Global Ocular Pain Subconjunctival Treatment Market

Market Size in USD Billion

USD

20.23 Billion

USD

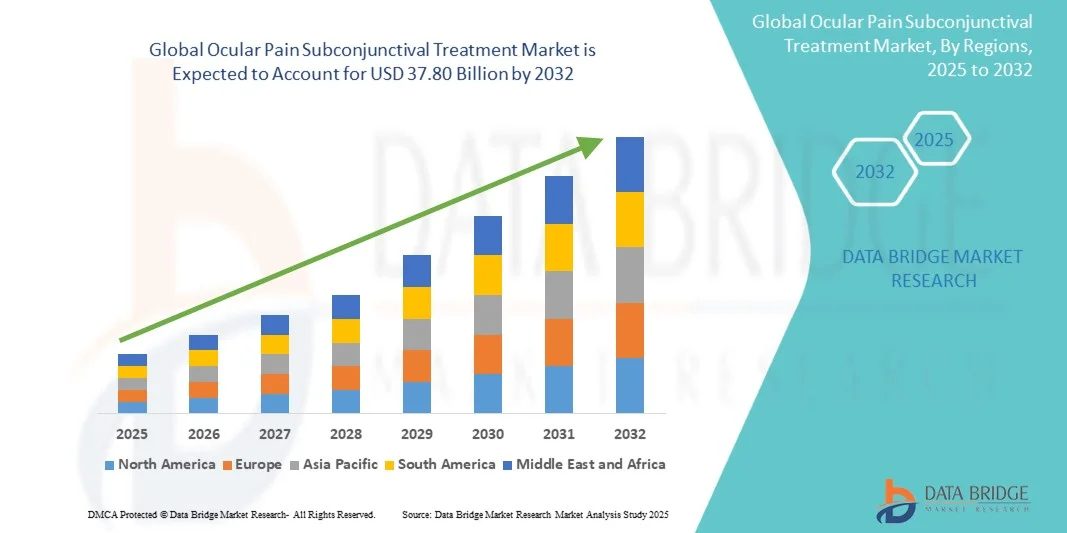

37.80 Billion

2024

2032

USD

20.23 Billion

USD

37.80 Billion

2024

2032

| 2025 - 2032 | |

| USD 20.23 Billion | |

| USD 37.80 Billion | |

| % | |

|

Ocular Pain Subconjunctival Treatment Market Size

- The global ocular pain subconjunctival treatment market size was valued at USD 20.23 billion in 2024 and is expected to reach USD 37.80 billion by 2032, at a CAGR of 8.13% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ocular disorders and the rising adoption of advanced ophthalmic therapies, leading to greater utilization of Ocular Pain Subconjunctival Treatment solutions in both clinical and outpatient settings

- Furthermore, growing patient demand for effective, rapid-acting, and minimally invasive pain management options is driving the adoption of Ocular Pain Subconjunctival Treatment, with healthcare providers increasingly integrating these therapies into standard ophthalmic care pathways. These converging factors are accelerating the uptake of Ocular Pain Subconjunctival Treatment solutions, thereby significantly boosting the industry's growth

Ocular Pain Subconjunctival Treatment Market Analysis

- The Ocular Pain Subconjunctival Treatment market encompasses therapies and interventions designed to manage and relieve pain associated with the subconjunctival region of the eye, including minimally invasive drug delivery and targeted pharmacological solutions

- The escalating prevalence of ocular disorders, coupled with advancements in ophthalmic therapies, is driving the growth of the Ocular Pain Subconjunctival Treatment market, as patients and healthcare providers increasingly seek targeted and effective pain management solutions.

- North America dominated the ocular pain subconjunctival treatment market with the largest revenue share of 40.06% in 2024, supported by advanced healthcare infrastructure, early adoption of novel ocular therapies, and a strong presence of key pharmaceutical and biotechnology players. The U.S. experienced substantial growth due to the availability of specialized ophthalmic clinics, increased patient access to advanced treatments, and rising awareness of ocular pain management

- Asia-Pacific is expected to be the fastest-growing region in the Ocular Pain Subconjunctival Treatment market during the forecast period, driven by increasing healthcare access, rising disposable incomes, and the expansion of specialty eye care centers in countries such as India, China, and Japan

- The Hospitals segment dominated the ocular pain subconjunctival treatment market with a market revenue share of 50% in 2024, due to the presence of advanced ophthalmic surgery units, trained staff, and comprehensive patient monitoring capabilities

