Global Ocular Carotidynia Market

Market Size in USD Million

USD

18.48 Million

USD

31.32 Million

2024

2032

USD

18.48 Million

USD

31.32 Million

2024

2032

| 2025 - 2032 | |

| USD 18.48 Million | |

| USD 31.32 Million | |

| % | |

|

Ocular Carotidynia Market Size

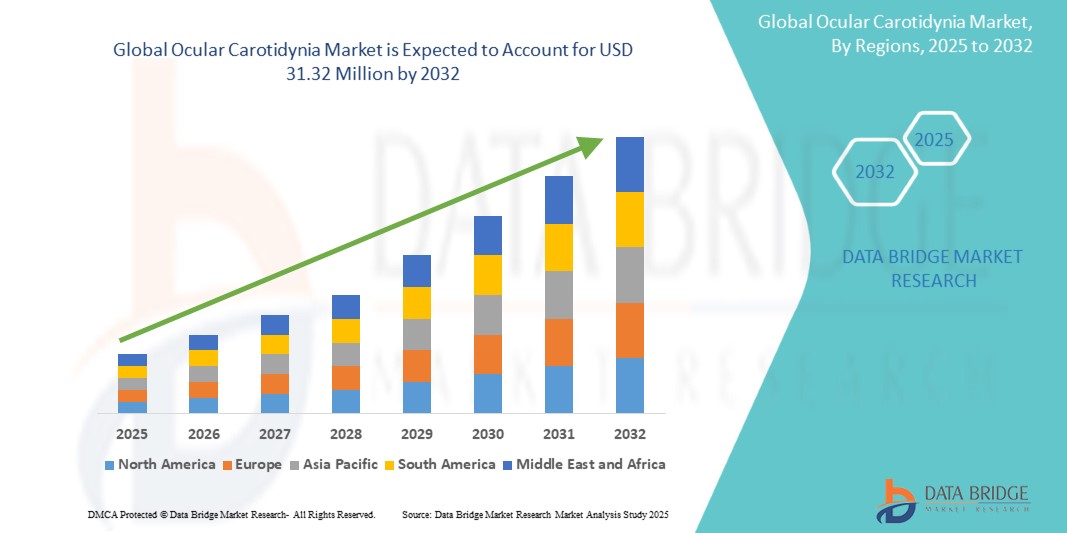

- The global ocular carotidynia market size was valued at USD 18.48 million in 2024 and is expected to reach USD 31.32 million by 2032, at a CAGR of 6.82% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ocular carotidynia and growing awareness among healthcare professionals and patients about early diagnosis and effective management strategies. The rising emphasis on precision diagnosis and treatment is driving the adoption of advanced ocular carotidynia solutions in hospitals and clinics

- Furthermore, increasing demand for accurate, reliable, and patient-friendly diagnostic and therapeutic solutions is establishing ocular carotidynia management systems as a preferred approach in both clinical and research settings. These converging factors are accelerating the uptake of ocular carotidynia solutions, thereby significantly boosting the industry's growth

Ocular Carotidynia Market Analysis

- The Ocular Carotidynia market is witnessing growth due to rising prevalence of ocular vascular disorders, increased awareness among patients and healthcare providers, and advancements in diagnostic technologies for early detection and treatment of carotid-related eye conditions

- The market expansion is further supported by ongoing research and development activities, introduction of innovative imaging modalities, and the growing adoption of minimally invasive interventions for ocular carotidynia

- North America dominated the ocular carotidynia market with the largest revenue share of 45% in 2024, driven by advanced healthcare infrastructure, high awareness of ocular health, and strong presence of leading ophthalmology and diagnostic companies. The U.S. remains the key contributor within the region, experiencing significant growth due to early adoption of innovative diagnostic and therapeutic solutions for ocular carotidynia

- Asia-Pacific is expected to be the fastest-growing region in the ocular carotidynia market during the forecast period, owing to increasing urbanization, rising disposable incomes, and expanding healthcare access in countries like China, India, and Japan. Growing awareness of ocular disorders and investment in healthcare infrastructure are further accelerating market growth

