Global Off Grid Controller Market

Market Size in USD Billion

USD

2.41 Billion

USD

6.27 Billion

2024

2032

USD

2.41 Billion

USD

6.27 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.41 Billion | |

| USD 6.27 Billion | |

| % | |

|

Off-Grid Controller Market Size

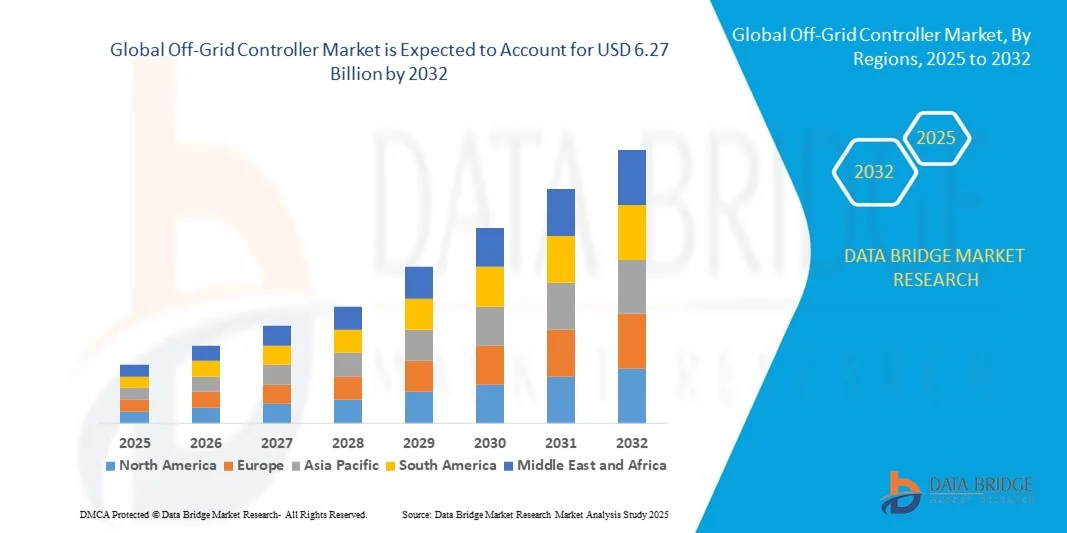

- The global off-grid controller market size was valued at USD 2.41 billion in 2024 and is expected to reach USD 6.27 billion by 2032, at a CAGR of 12.70% during the forecast period

- The market growth is largely fuelled by the increasing adoption of renewable energy systems, such as solar and wind, in remote and rural areas where grid connectivity is limited

- Rising government initiatives and incentives for off-grid energy solutions, coupled with advancements in energy storage and management technologies, are further supporting market expansion

Off-Grid Controller Market Analysis

- Growing demand for reliable and efficient off-grid energy systems in residential, commercial, and industrial applications is driving the development of advanced controllers with improved performance and monitoring capabilities

- Technological innovations, including IoT-enabled and smart controllers, are enhancing system efficiency, remote monitoring, and real-time energy management, making off-grid solutions more accessible and cost-effective

- North America dominated the off-grid controller containers market with the largest revenue share of 38.50% in 2024, driven by a growing demand for reliable decentralized power solutions and increasing awareness of renewable energy adoption

- Asia-Pacific region is expected to witness the highest growth rate in the global off-grid controller market, driven by increasing adoption of renewable energy solutions, technological advancements in smart controllers, and government support for off-grid and decentralized power projects

- The Maximum Power Point Tracking segment held the largest market revenue share in 2024 driven by its higher energy conversion efficiency and ability to optimize power output from solar panels. MPPT controllers are particularly preferred for both residential and commercial off-grid installations as they enhance system performance and reduce energy losses

Report Scope and Off-Grid Controller Market Segmentation

|

Attributes |

Off-Grid Controller Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Off-Grid Controller Market Trends