Report Scope and Ocular Pain Subconjunctival Treatment Market Segmentation

|

Attributes |

Ocular Pain Subconjunctival Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ocular Pain Subconjunctival Treatment Market Trends

Rising Focus on Targeted Ocular Pain Subconjunctival Therapies

- A notable trend in the global ocular pain subconjunctival treatment market is the increasing development and adoption of targeted therapies that deliver drugs directly to the subconjunctival space, enhancing treatment efficacy while minimizing systemic side effects

- For instance, pharmaceutical companies are advancing formulations such as corticosteroid injections and analgesic implants specifically designed for subconjunctival administration to manage post-surgical inflammation and ocular pain effectively

- These targeted approaches allow precise drug delivery, improving bioavailability at the affected site and reducing the need for repeated systemic medication

- Pharma firms are also exploring sustained-release delivery systems and biodegradable implants to provide longer-lasting effects, enhancing patient compliance and reducing treatment burden

- Innovation in formulation and administration methods is driving the development of more convenient and effective treatment options, making subconjunctival therapy increasingly preferred among ophthalmologists and eye care specialists

- The growing pipeline of novel therapies, combined with increased awareness among patients and clinicians regarding post-surgical and chronic ocular pain management, is further accelerating adoption of these treatments

- Overall, the trend toward targeted, minimally invasive, and patient-friendly subconjunctival therapies is significantly shaping market growth, as companies focus on improving outcomes while enhancing safety and convenience

Ocular Pain Subconjunctival Treatment Market Dynamics

Driver

Growing Need Due to Rising Prevalence of Ocular Disorders and Increasing Adoption of Advanced Treatments

- The increasing incidence of ocular conditions causing subconjunctival pain, coupled with rising awareness about specialized ophthalmic care, is a significant driver for the heightened demand for ocular pain subconjunctival treatments

- For instance, in April 2024, leading ophthalmic centers introduced advanced subconjunctival therapies, incorporating minimally invasive delivery systems and targeted pharmacological solutions. Such strategies by key players are expected to drive the Ocular Pain Subconjunctival Treatment industry growth in the forecast period

- As patients and healthcare providers increasingly seek effective and targeted solutions for ocular pain management, advanced subconjunctival treatments offer benefits such as rapid pain relief, reduced systemic side effects, and enhanced precision compared to traditional therapies

- Furthermore, the growing adoption of specialized eye care programs and the integration of novel drug formulations into clinical practice are strengthening the acceptance of subconjunctival treatment option

- The convenience of targeted drug delivery, improved patient outcomes, and reduced recovery time are key factors propelling the adoption of these therapies in both hospital and outpatient settings. The trend towards personalized ophthalmic care and the increasing availability of user-friendly treatment protocols further contribute to market growth

Restraint/Challenge

Concerns Regarding Treatment Accessibility and High Initial Costs

- Challenges such as limited access to specialized eye care centers and the relatively high cost of advanced subconjunctival therapies pose a barrier to widespread adoption, particularly in developing regions or among cost-sensitive patient groups

- In some regions, the lack of trained ophthalmic specialists and specialized equipment has delayed the implementation of novel treatment protocols, affecting market penetration

- Addressing these challenges through expanded healthcare infrastructure, patient education, and more affordable treatment alternatives is crucial for sustaining market growth. Companies and healthcare providers are focusing on streamlining delivery systems and optimizing treatment protocols to make therapies more accessible and cost-effective

- While prices are gradually stabilizing and generic options are emerging, the perceived premium of advanced ocular pain treatments can still hinder adoption, especially in areas with limited healthcare resources

- Overcoming these challenges through improved accessibility, awareness campaigns, and the development of cost-effective ocular pain subconjunctival treatment options will be vital for sustained growth of the market

Ocular Pain Subconjunctival Treatment Market Scope

The market is segmented on the basis of drug type, route of administration, and application.

• By Type

On the basis of type, the ocular pain subconjunctival treatment market is segmented into Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Corticosteroids, Analgesics, and Others. The Corticosteroids segment dominated the largest market revenue share of 42% in 2024, driven by their established efficacy in reducing ocular inflammation and post-surgical pain. Corticosteroids are widely preferred by ophthalmologists due to their rapid onset of action, ability to manage moderate to severe pain, and extensive clinical validation. The availability of multiple formulations, including sustained-release implants and injection solutions, further enhances their adoption. Hospitals and specialty clinics rely on corticosteroids for precise and predictable outcomes. Patient awareness and positive treatment outcomes contribute to their continued dominance. Advanced drug delivery technologies and regulatory approvals also support market stability for corticosteroids. The segment’s prevalence in post-operative care ensures consistent demand globally.

