Global Oled Panel Market

Market Size in USD Billion

USD

50.12 Billion

USD

149.81 Billion

2025

2033

USD

50.12 Billion

USD

149.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 50.12 Billion | |

| USD 149.81 Billion | |

| % | |

|

Organic Light Emitting Diode (OLED) Panel Market Overview

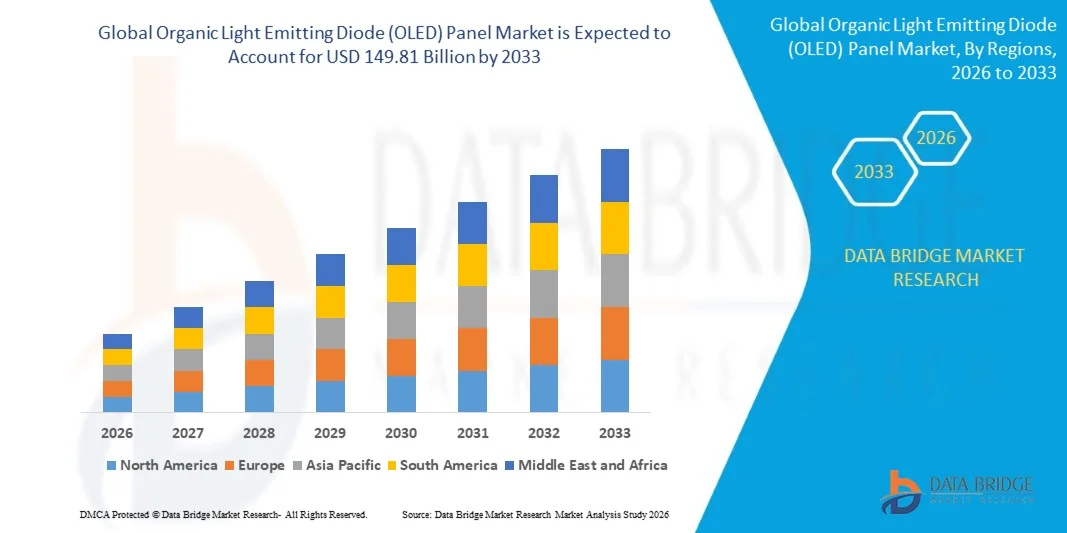

The Organic Light Emitting Diode (OLED) Panel Market was valued at USD 50.12 billion in 2025 and is projected to reach USD 149.81 billion by 2033, growing at a CAGR of 14.67% from 2026 to 2033. The market is witnessing strong expansion driven by rising demand for high-resolution, energy-efficient, and ultra-thin display technologies across smartphones, televisions, wearables, and automotive display systems. OLED panels offer superior contrast ratios, deeper blacks, faster response times, and flexible form factors, making them increasingly preferred over traditional LCD technologies.

The growing adoption of premium consumer electronics, combined with continuous advancements in display manufacturing processes such as flexible and foldable OLED technologies, is accelerating market growth. In addition, increasing integration of OLED displays in automotive infotainment systems and next-generation AR/VR devices is further supporting demand. For instance, leading consumer electronics manufacturers are expanding OLED adoption in flagship smartphones and smart TVs to enhance visual performance and user experience.

Key Market Trends & Insights

- North America dominated the organic light emitting diode (OLED) panel market with the largest revenue share of 33.4% in 2025, supported by strong consumer demand for premium electronics, early adoption of advanced display technologies, and the presence of leading technology manufacturers. The region benefits from high disposable income levels, rapid digital transformation, and strong penetration of OLED-enabled smartphones and smart TVs.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 16.9% from 2026 to 2033. Growth is driven by large-scale OLED manufacturing capabilities, strong presence of key display panel producers in China, South Korea, and Japan, and increasing demand for smartphones, televisions, and automotive displays. Government support for semiconductor and display production, along with rapid urbanization, is further strengthening regional market growth.

- The Flexible segment held the largest market revenue share of approximately 52.6% in 2025 driven by strong adoption in smartphones, foldable devices, and curved automotive displays. Flexible OLED technology enables lightweight, bendable, and ultra-thin display designs, making it highly suitable for premium consumer electronics and next-generation device innovation. Major manufacturers such as Samsung Display and BOE Technology have expanded flexible OLED production capacity to meet rising demand across high-end applications.

