Global Oil Gas Fabrication Market

Market Size in USD Billion

USD

90.20 Billion

USD

126.32 Billion

2024

2032

USD

90.20 Billion

USD

126.32 Billion

2024

2032

| 2025 - 2032 | |

| USD 90.20 Billion | |

| USD 126.32 Billion | |

| % | |

|

Oil Gas Fabrication Market Size

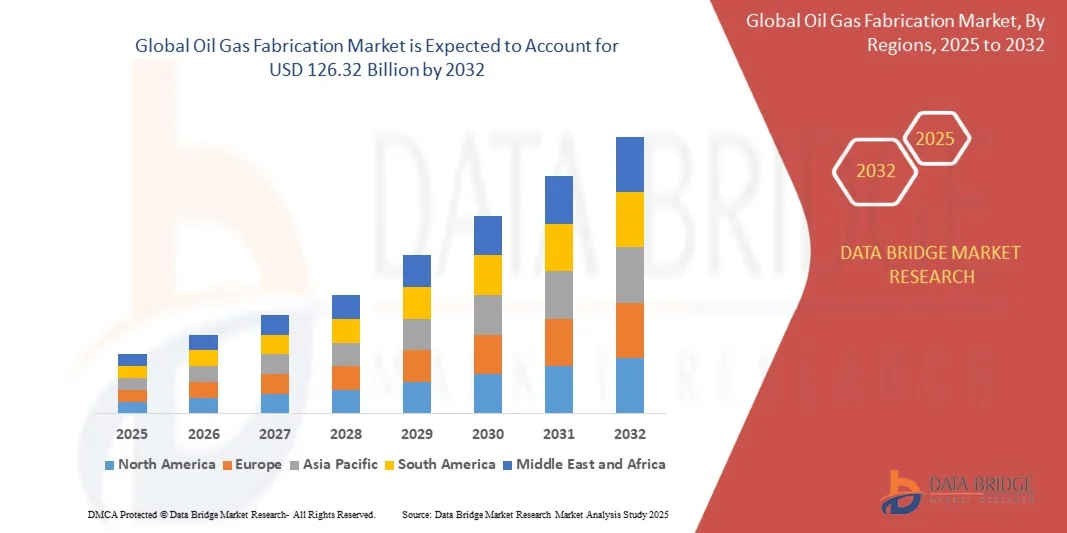

- The global oil gas fabrication market size was valued at USD 90.2 billion in 2024 and is expected to reach USD 126.32 billion by 2032, at a CAGR of 4.30% during the forecast period

- The market growth is largely fueled by increasing investments in both onshore and offshore oil & gas infrastructure, driven by rising global energy demand and the need to replace aging assets. Growing exploration and production activities, particularly in deepwater and ultra-deepwater fields, are creating substantial opportunities for fabrication of modular platforms, FPSOs, pipelines, and processing units

- Furthermore, technological advancements in fabrication processes, including modular construction, automated welding, and advanced steel and composite materials, are enabling faster project execution and higher operational efficiency. These innovations, combined with increasing demand for high-quality, durable, and safety-compliant structures, are accelerating the uptake of advanced fabrication solutions, thereby significantly boosting the market's growth

Oil Gas Fabrication Market Analysis

- Oil & gas fabrication, encompassing the design, construction, and assembly of platforms, pipelines, and storage facilities, is increasingly vital for the development of energy infrastructure worldwide. The ability to deliver large-scale, high-precision fabrication projects ensures continuity of production and minimizes operational downtime for operators

- The escalating demand for offshore and onshore fabrication solutions is primarily fueled by ongoing global energy expansion, deepwater exploration initiatives, and government-backed infrastructure projects. Rising environmental and safety regulations are further encouraging the adoption of technologically advanced and sustainable fabrication methods

- North America dominated the oil gas fabrication market with a share of over 35% in 2024, due to the presence of advanced oilfield infrastructure and strong investments in both onshore and offshore projects

- Asia-Pacific is expected to be the fastest growing region in the oil gas fabrication market during the forecast period due to increasing exploration activities, offshore developments, and investments in LNG projects in countries such as China, India, and Australia increasing exploration activities, offshore developments, and investments in LNG projects in countries such as China, India, and Australia

- Steel segment dominated the market with a market share of 60.5% in 2024, due to its high strength-to-weight ratio, versatility, and cost-effectiveness for both onshore and offshore structures. Steel fabrication supports modular construction and rapid deployment of platforms, pipelines, and processing units, making it a preferred choice for operators worldwide. Its widespread availability and established fabrication techniques further reinforce dominance, ensuring reliability and ease of maintenance

