Global Nuclear Medicine Diagnostics Market

Market Size in USD Billion

USD

8.82 Billion

USD

19.74 Billion

2025

2033

USD

8.82 Billion

USD

19.74 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.82 Billion | |

| USD 19.74 Billion | |

| % | |

|

Nuclear Medicine Diagnostics Market Overview

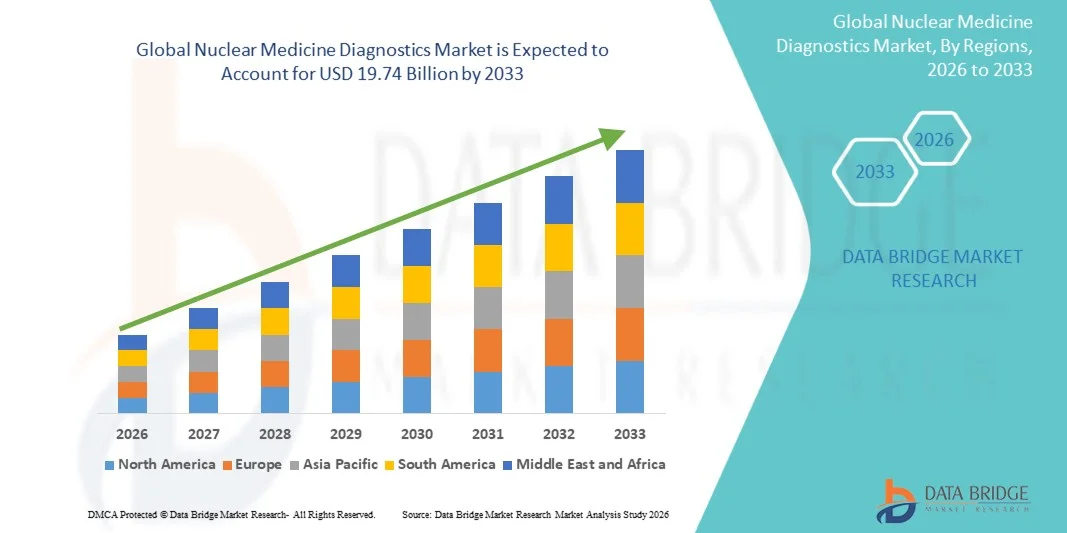

The Nuclear Medicine Diagnostics Market was valued at USD 8.82 billion in 2025 and is projected to reach USD 19.74 billion by 2033, growing at a CAGR of 10.60% from 2026 to 2033. The market is witnessing steady expansion driven by the rising prevalence of cancer and cardiovascular diseases, increasing adoption of advanced molecular imaging techniques, and growing integration of hybrid imaging systems such as PET/CT and SPECT/CT across healthcare facilities.

The demand for early and accurate disease diagnosis is significantly boosting the use of radiopharmaceutical-based imaging, enabling clinicians to detect abnormalities at a molecular level before structural changes occur. In addition, ongoing advancements in radiotracer development, expansion of cyclotron production capacity, and supportive government initiatives for nuclear medicine infrastructure are further accelerating market adoption. The increasing use of personalized medicine and targeted diagnostic approaches is also strengthening the role of nuclear medicine in modern healthcare systems.

Key Market Trends & Insights

- North America dominated the Nuclear Medicine Diagnostics Market with the largest revenue share of 38.12% in 2025, supported by advanced healthcare infrastructure, high adoption of PET/SPECT imaging, and strong reimbursement frameworks for oncology diagnostics.

- The SPECT Radiopharmaceuticals segment led the market with a 52.36% share in 2025, driven by its wide clinical availability, lower cost structure, and extensive use in cardiac, bone, and renal imaging.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by rising cancer prevalence, expanding diagnostic infrastructure, and increasing investments in nuclear medicine facilities across China, India, and Japan.

- PET Radiopharmaceuticals are the fastest-growing type, projected to register a CAGR of 7.3%, reflecting the surge in demand for high-resolution functional imaging in oncology and neurology.

- The SPECT Applications segment dominated the application type category with a 48.91% revenue share in 2025, led by its widespread use in myocardial perfusion imaging, bone scanning, and renal function assessment.

- Skeletal accounted for 31.44% of the market, preferred by the high utilization of bone scans for detecting metastasis, fractures, and infections.