- The Rigid segment accounted for approximately 38.4% market share in 2025, supported by its widespread use in mid-range smartphones, monitors, and televisions where cost efficiency and stable performance are key requirements. The Transparent OLED segment held around 9.0% market share in 2025 and is projected to grow at the fastest pace, driven by rising adoption in automotive HUDs, retail signage, and smart windows, particularly in South Korea, Japan, and Europe where smart infrastructure investments are increasing.

- The AMOLED segment dominated the market with approximately 86.7% share in 2025 due to its superior image quality, faster refresh rates, and energy efficiency, making it the preferred choice for smartphones, televisions, and wearable devices. AMOLED technology is widely adopted by leading OEMs such as Apple and Samsung for flagship devices, supporting premium display performance and advanced user interfaces.

- The PMOLED segment accounted for around 13.3% market share in 2025, primarily used in small-scale applications such as industrial instruments, medical devices, and simple wearable displays. However, its growth remains limited due to lower resolution and restricted display complexity compared to AMOLED systems, although it continues to be used in cost-sensitive and low-power applications.

- The Small-Sized segment held the largest market share of approximately 48.9% in 2025, driven by extensive use in smartphones, smartwatches, and handheld devices where high resolution and energy efficiency are critical. Strong global smartphone shipments, exceeding 1.2 billion units in 2025, continue to support dominance of this segment.

- The Medium-Sized segment accounted for approximately 27.5% market share in 2025, supported by rising adoption in tablets, laptops, and automotive infotainment systems. The Large-Sized segment held around 23.6% market share and is projected to grow steadily, driven by increasing demand for OLED televisions and premium home entertainment systems, with global OLED TV shipments surpassing 6 million units in 2025.

- The Mobile and Tablet segment dominated the market with approximately 44.2% share in 2025 due to strong adoption of OLED displays in premium smartphones and tablets, particularly in flagship models from Apple, Samsung, and Xiaomi.

- The Television segment accounted for around 26.8% market share in 2025, driven by increasing consumer preference for high-end OLED TVs offering superior contrast and cinematic picture quality. The Automotive segment held approximately 15.7% share, supported by growing integration of OLED displays in digital dashboards and infotainment systems in electric and luxury vehicles. The Wearable segment accounted for around 9.1% share due to increasing use in smartwatches and fitness trackers, while Other Products contributed approximately 4.2% share, including applications in AR/VR devices, industrial displays, and signage systems.

Market Size & Forecast

- Global Market Value (2025): USD 50.12 Billion

- Expected Market Value (2033): USD 149.81 Billion

- Forecast CAGR (2026–2033): 14.67%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Organic Light Emitting Diode (OLED) Panel Market Segmentation

|

Attributes |

Organic Light Emitting Diode (OLED) Panel Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Organic Light Emitting Diode (OLED) Panel Market Trends

Trend: Rapid Expansion Of Flexible, Foldable, And High-Resolution OLED Display Technologies

Increasing demand for ultra-thin, lightweight, and energy-efficient display solutions across smartphones, televisions, automotive displays, and next-generation wearable devices is accelerating the shift from LCD to OLED technology. OLED panels eliminate the need for backlighting, enabling superior contrast ratios, deeper blacks, and improved power efficiency, making them highly suitable for premium consumer electronics. In addition, manufacturers are increasingly investing in flexible and foldable OLED architectures to support innovative device form factors and enhance user experience.

In modern smartphones and tablets, OLED adoption has become standard among premium models, with companies such as Samsung and Apple significantly expanding OLED integration in flagship devices to improve display performance and battery efficiency. For instance, foldable smartphones shipped globally crossed nearly 15 million units in 2025, reflecting rapid commercialization of flexible OLED panels in consumer markets. In the television segment, OLED TV shipments from major manufacturers such as LG Display exceeded 6 million units in 2025, supported by rising demand for large-screen home entertainment systems with cinematic color accuracy and contrast.

