Global Office Based Surgical Product Market

Market Size in USD Billion

USD

1.81 Billion

USD

3.36 Billion

2024

2032

USD

1.81 Billion

USD

3.36 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.81 Billion | |

| USD 3.36 Billion | |

| % | |

|

Office-Based Surgical Product Market Size

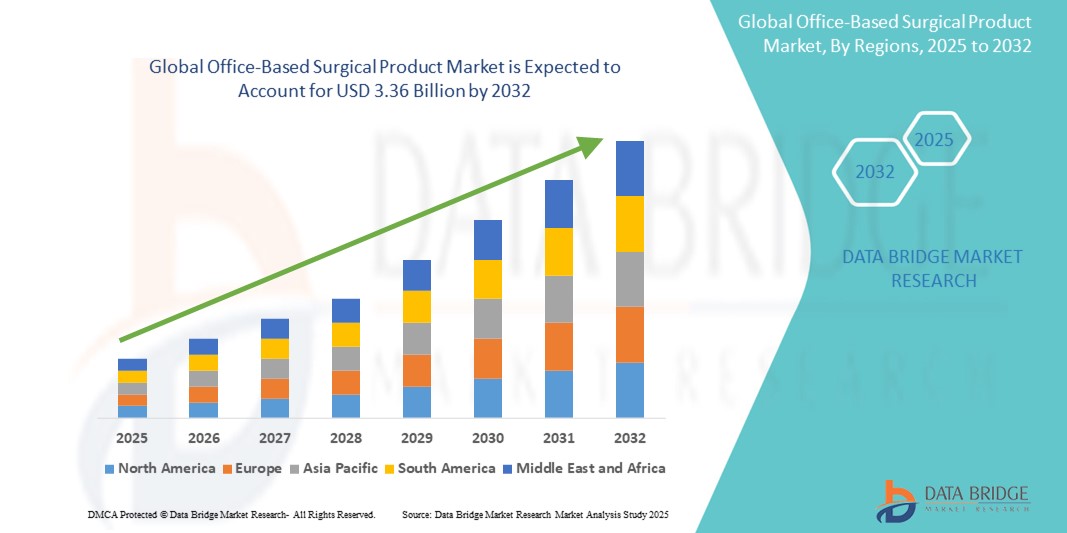

- The global Office-Based Surgical Product market size was valued at USD 1.81 billion in 2024 and is expected to reach USD 3.36 billion by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing shift from hospital-based procedures to office-based surgeries, supported by advancements in minimally invasive technologies and enhanced surgical instrumentation. These trends are making office-based surgical settings more viable and cost-effective, leading to broader adoption across dermatology, gynecology, ophthalmology, ENT, and other specialties

- Furthermore, rising patient preference for outpatient care, shorter recovery times, and reduced healthcare costs are establishing office-based surgical products as essential components in modern ambulatory care. These converging factors are accelerating the uptake of Office-Based Surgical Product solutions, thereby significantly boosting the industry's growth

Office-Based Surgical Product Market Analysis

- Office-based surgical products, comprising instruments, devices, and consumables used in minimally invasive and routine outpatient procedures, are becoming vital components in modern healthcare delivery due to their cost-effectiveness, convenience, and reduced need for hospital infrastructure. These products enable clinics to perform procedures such as dermatological surgeries, cataract removals, and minor orthopedic treatments more efficiently

- The rising demand for office-based surgical products is primarily driven by the growing preference for outpatient care, rising procedural volumes due to aging populations, advancements in medical technology, and increasing cost pressures on healthcare systems worldwide

- North America dominated the office-based surgical product market with the largest revenue share of 41.6% in 2024, owing to well-established healthcare infrastructure, favorable reimbursement policies, and high adoption rates of minimally invasive surgical technologies. The U.S. remains the key contributor, with strong procedural growth in dermatology, ophthalmology, and gynecology clinics, supported by continuous innovation from leading medical device manufacturers

