Global Ocular Giant Cell Arteritis Market

Market Size in USD Million

USD

65.22 Million

USD

115.80 Million

2024

2032

USD

65.22 Million

USD

115.80 Million

2024

2032

| 2025 - 2032 | |

| USD 65.22 Million | |

| USD 115.80 Million | |

| % | |

|

Ocular Giant Cell Arteritis Market Size

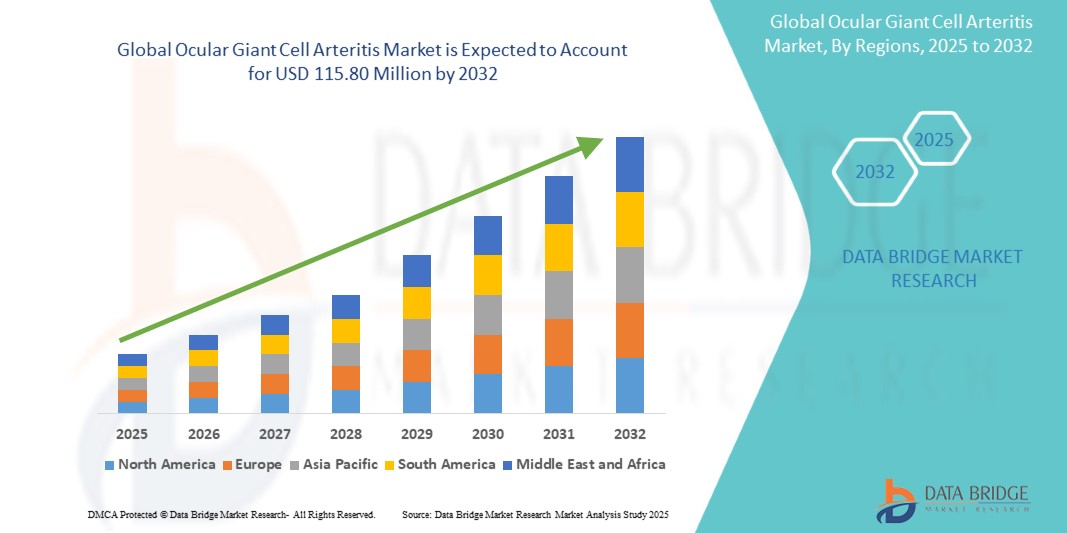

- The global ocular giant cell arteritis market size was valued at USD 65.22 million in 2024 and is expected to reach USD 115.80 million by 2032, at a CAGR of 7.44% during the forecast period

- The market growth is largely fueled by increasing awareness and prevalence of ocular giant cell arteritis (GCA), combined with advances in diagnostic techniques and treatment options, leading to improved patient outcomes and early disease detection

- Furthermore, rising investment in ophthalmology research and the development of novel therapies, such as corticosteroids and biologics, is expanding treatment options and supporting the growth of the ocular giant cell arteritis market

Ocular Giant Cell Arteritis Market Analysis

- Ocular Giant Cell Arteritis, a severe inflammatory condition affecting the arteries of the eye and surrounding structures, is increasingly gaining attention in healthcare due to its potential to cause irreversible vision loss and systemic complications. Hospitals, specialty clinics, and diagnostic centers are emphasizing early detection and effective treatment, making advanced diagnostic and therapeutic solutions critical in both clinical and research settings

- The escalating demand for ocular giant cell arteritis solutions is primarily fueled by the growing prevalence of cranial and large-vessel manifestations, increasing geriatric populations, and rising awareness among healthcare providers and patients. Enhanced imaging techniques, laboratory tests, and biopsy procedures are enabling early diagnosis and precise disease monitoring, further driving adoption across hospitals, specialty clinics, and ambulatory care centers

- North America dominated the ocular giant cell arteritis market with the largest revenue share of 38.5% in 2024, driven by well-established healthcare infrastructure, advanced diagnostic facilities, and high awareness regarding early detection and treatment of ocular and systemic manifestations of giant cell arteritis

- Asia-Pacific is expected to be the fastest-growing region in the ocular giant cell arteritis market during the forecast period, driven by a rising geriatric population, increasing healthcare investments, and growing awareness about ocular health and systemic complications of giant cell arteritis in countries such as China, Japan, and India

- The corticosteroids segment dominated the ocular giant cell arteritis market with a market revenue share of 52% in 2024, reflecting their established role as the first-line therapy to control inflammation and prevent vision-threatening complications

Report Scope and Ocular Giant Cell Arteritis Market Segmentation

|

Attributes |

Ocular Giant Cell Arteritis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ocular Giant Cell Arteritis Market Trends

Enhanced Diagnostic Accuracy and Treatment Personalization

- A significant and accelerating trend in the global ocular giant cell arteritis market is the integration of advanced diagnostic tools and personalized treatment approaches. This combination is significantly enhancing early detection, disease monitoring, and patient-specific therapy selection