- The hospitals segment dominated the ocular carotidynia market with a market revenue share of 48.7% in 2024, due to the availability of advanced diagnostic equipment, specialized ophthalmologists, and comprehensive treatment facilities. Hospitals cater to both acute and chronic cases, providing multi-disciplinary care for better patient outcomes. High patient volumes, established infrastructure, and the ability to offer end-to-end diagnosis and treatment make hospitals the preferred choice for Ocular Carotidynia care

Report Scope and Ocular Carotidynia Market Segmentation

|

Attributes |

Ocular Carotidynia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ocular Carotidynia Market Trends

Enhanced Diagnostic and Monitoring Capabilities

- A significant and accelerating trend in the global ocular carotidynia market is the adoption of advanced diagnostic and monitoring technologies that enable more precise detection and continuous tracking of symptoms. Innovations in imaging, electrophysiological testing, and automated patient monitoring systems are significantly enhancing the accuracy of diagnosis and the effectiveness of treatment plans

- For instance, high-resolution ocular imaging devices now allow ophthalmologists to visualize subtle vascular and muscular changes associated with Ocular Carotidynia, facilitating earlier intervention and more targeted therapies. Similarly, non-invasive monitoring tools can track patient-reported symptoms and physiological parameters over time, providing clinicians with valuable longitudinal data

- Integration of multi-modal diagnostic systems in clinical practice enables a comprehensive assessment of ocular health, helping differentiate Ocular Carotidynia from similar ophthalmic or neurological conditions. This reduces misdiagnosis and supports personalized treatment strategies

- Automated data analysis and interpretation tools allow healthcare providers to quickly identify patterns and anomalies, enhancing decision-making and reducing the likelihood of human error. The seamless incorporation of these systems into hospital workflows also improves operational efficiency and patient throughput

- The trend toward more precise, real-time monitoring and advanced diagnostics is reshaping patient expectations and standards of care in ophthalmology. Consequently, companies are focusing on developing devices that combine accuracy, reliability, and ease of use to support clinicians and patients alike

- Rising awareness among patients and healthcare professionals about the benefits of early detection and continuous monitoring is driving increased adoption of these technologies across both clinical and research settings. The emphasis on evidence-based management and improved patient outcomes further propels market growth

Ocular Carotidynia Market Dynamics

Driver

Growing Need Due to Rising Awareness and Improved Diagnostic Requirements

- The increasing prevalence of ocular disorders and the growing awareness among healthcare providers and patients about the importance of early diagnosis and treatment are significant drivers for the expansion of the Ocular Carotidynia market. Enhanced understanding of the condition’s impact on vision and overall eye health is encouraging more frequent screening and monitoring

- For instance, in 2024, several leading ophthalmology centers introduced advanced ocular imaging and monitoring protocols specifically targeting Ocular Carotidynia, aimed at improving diagnostic accuracy and treatment outcomes. Such initiatives by key institutions are expected to drive market growth during the forecast period

- As clinicians and patients recognize the benefits of timely intervention, the demand for sophisticated diagnostic and monitoring solutions has surged. These solutions provide high-resolution imaging, real-time monitoring, and comprehensive symptom tracking, offering a substantial improvement over conventional diagnostic approach

- Furthermore, the integration of multi-modal diagnostic devices and software platforms in clinical settings allows for more comprehensive patient assessments, helping differentiate Ocular Carotidynia from similar ocular or neurological disorders. This facilitates personalized treatment planning and better patient outcomes

- The increasing adoption of portable and non-invasive monitoring systems, coupled with advancements in ocular imaging technology, is further driving the market. These tools enable clinicians to track disease progression, evaluate treatment efficacy, and adjust therapeutic strategies in real time

Restraint/Challenge

High Costs of Advanced Diagnostics and Limited Awareness in Emerging Regions

- The relatively high cost of advanced diagnostic and monitoring systems for Ocular Carotidynia can be a significant barrier to widespread adoption, particularly in developing countries or regions with limited healthcare infrastructure

- In addition, limited awareness among certain populations about the symptoms and implications of Ocular Carotidynia may result in delayed diagnosis and underutilization of available diagnostic tools, hindering market growth