- The Central Nervous System segment is the fastest-growing procedure category, with a CAGR of 7.2%, driven by increasing application of PET imaging in neurodegenerative disorders such as Alzheimer’s and Parkinson’s disease.

Market Size & Forecast

- Global Market Value (2025): USD 8.82 Billion

- Expected Market Value (2033): USD 19.74 Billion

- Forecast CAGR (2026–2033): 10.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Nuclear Medicine Diagnostics Market Segmentation

|

Attributes |

Nuclear Medicine Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Siemens Healthineers AG (Germany) · GE HealthCare (U.S.) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Fujifilm Holdings Corporation (Japan) · Bracco Imaging S.p.A. (Italy) · Curium Pharma (France) · Cardinal Health, Inc. (U.S.) · Lantheus Holdings, Inc. (U.S.) · Novartis AG (Switzerland) · Bayer AG (Germany) · Eli Lilly and Company (U.S.) · Sotera Health Company (Nordion) (Canada) · IBA Radiopharma Solutions (Belgium) · Eckert & Ziegler SE (Germany) · Jubilant Pharma Limited (India) · Mallinckrodt Pharmaceuticals (Ireland) · Telix Pharmaceuticals Limited (Australia) · Life Molecular Imaging GmbH (Germany) · NTP Radioisotopes SOC Ltd (South Africa) · SOFIE Biosciences (U.S.) |

|

Market Opportunities |

· Expanding use of theranostics combining diagnostic imaging and targeted radionuclide therapy · Rising investment in cyclotron and radiopharmaceutical production facilities · Integration of AI-driven image reconstruction and quantification tools |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Nuclear Medicine Diagnostics Market Trends

Trend: Growth in Precision Oncology & Theranostic Imaging

Hospitals and imaging centers are increasingly adopting nuclear medicine diagnostics to support precision oncology, enabling early tumor detection, staging, and therapy monitoring through PET/CT and SPECT/CT systems. The integration of targeted radiotracers allows clinicians to visualize molecular processes in real time, improving diagnostic accuracy and treatment planning. Growing use of hybrid imaging platforms is also enhancing workflow efficiency, while AI-assisted image reconstruction and quantitative analysis are improving interpretation speed and consistency in complex clinical cases, supporting broader adoption across advanced healthcare systems. For instance, expanding use of PSMA PET imaging in prostate cancer diagnosis and management.

Nuclear Medicine Diagnostics Market Dynamics

Key Market Driver: Rising Cancer Burden and Demand for Early Molecular Diagnosis

The increasing global incidence of cancer and cardiovascular disorders is significantly driving demand for nuclear medicine diagnostics, as these modalities enable early and highly accurate disease detection at a molecular level. Healthcare providers are increasingly relying on PET and SPECT imaging to identify disease progression before anatomical changes become visible, improving patient outcomes and survival rates. Government initiatives supporting early screening programs and expanding reimbursement coverage for nuclear imaging procedures are further accelerating market growth across developed and emerging economies. For instance, growing adoption of FDG-PET scans for early detection of oncological and neurological disorders.

Key Restraint/Challenge: High Cost and Limited Radiopharmaceutical Availability

A major restraint in the Nuclear Medicine Diagnostics Market is the high cost associated with imaging systems, radiotracer production, and specialized facility requirements, making adoption challenging for smaller healthcare centers. In addition, the short half-life of radiopharmaceuticals and dependence on cyclotron infrastructure limit supply chain scalability and create regional access disparities. Regulatory complexities surrounding radioactive material handling further increase operational burden and compliance costs, slowing market penetration in cost-sensitive regions. For instance, limited availability of Technetium-99m due to supply chain disruptions in several countries.

Key Market Opportunity: Expansion of AI-Driven Imaging and Theranostics Platforms

The integration of artificial intelligence with nuclear imaging systems presents a strong growth opportunity by enabling faster image reconstruction, improved lesion detection, and enhanced quantitative analysis for clinical decision-making. Simultaneously, the rise of theranostics combining diagnostic imaging with targeted radionuclide therapy is expanding the clinical utility of nuclear medicine in personalized cancer treatment. Increasing investment in digital imaging platforms and hybrid hospital infrastructures is further supporting market expansion across oncology-focused care models. For instance, development of Lu-177 based theranostic treatments for neuroendocrine tumors and prostate cancer.

Nuclear Medicine Diagnostics Market Scope

The nuclear medicine diagnostics market is segmented on the basis of type, application, procedure, and end user.

