Global Ocular Pain Peribulbar Treatment Market

Market Size in USD Million

USD

9.35 Million

USD

16.09 Million

2024

2032

USD

9.35 Million

USD

16.09 Million

2024

2032

| 2025 - 2032 | |

| USD 9.35 Million | |

| USD 16.09 Million | |

| % | |

|

Ocular Pain Peribulbar Treatment Market Size

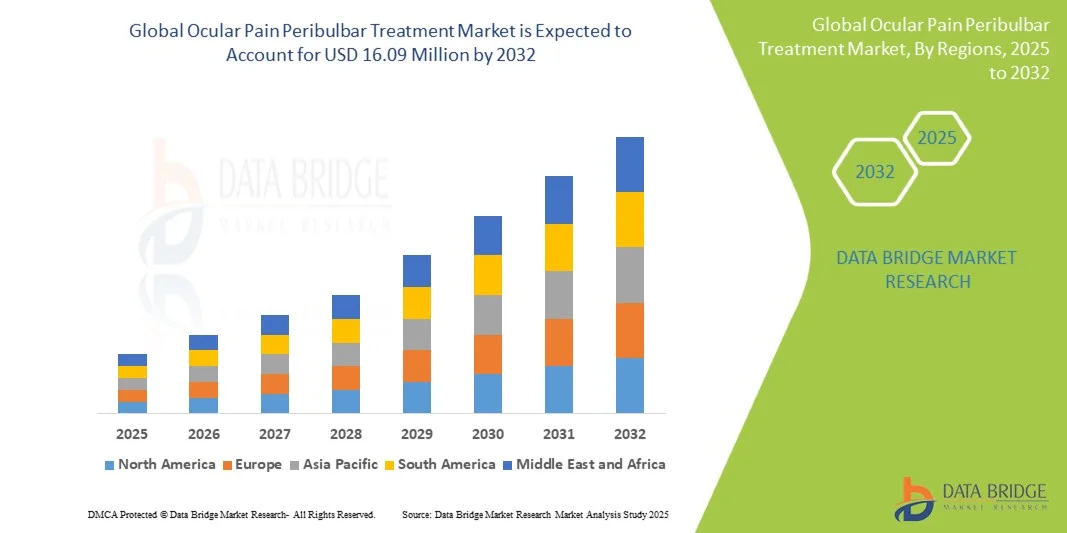

- The global ocular pain peribulbar treatment market size was valued at USD 9.35 Million in 2024 and is expected to reach USD 16.09 Million by 2032, at a CAGR of 7.03% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ocular disorders and the rising demand for effective pain management solutions in ophthalmic care, leading to higher adoption of Peribulbar treatment in both clinical and hospital settings.

- Furthermore, growing awareness among patients and ophthalmologists regarding advanced ocular pain management therapies, combined with technological advancements in drug delivery methods and minimally invasive procedures, is establishing Ocular Pain Peribulbar Treatment as a preferred solution for post-operative and chronic ocular pain. These converging factors are accelerating the uptake of peribulbar treatment solutions, thereby significantly boosting the industry’s growth

Ocular Pain Peribulbar Treatment Market Analysis

- Ocular Pain Peribulbar Treatment, encompassing advanced therapies for managing ocular inflammation and pain, is becoming increasingly vital in both hospital and clinic settings due to its effectiveness in providing targeted relief and improving patient outcome

- The escalating demand for Ocular Pain Peribulbar Treatment is primarily fueled by increasing prevalence of ocular disorders, rising awareness of early diagnosis and treatment, and the growing need for safe and effective pain management options

- North America dominated the ocular pain peribulbar treatment market with the largest revenue share of 48% in 2024, driven by advanced healthcare infrastructure, high disease awareness, and the presence of key pharmaceutical and diagnostic players. The U.S. witnessed substantial growth in diagnosis and treatment adoption, supported by early diagnostic protocols, availability of targeted therapies, and growing patient awareness of ocular disorders

- Asia-Pacific is expected to be the fastest-growing region in the ocular pain peribulbar treatment market during the forecast period due to increasing urbanization, rising disposable incomes, expanding healthcare access, and growing awareness of ocular health in countries such as China, India, and Japan. Improvements in healthcare infrastructure and the adoption of advanced diagnostic and treatment solutions are further driving regional growth

- The injection therapy segment dominated the ocular pain peribulbar treatment market with the largest market revenue share of 52.1% in 2024, due to its targeted delivery of therapeutics directly to the affected ocular region

