Global Nonablative Laser Resurfacing Devices Market

Market Size in USD Billion

USD

2.69 Billion

USD

4.58 Billion

2025

2033

USD

2.69 Billion

USD

4.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.69 Billion | |

| USD 4.58 Billion | |

| % | |

|

Nonablative Laser Resurfacing Devices Market Overview

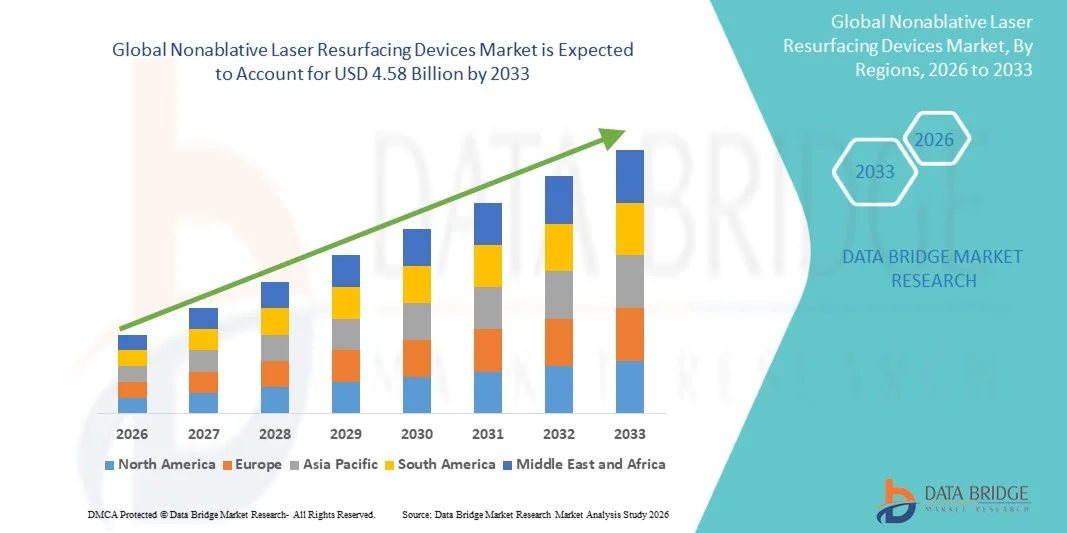

The Nonablative Laser Resurfacing Devices Market was valued at USD 2.69 billion in 2025 and is projected to reach USD 4.58 billion by 2033, growing at a CAGR of 6.90% from 2026 to 2033. Market growth is supported by rising consumer demand for minimally invasive aesthetic procedures, increasing prevalence of skin conditions such as acne scars, melasma, and photoaging, and growing awareness of advanced dermatological treatments among the global population.

The excellent safety profiles associated with nonablative laser procedures, combined with minimal downtime and reduced risk of adverse effects compared to ablative techniques, are driving increased adoption among both patients and dermatology professionals. Ongoing technological advancements in laser systems, including improved fractionated delivery mechanisms, enhanced cooling technologies, and integrated skin analysis platforms, are expanding the clinical applicability of nonablative laser resurfacing devices across medical dermatology and aesthetic medicine. In addition, growing investments in outpatient dermatology clinics, medical spas, and cosmetic surgery centers are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Nonablative Laser Resurfacing Devices Market with the largest revenue share of 38.7% in 2025, supported by high consumer spending on aesthetic procedures, advanced healthcare infrastructure, and the presence of leading market players.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.15% from 2026 to 2033, driven by expanding medical tourism, rising disposable incomes, and increasing demand for cosmetic dermatology services.

- The Nonablative Fractionated Lasers segment led the market with a 58.4% market share in 2025, reflecting strong clinical evidence supporting improved skin rejuvenation outcomes with reduced recovery times.

- The Radiofrequency Devices segment is anticipated to be the fastest-growing technology category, driven by increasing adoption of combination therapies and growing demand for skin tightening procedures.

- The Acne Scars segment dominated the end-use category with a 32.6% market share in 2025, supported by the high prevalence of acne-related scarring among adolescent and adult populations globally.

- The Melasma segment is expected to witness strong growth during the forecast period, driven by rising awareness of hyperpigmentation treatment options and expanding indications for nonablative laser therapies.

