Global Oligometastasis Treatment Market

Market Size in USD Billion

USD

2.50 Billion

USD

4.80 Billion

2024

2032

USD

2.50 Billion

USD

4.80 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.50 Billion | |

| USD 4.80 Billion | |

| % | |

|

Oligometastasis Treatment Market Size

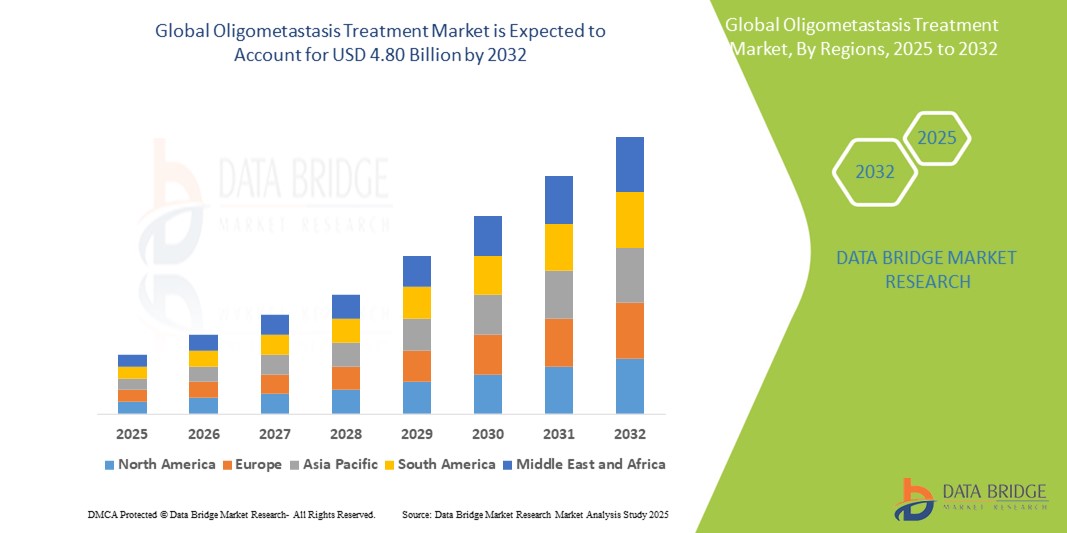

- The global oligometastasis treatment market size was valued at USD 2.50 billion in 2024 and is expected to reach USD 4.80 billion by 2032, at a CAGR of 8.50% during the forecast period

- The global oligometastasis treatment market growth is largely fueled by the increasing incidence of metastatic cancers and rising healthcare expenditure, alongside growing strategic collaborations among market players and a surge in research and development activities for targeted therapies, leading to increased demand for condition-specific treatments in both developed and developing regions.

- Furthermore, increasing awareness of oligometastatic disease and the availability of advanced diagnostic and imaging tools are establishing stereotactic body radiotherapy (SBRT), surgical resection, and immunotherapy as the preferred treatment approaches. These converging factors are accelerating the adoption of multimodal treatment strategies, thereby significantly boosting the global oligometastasis treatment market's growth.

Oligometastasis treatment Market Analysis

- Oligometastasis treatments, encompassing advanced radiation therapy (SBRT/SABR), surgical resection, and systemic therapies like chemotherapy and immunotherapy, are increasingly vital components of managing limited metastatic cancer in various patient populations due to their potential for disease control and improved patient outcomes.

- The escalating demand for effective oligometastasis treatments is primarily fueled by a greater understanding of the disease as an intermediate state, advancements in diagnostic imaging (e.g., PET/CT), and a growing emphasis on multidisciplinary treatment planning.

- North America holds a significant revenue share in the global oligometastasis treatment market in 2025, characterized by early adoption of advanced cancer therapies, high healthcare expenditure, and a strong presence of key research institutions and specialized hospitals, with the U.S. experiencing substantial growth in the adoption of multidisciplinary treatment approaches, particularly in comprehensive cancer centers and academic medical facilities, driven by innovations in stereotactic radiotherapy techniques and targeted drug development.

- Asia-Pacific is expected to be the fastest-growing region in the global oligometastasis treatment market during the forecast period due to increasing healthcare access, rising awareness of advanced cancer treatments, and growing investments in healthcare infrastructure.

- The Radiation Therapy segment (by Treatment) is expected to be a significant segment in the global oligometastasis treatment market in 2025, driven by the inherent need for highly precise and effective local interventions for limited metastatic growths.

Report Scope and Oligometastasis Treatment Market Segmentation

|

Attributes |

Oligometastasis Treatment Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Oligometastasis Treatment Market Trends

“Enhanced Treatment Precision Through Advanced Diagnostics and Personalized Approaches”

- A significant and accelerating trend in the global oligometastasis treatment market is the deepening integration with advanced diagnostic technologies and personalized treatment strategies, informed by molecular profiling and imaging innovations. This fusion of technologies is significantly enhancing treatment precision and improving patient outcomes.

- For instance, advanced imaging techniques like PET/CT and high-resolution MRI are increasingly being used to identify all metastatic sites and precisely delineate tumor volumes, allowing clinicians to tailor treatment plans based on the unique characteristics and exact location of each lesion. Similarly, liquid biopsies are emerging as tools to detect circulating tumor DNA (ctDNA) and predict treatment response, guiding systemic therapy choices.

