Global Nucleic Acid Labeling Market

Market Size in USD Billion

USD

2.96 Billion

USD

5.54 Billion

2024

2032

USD

2.96 Billion

USD

5.54 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.96 Billion | |

| USD 5.54 Billion | |

| % | |

|

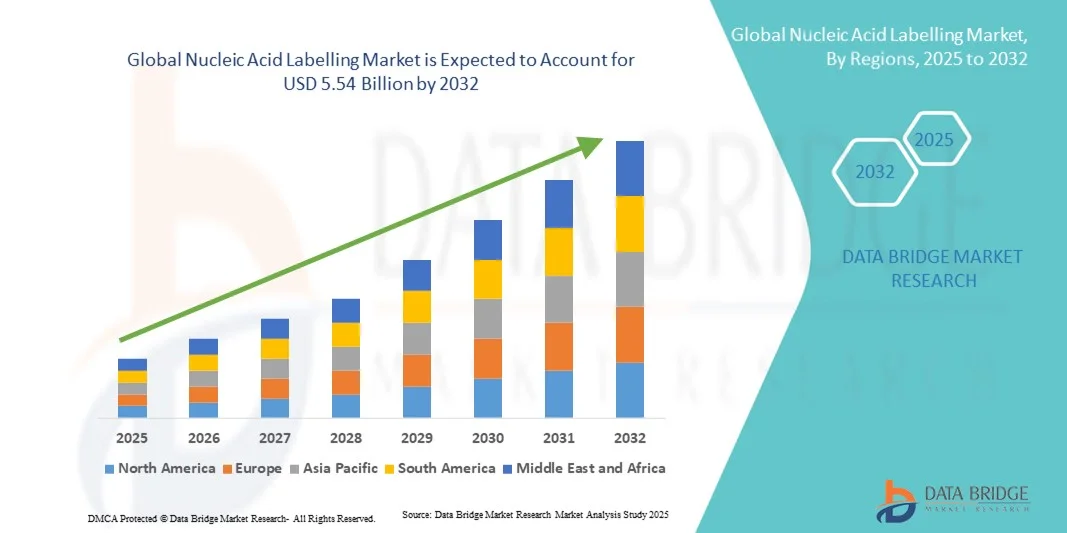

Nucleic Acid Labelling Market Size

- The global nucleic acid labelling market size was valued at USD 2.96 billion in 2024 and is expected to reach USD 5.54 billion by 2032, at a CAGR of 8.16% during the forecast period

- The market growth is largely fueled by the growing adoption and technological advancements in molecular biology, genomics, and biotechnology research, leading to increased demand for accurate and efficient nucleic acid detection and analysis in both academic and industrial settings

- Furthermore, rising demand for high-throughput screening, personalized medicine, and diagnostic applications is establishing nucleic acid labeling solutions as a critical tool for molecular diagnostics, gene expression studies, and drug discovery. These converging factors are accelerating the uptake of nucleic acid labeling solutions, thereby significantly boosting the industry's growth

Nucleic Acid Labelling Market Analysis

- Nucleic Acid Labeling, involving the attachment of fluorescent, radioactive, or chemical tags to DNA or RNA molecules, is increasingly vital in molecular biology, genomics, and diagnostic research due to its role in enabling precise detection, quantification, and analysis of nucleic acids in various applications

- The escalating demand for nucleic acid labeling is primarily fueled by the growing prevalence of genetic and infectious diseases, increased R&D in genomics and personalized medicine, and rising adoption of molecular diagnostic techniques across academic, clinical, and industrial research settings

- North America dominated the nucleic acid labeling market with the largest revenue share of 43.45% in 2024, characterized by advanced research infrastructure, substantial government and private funding in genomics, and a strong presence of key industry players. The U.S. witnessed significant growth due to innovations in labeling technologies, high adoption of next-generation sequencing, and increasing use of fluorescent and PCR-based labeling techniques