Market Size & Forecast

- Global Market Value (2025): USD 2.69 Billion

- Expected Market Value (2033): USD 4.58 Billion

- Forecast CAGR (2026–2033): 6.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Nonablative Laser Resurfacing Devices Market Segmentation

|

Attributes |

Nonablative Laser Resurfacing Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Cynosure LLC (U.S.) · Lumenis Be Ltd. (Israel) · Cutera Inc. (U.S.) · Candela Corporation (U.S.) · Alma Lasers (Israel) · Aerolase Corp. (U.S.) · Sciton Inc. (U.S.) · Solta Medical (Bausch Health Companies Inc.) (U.S.) · Fotona d.o.o. (Slovenia) · Venus Concept (Canada) · Lutronic Corporation (South Korea) · Quanta System S.p.A. (Italy) |

|

Market Opportunities |

· Expansion of nonablative laser platforms into emerging markets with growing aesthetic medicine infrastructure and rising consumer spending on cosmetic procedures · Development of portable, cost-effective laser systems enabling adoption in medical spas, outpatient clinics, and smaller dermatology practices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Nonablative Laser Resurfacing Devices Market Trends

Trend: Integration of Artificial Intelligence and Advanced Imaging in Laser Platforms

Clinical adoption of nonablative laser resurfacing devices continues to accelerate as technological innovations improve treatment precision, patient safety, and procedural outcomes. Advanced imaging systems, including real-time skin analysis and AI-powered treatment planning algorithms, enable practitioners to customize treatment parameters based on individual skin characteristics, optimizing energy delivery and minimizing adverse effects. Integration of smart cooling technologies and automated pulse modulation enhances patient comfort and reduces the risk of thermal injury during procedures.

For instance,

The Clear + Brilliant laser system has gained market traction due to its ability to deliver gentle fractionated treatments with minimal downtime, providing patients with a non-invasive option for skin rejuvenation and maintenance between more intensive procedures.

In addition, research demonstrates that combination therapies utilizing nonablative lasers alongside topical agents and radiofrequency devices yield superior outcomes for hyperpigmentation and textural irregularities, supporting broader clinical adoption across dermatology and aesthetic medicine specialties. The integration of AI-driven diagnostics and automated treatment protocols is expected to further enhance procedural standardization and expand market adoption during the forecast period.

Nonablative Laser Resurfacing Devices Market Dynamics

Key Market Driver: Rising Demand for Minimally Invasive Aesthetic Procedures

The growing preference for minimally invasive aesthetic treatments among patients seeking skin rejuvenation with minimal downtime is a primary driver of market growth. Nonablative laser resurfacing devices enable collagen remodeling, pigment reduction, and textural improvement without damaging the outer skin layer, resulting in shorter recovery periods and reduced risk of complications compared to ablative techniques. The increasing prevalence of skin conditions requiring cosmetic intervention, including photoaging, acne scarring, and melasma, is expanding the patient population eligible for nonablative procedures.

For instance,

A 2025 clinical study evaluating nonablative fractional laser treatment for acne scars demonstrated a 45% improvement in scar appearance scores after three treatment sessions, with 92% of patients reporting high satisfaction and return to normal activities within 24 hours. Rising demand for safe, effective, and convenient aesthetic procedures is expected to strengthen adoption of nonablative laser technologies globally.

Key Restraint/Challenge: High Equipment Costs and Reimbursement Limitations

The substantial capital investment required for advanced nonablative laser systems, along with ongoing maintenance, consumables, and training costs, presents a significant barrier to adoption, particularly for smaller dermatology practices and clinics in emerging markets. Limited insurance coverage and reimbursement for cosmetic procedures further restrict patient access and procedural volumes in certain regions.

For instance,

Healthcare providers evaluating nonablative laser adoption must balance clinical benefits against significant capital expenditure, with premium fractionated laser platforms requiring substantial initial investment compared to lower-cost alternatives. Reimbursement limitations for elective aesthetic procedures may constrain market growth in price-sensitive segments.

Key Market Opportunity: Expansion into Medical Spas and Outpatient Aesthetic Centers

The development of compact, user-friendly, and cost-effective nonablative laser systems is creating opportunities for adoption beyond traditional hospital-based dermatology departments. Medical spas, outpatient aesthetic centers, and cosmetic surgery clinics are increasingly incorporating nonablative laser platforms for skin rejuvenation, pigmentation treatment, and anti-aging procedures. Simultaneously, expanding aesthetic medicine infrastructure in Asia-Pacific, Latin America, and the Middle East is driving demand for nonablative laser capabilities in previously underserved markets.

For instance,

The global medical aesthetics market, including nonablative laser devices, is projected to experience sustained growth through 2033, driven by increasing consumer awareness, social media influence on beauty standards, and expanding access to cosmetic dermatology services worldwide. High equipment costs and limited reimbursement may constrain adoption among budget-sensitive providers.

Nonablative Laser Resurfacing Devices Market Scope

The nonablative laser resurfacing devices market is segmented on the basis of type, technology, and end-use.