- For instance, high-resolution imaging techniques such as optical coherence tomography (OCT) and fluorescein angiography allow ophthalmologists to detect early vascular changes associated with ocular GCA, enabling timely interventions

- The adoption of biomarker-based diagnostics and laboratory assays provides more precise monitoring of inflammatory activity, allowing clinicians to tailor corticosteroid or biologic therapy dosages for individual patients

- Advanced imaging and diagnostic platforms facilitate centralized tracking of disease progression, enabling healthcare providers to make informed decisions and adjust treatment protocols in real time

- This trend towards more accurate, data-driven, and personalized disease management is reshaping clinical expectations for ocular GCA care. Consequently, companies and research institutions are developing novel imaging systems, therapeutic biologics, and combination treatment strategies to improve patient outcomes

- The demand for innovative, reliable, and patient-centric diagnostic and therapeutic solutions is growing rapidly across both hospitals and specialty ophthalmology clinics, as clinicians increasingly prioritize early intervention, safety, and long-term vision preservation

Ocular Giant Cell Arteritis Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Awareness

- The increasing prevalence of ocular giant cell arteritis (GCA) among aging populations, coupled with growing awareness among patients and healthcare providers, is a significant driver for the heightened demand for effective diagnostic and therapeutic solutions

- For instance, in March 2023, Horizon Therapeutics announced the expansion of its research programs focused on rare inflammatory ocular diseases, including ocular GCA, aiming to improve early detection and targeted treatment strategies. Such initiatives by key companies are expected to drive the Ocular Giant Cell Arteritis market growth in the forecast period

- As clinicians become more aware of the potential risks of delayed diagnosis, including vision loss, there is an increasing emphasis on timely interventions and monitoring protocols, which drives the adoption of advanced imaging, laboratory assays, and personalized treatment approaches

- Furthermore, the growing focus on patient-centric care and multidisciplinary management strategies is making integrated diagnostic and therapeutic platforms essential in hospitals and specialty clinics, facilitating coordinated care and improved outcomes

- The convenience of minimally invasive monitoring, precise biomarker-based diagnosis, and targeted therapy administration are key factors propelling the adoption of ocular GCA solutions across healthcare settings. The trend towards early detection, combined with expanding treatment options, further contributes to market growth

Restraint/Challenge

Challenges Related to High Costs and Limited Awareness

- The relatively high cost of advanced diagnostic and therapeutic solutions for ocular GCA can pose a significant challenge to broader market adoption, particularly in developing regions or smaller clinics with limited budgets

- In addition, the lack of widespread awareness among general practitioners and some ophthalmologists about ocular GCA symptoms may result in delayed diagnosis and suboptimal treatment, hindering early intervention efforts

- Addressing these challenges through educational initiatives for healthcare professionals, development of cost-effective diagnostic tools, and expansion of treatment access is crucial for enhancing market penetration. Companies are increasingly focusing on providing validated, easy-to-use, and clinically reliable diagnostic and therapeutic solutions to reassure providers

- While costs are gradually decreasing with technological advancements and improved insurance coverage, the perceived premium for high-quality ocular GCA solutions can still limit adoption, especially in outpatient or community-based healthcare settings

- Overcoming these challenges through awareness campaigns, training programs, and the introduction of more affordable diagnostic and therapeutic solutions will be vital for sustained market growth

Ocular Giant Cell Arteritis Market Scope

The market is segmented on the basis of type, diagnosis, treatment, and end-user.

• By Type

On the basis of type, the ocular giant cell arteritis market is segmented into cranial giant cell arteritis, large vessel giant cell arteritis, systemic giant cell arteritis, and others. The cranial giant cell arteritis segment dominated the largest market revenue share of 45.3% in 2024, driven by its higher prevalence among patients and the critical need for early diagnosis to prevent irreversible vision loss. This type often presents with clear clinical symptoms such as temporal headaches, jaw claudication, and visual disturbances, which prompt rapid medical attention. Clinicians rely heavily on established diagnostic guidelines and immediate corticosteroid treatment to mitigate complications. The segment’s dominance is further reinforced by widespread awareness among ophthalmologists and rheumatologists, increasing hospital adoption, and integration of standardized treatment protocols. In addition, the availability of well-validated diagnostic tools and growing investments in clinical research make Cranial GCA the primary revenue contributor.

The large vessel giant cell arteritis segment is anticipated to witness the fastest growth rate of 22.1% from 2025 to 2032, driven by rising recognition of vascular complications such as aortic aneurysms and stenosis, which necessitate advanced monitoring and management. Increased adoption of non-invasive imaging techniques, enhanced clinician training, and patient awareness campaigns are fueling the rapid uptake of this sub-segment. Furthermore, ongoing research into targeted therapies and early intervention strategies is accelerating market growth across hospitals and specialty clinics.