Report Scope and Ocular Pain Peribulbar Treatment Market Segmentation

|

Attributes |

Ocular Pain Peribulbar Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ocular Pain Peribulbar Treatment Market Trends

“Enhanced Convenience Through Advanced Treatment Approaches”

- A significant and accelerating trend in the global ocular pain subtenon treatment market is the increasing use of targeted and minimally invasive treatment techniques, improving both efficacy and patient comfort. These approaches allow ophthalmologists to manage ocular inflammation and pain more precisely, reducing recovery time and enhancing overall outcomes

- For instance, the adoption of subtenon corticosteroid injections combined with advanced imaging techniques allows clinicians to deliver drugs directly to the affected ocular tissue, minimizing systemic exposure while maximizing therapeutic impact

- The integration of multimodal treatment plans, including immunosuppressive therapy alongside NSAIDs or corticosteroids, is enhancing treatment personalization for patients, allowing better management of chronic and acute ocular pain conditions

- For instance, specialty eye clinics in North America are increasingly using combined therapy protocols that adjust dosages based on patient response, leading to improved visual comfort and reduced inflammation

- With growing awareness among ophthalmologists and patients, Ocular Pain Subtenon Treatment is becoming more accessible in both hospital and clinic settings, facilitating early intervention and reducing long-term complications

Ocular Pain Peribulbar Treatment Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Ocular Disorders and Pain Management Awareness”

- The increasing prevalence of ocular pain conditions, combined with heightened patient awareness about the benefits of early diagnosis and effective pain management, is a significant driver for the market growth

- For instance, in March 2023, several ophthalmic centers in the U.S. launched awareness campaigns highlighting the advantages of timely subtenon corticosteroid injections in preventing chronic ocular pain and complications

- The growing focus on patient-centric care and individualized treatment plans is further fueling demand, as clinicians seek safer, more effective options to address both acute flare-ups and chronic ocular conditions

- Specialty ophthalmic clinics in India have introduced combined therapy regimens with close patient monitoring, significantly improving recovery rates and patient satisfaction

- Enhanced accessibility to advanced treatment options in hospitals and specialty clinics is enabling a larger patient population to receive timely and effective care, thus boosting market growth

Restraint/Challenge

“Concerns Regarding Treatment Costs and Procedure Risks”

- The high cost of advanced ocular pain subtenon treatment procedures and medications can be a barrier to adoption, particularly in developing regions or for patients with limited insurance coverage

- For instance, in late 2022, reports from healthcare providers in Southeast Asia highlighted that the upfront expense of corticosteroid injections and immunosuppressive therapy limited their use among economically disadvantaged patients

- Potential procedure-related complications, such as infection or incorrect drug placement, pose a challenge for clinicians and can limit patient willingness to undergo treatment

- Hospitals in North America have implemented stringent sterilization protocols and imaging-guided injection techniques to mitigate procedural risks, ensuring safer outcomes and improving patient trust

- Overcoming these challenges through cost-reduction strategies, insurance support, and enhanced clinician training will be critical for sustained market growth

- Collaborative programs between pharmaceutical companies and ophthalmology centers in Europe are offering subsidized treatment plans and patient education initiatives, facilitating broader access to Ocular Pain Subtenon Treatment

Ocular Pain Peribulbar Treatment Market Scope

The market is segmented on the basis of type, treatment, diagnosis, and end-users.

• By Type

On the basis of type, the ocular pain peribulbar treatment market is segmented into local anesthetics, corticosteroids, combination therapy, and others. The local anesthetics segment dominated the largest market revenue share of 46.3% in 2024, primarily due to its rapid and reliable pain relief during ocular procedures. Local anesthetics are preferred in hospitals and clinics for their controlled analgesic effect, minimal systemic side effects, and ease of administration. They are widely used in both adult and pediatric ophthalmic care, particularly for peribulbar injections. The segment benefits from strong clinical validation, high physician preference, and extensive availability in treatment facilities. Moreover, its use ensures patient comfort during diagnostic and therapeutic procedures. Growing awareness among healthcare providers about standardized pain management protocols further reinforces demand. In addition, local anesthetics are considered safe for repeated procedures, which is crucial for chronic or recurrent ocular conditions. Hospital and clinic procurement policies favor these agents for their cost-effectiveness and established efficacy. In combination with adjunct therapies, local anesthetics improve overall procedural efficiency. Regulatory approvals and inclusion in treatment guidelines also support widespread adoption, maintaining the segment’s market dominance. The consistent need for pain management in ocular surgeries ensures sustained growth in this segment. Overall, the local anesthetics segment’s clinical reliability, physician acceptance, and broad applicability solidify its leadership position in the market.