The automotive industry is also increasingly integrating OLED panels into digital instrument clusters, center consoles, and curved infotainment systems due to their design flexibility and high visibility under varying lighting conditions. In addition, the growing adoption of AR/VR headsets and wearable devices is further driving demand for compact, high-density OLED microdisplays capable of delivering immersive visual experiences. Pilot deployments in 2025 across premium EV models in Europe and South Korea reported enhanced cockpit visibility and reduced energy consumption of up to 20–25% compared to conventional LCD-based dashboards

Organic Light Emitting Diode (OLED) Panel Market Dynamics

Key Market Driver: Rising Demand For Premium Display Quality And Energy Efficient Consumer Electronics

The global shift toward high-end smartphones, smart TVs, laptops, and wearable devices is significantly increasing demand for OLED panels due to their superior visual performance and energy efficiency. OLED technology enables self-emissive pixels, eliminating backlight requirements and improving contrast, color accuracy, and response speed, which is critical for next-generation digital devices.

Leading consumer electronics manufacturers such as Samsung Electronics, LG Electronics, and Apple are continuously expanding OLED integration across premium product lines to enhance user experience and product differentiation. For instance, OLED smartphone shipments accounted for over 40% of global premium smartphone displays in 2025, reflecting strong adoption in high-value device categories. In the television segment, OLED penetration in the premium TV market exceeded 30% in developed economies such as South Korea and Japan, driven by increasing consumer preference for cinema-grade display quality.

In addition, rising adoption of energy-efficient displays in portable electronics is supporting battery optimization trends, particularly in smartphones and tablets where display power consumption accounts for a significant share of total device energy usage. This is further accelerating replacement of LCD technology with OLED across multiple device categories

Key Restraint/Challenge: High Manufacturing Costs And Limited Production Yield Efficiency

OLED panel manufacturing involves complex vacuum deposition processes, sensitive organic materials, and precision engineering requirements, resulting in high production costs compared to conventional LCD technologies. The reliance on expensive materials such as organic emissive compounds and thin-film encapsulation systems further increases overall panel cost structure, limiting adoption in budget-sensitive markets.

In addition, yield efficiency challenges during large-scale OLED panel production continue to impact profitability, particularly in large-size TV panels where defect rates can be higher during fabrication. Manufacturers such as LG Display and BOE Technology have reported ongoing efforts to improve yield rates, with large-panel OLED yields historically ranging between 60–75% depending on production generation and substrate size in 2025.

Commercial benchmarking indicates that OLED panels, For instance large-format TV panels, can cost nearly 30–40% more to produce than equivalent LCD panels, creating pricing pressure in highly competitive consumer electronics markets and restricting widespread penetration in low-cost device segments

Key Market Opportunity: Expansion In Automotive Displays And Next-Generation AR/VR And Wearable Devices

The rapid evolution of connected vehicles, smart cockpits, and immersive digital interfaces is creating strong demand for advanced display technologies such as OLED panels. Automotive OEMs are increasingly integrating OLED displays into curved dashboards, infotainment systems, and rear-seat entertainment modules due to their design flexibility, high contrast visibility, and thin form factor.

Companies such as BMW and Audi are incorporating OLED-based digital displays in premium vehicle models to enhance cabin aesthetics and driver interface functionality. For instance, next-generation electric vehicles launched in 2025 in Europe and China feature OLED cockpit systems with multi-display curved panels, improving user interaction and reducing dashboard energy consumption by up to 15–20% compared to conventional systems.

In addition, the growing AR/VR ecosystem is significantly expanding demand for OLED microdisplays due to their high refresh rates, fast response times, and compact pixel density capabilities. Wearable devices such as smartwatches and fitness trackers are also increasingly adopting OLED screens to enable always-on display functionality with low power consumption. Emerging investments in micro-OLED and flexible display manufacturing in South Korea, China, and the U.S. are further expected to unlock new growth opportunities across aerospace, defense, and metaverse-related applications

Organic Light Emitting Diode (OLED) Panel Market Scope

The market is segmented on the basis of type, display address scheme, size, and product.

• By Type

On the basis of type, the OLED panel market is segmented into Flexible, Rigid, and Transparent. The Flexible segment held the largest market revenue share of approximately 52.6% in 2025 driven by strong adoption in smartphones, foldable devices, and curved automotive displays. Flexible OLED technology enables lightweight, bendable, and ultra-thin display designs, making it highly suitable for premium consumer electronics and next-generation device innovation. Major manufacturers such as Samsung Display and BOE Technology have expanded flexible OLED production capacity to meet rising demand across high-end applications.

The Rigid segment accounted for approximately 38.4% market share in 2025, supported by its widespread use in mid-range smartphones, monitors, and televisions where cost efficiency and stable performance are key requirements. The Transparent OLED segment held around 9.0% market share in 2025 and is projected to grow at the fastest pace, driven by rising adoption in automotive HUDs, retail signage, and smart windows, particularly in South Korea, Japan, and Europe where smart infrastructure investments are increasing.