- Asia-Pacific is expected to be the fastest growing region in the nucleic acid labeling market during the forecast period, with a projected CAGR of 9.5%, driven by expanding genomics research, rising government initiatives in biotechnology, increasing R&D spending, and a growing number of molecular diagnostic laboratories in countries such as China, India, and Japan

- The Reagents and Kits segment dominated the nucleic acid labeling market with a revenue share of 66.8% in 2024. This dominance is largely attributed to the widespread use of reagents and kits across research, diagnostics, and molecular biology applications such as PCR, DNA sequencing, and in situ hybridization. Reagents and kits are valued for their standardized, ready-to-use formulations that ensure reproducibility, accuracy, and efficiency in laboratory experiments

Report Scope and Nucleic Acid Labelling Market Segmentation

|

Attributes |

Nucleic Acid Labelling Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Nucleic Acid Labelling Market Trends

Enhanced Efficiency Through AI and Automation Integration

- A significant and accelerating trend in the global Nucleic Acid Labeling market is the integration of artificial intelligence (AI) and automated workflows into labeling processes. This fusion of technologies is significantly enhancing accuracy, throughput, and reproducibility in research and clinical applications

- For instance, in 2024, Thermo Fisher Scientific introduced AI-powered automation in its nucleic acid labeling platforms, enabling researchers to optimize labeling protocols based on real-time reaction monitoring, reducing errors and improving experimental consistency

- AI integration allows predictive adjustments to labeling reactions, minimizing reagent wastage and improving labeling efficiency, especially in high-throughput genomic studies

- Automation and AI-enabled software also facilitate complex workflows such as multiplex labeling, next-generation sequencing (NGS) sample preparation, and CRISPR screening, ensuring precise and reproducible results across diverse applications

- The seamless integration of AI with laboratory information management systems (LIMS) allows centralized tracking of reagents, samples, and results, streamlining data management and reporting

- This trend toward intelligent, automated labeling systems is reshaping expectations in molecular biology and diagnostics, enabling faster, more reliable, and cost-efficient experiments

- Consequently, companies such as Agilent Technologies and New England Biolabs are developing AI-assisted and automated nucleic acid labeling solutions to meet growing demands from academic, pharmaceutical, and clinical research laboratories

- The demand for automated and AI-enhanced nucleic acid labeling is growing rapidly across research and clinical sectors, as laboratories prioritize throughput, accuracy, and reproducibility

Nucleic Acid Labelling Market Dynamics

Driver

Rising Demand for Precision and High-Throughput Research

- The increasing adoption of genomic research, personalized medicine, and molecular diagnostics is a key driver for the nucleic acid labeling market. High-throughput applications require accurate, reproducible, and scalable labeling methods to ensure reliable results

- For instance, in 2024, New England Biolabs launched enhanced fluorescent labeling kits optimized for high-throughput RNA and DNA sequencing applications, supporting accelerated research in genomics and diagnostics

- Growing prevalence of genetic and infectious diseases is prompting researchers and healthcare providers to adopt sensitive labeling techniques to detect, quantify, and analyze nucleic acids with high precision

- The expanding use of next-generation sequencing (NGS), CRISPR-based diagnostics, and multiplex assays has intensified demand for advanced labeling solutions that are compatible with automated and AI-enabled workflows

- The increasing number of molecular diagnostic laboratories, research institutes, and pharmaceutical R&D centers globally contributes to sustained market growth

- High reproducibility, reduced experimental variability, and the ability to perform complex multiplex labeling are critical factors driving adoption in both academic and industrial settings

- Rising government and private funding in genomics and molecular biology research is further supporting market expansion, especially in North America and Europe

- Overall, the need for precise, scalable, and efficient labeling solutions in cutting-edge research and clinical applications continues to propel the nucleic acid labeling market forward

Restraint/Challenge

Concerns Regarding Cost and Technical Complexity

- Despite the advantages, high costs associated with advanced nucleic acid labeling kits and automated systems remain a significant barrier to widespread adoption, particularly in emerging regions or smaller research labs