- Integration of sophisticated diagnostics in oligometastasis treatment enables features such as identifying potential therapeutic targets and predicting treatment response, leading to more intelligent clinical decision-making. For instance, the detection of specific genomic alterations might indicate sensitivity to particular targeted therapies or immunotherapies.

- The seamless integration of diagnostic insights with various treatment modalities facilitates a more coordinated and effective approach to managing this complex disease. Through a unified treatment plan, specialists can integrate stereotactic body radiation therapy (SBRT), surgical metastasectomy, chemotherapy, immunotherapy, and targeted therapies, creating a comprehensive and individualized patient experience. Furthermore, advanced radiation planning guided by functional imaging offers patients maximized local control with minimized toxicity.

- This trend towards more precise, targeted, and interconnected treatment strategies is fundamentally reshaping expectations for oligometastasis management. Consequently, research institutions and pharmaceutical companies are developing novel therapies based on molecular targets and exploring innovative combination strategies with local ablative treatments.

- The demand for oligometastasis treatments that offer seamless integration of advanced diagnostics and personalized approaches is growing rapidly across both specialized cancer centers and research institutions, as clinicians increasingly prioritize efficacy and improved patient survival.

Oligometastasis Treatment Market Dynamics

Driver

“Growing Need Due to Rising Cancer Prevalence and Advanced Diagnostic Adoption”

- The increasing prevalence of cancer and metastatic disease among individuals, coupled with the accelerating adoption of advanced diagnostic techniques, is a significant driver for the heightened demand for the global oligometastasis treatment market.

- For instance, advanced imaging modalities like PSMA-PET/CT are increasingly being used to identify and precisely localize even small metastatic lesions, looking forward to integrating state-of-the-art functional and molecular imaging into the diagnostic pathway for oligometastatic disease. Such strategies by key entities are expected to drive the oligometastasis treatment market growth in the forecast period.

- As healthcare professionals become more aware of the complexities of oligometastatic disease and seek enhanced diagnostic accuracy for their patients, advanced diagnostic tools offer features such as detailed molecular profiling, comprehensive imaging analysis, and circulating tumor DNA (ctDNA) detection, providing a compelling upgrade over traditional staging methods.

- Furthermore, the growing popularity of personalized medicine approaches and the desire for interconnected healthcare solutions are making sophisticated diagnostics an integral component of treatment planning for oligometastasis, offering seamless integration with multidisciplinary team discussions and treatment platforms.

- The benefit of precise tumor characterization, identification of potential therapeutic targets, and the ability to monitor disease progression through advanced diagnostic applications are key factors propelling the adoption of these technologies in both research and clinical settings. The trend towards earlier detection and the increasing availability of highly sensitive diagnostic platforms further contribute to market growth.

Restraint/Challenge

“Concerns Regarding Diagnostic Complexity and Treatment Costs”

- Concerns surrounding the diagnostic complexity and heterogeneity of oligometastatic disease, pose a significant challenge to broader market understanding and effective management. As this condition can exhibit diverse primary tumor types, metastatic sites, and biological profiles, accurate diagnosis and risk stratification can be challenging, raising anxieties among healthcare professionals about the optimal treatment strategies and patient outcomes.

- For instance, complex cases with overlapping features between true oligometastasis and early widespread disease have made some clinicians hesitant to adopt definitive local treatment protocols without extensive multidisciplinary review. The lack of a universally agreed-upon definition for oligometastasis further contributes to this challenge.

- Addressing these diagnostic challenges through enhanced imaging techniques (e.g., advanced PET tracers), standardized clinical criteria, and comprehensive molecular characterization is crucial for building clinician confidence. Institutions such as major cancer centers emphasize their integrated diagnostic approaches and expert multidisciplinary tumor boards in their clinical pathways to reassure referring physicians. Additionally, the relatively high cost associated with advanced diagnostic workup and multimodal treatment regimens for oligometastasis compared to purely palliative care can be a barrier to access for patients, particularly in regions with limited healthcare resources or for individuals with inadequate insurance coverage. While advancements in diagnostics may become more accessible over time, specialized therapies such as stereotactic radiation or complex surgical procedures often come with a higher price tag.

- While treatment costs may be partially offset by insurance in some regions, the perceived financial burden of managing a complex and potentially curative cancer can still hinder timely and comprehensive care, especially for those who lack adequate financial support or live in underserved areas.

- Overcoming these challenges through collaborative research efforts to refine diagnostic criteria, the development of more cost-effective diagnostic and therapeutic strategies, and improved access to specialized care will be vital for sustained improvement in patient outcomes in the oligometastasis treatment market.

Oligometastasis Treatment Market Scope

The market is segmented on the basis of sites of metastasis, diagnosis, treatment, route of administration, end users, and distribution channel.

By Treatment type

On the basis of treatment, the oligometastasis treatment market is segmented into Radiation Therapy (SBRT/SABR, SRS, Conventional), Surgery (Metastasectomy), Chemotherapy, Immunotherapy, Targeted Therapy, Ablative Techniques (RFA, Cryoablation, Microwave Ablation), and Others. The Radiation Therapy (SBRT/SABR, SRS, Conventional) segment dominates the largest market revenue share, driven by the highly precise and non-invasive nature of stereotactic ablative radiotherapy and the critical need for localized control of metastatic lesions. Healthcare professionals often prioritize addressing oligometastatic sites with high-dose, conformal radiation due to its potential for long-term disease control and significant impact on patient prognosis. The market also sees strong focus on advanced radiotherapy types due to ongoing research efforts aimed at developing effective treatment protocols and improving survival rates.