• By Display Address Scheme

On the basis of display address scheme, the market is segmented into Passive Matrix Organic Light Emitting Diode (PMOLED) Display and Active-Matrix Organic Light Emitting Diode (AMOLED) Display. The AMOLED segment dominated the market with approximately 86.7% share in 2025 due to its superior image quality, faster refresh rates, and energy efficiency, making it the preferred choice for smartphones, televisions, and wearable devices. AMOLED technology is widely adopted by leading OEMs such as Apple and Samsung for flagship devices, supporting premium display performance and advanced user interfaces.

The PMOLED segment accounted for around 13.3% market share in 2025, primarily used in small-scale applications such as industrial instruments, medical devices, and simple wearable displays. However, its growth remains limited due to lower resolution and restricted display complexity compared to AMOLED systems, although it continues to be used in cost-sensitive and low-power applications.

• By Size

On the basis of size, the OLED panel market is segmented into Small-Sized OLED Panel, Medium-Sized OLED Panel, and Large-Sized OLED Panel. The Small-Sized segment held the largest market share of approximately 48.9% in 2025, driven by extensive use in smartphones, smartwatches, and handheld devices where high resolution and energy efficiency are critical. Strong global smartphone shipments, exceeding 1.2 billion units in 2025, continue to support dominance of this segment.

The Medium-Sized segment accounted for approximately 27.5% market share in 2025, supported by rising adoption in tablets, laptops, and automotive infotainment systems. The Large-Sized segment held around 23.6% market share and is projected to grow steadily, driven by increasing demand for OLED televisions and premium home entertainment systems, with global OLED TV shipments surpassing 6 million units in 2025.

• By Product

On the basis of product, the OLED panel market is segmented into Mobile and Tablet, Television, Automotive, Wearable, and Other Products. The Mobile and Tablet segment dominated the market with approximately 44.2% share in 2025 due to strong adoption of OLED displays in premium smartphones and tablets, particularly in flagship models from Apple, Samsung, and Xiaomi.

The Television segment accounted for around 26.8% market share in 2025, driven by increasing consumer preference for high-end OLED TVs offering superior contrast and cinematic picture quality. The Automotive segment held approximately 15.7% share, supported by growing integration of OLED displays in digital dashboards and infotainment systems in electric and luxury vehicles. The Wearable segment accounted for around 9.1% share due to increasing use in smartwatches and fitness trackers, while Other Products contributed approximately 4.2% share, including applications in AR/VR devices, industrial displays, and signage systems.

Organic Light Emitting Diode (OLED) Panel Market Regional Analysis

North America Organic Light Emitting Diode (OLED) Panel Market Insight

North America dominated the OLED panel market with the largest revenue share of 33.4% in 2025, supported by strong demand for premium consumer electronics, high adoption of advanced display technologies, and rapid integration of OLED panels in smartphones, televisions, and automotive displays. The region benefits from a strong presence of leading technology companies, high disposable income, and early adoption of next-generation devices such as foldable smartphones and AR/VR headsets. In addition, increasing investments in digital entertainment, gaming, and connected vehicle ecosystems are further strengthening OLED penetration across end-use industries.

U.S. Organic Light Emitting Diode (OLED) Panel Market Insight

The U.S. OLED panel market captured the largest revenue share of 28.1% in North America in 2025, driven by strong demand for premium smartphones, smart TVs, and high-performance computing devices. Consumers in the country show a strong preference for high-resolution, energy-efficient displays, accelerating OLED adoption across leading brands such as Apple and Dell. For instance, OLED penetration in premium smartphone displays in the U.S. exceeded 45% in 2025, supported by continuous product innovation and rapid upgrade cycles in consumer electronics. In addition, growing adoption of OLED displays in automotive infotainment systems from manufacturers such as Tesla and General Motors is further expanding market growth.

Europe Organic Light Emitting Diode (OLED) Panel Market Insight

The Europe OLED panel market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for premium display technologies, rising adoption of electric vehicles, and strong emphasis on energy-efficient consumer electronics. The region’s strict sustainability regulations and focus on reducing power consumption in electronic devices are encouraging manufacturers to adopt OLED technology. Growing investments in automotive digitalization and smart mobility solutions are also accelerating OLED integration in vehicle dashboards and infotainment systems across major European markets.