By Type

On the basis of type, the Nonablative Laser Resurfacing Devices Market is segmented into nonablative fractionated lasers and nonablative nonfractionated lasers. The nonablative fractionated lasers segment dominated the market with a 58.4% market share in 2025. The nonablative fractionated lasers segment led the market due to its established clinical efficacy in treating acne scars, fine lines, and pigmentation disorders with reduced downtime compared to ablative alternatives. Strong clinical evidence supporting improved collagen remodeling and skin texture enhancement has driven widespread adoption across North America and Europe. High procedure volumes in dermatology clinics and medical spas contribute to segment leadership.

The nonablative nonfractionated lasers segment is expected to witness the fastest growth from 2026 to 2033 at a CAGR of 7.85%, driven by increasing adoption for vascular lesion treatment, hair removal applications, and combination therapy protocols. Technological advancements enabling improved energy delivery and enhanced safety profiles are expanding the clinical utility of nonfractionated platforms across diverse dermatological indications.

By Technology

On the basis of technology, the Nonablative Laser Resurfacing Devices Market is segmented into infrared lasers, fractional laser, high impact light sources, and radiofrequency devices. The fractional laser segment dominated the market with a 36.8% market share in 2025. The fractional laser segment led the market due to its ability to deliver targeted microcolumns of energy while preserving surrounding tissue, enabling faster healing and reduced complications. Widespread clinical adoption for acne scar treatment, skin rejuvenation, and pigmentation correction supports segment dominance. The availability of diverse fractional platforms across price points has expanded market accessibility.

The radiofrequency devices segment is expected to witness the fastest growth from 2026 to 2033 at a CAGR of 8.45%, driven by increasing demand for skin tightening procedures, combination therapy protocols, and non-laser alternatives for patients with contraindications to laser treatment. Growing adoption of microneedling RF and monopolar/bipolar RF platforms for facial contouring and body treatments is supporting segment expansion.

By End-use

On the basis of end-use, the Nonablative Laser Resurfacing Devices Market is segmented into facial and extra-facial wrinkles, acne scars, surgical/traumatic scars, melasma, and skin texture and discoloration. The acne scars segment dominated the market with a 32.6% market share in 2025 due to the high prevalence of acne-related scarring among adolescent and adult populations globally and strong clinical evidence supporting nonablative laser efficacy for scar remodeling. Growing awareness of treatment options and increasing patient willingness to pursue cosmetic interventions for acne sequelae contribute to segment leadership.

The melasma segment is expected to witness the fastest growth from 2026 to 2033 at a CAGR of 8.65%, driven by rising awareness of hyperpigmentation treatment options, expanding indications for nonablative laser therapies in diverse skin types, and growing demand for safe, effective treatments among populations with higher melasma prevalence. Technological advancements enabling precise energy delivery with reduced risk of post-inflammatory hyperpigmentation are supporting segment expansion.

Nonablative Laser Resurfacing Devices Market Regional Analysis

North America dominated the nonablative laser resurfacing devices market with a revenue share of 38.7% in 2025, supported by high consumer spending on aesthetic procedures, advanced healthcare infrastructure, and the presence of leading market players including Cynosure, Cutera, and Candela. Favorable regulatory pathways, robust clinical training infrastructure, and extensive practitioner experience with laser platforms contribute to regional market leadership.

U.S. Nonablative Laser Resurfacing Devices Market Insight

The U.S. nonablative laser resurfacing devices market held a dominant position within North America with a 78.5% regional market share in 2025. The market benefits from the highest concentration of dermatology practices and medical spas globally, extensive physician training programs, and strong consumer demand for aesthetic procedures. Academic medical centers, large dermatology groups, and cosmetic surgery practices continue to expand nonablative laser programs across skin rejuvenation, scar treatment, and pigmentation correction applications. Favorable out-of-pocket payment culture and high disposable incomes support procedural volumes and equipment investment.

Europe Nonablative Laser Resurfacing Devices Market Insight

The Europe nonablative laser resurfacing devices market remains a major contributor, with strong dermatology and aesthetic medicine programs across Germany, the U.K., France, and Italy. Growing adoption of fractional and radiofrequency platforms is providing diverse treatment options across public and private healthcare systems. Cross-disciplinary guidelines and structured training pathways are improving procedural outcomes and standardizing care delivery.

U.K. Nonablative Laser Resurfacing Devices Market Insight

The U.K. nonablative laser resurfacing devices market held a 19.2% share within Europe in 2025, characterized by expanding aesthetic dermatology programs within NHS dermatology departments and private cosmetic clinics. Investment in advanced laser platforms for acne scar treatment, skin rejuvenation, and pigmentation correction is improving access to nonablative options across diverse patient populations.