The Surgery (Metastasectomy) and Systemic Therapies (Chemotherapy, Immunotherapy, Targeted Therapy) segments are also significant due to their crucial role in managing oligometastatic disease and the necessity for accurate patient selection and appropriate combination strategies to prevent potential complications or recurrence. While specific treatment choices depend on primary tumor type and metastatic site, these modalities require careful monitoring and tailored treatment, contributing to the overall demand in the oligometastasis treatment market. The variety of surgical approaches for resectable lesions and the growing sophistication of systemic agents also contribute to these segments' importance.

By Diagnosis

On the basis of diagnosis, the oligometastasis treatment market is segmented into Ultrasound, CT Scan, Bone Scan, PET/CT, MRI, and Others. The PET/CT and MRI segments collectively held a significant market revenue share in the historical period, driven by their superior sensitivity and specificity in detecting limited metastatic lesions across various body sites. These advanced diagnostic tools are often used as part of comprehensive staging protocols to accurately identify the number and location of oligometastases.

The Ultrasound, CT Scan, and Bone Scan segments are also crucial and are anticipated to witness steady growth, driven by their widespread availability, cost-effectiveness, and utility for initial screening or specific site assessments. These diagnostic methods are often employed as preliminary evaluations or for guiding interventional procedures, contributing to the overall diagnostic pathway for oligometastasis. The advancements in imaging resolution and integration with AI-powered analysis are further enhancing their precision and utility in the identification of oligometastatic disease.

By Route of Administration

On the basis of route of administration, the oligometastasis treatment market is segmented into Oral, Injectable, and Others. The Injectable segment held a significant market revenue share in the historical period, driven by the common administration of systemic therapies like chemotherapy, immunotherapy, and targeted therapies through intravenous or subcutaneous injections to ensure rapid and precise delivery of active agents. Injectable routes are often used for high-potency drugs requiring controlled dosing and immediate systemic effect.

The Oral segment is also crucial and is anticipated to witness steady growth, driven by its convenience for patients and the increasing development of oral formulations for various targeted therapies and chemotherapy agents. Oral administration is often employed for maintenance therapies or for drugs that offer comparable efficacy to injectable forms with improved patient compliance, contributing to the overall demand in the oligometastasis treatment market. The advancements in drug encapsulation and bioavailability are further enhancing the precision and utility of orally administered treatments.

By End Users

On the basis of end users, the oligometastasis treatment market is segmented into Hospitals, Specialty Clinics, Research Institutes, and Others. The Hospitals segment held a significant market revenue share in the historical period, driven by their comprehensive infrastructure for multidisciplinary cancer care, including advanced diagnostic imaging, radiation oncology departments, and surgical capabilities. Hospitals are often the primary centers for initial diagnosis, complex treatment planning, and administration of various oligometastasis therapies.

The Specialty Clinics and Research Institutes segments are also crucial and are anticipated to witness steady growth, driven by their focused expertise in specific treatment modalities (e.g., radiation oncology clinics) and their pivotal role in clinical trials and novel therapeutic development. Specialty clinics often provide specialized outpatient care, while research institutes contribute significantly to advancing the understanding and treatment of oligometastatic disease, contributing to the overall demand in the oligometastasis treatment market. The advancements in outpatient treatment delivery and the increasing number of clinical studies are further enhancing the precision and utility of oligometastasis management in these settings.

Oligometastasis Treatment Market Regional Analysis

- North America holds a notable position in the oligometastasis treatment market with a significant revenue share, driven by a well-established healthcare system and increasing awareness of the treatability of limited metastatic cancer.

- Healthcare professionals in the region highly value access to advanced diagnostic tools (e.g., PET/CT), multidisciplinary treatment teams, and innovative therapeutic approaches such as stereotactic ablative radiotherapy (SBRT) and metastasis-directed surgery for managing oligometastatic disease.

- This focus on comprehensive care is further supported by robust research activities, the presence of specialized comprehensive cancer centers, and patient advocacy groups, establishing advanced treatment modalities as a favored approach for managing this complex disease in both primary and referral settings.

U.S. Oligometastasis Treatment Market Insight

The U.S. oligometastasis treatment market captured a significant revenue share within North America, fueled by the increasing focus on early detection and specialized management of limited metastatic cancer. Healthcare professionals are progressively prioritizing the improvement of patient outcomes through advanced diagnostic modalities like PET/CT and tailored local and systemic treatment strategies. The growing emphasis on multidisciplinary care teams, combined with the increasing availability of specialized comprehensive cancer centers and robust clinical research initiatives, further propels the oligometastasis treatment landscape. Moreover, the rising integration of sophisticated diagnostic technologies and the development of novel therapeutic approaches, particularly in stereotactic radiotherapy and targeted drug combinations, are significantly contributing to the market's evolution in the United States.