- Asia-Pacific is expected to be the fastest-growing region in the office-based surgical product market during the forecast period, projected to grow at a CAGR of 9.2% from 2025 to 2032, due to rapidly expanding healthcare access, urbanization, and growing investment in primary and ambulatory care settings across countries such as China, India, and Southeast Asia

- The portable segment dominated the office-based surgical product market with a revenue share of 57.6% in 2024, attributed to the flexibility and mobility it offers for healthcare practitioners working in limited-space settings. These devices are particularly useful for multi-room or small-practice offices where mobility is essential

Report Scope and Office-Based Surgical Product Market Segmentation

|

Attributes |

Office-Based Surgical Product Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Office-Based Surgical Product Market Trends

“Growing Shift Toward Minimally Invasive and Outpatient Procedures”

- A significant and accelerating trend in the global office-based surgical product market is the rising preference for minimally invasive procedures performed in outpatient and office-based settings. This shift is largely driven by advancements in surgical tools, reduced patient recovery times, and cost-effectiveness compared to inpatient hospital surgeries

- For instance, dermatological and ophthalmic procedures have seen an upsurge in demand due to the availability of compact and specialized instruments that allow physicians to perform surgeries in clinical settings without the need for hospitalization

- The evolution of energy-based devices, endoscopy systems, and compact surgical imaging tools is enabling specialists in ENT, gynecology, and general surgery to conduct a wide array of interventions safely within office-based surgical suites

- Furthermore, healthcare payers and government bodies are encouraging the adoption of outpatient care due to its potential to reduce healthcare system burdens. As a result, there is increased investment in mobile surgical kits and sterilization-compatible instruments designed specifically for office use

- With rising patient awareness and the growing demand for same-day procedures, device manufacturers are focusing on ergonomic, reusable, and portable solutions to meet the operational needs of office-based facilities

- The market is also benefiting from the rising number of ambulatory surgical centers (ASCs) and physician-owned clinics worldwide, particularly in North America and Asia-Pacific, which are accelerating the use of office-based surgical products across various specialties

Office-Based Surgical Product Market Dynamics

Driver

“Rising Demand Due to Advancements in Ambulatory Care and Office-Based Settings”

- The growing preference for minimally invasive procedures and the shift toward outpatient care are significant drivers fueling the demand for office-based surgical products. These procedures reduce hospital stays and associated costs, making them increasingly attractive to both patients and providers.

- For instance, in April 2024, Johnson & Johnson MedTech introduced a new line of portable electrosurgical units tailored for office-based dermatology and ENT procedures, showcasing the industry's commitment to device miniaturization and accessibility. Such innovations are expected to drive the Office-Based Surgical Product market in the coming years.

- Increased awareness among physicians regarding the clinical and economic benefits of performing minor surgeries in office settings—such as lower infection risks, faster patient turnover, and reduced overhead costs—is encouraging greater adoption of specialized surgical tools and devices.

- Furthermore, the expanding availability of high-performance, portable devices that can be seamlessly integrated into compact clinical spaces is enabling broader utilization across dermatology, gynecology, ophthalmology, and ENT practices.

- In addition, factors such as faster recovery times, reduced procedural costs, and growing insurance support for office-based interventions are significantly enhancing the market uptake of these solutions

Restraint/Challenge

“Concerns Regarding Equipment Costs and Clinical Training Barriers”

- The relatively high initial cost of specialized office-based surgical devices compared to traditional instruments can pose a barrier for small or newly established clinics. Budget constraints may delay upgrades or limit the ability to adopt comprehensive surgical systems

- For instance, advanced ophthalmic lasers or anesthesia monitoring systems used in outpatient settings often require substantial upfront investment and may not be economically feasible for solo practitioners

- Furthermore, effective use of these technologies often demands specialized clinical training and operational expertise. Inadequate training programs or resistance to adopting new technologies among older practitioners can slow down market penetration

- Regulatory complexities and compliance requirements can also create hesitation among physicians transitioning from hospital to office-based practices

- Overcoming these hurdles will require industry players to offer cost-effective device bundles, extended financing options, and robust technical training and after-sales support tailored for small to mid-sized clinics

Office-Based Surgical Product Market Scope

The market is segmented on the basis of product, application, modality, and distribution channel.