- The lack of standardized diagnostic protocols across healthcare facilities can lead to inconsistent detection rates, further restricting the adoption of advanced monitoring systems

- Insufficient training among general ophthalmologists and primary care physicians regarding the latest diagnostic techniques can delay patient referrals to specialized centers, affecting timely treatment

- Addressing these challenges through the development of cost-effective, user-friendly diagnostic devices, training healthcare professionals, and patient education programs is critical for market expansion

- Limited insurance coverage or reimbursement for advanced Ocular Carotidynia diagnostic tests in some regions can deter patients from opting for these solutions, impacting market growth

- Collaborations between device manufacturers, healthcare providers, and government agencies to raise awareness and subsidize equipment costs could significantly accelerate adoption in emerging markets

- Overcoming these barriers will help improve early detection rates, optimize treatment outcomes, and drive long-term growth in the Ocular Carotidynia market

- Continuous investment in research and development to create more compact, portable, and non-invasive monitoring solutions can also boost accessibility and market penetration globally

Ocular Carotidynia Market Scope

The market is segmented on the basis of type, diagnosis method, treatment approach, and application.

• By Type

On the basis of type, the ocular carotidynia market is segmented into acute ocular carotidynia, chronic ocular carotidynia, recurrent ocular carotidynia, and others. The acute ocular carotidynia segment dominated the largest market revenue share of 42.5% in 2024, driven by the high incidence of sudden-onset ocular pain and vascular-related complications that require immediate medical attention. Acute cases are often the first point of clinical intervention, resulting in frequent utilization of advanced diagnostic tools, pharmacological therapies, and hospital-based monitoring. Healthcare providers prioritize acute management due to the potential severity of symptoms and risk of associated ocular or neurological disorders. This segment benefits from established treatment protocols, high patient awareness, and better reimbursement coverage for urgent care. Acute Ocular Carotidynia patients usually undergo repeated consultations, which increases overall healthcare expenditure and market demand.

The chronic ocular carotidynia segment is expected to witness the fastest growth at a CAGR of 19.2% from 2025 to 2032, due to rising awareness of long-term ocular conditions and the need for continuous monitoring. Chronic cases require ongoing care, regular diagnostic evaluations, and long-term pharmacological management. The adoption of lifestyle modification programs, preventive care strategies, and patient education initiatives further fuels growth. As research uncovers new therapeutic options and monitoring technologies, the segment attracts investment from diagnostic and pharmaceutical companies. The increasing prevalence of chronic cases in aging populations is also driving market expansion, as sustained management improves patient quality of life and reduces complications.

• By Diagnosis Method

On the basis of diagnosis method, the ocular carotidynia market is segmented into clinical examination, imaging techniques, blood tests, and others. The clinical examination segment held the largest market share of 44.0% in 2024, owing to its fundamental role in initial diagnosis and patient triage. Physicians rely on thorough ocular examinations, symptom assessments, and patient history to detect Ocular Carotidynia. This method is widely accessible, cost-effective, and highly practical in hospital and clinic settings. Frequent use of clinical examinations for both acute and chronic cases ensures a steady revenue stream. Moreover, clinical examinations are often complemented by other diagnostic procedures to confirm findings, boosting the segment’s overall significance in the market.

The imaging techniques segment is expected to register the fastest CAGR of 18.5% from 2025 to 2032, driven by growing adoption of MRI, CT scans, and other advanced imaging methods for precise evaluation. Imaging helps differentiate Ocular Carotidynia from other vascular or neurological disorders, reducing misdiagnosis. Technological advancements in imaging equipment, higher resolution scans, and faster results make this method increasingly preferred in modern healthcare setups. Rising investments in diagnostic centers and hospital infrastructure further propel this segment. Increasing awareness among healthcare providers about the benefits of accurate imaging for treatment planning also supports rapid adoption.