The combination therapy segment is expected to witness the fastest CAGR of 18.5% from 2025 to 2032, driven by increasing adoption of integrated treatment approaches for complex ocular pain. Combination therapy, which blends local anesthetics with corticosteroids or other adjuvants, enhances both analgesic and anti-inflammatory effects, providing comprehensive pain management. The approach is gaining traction in specialized ophthalmology centers and pediatric clinics. Clinical studies supporting superior outcomes, especially in chronic or recurrent ocular conditions, are boosting adoption. Healthcare providers are increasingly favoring combination therapies for patients with high sensitivity or comorbidities. Improved formulations allow precise dosing and longer duration of action, enhancing patient comfort and procedural efficiency. The trend toward personalized treatment regimens further supports growth, particularly in hospitals with advanced ophthalmic services. Rising awareness among physicians and patients about enhanced efficacy is also contributing to adoption. In addition, government and institutional guidelines encouraging evidence-based practices are propelling the segment. Combination therapy’s ability to minimize repeat interventions makes it cost-effective in the long term. As more product innovations and formulations enter the market, adoption is expected to accelerate. Overall, these factors collectively drive the segment’s high CAGR in the forecast period.

• By Treatment

On the basis of treatment, the ocular pain peribulbar treatment market is segmented into injection therapy, topical therapy, systemic therapy, and others. The injection therapy segment held the largest market revenue share of 52.1% in 2024, due to its targeted delivery of therapeutics directly to the affected ocular region. This method ensures rapid and sustained pain relief, which is critical in both surgical and diagnostic procedures. Injection therapy is preferred in hospitals and clinics for its precision and predictable clinical outcomes. It is commonly used in adult and pediatric ophthalmology for managing severe or acute ocular pain. Physician familiarity, extensive training programs, and long-standing clinical use support market dominance. The segment benefits from high procedural success rates, reducing the need for repeat interventions. Moreover, injection therapy is adaptable with various pharmacological agents, offering flexibility in pain management. Regulatory approvals and evidence-based guidelines further strengthen adoption. Increasing patient volumes in tertiary care centers reinforce the segment’s growth. Clinical reliability and patient satisfaction drive consistent demand. Advanced techniques in peribulbar administration also enhance safety profiles. Injection therapy’s established efficacy, professional preference, and broad application in ocular care ensure its leadership position.

The topical therapy segment is projected to grow at the fastest CAGR of 17.8% from 2025 to 2032, owing to its non-invasive administration and growing preference for outpatient care. Topical formulations, such as drops or gels, provide localized pain relief with minimal systemic exposure. These treatments are particularly favored for mild-to-moderate ocular pain and post-procedural management. Technological advancements in drug delivery, including sustained-release formulations, improve efficacy and patient compliance. The ease of use allows patients to self-administer, reducing the need for hospital visits. Rising awareness about minimally invasive pain management supports adoption in clinics and ambulatory surgical centers. Increased preference for home-based care and convenience in outpatient settings further propels growth. Topical therapy also complements injection and systemic treatments, expanding its applicability. Expanding insurance coverage and guideline recommendations enhance accessibility. Growing adoption among pediatric and geriatric patients contributes to market momentum. Product innovations focusing on safety and enhanced penetration are supporting growth. Overall, these factors are expected to drive rapid expansion of the topical therapy segment.

• By Diagnosis

On the basis of diagnosis, the ocular pain peribulbar treatment market is segmented into slit lamp examination, tonometry, optical coherence tomography (OCT), fundus photography, and others. The slit lamp examination segment dominated the largest revenue share of 48.5% in 2024, being a fundamental diagnostic tool for evaluating ocular structures prior to peribulbar treatment. Its ability to provide detailed visualization of the anterior segment ensures accurate treatment planning. The segment benefits from wide availability in hospitals and clinics and is essential for both adult and pediatric patient assessments. Clinicians prefer slit lamps for their reliability, ease of use, and ability to detect subtle abnormalities. Training programs and clinical guidelines emphasize its use, supporting continued adoption. The tool allows real-time monitoring during procedures, enhancing patient safety and outcomes. Its affordability and low maintenance requirements further reinforce dominance. Moreover, slit lamp examinations facilitate quick decision-making in urgent care scenarios. Long-standing integration into ophthalmology protocols and extensive physician familiarity solidify the segment’s leading position. Overall, the combination of clinical necessity, proven efficacy, and widespread availability drives market dominance.