- By Product

On the basis of product, the office-based surgical product market is segmented into defibrillators, ventilation devices, vital sign monitoring devices, crash carts, resuscitation equipment, anaesthesia devices, and others. The defibrillators segment dominated the largest market revenue share of 28.9% in 2024, owing to their critical role in emergency cardiovascular care across office-based surgical settings. The growing prevalence of cardiac conditions and the need for rapid response equipment are driving demand for compact and efficient defibrillator units in outpatient procedures.

The anaesthesia devices segment is projected to witness the fastest CAGR of 21.2% from 2025 to 2032, supported by the rising number of minor surgeries performed in office settings and the increasing preference for minimally invasive procedures that still require anesthesia support. Technological advances in portable anesthesia systems are further contributing to their adoption.

- By Application

On the basis of application, the market is segmented into ENT, ophthalmology, dermatology, gynaecology, and others. The dermatology segment accounted for the largest market revenue share of 26.3% in 2024, driven by a surge in cosmetic and aesthetic procedures such as mole removal, skin resurfacing, and laser treatments that are often conducted in office-based settings.

The gynaecology segment is anticipated to grow at the fastest CAGR of 20.4% from 2025 to 2032, fueled by the rising demand for in-office hysteroscopies, colposcopies, and minor gynecological surgeries, reducing patient turnaround time and healthcare costs.

- By Modality

On the basis of modality, the market is segmented into portable and installed. The portable segment held the dominant revenue share of 57.6% in 2024, attributed to the flexibility and mobility it offers for healthcare practitioners working in limited-space settings. These devices are particularly useful for multi-room or small-practice offices where mobility is essential.

The installed segment is expected to register a steady CAGR during the forecast period due to its usage in high-throughput practices or where space constraints are not a concern.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tenders, retail sales, and others. Direct tenders accounted for the largest market revenue share of 48.7% in 2024, driven by bulk purchasing by healthcare facilities, cost efficiency, and long-term service contracts offered by manufacturers.

The retail sales segment is expected to witness the fastest CAGR of 19.3% from 2025 to 2032, owing to the increasing demand from smaller clinics and private practices purchasing specific surgical equipment through online or direct retail platforms for quicker deployment.

Office-Based Surgical Product Market Regional Analysis

- North America dominated the office-based surgical product market with the largest revenue share of 41.6% in 2024, driven by a rising shift of minor surgical procedures to outpatient settings and the growing preference for office-based interventions due to reduced hospital stays and cost-effectiveness

- The market is further supported by favorable reimbursement scenarios, technological advancements in minimally invasive equipment, and the increasing establishment of physician-owned office-based surgical suites

- The high adoption of patient-centric care models and the demand for convenient, low-risk procedures in dermatology, ophthalmology, gynecology, and pain management are strengthening the regional market

U.S. Office-Based Surgical Product Market Insight

The U.S. office-based surgical product market captured the largest revenue share of 71% in 2024 within North America, fueled by a mature healthcare infrastructure and an increasing volume of outpatient surgeries performed in office settings. Physicians are adopting advanced surgical tools, portable diagnostic systems, and compact electrosurgical units that enable them to conduct procedures more efficiently in private practice environments. Rising demand for quick turnaround and reduced healthcare costs is accelerating the transition from hospitals to office-based facilities.