Report Scope and Oil Gas Fabrication Market Segmentation

|

Attributes |

Oil Gas Fabrication Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Oil Gas Fabrication Market Trends

“Growth of Modular and Offshore Fabrication Solutions”

- The oil and gas fabrication market is undergoing a strong transformation driven by the growing adoption of modular and offshore fabrication solutions. Rising project complexity, cost constraints, and the need for faster execution timelines are pushing companies to adopt modular construction and prefabricated units that can be easily assembled on-site

- For instance, McDermott International and Kiewit Corporation have expanded their offshore fabrication yards to serve major oil and gas projects across North America and the Middle East. These companies are developing integrated fabrication facilities capable of handling large-scale modules for offshore platforms, LNG terminals, and refining infrastructure

- The shift toward modular fabrication is helping energy companies reduce on-site labor requirements, improve quality control, and shorten project delivery times. This approach allows multiple project components to be fabricated simultaneously in controlled environments, leading to improved efficiency and reduced risk of weather-related delays

- In addition, the increasing focus on offshore exploration and production activities, especially in regions such as the Gulf of Mexico and the North Sea, is driving demand for specialized offshore fabrication solutions. These include topside modules, subsea structures, and floating production storage and offloading (FPSO) components designed for deep-water operations

- Growing collaboration between engineering, procurement, and construction (EPC) contractors and fabrication service providers is enabling seamless integration between design, procurement, and manufacturing stages. This synergy enhances overall project performance while meeting stringent safety and environmental compliance standards

- The trend toward modularization and offshore fabrication is expected to continue expanding, supported by advancements in digital design tools, automation technologies, and global energy transition strategies. These developments are redefining cost efficiency and productivity benchmarks in oil and gas infrastructure development

Oil Gas Fabrication Market Dynamics

Driver

“Rising Global Energy Demand and Infrastructure Expansion”

- The growing global demand for energy and continuous investment in oil and gas infrastructure are major drivers fueling the expansion of the fabrication market. Increasing consumption of oil, natural gas, and LNG across developing and developed economies is generating significant demand for advanced fabrication capabilities

- For instance, companies such as Saipem and Hyundai Heavy Industries are securing large engineering and fabrication contracts for LNG and offshore platform projects in regions such as the Middle East, Africa, and East Asia. These projects are creating substantial opportunities for fabrication yards to expand capacity and integrate advanced technologies

- The development of new refineries, pipeline networks, and terminals is increasing the requirement for precision-engineered modules and structural components. Fabrication companies are upgrading their facilities to handle heavy lifting, complex welding, and high-strength steel production to meet these growing infrastructure needs

- In addition, governments and private investors are accelerating energy infrastructure modernization initiatives to ensure supply security and resilience. This is stimulating steady demand for integrated fabrication services covering design, assembly, and installation support for onshore and offshore developments

- As the global energy landscape continues to evolve with rising consumption and technological innovation, fabrication companies that focus on high-capacity, efficient, and safety-compliant production capabilities are poised to capture significant growth opportunities over the forecast period

Restraint/Challenge

“High Capital Costs and Regulatory Complexity”

- The oil and gas fabrication market faces considerable challenges arising from the high capital costs associated with infrastructure development and compliance with stringent regulatory standards. Establishing and maintaining large fabrication facilities involves significant investment in equipment, skilled labor, and safety systems

- For instance, companies such as Petrofac and National Petroleum Construction Company have reported substantial financial allocations toward upgrading fabrication yards to meet evolving offshore and environmental safety standards. These investments, while essential, can strain profitability, particularly during periods of oil price volatility

- Complex regulatory frameworks governing environmental safety, emissions control, and labor laws further increase operational complexity. Compliance often requires continual audits, facility certifications, and adherence to international construction standards, slowing project execution timelines

- The volatility of raw material prices and global supply chain disruptions adds to cost uncertainties, making budgeting and scheduling more difficult. Smaller fabrication firms face increasing difficulty competing with large-scale players that possess broader financial and technical resources

- To mitigate these challenges, the industry must emphasize efficient project planning, digital fabrication integration, and collaborative risk management approaches. Aligning fabrication practices with evolving regulatory frameworks and cost-optimization strategies will be essential to maintaining competitiveness in the dynamic oil and gas fabrication sector

Oil Gas Fabrication Market Scope

The market is segmented on the basis of fabrication type, structure, upstream sector, downstream sector, and fabrication material.