Europe Oligometastasis Treatment Insight

The European oligometastasis treatment market is projected to expand at a notable CAGR throughout the forecast period, primarily driven by established healthcare infrastructure and the escalating recognition of oligometastasis as a treatable condition. The increase in diagnostic capabilities, coupled with the demand for comprehensive cancer management, is fostering the adoption of advanced treatment protocols. European healthcare providers are also focused on improving patient outcomes and quality of life through multidisciplinary approaches. The region is experiencing significant advancements across diagnosis (e.g., advanced PET tracers), local ablative therapies (e.g., SBRT), and systemic therapies (e.g., immunotherapies, targeted therapies), with innovative treatments being integrated into both primary cancer centers and specialized oncology units.

U.K. Oligometastasis Treatment Market Insight

The U.K. oligometastasis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating focus on specialized cancer care and a desire for improved patient outcomes. Additionally, concerns regarding the progression of cancer to a limited metastatic state are encouraging both healthcare providers and research institutions to choose advanced diagnostic and therapeutic solutions. The UK’s commitment to healthcare innovation, alongside its well-established network of hospitals and specialized cancer centers, is expected to continue to stimulate market growth in the management of oligometastatic disease.

Germany Oligometastasis Treatment Market Insight

The German oligometastasis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of the potential for curative-intent treatment in limited metastatic settings and the demand for technologically advanced, evidence-based therapies. Germany’s well-developed healthcare system, combined with its emphasis on research and patient-centric care, promotes the adoption of innovative diagnostic and therapeutic strategies for oligometastasis, particularly in specialized oncology centers and university hospitals. The integration of advanced imaging, such as PSMA-PET/CT, and highly precise radiation techniques like SBRT, is driving significant progress in patient management.

Asia-Pacific Oligometastasis Treatment Market Insight

The Asia-Pacific oligometastasis treatment market is poised to grow at a significant CAGR, driven by increasing urbanization, rising healthcare awareness, and advancements in medical infrastructure in countries such as China, Japan, and India. The region's growing focus on improving cancer care, supported by government initiatives promoting healthcare modernization, is driving the adoption of advanced treatment modalities for limited metastatic disease. Furthermore, as APAC emerges as a growing hub for medical research and development, the accessibility and affordability of specialized treatments for oligometastasis are expanding to a wider patient base.

Japan Oligometastasis Treatment Market Insight

The Japan oligometastasis treatment market is gaining attention due to the country’s advanced medical infrastructure, rapid aging population, and emphasis on high-quality cancer care. The Japanese market places a significant emphasis on precise diagnostics and effective treatments for limited metastatic disease, and the adoption of advanced medical technologies like particle therapy (proton and carbon-ion beam therapy) and sophisticated imaging is driven by the increasing number of specialized medical centers and research initiatives. The integration of sophisticated imaging techniques and molecular profiling in treatment planning, along with a focus on multidisciplinary care, is fueling growth. Moreover, Japan's aging population is likely to spur demand for comprehensive and personalized cancer care solutions in both hospital and academic settings, as oligometastasis becomes a more recognized and actively treated stage of cancer

China Oligometastasis Treatment Market Insight

The China oligometastasis treatment market accounted for a notable revenue share in the Asia Pacific region, attributed to the country's increasing healthcare expenditure, rapid urbanization, and growing adoption of advanced medical treatments. China stands as one of the largest healthcare markets globally, and specialized treatments for limited metastatic cancer like oligometastasis are becoming increasingly prioritized in major hospitals and oncology centers. The push towards improving cancer care infrastructure and the increasing availability of advanced diagnostic (e.g., highly sensitive PET tracers) and local ablative (e.g., SBRT, interventional radiology) options, alongside growing awareness among healthcare professionals, are key factors propelling the market in China

Oligometastasis Treatment Market Share

The oligometastasis treatment industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (USA)

- Philogen (Switzerland)

- AbbVie Inc. (USA)

- Amgen Inc. (USA)

- AstraZeneca (UK)

- Bayer AG (Germany)

- Bristol-Myers Squibb Company (USA)

- CELGENE CORPORATION (USA)

- Lilly (USA)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Johnson & Johnson Services, Inc. (USA)

- Pfizer Inc. (USA)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- GlaxoSmithKline plc. (UK)

- Promega Corporation (USA)

- Akorn, Incorporated (USA)

- Reata Pharmaceuticals, Inc. (USA)

- Genentech, Inc. (USA)

- Varian Medical Systems (USA)

- Elekta (Sweden)

- Accuray (USA)

- Siemens Healthineers AG (Germany)

- Boston Scientific Corporation (USA)

- Medtronic (Ireland)

- Intuitive Surgical (USA)

- Stryker (USA)

- Terumo Corporation (Japan)

- Olympus Corporation (Japan)

Latest Developments in Global Oligometastasis Treatment Market

- In 2025, significant strides were made in the application of PSMA Radioligand Therapy (RLT) for oligometastatic prostate cancer, focusing on potentially curative interventions for limited disease burden. This approach, discussed at the PSMA and Beyond 2025 meeting, aims to enhance treatment efficacy and control tumor progression, marking a shift towards more targeted therapeutic strategies

- In 2025, the integration of Artificial Intelligence (AI) in radiation oncology continued to accelerate, particularly impacting adaptive radiotherapy and automated treatment planning for complex cases like oligometastatic disease. This aims to significantly improve treatment precision by accounting for anatomical changes in real-time, enhancing patient outcomes.

