermal methods to comply with evolving food safety regulations while maintaining product quality. The growth of functional dairy products and private-label dairy offerings is also contributing to market expansion.

Germany Non-Thermal Pasteurization in Dairy Industry Market Insight

The Germany non-thermal pasteurization in dairy industry market is anticipated to register considerable growth during the forecast period, driven by the country’s strong dairy processing sector and emphasis on technological innovation. German dairy producers are increasingly integrating non-thermal pasteurization solutions to improve processing efficiency, reduce energy consumption, and align with sustainability goals. The demand for premium, organic, and additive-free dairy products further supports adoption across the market.

Asia-Pacific Non-Thermal Pasteurization in Dairy Industry Market Insight

The Asia-Pacific non-thermal pasteurization in dairy industry market is expected to grow at the fastest CAGR during the forecast period, driven by expanding dairy consumption, increasing food safety awareness, and rapid industrialization of dairy processing in countries such as China and India. Rising investments in modern dairy infrastructure and advanced preservation technologies are accelerating the adoption of non-thermal pasteurization methods. In addition, supportive government initiatives aimed at improving food quality and safety are strengthening market growth across the region.

Japan Non-Thermal Pasteurization in Dairy Industry Market Insight

The Japan non-thermal pasteurization in dairy industry market is gaining traction due to the country’s strong focus on food safety, quality assurance, and technological advancement. Japanese dairy manufacturers are increasingly adopting non-thermal pasteurization techniques to preserve flavor, texture, and nutritional value while ensuring microbial safety. The growing demand for premium dairy products and ready-to-consume offerings is further driving market growth.

China Non-Thermal Pasteurization in Dairy Industry Market Insight

The China non-thermal pasteurization in dairy industry market held the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising disposable incomes, and growing awareness of dairy product safety and quality. The expansion of large-scale dairy processing facilities, along with increased investments in advanced food preservation technologies, is driving the adoption of non-thermal pasteurization across the country. In addition, strong government oversight and modernization of the dairy supply chain are key factors propelling market growth in China.

Non-Thermal Pasteurization in Dairy Industry Market Share

The Non-Thermal Pasteurization in Dairy Industry is primarily led by well-established companies, including:

• Hiperbaric S.A. (Spain)

• Thyssenkrupp AG (Germany)

• Bosch Packaging Technology (Germany)

• Stansted Fluid Power Ltd. (U.K.)

• Pulsemaster BV (Netherlands)

• Nordion Inc. (Canada)

• Elea Technology GmbH (Germany)

• Buhler Group (Switzerland)

• Krones AG (Germany)

• JBT Corporation (U.S.)

• CHIC FresherTech (China)

• Multivac Group (Germany)

• Dukane Corporation (U.S.)

• HPP Italia Srl (Italy)

• Symbios Technologies (U.S.)

• Universal Pasteurization Company (U.S.)

• Next Generation Pasteurization (U.S.)

• FresherTech (China)

• Food Physics Ltd. (U.K.)

Latest Developments in Global Non-Thermal Pasteurization in Dairy Industry Market

- In April 2023, MarketsandMarkets published a report forecasting that the global non-thermal pasteurization market — which includes technologies used in the dairy industry such as High Pressure Processing (HPP) and Pulsed Electric Field (PEF) — would grow from USD 2.3 billion in 2023 to USD 5.7 billion by 2028, at a 20.0% CAGR, driven by rising demand for minimally processed, nutritious food products that retain their natural flavor and quality. This highlights growing industry emphasis on non-thermal methods in dairy to meet consumer preferences for freshness and clean labels

- In June 2024, Technavio released market research indicating the non-thermal pasteurization market is set to grow by USD 6.92 billion from 2024 to 2028 at a notable 29.19% CAGR, with HPP technology adoption increasing among food producers — including dairy processors — due to its ability to maintain original taste and texture while enhancing food safety. This underscores investment by dairy manufacturers into advanced non-thermal equipment to meet sustainability and quality goals

- In April 2024, Hiperbaric launched a compact HPP machine designed for small and medium-sized enterprises (SMEs) processing dairy and other products, enabling smaller dairy operators to adopt non-thermal pasteurization without the capital intensity of larger systems. This development helps widen technology access across diverse dairy producers rather than only large industrial players

- In June 2024, Bosch announced a partnership with a major food manufacturer to co-develop advanced non-thermal pasteurization solutions that emphasize energy efficiency and reduced operational costs, signaling increased collaboration between equipment makers and dairy producers seeking competitive advantages in quality and sustainability. Bosch’s efforts illustrate how legacy food tech companies are pivoting toward non-thermal innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.