- By Type

On the basis of type, the Nuclear Medicine Diagnostics Market is segmented into SPECT radiopharmaceuticals and PET radiopharmaceuticals. The SPECT Radiopharmaceuticals segment dominated the market with a 52.36% share in 2025, owing to its wide clinical availability, lower cost structure, and extensive use in cardiac, bone, and renal imaging. SPECT tracers such as Technetium-99m are widely adopted due to their reliable diagnostic performance and established supply chain across hospitals and imaging centers. The segment benefits from strong integration in routine diagnostic workflows, particularly in developing healthcare systems. Its compatibility with existing gamma camera infrastructure further strengthens adoption. High procedural volume in cardiology and skeletal imaging continues to support demand. However, resolution limitations compared to PET imaging slightly restrict its use in advanced oncology applications.

The PET Radiopharmaceuticals segment is expected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing demand for high-resolution functional imaging in oncology and neurology. PET tracers such as FDG are widely used for early cancer detection, staging, and treatment monitoring. Growing adoption of hybrid PET/CT systems is significantly improving diagnostic accuracy and clinical decision-making. Expanding cyclotron infrastructure and radiotracer production capacity are enhancing accessibility across emerging markets. Rising use in personalized medicine and theranostic applications is further accelerating growth. Continuous advancements in novel PET tracers are expanding clinical applications beyond oncology into cardiology and neurodegenerative disorders.

- By Application

On the basis of application, the Nuclear Medicine Diagnostics Market is segmented into SPECT applications and PET applications. The SPECT Applications segment dominated the market with a 48.91% share in 2025, primarily due to its widespread use in myocardial perfusion imaging, bone scanning, and renal function assessment. Its strong presence in routine hospital diagnostics makes it a preferred modality in both developed and emerging healthcare systems. Lower procedural costs and broad reimbursement coverage further support its dominance. Established clinical protocols and widespread availability of gamma imaging systems contribute to consistent demand. It is extensively used in cardiology departments for non-invasive functional assessment. However, slower spatial resolution compared to PET limits its use in highly complex oncology cases.

The PET Applications segment is projected to grow at the fastest CAGR of 7.5% from 2026 to 2033, driven by increasing utilization in oncology, neurology, and cardiology diagnostics. PET imaging provides superior sensitivity and quantitative accuracy, enabling early disease detection at the molecular level. Rising demand for cancer staging and therapy response evaluation is significantly boosting adoption. Integration of PET with CT and MRI is improving anatomical correlation and diagnostic precision. Expanding use of novel radiotracers is broadening clinical applications. Increasing focus on precision medicine and AI-assisted image analysis is further strengthening growth momentum.

- By Procedure

On the basis of procedure, the Nuclear Medicine Diagnostics Market is segmented into central nervous system, endocrine, skeletal, gastrointestinal, genito-urinary, and pulmonary applications. The Skeletal segment dominated the market with a 31.44% share in 2025, owing to high utilization of bone scans for detecting metastasis, fractures, and infections. Bone scintigraphy using SPECT imaging remains a standard diagnostic tool in oncology and orthopedics. Its ability to detect early bone abnormalities supports widespread clinical use. Increasing cancer prevalence, particularly prostate and breast cancer, further drives demand. The segment benefits from high diagnostic reliability and cost-effectiveness compared to advanced imaging alternatives. Established clinical guidelines ensure consistent procedural adoption across hospitals.

The Central Nervous System segment is expected to grow at the fastest CAGR of 7.2% from 2026 to 2033, driven by increasing application of PET imaging in neurodegenerative disorders such as Alzheimer’s and Parkinson’s disease. Growing demand for early diagnosis of brain disorders is significantly boosting adoption. Advanced radiotracers targeting amyloid and tau proteins are improving diagnostic accuracy. Rising aging population globally is further accelerating demand for neurological imaging. Integration of PET with MRI is enhancing structural and functional brain mapping. Expanding research in psychiatric and cognitive disorders is also contributing to market growth.