- In 2025, novel systemic therapies received accelerated FDA approvals for various metastatic cancers, which are relevant for managing the systemic component of oligometastatic disease. These approvals include targeted therapies and immunotherapies, highlighting the growing toolkit for personalized treatment approaches

- In 2024, the role of liquid biopsy in oligometastasis management gained further traction, with active investigation into its potential for minimal residual disease detection and monitoring treatment response. This minimally invasive approach promises to provide real-time insights into tumor dynamics, guiding adaptive therapeutic interventions

- In 2024, ongoing clinical trials continued to provide crucial insights into optimal treatment sequences and patient selection criteria for oligometastatic GI cancers, underscoring the evolving understanding of this disease state. Results from these studies are expected to further refine treatment algorithms and foster more personalized approaches.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL OLIGOMETASTASIS TREATMENT MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL OLIGOMETASTASIS TREATMENT MARKET SIZE

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 TRIPOD DATA VALIDATION MODEL

2.2.4 MARKET GUIDE

2.2.5 MULTIVARIATE MODELLING

2.2.6 TOP TO BOTTOM ANALYSIS

2.2.7 CHALLENGE MATRIX

2.2.8 APPLICATION COVERAGE GRID

2.2.9 STANDARDS OF MEASUREMENT

2.2.10 VENDOR SHARE ANALYSIS

2.2.11 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.12 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL OLIGOMETASTASIS TREATMENT MARKET : RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.2 PORTER’S FIVE FORCES MODEL

5 INDUSTRY INSIGHTS

5.1 PATENT ANALYSIS

5.1.1 PATENT LANDSCAPE

5.1.2 USPTO NUMBER

5.1.3 PATENT EXPIRY

5.1.4 EPIO NUMBER

5.1.5 PATENT STRENGTH AND QUALITY

5.1.6 PATENT CLAIMS

5.1.7 PATENT CITATIONS

5.1.8 PATENT LITIGATION AND LICENSING

5.1.9 FILE OF PATENT

5.1.10 PATENT RECEIVED CONTRIES

5.1.11 TECHNOLOGY BACKGROUND

5.2 DRUG TREATMENT RATE BY MATURED MARKETS

5.3 DEMOGRAPHIC TRENDS: IMPACTS ON ALL INCIDENCE RATES

5.4 PATIENT FLOW DIAGRAM

5.5 KEY PRICING STRATEGIES

5.6 KEY PATIENT ENROLLMENT STRATEGIES

5.7 INTERVIEWS WITH SPECIALIST

5.8 OTHER KOL SNAPSHOTS

6 EPIDEMIOLOGY

6.1 INCIDENCE OF ALL BY GENDER

6.2 TREATMENT RATE

6.3 MORTALITY RATE

6.4 DRUG ADHERENCE AND THERAPY SWITCH MODEL

6.5 PATIENT TREATMENT SUCCESS RATES

7 MERGERS AND ACQUISITION

7.1 LICENSING

7.2 COMMERCIALIZATION AGREEMENTS

8 REGULATORY FRAMEWORK

8.1 REGULATORY APPROVAL PROCESS

8.2 GEOGRAPHIES’ EASE OF REGULATORY APPROVAL

8.3 REGULATORY APPROVAL PATHWAYS

8.4 LICENSING AND REGISTRATION

8.5 POST-MARKETING SURVEILLANCE

8.6 GOOD MANUFACTURING PRACTICES (GMPS) GUIDELINES

9 PIPELINE ANALYSIS

9.1 CLINICAL TRIALS AND PHASE ANALYSIS

9.2 DRUG THERAPY PIPELINE

9.3 PHASE III CANDIDATES

9.4 PHASE II CANDIDATES

9.5 PHASE I CANDIDATES

9.6 OTHERS (PRE-CLINICAL AND RESEARCH)

TABLE 1 GLOBAL CLINICAL TRIAL MARKET FOR OLIGOMETASTASIS TREATMENT MARKET

Company Name Therapeutic Area

XX XX

XX XX

XX XX

XX XX

XX XX

XX XX

Sources: Press Releases, Annual Reports, SEC Filings, Investor Presentations, Other Government Sources, Analysis Based on Inputs from Secondary, Expert Interviews

TABLE 2 DISTRIBUTION OF PRODUCTS AND PROJECTS BY PHASE

Phase Number of Projects

Preclinical/Research Projects XX

Clinical Development XX

Phase I XX

Phase II XX

Phase III XX

U.S. Filed/Approved But Not Yest Marketed XX

Total XX

Sources: Press Releases, Annual Reports, SEC Filings, Investor Presentations, Other Government Sources, Analysis Based on Inputs from Secondary, Expert Interviews

TABLE 3 DISTRIBUTION OF PROJECTS BY THERAPEUTIC AREA AND PHASE

Therapeutic Area Preclinical/ Research Project

XX XX

XX XX

XX XX

XX XX

XX XX

Total Projects XX

Sources: Press Releases, Annual Reports, SEC Filings, Investor Presentations, Other Government Sources, Analysis Based on Inputs from Secondary, Expert Interviews

TABLE 4 DISTRIBUTION OF PROJECTS BY SCIENTIFIC APPROACH AND PHASE

Technology Preclinical/ Research Project

XX XX

XX XX

XX XX

XX XX

XX XX

Total Projects XX

Sources: Press Releases, Annual Reports, SEC Filings, Investor Presentations, Other Government Sources, Analysis Based on Inputs from Secondary, Expert Interviews