The NSAIDs segment is expected to witness the fastest CAGR of 20% from 2025 to 2032, fueled by growing preference for non-steroidal therapies that minimize systemic side effects. NSAIDs are increasingly adopted in outpatient procedures and for patients who are steroid-sensitive. Emerging formulations such as topical drops and subconjunctival injections improve bioavailability and patient compliance. Clinical studies highlighting their efficacy in pain management and inflammation control support faster adoption. Physicians are integrating NSAIDs into combination therapies for enhanced post-surgical outcomes. The oral and injectable administration options for NSAIDs further facilitate flexible treatment strategies. Regulatory approvals in key markets encourage broader usage. Technological advancements and growing patient demand for safer alternatives drive segment growth.

• By Route of Administration

On the basis of route of administration, the ocular pain subconjunctival treatment market is segmented into Subconjunctival, Topical, Injectable, and Others. The Injectable segment dominated the largest market revenue share of 46% in 2024, owing to its direct delivery to the affected ocular site, ensuring rapid therapeutic effects and improved pain control. Injectable formulations allow precise dosing, longer duration of action, and high patient adherence under clinical supervision. Hospitals and ambulatory surgical centers extensively use injectable treatments for post-operative pain management. The segment benefits from widespread physician familiarity, strong clinical evidence, and high adoption in specialized ophthalmic care centers. Supportive infrastructure and patient monitoring programs reinforce its market dominance. Regulatory backing and proven safety profiles enhance confidence among healthcare providers. The use of injectables is particularly prevalent in complex ocular procedures, solidifying its market leadership.

The Subconjunctival segment is anticipated to witness the fastest CAGR of 21% from 2025 to 2032, driven by the increasing focus on targeted drug delivery to improve efficacy while minimizing systemic exposure. Subconjunctival administration allows localized, sustained drug release, reducing the need for repeated dosing. It is gaining traction in both hospital and specialty clinic settings, especially for post-surgical and chronic ocular pain management. Innovations in biodegradable implants and sustained-release formulations are fueling faster adoption. Patient preference for minimally invasive procedures supports segment growth. Clinical trials and successful outcomes further encourage physician confidence. Healthcare providers are increasingly recommending this route for improved precision and reduced adverse effects. Growing awareness and training programs enhance adoption rates globally.

• By Application

On the basis of application, the ocular pain subconjunctival treatment market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others. The Hospitals segment accounted for the largest market revenue share of 50% in 2024, due to the presence of advanced ophthalmic surgery units, trained staff, and comprehensive patient monitoring capabilities. Hospitals provide a controlled environment for administering intracameral treatments, ensuring accurate dosing and safety. Specialized ophthalmology departments and post-operative care programs reinforce hospital dominance. Access to a wide patient base and multidisciplinary care teams drives consistent treatment adoption. Hospitals also benefit from strong insurance coverage and government support. Established supply chains and infrastructure support reliable drug availability. Clinical expertise and adherence to standardized treatment protocols further strengthen the hospital segment.

The Specialty Clinics segment is expected to witness the fastest CAGR of 22% from 2025 to 2032, driven by the expansion of outpatient eye care centers and increased patient preference for convenient, focused care. Specialty clinics provide streamlined access to targeted ocular pain treatments, enabling rapid interventions and personalized care. Growth in ambulatory surgical procedures and the rise of eye care chains contribute to faster adoption. Clinics offer flexible scheduling, reduced wait times, and focused post-operative follow-ups. Advanced drug delivery systems and patient education programs enhance clinic-based treatment uptake. Market penetration is further boosted by rising awareness of minimally invasive therapies. The segment’s efficiency and patient-centric approach support robust growth during the forecast period.