Germany Nonablative Laser Resurfacing Devices Market Insight

Germany held a leading 24.6% market share within Europe in 2025. The country's robust healthcare infrastructure and advanced dermatological capabilities support comprehensive aesthetic laser programs across dermatology practices and cosmetic surgery centers. Strong clinical training networks and favorable payment frameworks contribute to high procedure volumes and technology adoption.

Asia-Pacific Nonablative Laser Resurfacing Devices Market Insight

The Asia-Pacific nonablative laser resurfacing devices market is poised for rapid growth with a CAGR of 9.15% during the forecast period, driven by expanding medical tourism, rising disposable incomes, and increasing demand for cosmetic dermatology services. Private healthcare systems and aesthetic clinics in China, Japan, India, and South Korea are investing in advanced laser capabilities to meet growing patient demand and improve clinical outcomes.

Japan Nonablative Laser Resurfacing Devices Market Insight

The Japan nonablative laser resurfacing devices market held a 22.4% regional share in 2025, benefiting from advanced healthcare infrastructure, strong practitioner expertise, and high consumer awareness of aesthetic procedures. Nonablative fractional laser treatments for skin rejuvenation and pigmentation correction are well-established, with expanding applications in combination therapy protocols.

China Nonablative Laser Resurfacing Devices Market Insight

The China nonablative laser resurfacing devices market is expected to grow at a CAGR of 10.25% from 2026 to 2033, representing the fastest growth among Asia-Pacific countries. Market expansion is driven by healthcare modernization initiatives, expanding private aesthetic clinic networks, and increasing consumer demand for advanced skin treatment options. Domestic laser device development is complementing imported platforms, improving market accessibility across diverse healthcare settings.

Nonablative Laser Resurfacing Devices Market Share

The nonablative laser resurfacing devices industry is primarily led by well-established companies, including:

- Cynosure LLC (U.S.)

- Lumenis Be Ltd. (Israel)

- Cutera Inc. (U.S.)

- Candela Corporation (U.S.)

- Alma Lasers (Israel)

- Aerolase Corp. (U.S.)

- Sciton Inc. (U.S.)

- Solta Medical (Bausch Health Companies Inc.) (U.S.)

- Fotona d.o.o. (Slovenia)

- Venus Concept (Canada)

- Lutronic Corporation (South Korea)

- Quanta System S.p.A. (Italy)

Latest Developments in Nonablative Laser Resurfacing Devices Market

- In March 2026, Cynosure LLC announced the launch of its next-generation PicoSure Pro platform with enhanced fractionated delivery for improved treatment of acne scars and pigmentation disorders. The updated system incorporates advanced skin imaging and AI-powered treatment optimization, enabling practitioners to customize protocols based on individual patient characteristics.

- In January 2026, Cutera Inc. received U.S. FDA clearance for expanded indications of its Secret RF microneedling radiofrequency platform for the treatment of acne scars and skin laxity. The clearance supports broader clinical adoption and strengthens the company's position in the combination therapy segment.

- In November 2025, Candela Corporation announced a strategic partnership with a leading European dermatology clinic network to expand access to its Nordlys platform across multiple locations. The partnership aims to increase procedural volumes and enhance training programs for practitioners across the region.

- In September 2025, Lumenis Be Ltd. launched its Legend Pro+ platform with integrated monopolar and bipolar radiofrequency capabilities for comprehensive skin rejuvenation treatments. The system enables practitioners to address multiple skin concerns in a single treatment session, improving patient convenience and clinical efficiency.

- In July 2025, Alma Lasers announced the commercial launch of its Harmony XL Pro platform with enhanced nonablative fractional capabilities for the treatment of melasma and hyperpigmentation. The platform incorporates advanced cooling technology and customizable treatment protocols for diverse skin types.

- In May 2025, Sciton Inc. received U.S. FDA clearance for its MOXI laser system for the treatment of benign pigmented lesions and skin revitalization. The clearance expanded the clinical indications for the company's nonablative fractionated platform.

- In February 2025, Aerolase Corp. announced the expansion of its Neo Elite platform into the Asia-Pacific market, with distribution agreements in China, South Korea, and Australia. The expansion supports the company's strategy to address growing demand for advanced laser dermatology solutions in emerging markets.

- In October 2024, Fotona d.o.o. launched its SP Dynamis Pro platform with enhanced Nd:YAG and Er:YAG capabilities for combination ablative and nonablative treatments. The system enables practitioners to perform comprehensive skin rejuvenation protocols with reduced treatment sessions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.