- Complex workflows and the need for specialized equipment and trained personnel can also hinder adoption, as not all laboratories are equipped to handle high-throughput or automated labeling techniques

- Addressing these challenges requires cost-effective solutions, simplified protocols, and educational initiatives to train researchers in the use of advanced labeling technologies

- Ensuring compatibility with diverse reagents, workflows, and instrumentation is crucial for building trust and maximizing the utility of labeling platforms

- Market adoption may be slowed in regions with limited access to advanced laboratory infrastructure, despite growing interest in genomic and molecular diagnostic research

- Overcoming these challenges through user-friendly kits, modular automation, and flexible AI-assisted platforms will be essential for sustained growth

- Companies such as Thermo Fisher Scientific, Agilent Technologies, and New England Biolabs are actively working to develop affordable, simplified, and high-performance solutions to expand adoption globally

Nucleic Acid Labelling Market Scope

The market is segmented on the basis of products, labelling technique and application.

- By Products

On the basis of products, the nucleic acid labelling market is segmented into reagents and kits and services. The Reagents and Kits segment dominated the market with a revenue share of 66.8% in 2024. This dominance is largely attributed to the widespread use of reagents and kits across research, diagnostics, and molecular biology applications such as PCR, DNA sequencing, and in situ hybridization. Reagents and kits are valued for their standardized, ready-to-use formulations that ensure reproducibility, accuracy, and efficiency in laboratory experiments. They simplify complex workflows, reduce errors, and enhance productivity in both academic and industrial laboratories. The growing demand for high-throughput research, personalized medicine, and precision diagnostics further strengthens this segment’s leadership. With increasing investment in life sciences research and continuous innovation in molecular biology techniques, reagents and kits have become indispensable in experimental protocols. Their compatibility with multiple labeling techniques, user-friendly designs, and reliability for sensitive experiments reinforce their strong market position. Furthermore, the increasing need for rapid, high-accuracy testing in genomics and clinical applications contributes to sustained adoption and continued growth in this segment.

The Services segment is anticipated to witness the fastest growth at a CAGR of 8.15% from 2025 to 2032. This growth is driven by the rising trend of outsourcing complex labeling tasks to contract research organizations and specialized service providers. Services encompass custom labeling, assay development, and high-complexity workflows that many laboratories cannot manage internally due to resource constraints or technical expertise requirements. The rapid expansion of genomics, diagnostics, and pharmaceutical R&D is prompting researchers and companies to rely more on external service providers. These services offer cost-effective and scalable solutions, enabling laboratories to focus on their core research while ensuring high-quality, reproducible results. In addition, the growing adoption of advanced technologies, automation, and AI-assisted workflows by service providers is enhancing efficiency and reliability. The ability of CROs to provide tailored solutions, faster turnaround times, and specialized expertise makes the services segment highly attractive for laboratories and research organizations worldwide.

- By Labelling Technique

On the basis of labelling technique, the nucleic acid labelling market is segmented into PCR, Nick Translation, Random Primer, In Vitro Transcription, Reverse Transcription, and End Labelling. The PCR-based labelling segment dominated the market in 2024 with a revenue share of 38.7%, due to its high efficiency, reproducibility, and compatibility with high-throughput applications such as sequencing, gene editing, and molecular diagnostics. PCR labeling is extensively used in research and clinical laboratories for precise and rapid results, supporting a variety of experimental protocols. The segment benefits from widespread adoption in molecular biology research, personalized medicine, and diagnostic workflows, which require accurate amplification and detection of nucleic acids. Automation and AI-assisted PCR workflows enhance reliability, reduce reagent consumption, and improve experimental reproducibility. Furthermore, PCR-based labeling kits are widely accessible, user-friendly, and compatible with multiple downstream applications, solidifying their leadership position. Continuous innovation in polymerase enzymes, fluorescent dyes, and probe technologies further drives adoption across laboratories globally. Growing government and private funding in genomics and biotechnology research, along with increasing collaborations between academic and industrial entities, continues to reinforce PCR labeling as the dominant technique.