The optical coherence tomography (OCT) segment is anticipated to witness the fastest CAGR of 19.2% from 2025 to 2032, owing to its advanced imaging capabilities and rising adoption in specialized ophthalmology centers. OCT allows high-resolution visualization of ocular structures, enabling early detection of complications and precise treatment planning. The technology supports personalized patient management, which is increasingly favored in hospitals and clinics. Rising investment in diagnostic imaging infrastructure and government initiatives promoting advanced ophthalmic care drive adoption. OCT is particularly valuable for monitoring treatment efficacy and post-procedural outcomes. Technological innovations improving image quality and reducing acquisition time enhance usability. Increasing clinician awareness about the benefits of OCT in complex ocular pain cases is further boosting market growth. The tool’s ability to integrate with digital health systems supports centralized patient management. Growing availability in tertiary care centers and specialized clinics expands access. Evidence from clinical studies highlighting superior diagnostic accuracy fuels adoption. Overall, OCT’s technological advantages and clinical relevance underpin its rapid growth.

• By End-Users

On the basis of end-users, the ocular pain peribulbar treatment market is segmented into hospitals, clinics, ambulatory surgical centers, and others. The hospitals segment accounted for the largest revenue share of 55% in 2024, driven by high patient volumes, advanced ophthalmic infrastructure, and availability of specialized care teams. Hospitals offer comprehensive diagnostic and treatment facilities, ensuring complete care from evaluation to post-procedure monitoring. The segment benefits from established procurement channels, trained ophthalmologists, and adherence to clinical guidelines. Hospitals handle both routine and complex ocular pain cases, reinforcing segment dominance. Higher procedure frequency and institutional adoption of standardized protocols further support growth. The segment also benefits from collaborations with pharmaceutical companies for continuous supply of treatment agents. Inpatient care and advanced surgical facilities make hospitals the preferred setting for peribulbar treatment. Long-term partnerships with insurance providers and government support enhance accessibility. Widespread use in tertiary care centers sustains consistent revenue streams. Overall, hospitals’ capacity, infrastructure, and professional expertise secure their leading market position.

The ambulatory surgical centers segment is expected to witness the fastest CAGR of 18% from 2025 to 2032, supported by the increasing shift toward outpatient ophthalmic procedures and patient preference for same-day care. These centers offer cost-effective, convenient, and efficient treatment options for minor and moderate ocular pain cases. Their growing adoption is fueled by rising healthcare awareness, expansion of eye care networks, and technological upgrades in outpatient facilities. Ambulatory surgical centers benefit from lower operational costs, faster patient turnover, and increasing insurance coverage. The convenience and accessibility appeal to both adult and pediatric patients. Integration with advanced diagnostic and treatment equipment enhances procedural accuracy. Clinicians favor these centers for streamlined workflows and focused patient management. Expanding number of specialized ophthalmology centers further propels adoption. Patient education campaigns emphasizing minimally invasive care boost utilization. Overall, these factors collectively drive the rapid growth of ambulatory surgical centers in the peribulbar treatment market.

Ocular Pain Peribulbar Treatment Market Regional Analysis

- North America dominated the ocular pain peribulbar treatment market with the largest revenue share of 48% in 2024, driven by advanced healthcare infrastructure, high disease awareness, and the presence of key pharmaceutical and diagnostic players. The availability of early diagnostic protocols, targeted therapies, and specialized ophthalmic centers facilitated widespread adoption of treatment solutions for ocular pain

- Patients and healthcare providers in the region are increasingly prioritizing early intervention and personalized care, further supporting the market growth.

- Advanced hospital facilities, increasing access to specialty clinics, and a strong focus on patient education about ocular disorders have all contributed to the dominance of North America in this market

U.S. Ocular Pain Peribulbar Treatment Market Insight

The U.S. ocular pain peribulbar treatment market captured the largest revenue share in 2024 within North America, fueled by the increasing adoption of early diagnosis and treatment protocols. Patients are becoming more aware of available treatment options, including corticosteroid injections, NSAIDs, and immunosuppressive therapies. In addition, the presence of specialized ophthalmic centers and the availability of advanced diagnostic tools, such as imaging-guided assessments, are significantly propelling market growth.