Ocular Pain Subconjunctival Treatment Market Regional Analysis

- North America dominated the ocular pain subconjunctival treatment market with the largest revenue share of 40.06% in 2024

- Supported by advanced healthcare infrastructure, early adoption of novel ocular therapies, and a strong presence of key pharmaceutical and biotechnology players

- The region’s growth is largely fueled by the availability of specialized ophthalmic clinics, increasing patient access to advanced treatment options, and rising awareness of effective ocular pain management solutions

U.S. Ocular Pain Subconjunctival Treatment Market Insight

The U.S. ocular pain subconjunctival treatment market captured the largest revenue share in 2024 within North America, driven by the widespread adoption of advanced ocular therapies, including novel formulations for targeted pain management. The expansion of specialty eye care centers and outpatient clinics, coupled with increasing patient enrollment in ocular pain management programs, is propelling the market forward. Moreover, rising awareness among patients and healthcare providers regarding the benefits of minimally invasive subconjunctival treatments is significantly contributing to market growth.

Europe Ocular Pain Subconjunctival Treatment Market Insight

The Europe ocular pain subconjunctival treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising prevalence of ocular disorders, stringent healthcare regulations, and increasing adoption of advanced therapeutic interventions. Countries across the region are witnessing growth in both hospital and outpatient ophthalmic services, with enhanced treatment protocols and improved patient care driving demand.

U.K. Ocular Pain Subconjunctival Treatment Market Insight

The U.K. ocular pain subconjunctival treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing awareness about ocular pain management and the rising adoption of advanced therapies in clinical practice. The country’s well-established healthcare system and growing patient access to specialized eye care solutions further stimulate market growth.

Germany Ocular Pain Subconjunctival Treatment Market Insight

The Germany ocular pain subconjunctival treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing prevalence of ocular conditions, strong healthcare infrastructure, and an emphasis on advanced, evidence-based ophthalmic therapies. The integration of modern treatment approaches in both hospitals and specialty clinics is enhancing patient outcomes and driving adoption.

Asia-Pacific Ocular Pain Subconjunctival Treatment Market Insight

The Asia-Pacific ocular pain subconjunctival treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare access, rising disposable incomes, and expansion of specialty eye care centers in countries such as India, China, and Japan. Government initiatives promoting advanced ophthalmic care and investment in healthcare infrastructure are further supporting market growth across the region.

Japan Ocular Pain Subconjunctival Treatment Market Insight

The Japan ocular pain subconjunctival treatment market is gaining momentum due to the country’s high awareness of ocular health, rapid urbanization, and rising adoption of advanced ophthalmic therapies. An aging population and increasing patient focus on targeted ocular pain management are expected to drive demand in both hospitals and outpatient care settings.

China Ocular Pain Subconjunctival Treatment Market Insight

The China ocular pain subconjunctival treatment market accounted for the largest revenue share in Asia-Pacific in 2024, supported by expanding healthcare infrastructure, government-led ophthalmic initiatives, and growing adoption of advanced subconjunctival therapies. Increasing patient awareness, coupled with the rising number of specialty eye care centers and accessible treatment options, is propelling market growth across both urban and semi-urban regions.

Ocular Pain Subconjunctival Treatment Market Share

The Ocular Pain Subconjunctival Treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Novartis AG (Switzerland)

- Alcon Inc. (Switzerland)

- Bausch + Lomb (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- EyePoint Pharmaceuticals, Inc. (U.S.)

- Ocular Therapeutix, Inc. (U.S.)

- KALA BIO (U.S.)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Nicox (France)

Latest Developments in Global Ocular Pain Subconjunctival Treatment Market

- In May 2025, EyeCool Therapeutics announced positive results from a pilot study of its investigational device, ETX-4143, designed to treat chronic ocular surface pain. The device gently cools the surface of each eye, targeting myelinated long ciliary nerves associated with ocular pain. Patients experienced immediate relief that improved over subsequent weeks. The study demonstrated a favorable safety profile and statistically significant reduction in eye pain severity

- In May 2025, Alcon announced the FDA approval of TRYPTYR (acoltremon ophthalmic solution) 0.003% for the treatment of dry eye disease. This first-in-class TRPM8 receptor agonist stimulates corneal sensory nerves to increase natural tear production. While primarily indicated for dry eye disease, this approval reflects ongoing innovation in ophthalmic treatments

- In January 2025, the FDA approved Journavx (suzetrigine) 50 mg oral tablets for the treatment of moderate to severe acute pain in adults. This first-in-class non-opioid analgesic targets a pain-signaling pathway involving sodium channels in the peripheral nervous system, before pain signals reach the brain. Journavx offers a non-addictive alternative to traditional opioids for acute pain management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.