Nick translation labelling segment is also the fastest-growing, projected at a CAGR of 9.65% from 2025 to 2032. The growth is driven by increasing applications in next-generation sequencing, gene expression analysis, and RNA studies. Automated and AI-assisted PCR labeling solutions provide high consistency, reduce experimental errors, and allow high-throughput scalability. Rising demand for accurate and rapid diagnostics, pathogen detection, and personalized medicine further accelerates the adoption of PCR-based labeling. Laboratories worldwide are increasingly leveraging PCR-based methods for large-scale studies and clinical applications due to their speed, reliability, and adaptability. Continuous improvements in workflow automation, reagent formulation, and data analytics are enhancing efficiency and reproducibility, fueling sustained growth in this segment globally.

- By Application

On the basis of application, the nucleic acid labelling market is segmented into DNA Sequencing, PCR, FISH, Microarray, In Situ Hybridization, Blotting, and Other Applications. The DNA Sequencing segment dominated the market in 2024 with a revenue share of 28.54%, driven by the increasing adoption of genomics research, personalized medicine, and high-throughput sequencing technologies. Labeled nucleotides are critical for accurate, reproducible, and high-sensitivity results in sequencing workflows. Rising demand for rapid pathogen detection, genomic profiling, and precision diagnostics strengthens the segment’s market position. The segment benefits from advancements in sequencing platforms, improved reagent kits, and the integration of automated workflows, which enhance throughput and reliability. DNA sequencing is central to modern research and diagnostics, enabling scientists and clinicians to conduct comprehensive genomic studies efficiently. The segment’s dominance is further reinforced by increasing investment in genetic research, collaborations between academic and industry players, and the development of novel sequencing techniques. With growing awareness of personalized medicine and genomics applications, the demand for DNA sequencing continues to rise globally, ensuring sustained leadership for this segment.

The FISH application segment is expected to witness the fastest growth at a CAGR of 10.87% from 2025 to 2032, driven by increasing use in clinical diagnostics, cytogenetics, and gene mapping studies. Advancements in fluorescent probes, automation, and AI-assisted analysis tools enable higher throughput, accuracy, and reproducibility. The technique is increasingly adopted in laboratories to study chromosomal abnormalities, gene expression patterns, and molecular interactions. Growing applications in oncology, prenatal diagnostics, and molecular research further accelerate adoption. Automation reduces manual errors and processing times, making FISH more accessible and reliable for large-scale studies. Rising awareness of precision medicine and early disease detection is fueling demand for FISH labeling techniques across research and clinical laboratories worldwide. The flexibility of FISH for multiplexed assays and complex diagnostics workflows contributes to its rapid growth, making it the fastest-growing application segment.

Nucleic Acid Labelling Market Regional Analysis

- North America dominated the nucleic acid labelling market with the largest revenue share of 43.45% in 2024

- The region’s growth is driven by advanced research infrastructure, substantial government and private funding in genomics, and the presence of leading industry players. Increasing demand for next-generation sequencing and molecular diagnostic applications supports market expansion

- The region benefits from extensive R&D investments, collaborations between biotechnology companies and research institutions, and well-established clinical and academic networks, reinforcing its leadership position

U.S. Nucleic Acid Labelling Market Insight

The U.S. nucleic acid labelling market captured the largest revenue share within North America in 2024. Growth is fueled by widespread adoption of advanced labeling technologies, innovations in fluorescent and PCR-based techniques, and rising applications in molecular diagnostics, clinical research, and biopharmaceutical studies. A robust ecosystem of public and private funding, high adoption of laboratory instruments, and strong collaborations between biotech companies, hospitals, and research centers further strengthen the U.S. market.