• By Fabrication Type

On the basis of fabrication type, the oil & gas fabrication market is segmented into onshore fabrication and offshore fabrication. The onshore fabrication segment dominated the market with the largest revenue share in 2024, driven by the relatively lower complexity and cost of construction compared to offshore projects. Onshore fabrication facilities allow for easier logistics, workforce access, and equipment installation, making them attractive for operators focusing on rapid project deployment. Moreover, onshore projects benefit from simplified regulatory procedures and reduced environmental constraints, enhancing their appeal to investors. The segment also sees sustained demand due to steady growth in land-based exploration and development activities across mature and emerging oil-producing regions.

The offshore fabrication segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing exploration in deepwater and ultra-deepwater reserves. Offshore projects, although capital-intensive, offer access to untapped hydrocarbon reserves and are driven by technological advancements in subsea construction, modular platforms, and floating structures. Rising investments by national oil companies and private operators in offshore developments further accelerate market adoption. The shift toward energy diversification and offshore LNG projects is also contributing to growth, highlighting the strategic importance of offshore fabrication in meeting global energy demands.

• By Structure

On the basis of structure, the oil & gas fabrication market is segmented into fixed platforms, semi-submersible platforms, jack-up platforms, and floating production storage and offloading (FPSO) units. The fixed platforms segment dominated the market in 2024 due to their proven stability, durability, and long operational lifespan in shallow-water fields. Fixed platforms are widely preferred for their ability to support heavy drilling and production equipment while providing safety and reliability in varying marine conditions. Their extensive track record in global offshore operations reinforces market confidence and encourages long-term investment.

The FPSO segment is anticipated to witness the fastest growth from 2025 to 2032, driven by increasing deepwater exploration and the need for flexible, deployable solutions in remote offshore regions. FPSOs offer advantages such as mobility, shorter installation timelines, and the ability to process and store hydrocarbons at sea, eliminating dependency on pipelines. Companies are increasingly adopting FPSO units for frontier oil fields, supported by innovations in hull design, mooring systems, and topside modularity. The growing demand for floating production solutions aligns with rising offshore oil and gas activities in Africa, South America, and Southeast Asia.

• By Upstream Sector

On the basis of upstream sector, the market is segmented into exploration and production (E&P), transportation, and storage. The E&P segment dominated the market in 2024, owing to the continuous expansion of hydrocarbon exploration projects and development of new oil and gas fields globally. Operators focus on advanced fabrication facilities to optimize production efficiency, enhance operational safety, and reduce downtime in extraction operations. Investment in modular and pre-fabricated E&P structures enables faster commissioning and cost control, reinforcing their dominant position. The growing demand for energy security in both developed and emerging markets further supports the sustained dominance of E&P fabrication activities.

The transportation segment is expected to witness the fastest growth rate from 2025 to 2032, driven by rising investments in subsea pipelines, LNG transport infrastructure, and oil tanker facilities. Transportation fabrication requires specialized engineering for high-pressure and corrosion-resistant pipelines, and the adoption of innovative materials ensures reliability and operational efficiency. Technological advancements in automated fabrication and pipeline welding accelerate project execution, while increasing cross-border energy trade stimulates demand. Companies are increasingly prioritizing transportation solutions to improve supply chain connectivity and reduce logistical challenges in oil and gas operations.

• By Downstream Sector

On the basis of downstream sector, the market is segmented into refining, petrochemicals, and liquefied natural gas (LNG). The refining segment dominated the market in 2024 due to the high volume of crude oil processing and established global refining infrastructure. Refining fabrication facilities require complex process units, storage tanks, and modular units to ensure operational efficiency and compliance with environmental standards. Continuous modernization of refineries to improve output, product quality, and energy efficiency supports the dominant position of this segment. The demand for downstream fabrication in refining is also reinforced by ongoing upgrades in mature markets and expansion projects in emerging economies.

The LNG segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by increasing global natural gas demand and the expansion of LNG export terminals. LNG fabrication involves advanced cryogenic storage tanks, regasification units, and liquefaction modules requiring precision engineering and innovative materials. Growth is particularly strong in regions such as the U.S., Qatar, and Australia, where large-scale LNG projects are being commissioned. Rising focus on cleaner fuels and international gas trade agreements further accelerate LNG fabrication market expansion.

• By Fabrication Material

On the basis of fabrication material, the market is segmented into steel, concrete, and composite materials. The steel segment dominated the market with the largest share of 60.5% in 2024, driven by its high strength-to-weight ratio, versatility, and cost-effectiveness for both onshore and offshore structures. Steel fabrication supports modular construction and rapid deployment of platforms, pipelines, and processing units, making it a preferred choice for operators worldwide. Its widespread availability and established fabrication techniques further reinforce dominance, ensuring reliability and ease of maintenance.