• By Treatment Approach

On the basis of treatment approach, the ocular carotidynia market is segmented into pharmacological therapy, surgical intervention, lifestyle management, and others. The pharmacological therapy segment dominated the largest market share of 46.3% in 2024, as medications such as analgesics, anti-inflammatory agents, and vasodilators are widely prescribed to manage symptoms effectively. This segment’s growth is supported by standardized treatment protocols, broad patient acceptance, and insurance coverage in several regions. Pharmacological therapy allows rapid symptom relief, reducing hospitalization duration and improving patient outcomes. The segment also benefits from ongoing R&D for new drugs targeting underlying causes and reducing recurrence rates.

The lifestyle management segment is projected to witness the fastest growth at a CAGR of 20.1% during the forecast period. Increasing awareness of preventive care and non-pharmacological interventions, such as stress reduction, eye exercises, dietary adjustments, and ergonomic modifications, is driving adoption. Patients increasingly prefer integrated management strategies combining medication with lifestyle adjustments. Growing patient education initiatives, wellness programs in clinics, and digital health solutions that support lifestyle monitoring are fueling demand. The trend towards holistic care, particularly in chronic cases, ensures that lifestyle management will remain a key growth driver in the Ocular Carotidynia market.

• By Application

On the basis of application, the ocular carotidynia market is segmented into hospitals, clinics, research institutions, and others. The hospitals segment held the largest market revenue share of 48.7% in 2024, due to the availability of advanced diagnostic equipment, specialized ophthalmologists, and comprehensive treatment facilities. Hospitals cater to both acute and chronic cases, providing multi-disciplinary care for better patient outcomes. High patient volumes, established infrastructure, and the ability to offer end-to-end diagnosis and treatment make hospitals the preferred choice for Ocular Carotidynia care.

The clinics segment is expected to witness the fastest CAGR of 17.8% from 2025 to 2032, as outpatient services become more popular for routine diagnosis and follow-up care. Clinics provide easy access, faster appointments, and personalized patient management, making them ideal for recurring monitoring. Rising investments in community healthcare, telemedicine integration, and adoption of portable diagnostic tools are boosting clinic-based care. The segment benefits from increased patient awareness, convenience of local treatment centers, and expansion of specialized ophthalmology practices, driving rapid market growth.

Ocular Carotidynia Market Regional Analysis

- North America dominated the ocular carotidynia market with the largest revenue share of 45% in 2024, driven by advanced healthcare infrastructure, high awareness of ocular health, and strong presence of leading ophthalmology and diagnostic companies

- The region, experiencing significant growth due to early adoption of innovative diagnostic and therapeutic solutions for ocular carotidynia. Investments in state-of-the-art imaging technologies, specialized ophthalmology clinics, and the availability of skilled medical professionals further strengthen the market position

- Continuous research in minimally invasive interventions and improved clinical outcomes is also contributing to the growth of the market in North America

U.S. Ocular Carotidynia Market Insight

The U.S. ocular carotidynia market captured the largest revenue share within North America in 2024, fueled by the increasing prevalence of carotid-related ocular disorders and rising patient awareness. Hospitals and specialized ophthalmology centers are adopting advanced diagnostic modalities, including high-resolution imaging and non-invasive monitoring, to enhance early detection. The strong presence of clinical research organizations and ongoing government initiatives in ocular healthcare are accelerating growth. Furthermore, the development of targeted therapeutic interventions and collaborations between private and public healthcare institutions support the expansion of the U.S. market.

Europe Ocular Carotidynia Market Insight

The Europe ocular carotidynia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing awareness of ocular health, increasing government initiatives for rare disease management, and strong healthcare infrastructure. The presence of leading ophthalmology centers and well-established clinical research facilities is promoting early diagnosis and treatment. European patients are increasingly adopting advanced imaging techniques and minimally invasive therapies. The region is also witnessing growth across hospital networks and specialty clinics, with a focus on improving clinical outcomes and reducing complication rates.

U.K. Ocular Carotidynia Market Insight

The U.K. ocular carotidynia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising patient awareness, the presence of highly specialized ophthalmology facilities, and ongoing government-led healthcare initiatives. Increased focus on early diagnosis, preventive care, and access to innovative treatments is fueling market growth. In addition, collaborations between research institutions and healthcare providers are enhancing therapeutic development and clinical trial adoption.