Europe Office-Based Surgical Product Market Insight

The Europe office-based surgical product market is projected to grow at a substantial CAGR during the forecast period, driven by healthcare reforms encouraging decentralization of surgical services and the growing adoption of ambulatory care models. Countries such as Germany, the U.K., and France are investing in advanced equipment for specialist clinics, dermatology centers, and ENT practices to facilitate office-based procedures. Technological innovation, patient preference for local access to care, and the push toward operational efficiency are fostering growth.

U.K. Office-Based Surgical Product Market Insight

The U.K. office-based surgical product market is anticipated to witness steady growth, driven by the increasing number of minor procedures conducted outside hospitals. Growing investments in private surgical clinics and demand for efficient dermatology, podiatry, and aesthetic treatments are supporting this trend. Government efforts to relieve pressure on NHS hospitals by promoting day surgeries and outpatient procedures are contributing significantly to the market's expansion.

Germany Office-Based Surgical Product Market Insight

The Germany office-based surgical product market is expected to expand at a robust CAGR during the forecast period, supported by the country’s strong medical device manufacturing base and emphasis on technological integration. Demand for outpatient surgery continues to grow in response to aging demographics, efficiency mandates, and reimbursement structures that favor cost-saving solutions. Office-based procedures are becoming increasingly common in specialties such as ophthalmology, pain therapy, and ENT.

Asia-Pacific Office-Based Surgical Product Market Insight

The Asia-Pacific office-based surgical product market is poised to register the fastest CAGR of 9.2% from 2025 to 2032, driven by rapid urbanization, growing healthcare expenditure, and rising access to ambulatory and specialty clinics across countries like China, India, and Japan. Increasing government initiatives to improve outpatient infrastructure and cost-effective care delivery are creating a favorable landscape. A shift toward decentralized care models, combined with the affordability of compact and locally manufactured devices, is propelling market expansion.

Japan Office-Based Surgical Product Market Insight

The Japan office-based surgical product market is gaining momentum, supported by the country’s focus on innovation, aging population, and preference for high-precision, minimally invasive surgical options. Office-based procedures in urology, ophthalmology, and cosmetic dermatology are rising, as physicians leverage advanced imaging and diagnostic tools suited for smaller clinics. The cultural preference for efficiency, safety, and quality is driving adoption.

China Office-Based Surgical Product Market Insight

The China office-based surgical product market held the largest revenue share in Asia Pacific in 2024, attributed to an expanding middle class, rapid healthcare infrastructure development, and strong support for outpatient care models. Growth in private clinics, dermatology centers, and specialty practices—paired with favorable policies encouraging community-level treatment—is fueling demand for compact and affordable surgical tools. Local manufacturers are playing a key role in accelerating access to office-based solutions across both urban and semi-urban settings.

Office-Based Surgical Product Market Share

The office-based surgical product industry is primarily led by well-established companies, including:

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Intuitive Surgical (U.S.)

- Boston Scientific Corporation (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- Smith + Nephew (U.K.)

- Zimmer Biomet (U.S.)

- Cook (U.S.)

- Hologic, Inc. (U.S.)

- Terumo Corporation (Japan)

- BD (U.S.)

- KLS Martin Group (Germany)

- Arthrex, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

Latest Developments in Global Office-Based Surgical Product Market

- In March 2025, Johnson & Johnson MedTech introduced the DUALT Energy System, a multi‑modal electrosurgical platform that integrates monopolar, bipolar, ultrasonic, and advanced bipolar energy into one unit, and is managed via the Polyphonic Fleet digital device management system

- In April 2025, Johnson & Johnson MedTech completed the first clinical procedures using its OTTAVA Robotic Surgical System for gastric bypass surgery at Memorial Hermann–Texas Medical Center—marking a major milestone ahead of FDA De Novo submission

- In July 2025, Zimmer Biomet announced it will acquire Monogram Technologies for approximately USD 177 million, adding semi‑autonomous and fully autonomous surgical robotics—including a recently FDA‑approved semi‑autonomous knee replacement system—to its product portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.