The composite materials segment is expected to witness the fastest growth rate from 2025 to 2032, driven by demand for lightweight, corrosion-resistant, and high-strength alternatives to conventional steel and concrete. Composites are increasingly used in deepwater and offshore applications, including pipelines, subsea structures, and FPSO modules, where durability and longevity are critical. Technological innovations in fiber-reinforced plastics, carbon fiber composites, and hybrid materials expand their applicability, while rising environmental and safety standards promote adoption in modern oil and gas projects.

Oil Gas Fabrication Market Regional Analysis

- North America dominated the oil gas fabrication market with the largest revenue share of over 35% in 2024, driven by the presence of advanced oilfield infrastructure and strong investments in both onshore and offshore projects

- Operators in the region are increasingly focusing on upgrading existing platforms and fabricating modular solutions to enhance operational efficiency and safety

- The widespread adoption of modern fabrication technologies, coupled with stringent regulatory standards, supports high-quality construction and reduces project timelines. The U.S., in particular, is investing heavily in offshore and deepwater projects, further strengthening the market's dominance in North America

U.S. Oil & Gas Fabrication Market Insight

The U.S. oil & gas fabrication market captured the largest revenue share within North America in 2024, fueled by extensive onshore and offshore E&P activities. Rising oil and gas production in shale fields, coupled with a push for modernization of aging infrastructure, drives demand for advanced fabrication solutions. Fabrication services focusing on steel-based platforms, pipelines, and modular units are witnessing robust adoption. In addition, government incentives and technological support for deepwater and offshore exploration projects are further accelerating market growth.

Europe Oil & Gas Fabrication Market Insight

The Europe oil & gas fabrication market is projected to expand at a steady CAGR during the forecast period, driven by investments in renewable integration, offshore platforms, and subsea infrastructure. Operators are increasingly focusing on high-precision fabrication techniques to meet stringent environmental and safety regulations. Countries such as Norway and the Netherlands are witnessing strong demand for offshore structures and modular platforms. Furthermore, advancements in fabrication materials, such as composite and corrosion-resistant steel, are fostering growth in both E&P and downstream sectors.

U.K. Oil & Gas Fabrication Market Insight

The U.K. oil & gas fabrication market is anticipated to grow at a notable CAGR during the forecast period, driven by ongoing offshore development projects in the North Sea. The need to replace aging infrastructure and improve operational efficiency is encouraging investments in modern fabrication techniques. Modular fabrication solutions and FPSO units are gaining traction, while the government’s focus on safety and sustainability standards further promotes market adoption. The U.K.’s well-established supply chain and skilled workforce support large-scale fabrication projects for both domestic and export demands.

Germany Oil & Gas Fabrication Market Insight

The Germany oil & gas fabrication market is expected to expand at a considerable CAGR during the forecast period, fueled by investments in energy infrastructure and the integration of advanced technologies in fabrication processes. German operators emphasize high-quality, environmentally compliant solutions, particularly for refining and petrochemical projects. The growing focus on modular fabrication units and durable offshore structures supports market growth. Moreover, the adoption of steel and composite materials in fabrication projects aligns with the country’s sustainability and industrial innovation priorities.

Asia-Pacific Oil & Gas Fabrication Market Insight

The Asia-Pacific oil & gas fabrication market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing exploration activities, offshore developments, and investments in LNG projects in countries such as China, India, and Australia. The region’s growing demand for energy and expanding oilfield infrastructure fuels fabrication requirements for both onshore and offshore sectors. In addition, Asia-Pacific is emerging as a manufacturing hub for oil & gas fabrication, with cost-effective labor, abundant raw materials, and advanced shipyard facilities enhancing market expansion.

Japan Oil & Gas Fabrication Market Insight

The Japan oil & gas fabrication market is gaining momentum due to rising offshore exploration projects and increasing focus on LNG import infrastructure. The country prioritizes high-quality fabrication services to meet stringent safety and seismic standards. Integration of automated fabrication technologies and advanced steel structures supports efficient production timelines. Japan’s emphasis on renewable energy integration and modular platform adoption is further propelling demand across offshore and downstream projects.