- By End User

On the basis of end user, the Nuclear Medicine Diagnostics Market is segmented into hospitals, diagnostic centers, and research institutes. The Hospitals segment dominated the market with a 61.28% share in 2025, as they serve as primary facilities for nuclear imaging procedures requiring specialized infrastructure and radiopharmaceutical handling. Hospitals benefit from integrated diagnostic departments, enabling seamless patient management and treatment planning. High patient inflow for oncology and cardiology diagnostics further strengthens dominance. Availability of advanced imaging systems and trained nuclear medicine specialists supports procedural efficiency. Strong reimbursement frameworks in developed regions enhance accessibility. Continuous expansion of hospital-based imaging networks is further reinforcing market leadership.

The Diagnostic Centers segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by rising demand for outpatient imaging services and cost-effective diagnostic solutions. These centers are increasingly adopting PET/CT and SPECT/CT systems to meet growing patient volumes. Shorter waiting times and specialized imaging services are attracting more patients compared to hospitals. Expansion of private diagnostic chains in emerging economies is supporting growth. Increasing awareness of early disease detection is further boosting demand. Technological advancements are enabling compact and efficient imaging system deployment in standalone centers.

Nuclear Medicine Diagnostics Market Regional Analysis

North America dominated the Nuclear Medicine Diagnostics Market with the largest revenue share of 38.12% in 2025, supported by advanced healthcare infrastructure, high adoption of PET/SPECT imaging, and strong reimbursement frameworks for oncology diagnostics. The region also benefits from a well-established radiopharmaceutical supply chain, extensive presence of leading diagnostic imaging centers, and continuous investments in molecular imaging research. Increasing cancer prevalence, growing demand for early and accurate disease detection, and rapid adoption of hybrid imaging technologies continue to strengthen North America’s leadership position in the global market.

U.S. Nuclear Medicine Diagnostics Market Insight

The U.S. nuclear medicine diagnostics market is witnessing strong growth due to rising cancer and cardiovascular disease burden, advanced healthcare infrastructure, and high adoption of PET/CT and SPECT/CT imaging systems. The country’s well-established radiopharmaceutical ecosystem, strong reimbursement policies, and continuous investment in molecular imaging research are driving demand across hospitals and diagnostic centers. Increasing use of theranostic approaches, AI-enabled imaging platforms, and precision oncology solutions is further accelerating market adoption across clinical and research applications.

Europe Nuclear Medicine Diagnostics Market Insight

The Europe nuclear medicine diagnostics market remains a major contributor to global revenue, driven by strong government support for healthcare innovation, widespread adoption of hybrid imaging technologies, and robust clinical research networks. The region benefits from established nuclear medicine infrastructure, high procedural standardization, and increasing use of PET and SPECT imaging in oncology and cardiology. Growing focus on early disease detection and personalized medicine is further supporting market expansion across major European healthcare systems.

U.K. Nuclear Medicine Diagnostics Market Insight

The U.K. nuclear medicine diagnostics market is experiencing steady growth, supported by expanding NHS diagnostic capabilities, increasing adoption of PET/CT imaging, and rising focus on early cancer detection programs. Investments in advanced imaging infrastructure and radiopharmaceutical production are improving access to nuclear medicine services. Integration of AI-based image analysis and growing clinical trials in oncology are further enhancing diagnostic efficiency and accuracy across healthcare facilities.

Germany Nuclear Medicine Diagnostics Market Insight

The Germany nuclear medicine diagnostics market is expanding steadily due to strong medical imaging research capabilities, advanced hospital infrastructure, and increasing adoption of PET and SPECT technologies. The country’s well-developed radiopharmaceutical supply chain and focus on precision diagnostics are driving demand across oncology, neurology, and cardiology applications. Continuous technological advancements and strong collaboration between research institutes and healthcare providers are further strengthening market growth.

Asia-Pacific Nuclear Medicine Diagnostics Market Insight

The Asia-Pacific nuclear medicine diagnostics market is expected to witness rapid growth, driven by rising cancer prevalence, expanding healthcare infrastructure, and increasing adoption of advanced imaging technologies in countries such as China, India, and Japan. Growing awareness of early disease diagnosis, rising investments in nuclear medicine facilities, and expanding availability of radiopharmaceuticals are supporting regional market expansion. Increasing integration of hybrid imaging systems and government initiatives in healthcare modernization are further accelerating growth across the region.

Japan Nuclear Medicine Diagnostics Market Insight

The Japan nuclear medicine diagnostics market is witnessing consistent growth due to strong adoption of advanced imaging technologies, high prevalence of age-related diseases, and continuous innovation in radiopharmaceutical development. Hospitals and research institutes are increasingly using PET/CT and SPECT/CT systems for oncology, neurology, and cardiovascular diagnostics. The country’s focus on precision medicine and early disease detection is further enhancing the adoption of nuclear imaging solutions across clinical settings.