Europe Ocular Pain Peribulbar Treatment Market Insight

The Europe ocular pain peribulbar treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of ocular health, a focus on preventive care, and the availability of advanced treatment facilities. Urbanization and the demand for high-quality healthcare services are fostering adoption across hospitals and specialty ophthalmic centers. European patients are increasingly seeking treatments that offer both efficacy and minimal side effects, contributing to market growth across residential and commercial healthcare setups.

U.K. Ocular Pain Peribulbar Treatment Market Insight

The U.K. ocular pain peribulbar treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by rising awareness about ocular disorders and the availability of advanced treatment options in hospitals and clinics. Patients are increasingly seeking timely interventions for both acute and chronic ocular pain conditions. The country’s strong healthcare infrastructure and access to specialty ophthalmic care encourage broader adoption of treatment solutions.

Germany Ocular Pain Peribulbar Treatment Market Insight

The Germany ocular pain peribulbar treatment market is expected to expand at a considerable CAGR during the forecast period, driven by growing awareness of ocular health, access to advanced diagnostic and treatment solutions, and the presence of well-established healthcare facilities. The country’s emphasis on innovative, effective, and safe treatment options supports adoption in hospitals, clinics, and specialty ophthalmic centers.

Asia-Pacific Ocular Pain Peribulbar Treatment Market Insight

The Asia-Pacific ocular pain peribulbar treatment market is expected to be the fastest-growing region during the forecast period due to increasing urbanization, rising disposable incomes, expanding healthcare access, and growing awareness of ocular health in countries such as China, India, and Japan. Improvements in healthcare infrastructure, the availability of advanced diagnostic tools, and the adoption of effective treatment solutions are further driving regional growth.

Japan Ocular Pain Peribulbar Treatment Market Insight

The Japan ocular pain peribulbar treatment market is gaining momentum due to a high level of health awareness, increasing urbanization, and access to advanced ophthalmic care. Patients in Japan are actively seeking timely treatment for ocular pain conditions, supported by well-equipped hospitals and specialty clinics. The focus on patient-centric care and safe, effective therapies is contributing to market growth.

China Ocular Pain Peribulbar Treatment Market Insight

The China ocular pain peribulbar treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the expanding middle class, rapid urbanization, and increasing healthcare access. Rising awareness about ocular disorders, coupled with improvements in hospital infrastructure and the availability of advanced treatment options, has significantly boosted market adoption. China continues to emerge as a major market for Ocular Pain Subtenon treatments, with growth supported by government initiatives promoting better healthcare access and increased investment in ophthalmology services.

Ocular Pain Peribulbar Treatment Market Share

The ocular pain peribulbar treatment industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Bausch + Lomb (U.S.)

- Novartis AG (Switzerland)

- Santen Pharmaceutical Co., Ltd. (Japan)

- F. Hoffmann-La Roche (Switzerland)

- Sun Pharmaceutical Industries Ltd. (India)

- Théa Pharma Inc. (France)

- URSAPHARM Arzneimittel GmbH (Germany)

- Laboratoires Théa (France)

- Ocular Therapeutix, Inc. (U.S.)

- D.Western Therapeutics Institute, Inc. (Japan)

- Kowa Company, Ltd. (Japan)

- Kowa Company, Ltd. (U.S.)

Latest Developments in Ocular Pain Peribulbar Treatment Market

- In May 2025, EyeCool Therapeutics announced promising results from a pilot clinical study evaluating ETX-4143 for chronic ocular surface pain. The study demonstrated a significant reduction in patient-reported pain levels, highlighting its potential as a novel therapeutic approach for managing persistent eye discomfort. Following these results, the company received FDA approval for an investigational device exemption and is planning to initiate pivotal U.S. clinical trials, marking a critical step toward commercialization and broader clinical use

- In June 2025, the U.S. FDA approved Byqlovi (clobetasol propionate ophthalmic suspension) 0.05% for treating postoperative inflammation and pain following ocular surgeries. Harrow acquired the exclusive U.S. commercial rights and is set to launch the product in the fourth quarter of 2025. This approval addresses a significant need for effective pain management after eye procedures, offering ophthalmologists a new option to enhance patient comfort and recovery

- In June 2025, the FDA granted Fast Track designation to urcosimod, an investigational drug aimed at treating neuropathic corneal pain. This designation underscores the urgency and unmet medical need for therapies targeting persistent eye pain caused by nerve damage, allowing for accelerated development and closer regulatory guidance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.