China Oil & Gas Fabrication Market Insight

The China oil & gas fabrication market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding offshore and onshore production, and large-scale LNG projects. The presence of numerous domestic shipyards and fabrication companies provides cost-effective, high-capacity solutions. Government initiatives to enhance energy infrastructure and the growing number of deepwater exploration projects are key factors driving market growth. In addition, China’s strategic position in the regional supply chain for steel and modular components strengthens its fabrication capabilities and market dominance.

Oil Gas Fabrication Market Share

The oil gas fabrication industry is primarily led by well-established companies, including:

- Newpark Resources Inc. (U.S.)

- TechnipFMC plc (U.K.)

- DryDocks World (U.A.E.)

- Larsen & Toubro Limited (India)

- McDermott International, Inc. (U.S.)

- Lamprell plc (U.A.E.)

- Northern Weldarc Ltd. (Canada)

- JGC Corporation (Japan)

- Gulf Piping Company (IMCC Group) (U.A.E.)

- Bechtel Corporation (U.S.)

- Eversendai Corporation Berhad (Malaysia)

- Fluor Corporation (U.S.)

- National Petroleum Construction Company (NPCC) (U.A.E.)

- Saipem S.p.A. (Italy)

- Lefebvre Engineering FZC (U.A.E.)

- Integrated Flow Solutions, Inc. (U.S.)

Latest Developments in Global Oil Gas Fabrication Market

- In 2025, NOV announced the acquisition of National Oilwell Varco's fabrication business for USD 2.8 billion. This acquisition significantly strengthens NOV’s manufacturing and fabrication capabilities, enabling the company to deliver a broader range of integrated solutions across onshore and offshore oil & gas projects. By combining resources and technological expertise, NOV can undertake larger and more complex fabrication projects, including modular platforms, FPSOs, and subsea systems. The deal also reflects ongoing consolidation in the oil & gas fabrication market, which is expected to enhance competitiveness, improve operational efficiency, and expand service portfolios. Overall, this development is projected to accelerate market growth by meeting the rising global demand for new and upgraded oilfield infrastructure and boosting capacity for retrofitting aging assets

- In August 2022, Drydocks World-Dubai signed a strategic agreement with Silverstream Technologies to promote air lubrication technology for vessels serviced at its shipyard. Air lubrication reduces hydrodynamic drag, improves fuel efficiency, and helps vessels meet IMO’s Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) regulations. By becoming an approved installer of this technology, Drydocks World positions itself as a key player in sustainable ship and offshore fabrication solutions. This collaboration strengthens the market for retrofit services and energy-efficient technologies in the oil & gas sector, encouraging adoption of eco-friendly fabrication practices. It also opens new opportunities for shipyards and offshore fabrication providers to differentiate themselves with high-value, regulatory-compliant solutions

- In May 2022, Drydocks World entered an agreement with Yinson Production of Malaysia to modernize, refurbish, and convert the FPSO Atlanta for the Brazilian oil company Enauta. This project demonstrates the increasing reliance on refurbishment and life-extension services for offshore floating production systems, especially in deepwater operations. The FPSO Atlanta upgrade underscores the strategic importance of modular and specialized fabrication capabilities in extending asset lifespans, optimizing production efficiency, and reducing capital expenditures for operators. Market-wise, this highlights a growing segment of the oil & gas fabrication industry focused on retrofitting and modernization, which is expected to expand as offshore reserves mature and operators seek cost-effective infrastructure solutions

- In April 2022, the federal government awarded Chantier Davie a USD 6.5-million contract for refit work on the Canadian Coast Guard ship CCGS Louis S. St-Laurent at its Quebec City facilities. Subcontracted through Babcock Canada, this project emphasizes the increasing demand for precision fabrication services in government and defense sectors, including specialized retrofits and maintenance of offshore vessels. The contract reflects a broader trend in the oil & gas fabrication market toward multi-service shipyards capable of handling both energy and maritime projects. Such government-backed initiatives generate revenue for fabrication providers and strengthen technical capabilities and workforce expertise, contributing to long-term market stability and growth in the region

- In April 2021, the construction arm of L&T secured orders to design and construct two 132/11kV substations in Dubai, UAE, including advanced gas-insulated switchgear. These turnkey orders highlight the rising demand for integrated engineering and fabrication solutions across energy infrastructure projects, which often intersect with oil & gas operations. The project reflects a growing focus on modernization, high-efficiency technologies, and large-scale infrastructure development in the Middle East. For the oil & gas fabrication market, this demonstrates the expanding role of diversified fabrication providers who can deliver complex, high-precision solutions, supporting both upstream and downstream sectors while enabling rapid project execution and compliance with stringent operational standards

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.