FIGURE 1 TOP ENTITIES BASED ON R&D GLANCE FOR OLIGOMETASTASIS TREATMENT MARKET

Sources: Press Releases, Annual Reports, SEC Filings, Investor Presentations, Other Government Sources, Analysis Based on Inputs from Secondary, Expert Interviews

10 MARKETED DRUG ANALYSIS

10.1 DRUG

10.1.1 BRAND NAME

10.1.2 GENERICS NAME

10.2 THERAPEUTIC INDIACTION

10.3 PHARACOLOGICAL CLASS OD THE DRUG

10.4 DRUG PRIMARY INDICATION

10.5 MARKET STATUS

10.6 MEDICATION TYPE

10.7 DRUG DOSAGES FORM

10.8 DOSAGES AVAILABILITY

10.9 PACKAGING TYPE

10.1 DRUG ROUTE OF ADMINISTRATION

10.11 DOSING FREQUENCY

10.12 DRUG INSIGHT

10.13 AN OVERVIEW OF THE DRUG DEVELOPMENT ACTIVITIES SUCH AS REGULATORY MILSTONE, SAFETY DATA AND EFFICACY DATA, MARKET EXCLUSIVITY DATA.

10.13.1 FORECAST MARKET OUTLOOK

10.13.2 CROSS COMPETITION

10.13.3 THERAPEUTIC PORTFOLIO

10.13.4 CURRENT DEVELOPMENT SCENARIO

11 MARKET ACCESS

11.1 10-YEAR MARKET FORECAST

11.2 CLINICAL TRIAL RECENT UPDATES

11.3 ANNUAL NEW FDA APPROVED DRUGS

11.4 DRUGS MANUFACTURER AND DEALS

11.5 MAJOR DRUG UPTAKE

11.6 CURRENT TREATMENT PRACTICES

11.7 IMPACT OF UPCOMING THERAPY

12 R & D ANALYSIS

12.1 COMPARATIVE ANALYSIS

12.2 DRUG DEVELOPMENTAL LANDSCAPE

12.3 IN-DEPTH INSIGHTS ON REGULATORY MILESTONES

12.4 THERAPEUTIC ASSESSMENT

12.5 ASSET-BASED COLLABORATIONS AND PARTNERSHIPS

13 MARKET OVERVIEW

13.1 DRIVERS

13.2 RESTRAINTS

13.3 OPPORTUNITIES

13.4 CHALLENGES

14 OLIGOPROGRESSIVE DISEASE MARKET SCENARIO

14.1 INTRODUCTION

14.2 TYPE OF OLIGOPROGRESSIVE DISEASE

14.2.1 REPEAT OLIGOPROGRESSION

14.2.2 INDUCED OLIGOPROGRESSION

14.2.3 OTHERS

14.3 TYPE OF THERAPY (QUALILATITVE AND QUANTITAITE ANALSYIS)

14.3.1 TARGETED THERAPY

14.3.1.1. STEREOTACTIC RADIOSURGERY

14.3.1.2. CRYOTHERAPY

14.3.1.3. SURGERY

14.3.2 LOCAL THERAPY

14.3.2.1. RADIATION THERAPY

14.3.2.2. NONRADIATION ABLATIVE PROCEDURES

14.3.3 MINIMALLY INVASIVE THERAPY

14.4 PIPLEINE ANALYSIS

14.5 MARKET POTENTIAL

15 GLOBAL OLIGOMETASTASIS TREATMENT MARKET , BY SITES OF METASTASIS

15.1 OVERVIEW

15.2 BONES

15.3 BRAIN

15.4 LIVER

15.5 LUNGS

15.6 ADRENAL GLAND

15.7 LYMPH NODES

15.8 OTHERS

16 GLOBAL OLIGOMETASTASIS TREATMENT MARKET , BY TREATMENT

16.1 OVERVIEW

16.2 SURGERY

16.3 ABLATIVE THERAPY

16.3.1 RADIOFREQUENCY ABLATION (RFA)

16.3.2 MICROWAVE ABLATION (MWA)

16.3.3 CRYOABLATION

16.3.4 HIGH-INTENSITY FOCUSED ULTRASOUND (HIFU)

16.4 SYSTEMIC THERAPY

16.4.1 CHEMOTHERAPY

16.4.2 TARGETED THERAPY

16.4.3 IMMUNO THERAPY

16.4.4 HORMONE THERAPY

16.5 RADIATION THERAPY

16.6 THORACENTESIS

16.7 ORGAN TRANSPLANT

16.8 OTHERS

17 GLOBAL OLIGOMETASTASIS TREATMENT MARKET , BY DIAGNOSIS

17.1 OVERVIEW

17.2 IMAGING

17.2.1 ULTRASOUND

17.2.2 MRI

17.2.3 PET SCAN

17.2.4 CT SCAN

17.2.5 BONE SCAN

17.3 BIOPSY

17.3.1 NEEDLE BIOPSY

17.3.2 CORE BIOPSY

17.3.3 FINE NEEDLE ASPIRATION

17.3.4 OTHERS

17.4 OTHERS

18 GLOBAL OLIGOMETASTASIS TREATMENT MARKET BY DRUG TYPE

18.1 OVERVIEW

18.2 BRANDED

18.2.1 HERCEPTIN

18.2.2 OPDIVO

18.2.3 YERVOY

18.2.4 EMPLICITI

18.2.5 AVASTIN

18.2.6 RITUXAN

18.2.7 XALKORI

18.2.8 INLYTA

18.2.9 SUTENT

18.2.10 TECENTRIQ

18.2.11 ZYTIGA

18.2.12 DARZALEX

18.2.13 IMBRUVICA

18.2.14 OTHERS

18.3 GENERIC

19 GLOBAL OLIGOMETASTASIS TREATMENT MARKET BY ROUTE OF ADMINISTRATION

19.1 OVERVIEW

19.2 ORAL

19.2.1 TABLETS

19.2.2 CAPSULES

19.2.3 OTHERS

19.3 INJECTABLE

19.4 OTHERS

20 GLOBAL OLIGOMETASTASIS TREATMENT MARKET BY END USER

20.1 OVERVIEW

20.2 HOSPITALS

20.2.1 PRIVATE

20.2.2 PUBLIC

20.3 SPECIALTY CLINICS

20.4 HOME HEALTHCARE

20.5 OTHERS

21 GLOBAL OLIGOMETASTASIS TREATMENT MARKET BY DISTRIBUTION CHANNEL

21.1 OVERVIEW

21.2 HOSPITAL PHARMACIES

21.3 ONLINE PHARMACIES

21.4 RETAIL PHARMACIES

21.5 OTHERS

22 GLOBAL OLIGOMETASTASIS TREATMENT MARKET BY REGION

GLOBAL OLIGOMETASTASIS TREATMENT MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