• By Diagnosis

On the basis of diagnosis, the ocular giant cell arteritis market is segmented into Temporal Artery Biopsy, Laboratory Tests (ESR, CRP), Imaging Techniques (Ultrasound, MRI, PET-CT), and Others. The Temporal Artery Biopsy segment held the largest market revenue share of 48% in 2024, owing to its recognition as the gold standard for definitive diagnosis. This procedure enables direct histological confirmation of inflammation in the temporal artery, providing clinicians with high confidence in treatment planning. Hospitals and specialty clinics adopt this diagnostic approach extensively due to its accuracy and established clinical protocols. The segment’s dominance is further supported by integration with rapid corticosteroid therapy, which is essential to prevent vision loss, and ongoing training programs that ensure high-quality biopsy procedures.

The Imaging Techniques segment is expected to witness the fastest CAGR of 20.4% from 2025 to 2032, propelled by technological advancements in ultrasound, MRI, and PET-CT modalities. These non-invasive imaging solutions allow early detection of large vessel involvement and disease progression without the need for surgical intervention. Adoption is increasing in hospitals and diagnostic laboratories due to the combination of patient comfort, precise visualization of vascular inflammation, and capability for longitudinal monitoring. In addition, rising awareness of the benefits of non-invasive diagnostics among clinicians and patients is contributing to rapid market growth.

• By Treatment

On the basis of treatment, the ocular giant cell arteritis market is segmented into corticosteroids, immunosuppressive drugs, biologics, and others. The corticosteroids segment dominated the largest market revenue share of 52% in 2024, reflecting their established role as the first-line therapy to control inflammation and prevent vision-threatening complications. Hospitals and specialty clinics widely use corticosteroids due to their rapid symptom management, proven efficacy, and alignment with clinical guidelines. High adoption is supported by experienced clinical staff, hospital protocols for early intervention, and the immediate availability of medications for acute cases. The segment continues to benefit from robust research validating dosage strategies and tapering schedules to optimize patient outcomes.

The biologics segment is anticipated to witness the fastest growth rate of 24.6% from 2025 to 2032, driven by increasing approval and adoption of targeted therapies such as IL-6 inhibitors. These therapies offer safer long-term options with fewer systemic side effects, especially for patients intolerant to corticosteroids. Growth is further propelled by clinical trials, expanding specialty clinic adoption, and patient preference for precision-targeted treatments. The segment’s rise is also supported by increased awareness among healthcare providers about biologics’ efficacy in reducing relapse rates and improving long-term quality of life.

• By End-User

On the basis of end-user, the ocular giant cell arteritis market is segmented into hospitals, specialty clinics, ambulatory care centers, and research & diagnostic laboratories. The hospitals segment accounted for the largest market revenue share of 46.7% in 2024, owing to their ability to handle high patient volumes and complex cases requiring immediate intervention. Hospitals benefit from integrated care pathways, access to advanced imaging, laboratory facilities, and multidisciplinary teams capable of rapid diagnosis and treatment. Adoption is reinforced by comprehensive protocols, established clinician expertise, and hospital investment in early detection programs, ensuring sustained market dominance.

The specialty clinics segment is expected to witness the fastest CAGR of 21.8% from 2025 to 2032, driven by focused expertise in ophthalmology and rheumatology, enabling early detection and targeted therapy administration. Specialty clinics are increasingly equipped with advanced diagnostic tools and personalized treatment regimens, catering to patients seeking specialized care. Rising patient awareness of specialized services and the convenience of focused care delivery are key factors contributing to the rapid growth of this sub-segment.

Ocular Giant Cell Arteritis Market Regional Analysis

- North America dominated the ocular giant cell arteritis market with the largest revenue share of 38.5% in 2024

- Driven by well-established healthcare infrastructure, advanced diagnostic facilities, and high awareness regarding early detection and treatment of ocular and systemic manifestations of giant cell arteritis

- Early detection initiatives, effective treatment protocols, and strong support from key healthcare providers further reinforce the region’s leadership position

U.S. Ocular Giant Cell Arteritis Market Insight

The U.S. ocular giant cell arteritis market captured the largest revenue share within North America, fueled by increasing diagnosis rates, availability of advanced imaging modalities such as MRI, PET-CT, and ultrasound, and widespread adoption of corticosteroid and biologic therapies. Specialty clinics and hospitals are focusing on comprehensive patient management, including regular monitoring and follow-up care. Ongoing research in targeted immunosuppressive treatments and increased awareness among ophthalmologists and rheumatologists are also contributing to growth. Government healthcare initiatives, coupled with strong reimbursement policies, support the expansion of diagnostic and treatment services, further propelling the U.S. market.