Rise of Smart And Modular Off-Grid Controller Solutions

- The growing adoption of smart off-grid controllers is transforming the energy management landscape by enabling real-time monitoring and control of decentralized power systems. The portability and programmability of these controllers allow for immediate adjustments, especially in remote or off-grid locations, resulting in improved energy efficiency and reduced operational costs. In addition, advanced analytics and predictive algorithms help anticipate energy demand, optimize storage usage, and minimize system downtime, further enhancing performance and reliability

- The high demand for reliable power management in rural and under-served regions is accelerating the deployment of modular and solar-integrated off-grid controllers. These solutions are particularly effective where grid access is limited, helping optimize energy usage and ensure uninterrupted power supply. In addition, these controllers support hybrid energy integration, enabling seamless operation with solar panels, wind turbines, and backup generators, which improves system flexibility and adoption

- The affordability and user-friendly interface of modern off-grid controllers are making them attractive for both small-scale and commercial installations, leading to enhanced energy management. Consumers and businesses benefit from easier system integration and lower maintenance costs, which ultimately improves operational reliability. In addition, scalable configurations allow controllers to adapt to growing energy needs and changing consumption patterns, offering long-term value and operational efficiency

- For instance, in 2023, several solar mini-grid projects in Sub-Saharan Africa reported increased uptime and reduced energy wastage after implementing intelligent off-grid controllers developed by regional technology providers. These controllers enabled better load balancing and predictive maintenance, improving system performance and user satisfaction. In addition, real-time monitoring dashboards allowed operators to identify faults quickly, reduce energy losses, and maintain consistent power supply to end users

- While smart off-grid controllers are accelerating energy efficiency and reliability, their impact depends on continued innovation, technical support, and scalability. Manufacturers must focus on IoT integration, modular platforms, and renewable energy compatibility to fully capitalize on growing demand. In addition, continuous firmware updates and remote management capabilities ensure improved longevity, adaptability, and alignment with evolving energy management standards

Off-Grid Controller Market Dynamics

Driver

Increasing Demand for Reliable Power Supply and Renewable Energy Integration

- The rise in energy demand and adoption of renewable sources is pushing businesses and households to implement off-grid controllers that optimize energy storage and consumption. This leads to significant cost savings and reduced carbon footprint, encouraging investment in smart energy technologies. In addition, improved energy monitoring and reporting help meet environmental compliance and sustainability targets, enhancing adoption

- Energy service providers are increasingly aware of the operational benefits associated with intelligent controllers, including load management, fault detection, and predictive maintenance. This awareness is driving higher adoption across residential, commercial, and industrial sectors. In addition, enhanced interoperability with smart meters, energy management platforms, and mobile applications allows providers to deliver efficient services and reduce operational complexity

- Government programs and international initiatives supporting rural electrification and sustainable energy are fostering investments in off-grid solutions. From subsidized solar projects to regulatory frameworks, supportive policies are enabling faster deployment of advanced controllers. In addition, financial incentives such as grants, tax credits, and low-interest loans encourage end-users and providers to adopt advanced off-grid systems, boosting market growth

- For instance, in 2022, several Asian and African governments launched programs to integrate smart off-grid controllers with solar mini-grids, boosting adoption among rural households and small businesses. In addition, public-private partnerships facilitated capacity building, technical training, and localized manufacturing, further improving deployment efficiency and accessibility

- While operational cost savings and regulatory support are driving the market, challenges such as infrastructure readiness, technical expertise, and system interoperability must be addressed for long-term adoption. In addition, integration with legacy systems and ensuring cybersecurity for connected controllers remain critical for reliable and safe operations

Restraint/Challenge

High Cost Of Advanced Controllers And Limited Technical Expertise In Rural Areas

- The high price of sophisticated off-grid controllers, including IoT-enabled and AI-integrated systems, limits accessibility for small-scale users and remote installations. Capital-intensive investments remain a significant barrier to widespread deployment. In addition, high upfront costs may delay adoption despite long-term operational savings, discouraging small businesses and households from immediate implementation

- Many rural and under-served regions lack trained personnel capable of installing, operating, or maintaining advanced off-grid controllers. The absence of technical support and local service infrastructure further reduces adoption. In addition, inadequate knowledge transfer and training programs result in improper usage, system inefficiencies, and reduced overall reliability of energy systems