22.1 NORTH AMERICA

22.1.1 U.S.

22.1.2 CANADA

22.1.3 MEXICO

22.2 EUROPE

22.2.1 GERMANY

22.2.2 U.K.

22.2.3 ITALY

22.2.4 FRANCE

22.2.5 SPAIN

22.2.6 RUSSIA

22.2.7 SWITZERLAND

22.2.8 TURKEY

22.2.9 BELGIUM

22.2.10 NETHERLANDS

22.2.11 DENMARK

22.2.12 SWEDEN

22.2.13 POLAND

22.2.14 NORWAY

22.2.15 FINLAND

22.2.16 REST OF EUROPE

22.3 ASIA-PACIFIC

22.3.1 JAPAN

22.3.2 CHINA

22.3.3 SOUTH KOREA

22.3.4 INDIA

22.3.5 SINGAPORE

22.3.6 THAILAND

22.3.7 INDONESIA

22.3.8 MALAYSIA

22.3.9 PHILIPPINES

22.3.10 AUSTRALIA

22.3.11 NEW ZEALAND

22.3.12 VIETNAM

22.3.13 TAIWAN

22.3.14 REST OF ASIA-PACIFIC

22.4 SOUTH AMERICA

22.4.1 BRAZIL

22.4.2 ARGENTINA

22.4.3 REST OF SOUTH AMERICA

22.5 MIDDLE EAST AND AFRICA

22.5.1 SOUTH AFRICA

22.5.2 EGYPT

22.5.3 BAHRAIN

22.5.4 UNITED ARAB EMIRATES

22.5.5 KUWAIT

22.5.6 OMAN

22.5.7 QATAR

22.5.8 SAUDI ARABIA

22.5.9 REST OF MEA

22.6 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

23 GLOBAL OLIGOMETASTASIS TREATMENT MARKET, SWOT AND DBMR ANALYSIS

24 GLOBAL OLIGOMETASTASIS TREATMENT MARKET, COMPANY LANDSCAPE

24.1 COMPANY SHARE ANALYSIS: GLOBAL

24.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

24.3 COMPANY SHARE ANALYSIS: EUROPE

24.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

24.5 MERGERS & ACQUISITIONS

24.6 NEW PRODUCT DEVELOPMENT & APPROVALS

24.7 EXPANSIONS

24.8 REGULATORY CHANGES

24.9 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

25 GLOBAL OLIGOMETASTASIS TREATMENT MARKET, COMPANY PROFILE

25.1 GSK PLC.

25.1.1 COMPANY OVERVIEW

25.1.2 REVENUE ANALYSIS

25.1.3 GEOGRAPHIC PRESENCE

25.1.4 PRODUCT PORTFOLIO

25.1.5 RECENT DEVELOPMENTS

25.2 PFIZER INC

25.2.1 COMPANY OVERVIEW

25.2.2 REVENUE ANALYSIS

25.2.3 GEOGRAPHIC PRESENCE

25.2.4 PRODUCT PORTFOLIO

25.2.5 RECENT DEVELOPMENTS

25.3 MERCK & CO., INC

25.3.1 COMPANY OVERVIEW

25.3.2 REVENUE ANALYSIS

25.3.3 GEOGRAPHIC PRESENCE

25.3.4 PRODUCT PORTFOLIO

25.3.5 RECENT DEVELOPMENTS

25.4 PHILOGEN S.P.A.

25.4.1 COMPANY OVERVIEW

25.4.2 REVENUE ANALYSIS

25.4.3 GEOGRAPHIC PRESENCE

25.4.4 PRODUCT PORTFOLIO

25.4.5 RECENT DEVELOPMENTS

25.5 IMMUNESENSOR THERAPEUTICS

25.5.1 COMPANY OVERVIEW

25.5.2 REVENUE ANALYSIS

25.5.3 GEOGRAPHIC PRESENCE

25.5.4 PRODUCT PORTFOLIO

25.5.5 RECENT DEVELOPMENTS

25.6 ABBVIE INC

25.6.1 COMPANY OVERVIEW

25.6.2 REVENUE ANALYSIS

25.6.3 GEOGRAPHIC PRESENCE

25.6.4 PRODUCT PORTFOLIO

25.6.5 RECENT DEVELOPMENTS

25.7 AMGEN INC.

25.7.1 COMPANY OVERVIEW

25.7.2 REVENUE ANALYSIS

25.7.3 GEOGRAPHIC PRESENCE