China Nuclear Medicine Diagnostics Market Insight

The China nuclear medicine diagnostics market is growing rapidly, driven by increasing cancer incidence, expanding healthcare infrastructure, and strong government support for advanced medical imaging technologies. Rising adoption of PET/CT and SPECT/CT systems across hospitals and diagnostic centers is significantly boosting market demand. Investments in radiopharmaceutical production facilities, growing clinical research activities, and increasing awareness of early disease detection are positioning China as one of the fastest-growing markets globally.

Nuclear Medicine Diagnostics Market Share

The nuclear medicine diagnostics industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Fujifilm Holdings Corporation (Japan)

- Bracco Imaging S.p.A. (Italy)

- Curium Pharma (France)

- Cardinal Health, Inc. (U.S.)

- Lantheus Holdings, Inc. (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Eli Lilly and Company (U.S.)

- Sotera Health Company (Nordion) (Canada)

- IBA Radiopharma Solutions (Belgium)

- Eckert & Ziegler SE (Germany)

- Jubilant Pharma Limited (India)

- Mallinckrodt Pharmaceuticals (Ireland)

- Telix Pharmaceuticals Limited (Australia)

- Life Molecular Imaging GmbH (Germany)

- NTP Radioisotopes SOC Ltd (South Africa)

- SOFIE Biosciences (U.S.)

Latest Developments in Nuclear Medicine Diagnostics Market

- In May 2024, Siemens Healthineers advanced its molecular imaging portfolio with next-generation PET/CT systems integrated with AI-driven nuclear medicine solutions. These enhancements improved lesion detectability, reduced scanning time, and enabled more precise quantitative analysis in clinical diagnostics. The development supported wider adoption of precision imaging in oncology and neurological disorder assessment. It also strengthened digital transformation across nuclear medicine departments through AI integration. The innovation reinforced Siemens Healthineers’ leadership in advanced diagnostic imaging technologies

- In December 2023, Lantheus Holdings received FDA approval for Posluma (flotufolastat F 18 injection), expanding PET imaging options for prostate cancer detection. The radiopharmaceutical enabled more efficient imaging due to its fluorine-18 isotope, which offers longer half-life and improved distribution logistics compared to gallium-based agents. This development enhanced accessibility of PSMA PET imaging across diagnostic centers and hospitals. It also improved workflow efficiency and scalability of nuclear medicine procedures. The approval strengthened the role of PET imaging in precision oncology diagnostics

- In June 2023, GE HealthCare launched the Omni Legend PET/CT system to enhance nuclear medicine diagnostic imaging performance. The system introduced improved sensitivity, faster scan times, and AI-enabled image reconstruction to support oncology, cardiology, and neurology applications. This innovation significantly improved diagnostic accuracy and workflow efficiency in clinical settings. It also strengthened adoption of hybrid PET/CT systems across hospitals and imaging centers. The launch reflected growing demand for advanced molecular imaging platforms globally

- In May 2022, Novartis received FDA approval for Pluvicto (lutetium Lu 177 vipivotide tetraxetan), expanding theranostic applications in prostate cancer imaging and treatment. The U.S. Food and Drug Administration approval marked a major advancement in nuclear medicine diagnostics by integrating PET-based patient selection with targeted radioligand therapy for PSMA-positive metastatic castration-resistant prostate cancer. This development strengthened precision oncology workflows and accelerated adoption of radiopharmaceutical imaging across cancer centers. It also highlighted the growing role of molecular imaging in guiding targeted therapies. The approval significantly reinforced the global shift toward theranostics-based nuclear medicine approaches

- In March 2022, the U.S. FDA approved Locametz (gallium Ga 68 gozetotide), advancing PSMA PET imaging for prostate cancer diagnosis. The approval enabled highly accurate PET imaging for detecting PSMA-positive lesions in patients with suspected metastasis or recurrence, significantly improving staging and treatment planning. This development expanded the use of gallium-based radiotracers in nuclear medicine diagnostics and strengthened PET/CT adoption in oncology workflows. It also improved early detection capabilities for prostate cancer patients across healthcare systems. The approval supported wider clinical integration of targeted molecular imaging technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.