- Supply chain challenges, including availability of compatible components and timely replacement parts, can hinder system performance and reliability. Variability in local energy conditions and environmental factors may increase operational complexity and costs. In addition, import dependencies, logistical delays, and component scarcity in remote regions exacerbate deployment challenges, slowing market growth

- For instance, in 2023, several rural energy projects in Southeast Asia and Africa reported delays in deploying off-grid controllers due to insufficient technical support, fragmented supply chains, and high installation costs. In addition, system downtime, lack of monitoring tools, and limited access to repair services negatively impacted energy availability and project outcomes

- While off-grid controller technologies continue to evolve, addressing cost, technical expertise, and supply chain limitations is crucial. Market stakeholders must focus on modular solutions, training programs, and localized support to expand adoption and ensure sustainable growth. In addition, fostering partnerships with local manufacturers, distributors, and service providers can strengthen the ecosystem, reduce costs, and enhance market penetration

Off-Grid Controller Market Scope

The off-grid controller market is segmented on the basis of type, stage, size, and voltage

- By Type

On the basis of type, the off-grid controller market is segmented into Pulse Width Modulation, Maximum Power Point Tracking, and Others. The Maximum Power Point Tracking segment held the largest market revenue share in 2024 driven by its higher energy conversion efficiency and ability to optimize power output from solar panels. MPPT controllers are particularly preferred for both residential and commercial off-grid installations as they enhance system performance and reduce energy losses.

The Pulse Width Modulation segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its affordability, simplicity, and reliable performance for small-scale solar and off-grid applications. PWM controllers are particularly popular for ease of integration, low maintenance requirements, and suitability in regions with moderate solar conditions, making them an attractive option for cost-conscious consumers.

- By Stage

On the basis of stage, the market is segmented into Stage I, Stage II, and Stage III. Stage II controllers held the largest market revenue share in 2024 due to their balanced performance, providing both protection and efficient energy management in off-grid systems. Stage II controllers are commonly used in medium-capacity solar and hybrid energy systems for households and small businesses.

The Stage III segment is expected to witness the fastest growth rate from 2025 to 2032, driven by advanced functionalities, including remote monitoring, load management, and fault detection. Stage III controllers are particularly effective for large-scale installations and commercial projects, offering scalable solutions and integration with smart energy platforms.

- By Size

On the basis of size, the market is segmented into 10A, 20A, 30A, 40A, and 60A. The 20A segment held the largest market revenue share in 2024 due to its suitability for small to medium off-grid setups, providing efficient energy management without excessive investment. These controllers are commonly deployed in residential solar systems and small commercial mini-grids.

The 60A segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing adoption of large-capacity off-grid installations and commercial solar projects. High-capacity controllers allow for better load handling, improved energy distribution, and support for multiple power sources in complex off-grid setups.

- By Voltage

On the basis of voltage, the market is segmented into 12V, 24V, and 48V. The 24V segment held the largest market revenue share in 2024 driven by its compatibility with mid-sized off-grid systems and wide adoption in solar and hybrid energy projects. 24V controllers offer balanced performance, improved energy efficiency, and lower line losses.

The 48V segment is expected to witness the fastest growth rate from 2025 to 2032, driven by high-capacity off-grid applications and industrial installations requiring robust energy management. 48V controllers are particularly popular for commercial mini-grids, large-scale solar projects, and hybrid energy systems, providing superior performance and reliability.