Europe Nucleic Acid Labelling Market Insight

The Europe nucleic acid labelling market is projected to expand at a substantial CAGR during the forecast period, driven by strict regulatory standards, growing R&D investments, and the increasing need for precise and efficient nucleic acid labeling in diagnostics and research. The region is witnessing significant growth across molecular diagnostics, clinical research, and pharmaceutical applications. Advanced research infrastructure and collaborations between biotechnology companies and research institutions support market expansion.

U.K. Nucleic Acid Labelling Market Insight

The U.K. nucleic acid labelling market is anticipated to grow at a noteworthy CAGR, propelled by increasing genomics research, robust healthcare infrastructure, and rising demand for molecular diagnostics. Expanding government initiatives, high R&D spending, and a strong presence of research institutions contribute to market growth. The country also benefits from well-established academic and clinical research networks that foster the adoption of advanced nucleic acid labeling techniques.

Germany Nucleic Acid Labelling Market Insight

The Germany nucleic acid labelling market is expected to witness considerable growth, driven by strong investment in biotechnology, increasing awareness of molecular diagnostics, and the adoption of innovative labeling technologies. The country’s well-developed research infrastructure, emphasis on innovation, and robust funding mechanisms support market expansion. Collaborative efforts between academic institutions, research centers, and private companies further strengthen the German market.

Asia-Pacific Nucleic Acid Labelling Market Insight

The Asia-Pacific nucleic acid labelling market is expected to be the fastest-growing region in the market during the forecast period, with a projected CAGR of 9.5%. Growth is fueled by expanding genomics research, rising government initiatives in biotechnology, increasing R&D spending, and the growing number of molecular diagnostic laboratories in countries such as China, India, and Japan. Rapid urbanization and technological advancements further enhance market adoption.

Japan Nucleic Acid Labelling Market Insight

The Japan nucleic acid labelling market is witnessing significant market growth due to a strong focus on biotechnology, advanced research infrastructure, and increasing applications in molecular diagnostics. Government support, high R&D investments, and the presence of leading biotechnology companies drive market expansion. Japan’s emphasis on innovative research and clinical studies contributes to widespread adoption of nucleic acid labeling technologies.

China Nucleic Acid Labelling Market Insight

The China nucleic acid labelling market accounted for the largest revenue share in the Asia-Pacific region in 2024. Market growth is driven by expanding genomics research, rising government initiatives, increasing investments in biotechnology, and the growing number of molecular diagnostic laboratories. Rapid urbanization, a large research-focused workforce, and strong domestic manufacturing capabilities further boost the adoption of nucleic acid labeling technologies.

Nucleic Acid Labelling Market Share

The nucleic acid labelling industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Merck KGaA (Germany)

- Agilent Technologies, Inc. (U.S.)

- Takara Bio Inc. (Japan)

- New England Biolabs (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Promega Corporation (U.S.)

- Sigma-Aldrich (U.S.)

- PerkinElmer (U.S.)

- Enzo Biochem Inc. (U.S.)

- GenScript (China)

Latest Developments in Global Nucleic Acid Labelling Market

- In May 2025, TriLink BioTechnologies introduced a new in vitro transcription (IVT) kit featuring CleanCap AG (3′ OMe) for co-transcriptional capping and CleanScribe RNA Polymerase to reduce double-stranded RNA. This kit aims to simplify mRNA synthesis workflows, offering up to twice the mRNA yield and up to 85% lower dsRNA compared to other kits on the market

- In February 2025, TriLink BioTechnologies partnered with Avantorto expand the availability of its nucleic acid products across Europe, the Middle East, and Africa (EMEA). This distribution partnership is expected to improve the ordering process and offer shorter lead times for European customers, increasing access to TriLink’s novel nucleic acid technologies

- In January 2025, Biotium launched the EMBER Ultra RNA and DNA Gel Kits, providing the most sensitive nucleic acid gel staining available. These kits offer time-saving convenience and are designed for efficient penetration and staining of polyacrylamide gels

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.