25.7.4 PRODUCT PORTFOLIO

25.7.5 RECENT DEVELOPMENTS

25.8 ASTRAZENECA

25.8.1 COMPANY OVERVIEW

25.8.2 REVENUE ANALYSIS

25.8.3 GEOGRAPHIC PRESENCE

25.8.4 PRODUCT PORTFOLIO

25.8.5 RECENT DEVELOPMENTS

25.9 BAYER AG

25.9.1 COMPANY OVERVIEW

25.9.2 REVENUE ANALYSIS

25.9.3 GEOGRAPHIC PRESENCE

25.9.4 PRODUCT PORTFOLIO

25.9.5 RECENT DEVELOPMENTS

25.1 LILLY

25.10.1 COMPANY OVERVIEW

25.10.2 REVENUE ANALYSIS

25.10.3 GEOGRAPHIC PRESENCE

25.10.4 PRODUCT PORTFOLIO

25.10.5 RECENT DEVELOPMENTS

25.11 BRISTOL-MYERS SQUIBB

25.11.1 COMPANY OVERVIEW

25.11.2 REVENUE ANALYSIS

25.11.3 GEOGRAPHIC PRESENCE

25.11.4 PRODUCT PORTFOLIO

25.11.5 RECENT DEVELOPMENTS

25.12 F. HOFFMANN-LA ROCHE LTD

25.12.1 COMPANY OVERVIEW

25.12.2 REVENUE ANALYSIS

25.12.3 GEOGRAPHIC PRESENCE

25.12.4 PRODUCT PORTFOLIO

25.12.5 RECENT DEVELOPMENTS

25.13 JOHNSON & JOHNSON

25.13.1 COMPANY OVERVIEW

25.13.2 REVENUE ANALYSIS

25.13.3 GEOGRAPHIC PRESENCE

25.13.4 PRODUCT PORTFOLIO

25.13.5 RECENT DEVELOPMENTS

25.14 SANOFI

25.14.1 COMPANY OVERVIEW

25.14.2 REVENUE ANALYSIS

25.14.3 GEOGRAPHIC PRESENCE

25.14.4 PRODUCT PORTFOLIO

25.14.5 RECENT DEVELOPMENTS

25.15 TAKEDA PHARMACEUTICAL COMPANY LIMITED

25.15.1 COMPANY OVERVIEW

25.15.2 REVENUE ANALYSIS

25.15.3 GEOGRAPHIC PRESENCE

25.15.4 PRODUCT PORTFOLIO

25.15.5 RECENT DEVELOPMENTS

25.16 AMGEN INC.

25.16.1 COMPANY OVERVIEW

25.16.2 REVENUE ANALYSIS

25.16.3 GEOGRAPHIC PRESENCE

25.16.4 PRODUCT PORTFOLIO

25.16.5 RECENT DEVELOPMENTS

25.17 NOVARTIS AG

25.17.1 COMPANY OVERVIEW

25.17.2 REVENUE ANALYSIS

25.17.3 GEOGRAPHIC PRESENCE

25.17.4 PRODUCT PORTFOLIO

25.17.5 RECENT DEVELOPMENTS

25.18 GILEAD SCIENCES, INC

25.18.1 COMPANY OVERVIEW

25.18.2 REVENUE ANALYSIS

25.18.3 GEOGRAPHIC PRESENCE

25.18.4 PRODUCT PORTFOLIO

25.18.5 RECENT DEVELOPMENTS

25.19 SUN PHARMACEUTICAL INDUSTRIES LTD

25.19.1 COMPANY OVERVIEW

25.19.2 REVENUE ANALYSIS

25.19.3 GEOGRAPHIC PRESENCE

25.19.4 PRODUCT PORTFOLIO

25.19.5 RECENT DEVELOPMENTS

25.2 CELLTRION HEALTHCARE CO.,LTD.

25.20.1 COMPANY OVERVIEW

25.20.2 REVENUE ANALYSIS

25.20.3 GEOGRAPHIC PRESENCE

25.20.4 PRODUCT PORTFOLIO

25.20.5 RECENT DEVELOPMENTS

25.21 HANMI PHARMACEUTICAL

25.21.1 COMPANY OVERVIEW

25.21.2 REVENUE ANALYSIS

25.21.3 GEOGRAPHIC PRESENCE

25.21.4 PRODUCT PORTFOLIO

25.21.5 RECENT DEVELOPMENTS

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

26 RELATED REPORTS

27 CONCLUSION

28 QUESTIONNAIRE

29 ABOUT DATA BRIDGE MARKET RESEARCH

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.