Off-Grid Controller Market Regional Analysis

- North America dominated the off-grid controller containers market with the largest revenue share of 38.50% in 2024, driven by a growing demand for reliable decentralized power solutions and increasing awareness of renewable energy adoption

- Consumers and businesses in the region highly value the efficiency, modularity, and real-time monitoring capabilities offered by off-grid controller containers, enabling optimized energy management in remote locations

- This widespread adoption is further supported by strong government incentives for renewable energy projects, technological advancements, and rising investments in rural electrification, establishing off-grid controller containers as a preferred solution for residential, commercial, and industrial applications

U.S. Off-Grid Controller Containers Market Insight

The U.S. off-grid controller containers market captured the largest revenue share in 2024 within North America, fueled by rapid deployment of solar mini-grids and microgrid systems. Businesses and households are increasingly prioritizing energy reliability and system efficiency through advanced controller solutions. The growing trend of smart energy management, combined with rising adoption of IoT-integrated controllers and modular systems, further propels the market. Moreover, supportive federal and state-level initiatives promoting renewable energy and sustainable power solutions are significantly contributing to market expansion.

Europe Off-Grid Controller Containers Market Insight

The Europe market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by stringent energy efficiency regulations and rising demand for decentralized power systems in both urban and remote areas. The increase in renewable energy projects, coupled with government incentives and rising awareness regarding energy sustainability, is fostering adoption. European consumers and enterprises are also drawn to the flexibility, scalability, and energy optimization features of modern off-grid controller containers. The region is experiencing significant growth across residential, commercial, and industrial applications.

U.K. Off-Grid Controller Containers Market Insight

The U.K. market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing government initiatives supporting off-grid energy solutions and the growing need for reliable backup power in rural and urban regions. In addition, concerns regarding power outages and energy security are encouraging households and businesses to adopt modular controller systems. The UK’s emphasis on clean energy and smart grid integration, alongside its robust renewable energy infrastructure, is expected to continue driving market growth.

Germany Off-Grid Controller Containers Market Insight

The Germany market is expected to witness the fastest growth rate from 2025 to 2032, fueled by rising awareness of energy efficiency, technological advancement, and the adoption of renewable power systems. Germany’s focus on sustainable energy solutions, coupled with well-established infrastructure and incentives for rural electrification, promotes the adoption of off-grid controller containers. Integration with solar and battery storage systems is increasingly prevalent, with strong preference for scalable, modular, and eco-friendly solutions aligning with consumer and industrial expectations.

Asia-Pacific Off-Grid Controller Containers Market Insight

The Asia-Pacific market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, India, and Japan. The region's growing inclination towards renewable energy, supported by government initiatives promoting rural electrification and sustainability, is driving adoption. Furthermore, APAC emerging as a hub for manufacturing off-grid controller systems and components is increasing affordability and accessibility, expanding the consumer base.

Japan Off-Grid Controller Containers Market Insight

The Japan market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s advanced technological landscape, rapid urbanization, and strong emphasis on energy security. The adoption of off-grid controller containers is driven by the integration with solar and microgrid systems, supporting both residential and commercial energy needs. In addition, Japan’s focus on energy efficiency and smart infrastructure is boosting demand for modular and IoT-enabled controller solutions.

China Off-Grid Controller Containers Market Insight

The China market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s rapid industrialization, expanding rural electrification programs, and high adoption of renewable energy solutions. China stands as one of the largest markets for off-grid energy management systems, and off-grid controller containers are increasingly deployed across residential, commercial, and industrial applications. The push towards smart grids and affordable modular solutions, alongside strong domestic manufacturing capabilities, are key factors propelling the market.

Off-Grid Controller Market Share

The Off-Grid Controller industry is primarily led by well-established companies, including:

- ABB (Switzerland)

- Schneider Electric (France)

- Canadian Solar (Canada)

- ENGIE (France)

- SunPower Corporation (U.S.)

- Trina Solar (China)

- REC Solar Holdings AS (Norway)

- SOLARWATT (Germany)

- ENF Ltd (China)

- Wuxi Suntech Power Co., Ltd. (China)

- JA SOLAR Technology Co., Ltd (China)

- Saur Energy (India)

- Hanwha Group (South Korea)

- M-KOPA Kenya (Kenya)

- Oolu LLC (Senegal)

- Yaskawa – Solectria Solar (U.S.)

- Delta Electronics, Inc. (Taiwan)

- SMA Solar Technology AG (Germany)

- Jinko Solar (China)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Off Grid Controller Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Off Grid Controller Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Off Grid Controller Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.