Europe Ocular Giant Cell Arteritis Market Insight

The Europe ocular giant cell arteritis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of giant cell arteritis among the aging population, improved healthcare infrastructure, and rising investments in diagnostic imaging technologies. European countries are implementing early screening programs and specialized care pathways, encouraging timely diagnosis and treatment. Hospitals and specialty clinics are increasingly adopting advanced laboratory tests, temporal artery biopsy procedures, and imaging techniques to enhance patient outcomes. Regulatory support and patient awareness initiatives further strengthen market growth across the region.

U.K. Ocular Giant Cell Arteritis Market Insight

The U.K. ocular giant cell arteritis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by heightened awareness of ocular and systemic complications associated with giant cell arteritis. The growing geriatric population and government-led healthcare programs for early detection and treatment are encouraging patients to seek specialized care. Hospitals and specialty clinics in the U.K. are expanding their diagnostic capabilities, including high-resolution imaging and laboratory-based testing. Integration of standardized treatment protocols and the availability of biologics and corticosteroids contribute to market expansion.

Germany Ocular Giant Cell Arteritis Market Insight

The Germany ocular giant cell arteritis market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, emphasis on early diagnosis, and increasing prevalence of age-related autoimmune conditions. Hospitals and specialty clinics are focusing on multi-disciplinary approaches combining ophthalmology and rheumatology expertise. Adoption of advanced imaging technologies, laboratory testing methods, and biologic therapies is increasing. Government healthcare policies and patient awareness campaigns further drive demand, supporting the sustained growth of the German market.

Asia-Pacific Ocular Giant Cell Arteritis Market Insight

The Asia-Pacific ocular giant cell arteritis market is poised to grow at the fastest CAGR during the forecast period, driven by a rising geriatric population, increasing healthcare investments, and growing awareness about ocular health and systemic complications of giant cell arteritis in countries such as China, Japan, and India. Expansion of hospital networks, improvement in diagnostic capabilities, and government healthcare initiatives are accelerating market growth across the region. In addition, increasing availability of advanced treatment options, enhanced training for healthcare professionals, and collaborations with international healthcare providers are further supporting market adoption.

Japan Ocular Giant Cell Arteritis Market Insight

The Japan ocular giant cell arteritis market is gaining momentum due to the country’s aging population, high prevalence of ocular complications, and advanced healthcare infrastructure. Hospitals and specialty clinics are adopting state-of-the-art diagnostic techniques, including imaging and laboratory tests, to facilitate early detection and effective patient management. Public awareness campaigns and government-supported health programs contribute to increased patient engagement. The growing demand for personalized treatment approaches and integration of biologic therapies supports continued market growth.

China Ocular Giant Cell Arteritis Market Insight

The China ocular giant cell arteritis market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid expansion of hospital networks, increasing investments in healthcare infrastructure, and rising demand for advanced diagnostic and treatment solutions. Government initiatives promoting ocular health, increased prevalence of geriatric patients, and higher healthcare spending are driving adoption in hospitals and specialty clinics. The availability of advanced imaging modalities, laboratory diagnostics, and targeted therapies, coupled with growing patient awareness, is supporting the country’s rapid market growth.

Ocular Giant Cell Arteritis Market Share

The ocular giant cell arteritis industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Lilly USA, LLC (U.S.)

- Amgen (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Boehringer Ingelheim International GmbH (Germany)

- Bayer AG (Germany)

- AstraZeneca (U.K.)

Latest Developments in Global Ocular Giant Cell Arteritis Market

- In July 2025, Novartis announced that its drug Cosentyx (secukinumab) failed to meet expectations in a late-stage Phase III trial for treating giant cell arteritis. The trial did not demonstrate a significant improvement in achieving sustained remission for patients with newly diagnosed or relapsing GCA, falling short of the positive outcomes observed in an earlier Phase II study. Despite this setback, Novartis emphasized its continued commitment to advancing research and development in the field of immune-mediated diseases

- In April 2025, AbbVie announced that the U.S. Food and Drug Administration (FDA) approved RINVOQ (upadacitinib), 15 mg once daily, for the treatment of adults with giant cell arteritis (GCA). This approval marks RINVOQ as the first and only oral Janus Kinase (JAK) inhibitor approved for GCA in adults. The approval followed positive top-line results from the SELECT-GCA Phase 3 study, which demonstrated that upadacitinib, in combination with a 26-week steroid taper regimen, achieved sustained remission from week 12 to week 52 in adults with GCA

- In April 2024, AbbVie announced positive top-line results from their Phase 3 study of upadacitinib (RINVOQ) for treating giant cell arteritis. The study met its primary endpoint, showing that upadacitinib, combined with a 26-week steroid taper regimen, achieved sustained remission. In addition, key secondary endpoints were also met, demonstrating the drug's potential as a treatment option for GCA

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.