U.K. Organic Light Emitting Diode (OLED) Panel Market Insight

The U.K. OLED panel market is expected to witness steady growth from 2026 to 2033, supported by rising demand for smart TVs, smartphones, and connected home devices. Increasing consumer preference for high-quality streaming experiences and advanced gaming displays is driving OLED adoption in the country. For instance, OLED TV sales in the U.K. accounted for nearly 22% of the premium television segment in 2025, reflecting strong consumer shift toward high-end display technologies. In addition, expanding smart home ecosystems and increasing integration with IoT-enabled devices are further supporting market expansion.

Germany Organic Light Emitting Diode (OLED) Panel Market Insight

The Germany OLED panel market is expected to witness strong growth from 2026 to 2033, driven by increasing demand for advanced automotive display systems, industrial visualization tools, and energy-efficient consumer electronics. Germany’s strong automotive manufacturing base is a key factor supporting OLED adoption in digital dashboards and infotainment systems across premium vehicle segments. For instance, leading German automakers have increased OLED integration in luxury vehicle models launched in 2025, improving cabin aesthetics and reducing energy consumption compared to conventional LCD systems. In addition, rising emphasis on sustainability and green technology is further accelerating OLED adoption across multiple sectors.

Asia-Pacific Organic Light Emitting Diode (OLED) Panel Market Insight

The Asia-Pacific OLED panel market is expected to witness the fastest growth rate from 2026 to 2033, supported by large-scale display manufacturing, rapid urbanization, and strong demand for smartphones, televisions, and wearable devices. Countries such as China, South Korea, and Japan dominate global OLED production, with major manufacturers such as Samsung Display, LG Display, and BOE Technology driving supply expansion. The region accounted for over 45% of global OLED production capacity in 2025, reflecting its dominance in the display manufacturing ecosystem. In addition, rising adoption of foldable smartphones and smart devices is further accelerating regional market growth.

Japan Organic Light Emitting Diode (OLED) Panel Market Insight

The Japan OLED panel market is expected to witness steady growth from 2026 to 2033, driven by strong demand for high-quality displays in consumer electronics, automotive systems, and industrial applications. Japan’s advanced electronics industry and focus on precision manufacturing support OLED integration in compact devices such as smartphones, cameras, and wearable technologies. For instance, OLED adoption in premium smartphones and gaming devices in Japan exceeded 50% penetration in 2025, reflecting strong consumer preference for high-performance display technology. In addition, increasing use of OLED panels in automotive infotainment systems from companies such as Toyota and Honda is further supporting market expansion.

China Organic Light Emitting Diode (OLED) Panel Market Insight

The China OLED panel market accounted for the largest market revenue share of 38.6% in Asia-Pacific in 2025, attributed to strong domestic manufacturing capabilities, rapid urbanization, and high adoption of smart devices. China is one of the largest production hubs for OLED panels, with companies such as BOE Technology and TCL CSOT expanding production capacity to meet global demand. For instance, China’s OLED smartphone shipments exceeded 300 million units in 2025, driven by strong demand from both domestic and international markets. In addition, government initiatives supporting smart city development and consumer electronics innovation are further accelerating OLED market expansion across residential, commercial, and industrial applications.

Organic Light Emitting Diode (OLED) Panel Market Share

The Organic Light Emitting Diode (OLED) Panel industry is primarily led by well-established companies, including:

- Emerson Electric Co. (U.S.)

- Advantech Co., Ltd. (Taiwan)

- Innolux Corporation (Taiwan)

- Pepperl+Fuchs SE (Germany)

- Planar (U.S.)

- AU Optronics Corp. (Taiwan)

- LG Display Co., Ltd. (South Korea)

- Japan Display Inc. (Japan)

- General Digital Corporation (U.S.)

- Samsung (South Korea)

- Rockwell Automation, Inc. (U.S.)

- Panasonic Corporation (Japan)

- Sharp NEC Display Solutions, Ltd. (Japan)

- Schneider Electric (France)

- Sony Corporation (Japan)

- Corning Incorporated (U.S.)

- DuPont (U.S.)

- Kateeva (U.S.)

- FlexEnable Limited (U.K.)

- TOSHIBA CORPORATION (Japan)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Oled Panel Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Oled Panel Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Oled Panel Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.