Germany Ocular Carotidynia Market Insight

The Germany ocular carotidynia market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, innovation-driven ophthalmology research, and government support for rare ocular disease management. Hospitals and specialty clinics are increasingly utilizing high-precision diagnostic tools and adopting minimally invasive treatment approaches. Patient education initiatives, coupled with awareness campaigns, are also driving the demand for timely diagnosis and intervention.

Asia-Pacific Ocular Carotidynia Market Insight

The Asia-Pacific ocular carotidynia market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and expanding healthcare access in countries such as China, India, and Japan. Government initiatives promoting healthcare infrastructure development, rising patient awareness, and the growth of specialty ophthalmology centers are accelerating adoption. Technological advancements in diagnostic imaging and therapeutic procedures further enhance market growth.

Japan Ocular Carotidynia Market Insight

The Japan ocular carotidynia market is gaining momentum due to the country’s focus on advanced healthcare, high patient awareness, and strong adoption of innovative diagnostic technologies. Hospitals and specialized clinics are actively incorporating advanced imaging and treatment solutions for carotid-related ocular conditions. The aging population and emphasis on preventive care are further driving market demand.

China Ocular Carotidynia Market Insight

The China ocular carotidynia market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the expanding healthcare infrastructure, growing middle-class population, and increasing awareness about ocular disorders. The rising number of specialty ophthalmology centers, government-led health initiatives, and availability of advanced diagnostic technologies are key factors propelling market growth. Continuous investment in healthcare facilities and medical training programs is further strengthening the market in China.

Ocular Carotidynia Market Share

The ocular carotidynia industry is primarily led by well-established companies, including:

- Alcon (Switzerland)

- Bausch + Lomb (U.S.)

- Hoya Corporation (Japan)

- Johnson & Johnson and its affiliates (U.S.)

- Zeiss Group (Germany)

- Topcon Corporation (Japan)

- Nidek Co., Ltd. (Japan)

- Essilor International (France)

- F. Hoffmann-La Roche AG (Switzerland)

- Fujifilm Holdings Corporation (Japan)

- Carl Zeiss Meditec AG (Germany)

- Novartis AG (Switzerland)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Lumenis Ltd. (Israel)

- Iridex Corporation (U.S.)

Latest Developments in Global Ocular Carotidynia Market

- In December 2024, a comprehensive review article titled “Transient Perivascular Inflammation of the Carotid Artery as a Poorly Recognized Cause of Neck Pain” was published in Vasa. This article highlighted the underdiagnosis of Transient Perivascular Inflammation of the Carotid Artery (TIPIC) syndrome, commonly known as Ocular Carotidynia or Fay syndrome. It emphasized the need for increased awareness among clinicians to improve diagnosis and management of this rare condition

- In February 2024, a case report was published in Pain Medicine detailing a patient diagnosed with TIPIC syndrome. The report discussed the clinical presentation, diagnostic challenges, and treatment approaches for this rare condition, contributing valuable insights to the medical community

- In July 2023, the University of Southern California's Ostrow School of Dentistry published an article on its website discussing the symptoms, diagnosis, and treatment options for Carotidynia. The article provided an overview of the condition, including its clinical features and management strategies, aimed at educating both healthcare professionals and the public

- In August 2022, an article titled “Carotidynia: Symptoms, Diagnosis, and Treatment Options” was published on the USC Ostrow School of Dentistry's website. The article explored the clinical presentation of Carotidynia, diagnostic approaches, and available treatment modalities, serving as a resource for dental and medical professionals

- In March 2022, a study published in Frontiers in Neurology examined the association between carotid artery disease and ocular manifestations, including Carotidynia. The study provided evidence linking carotid artery pathology with ocular symptoms, enhancing understanding of the systemic nature of the condition

- In May 2021, a research article titled “Carotidynia: Overview of an Uncommon Identification for Unilateral Neck Pain” was published in The Journal of Clinical Neurology. The article reviewed the etiology, clinical presentation, and management of Carotidynia, contributing to the recognition of this rare condition in clinical practice

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.