Global Oliguria Market

Market Size in USD Billion

USD

1.80 Billion

USD

3.38 Billion

2025

2033

USD

1.80 Billion

USD

3.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.80 Billion | |

| USD 3.38 Billion | |

| % | |

|

Oliguria Market Size

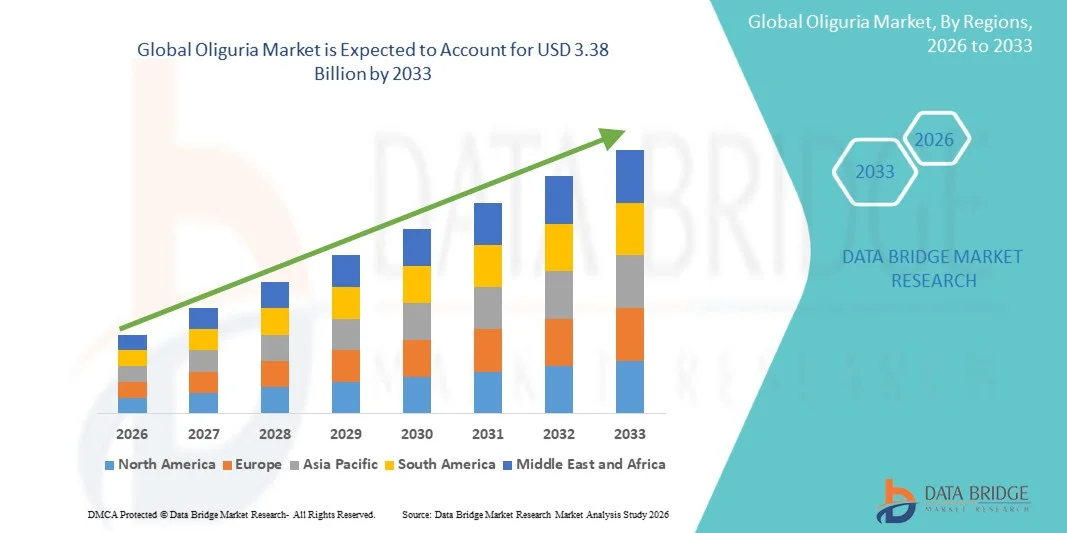

- The global Oliguria market size was valued at USD 1.80 billion in 2025and is expected to reach USD 3.38 billion by 2033, at a CAGR of 8.2% during the forecast period

- The market growth is primarily driven by the rising incidence of acute kidney injury (AKI), sepsis-related renal complications, and postoperative renal dysfunction, which frequently present oliguria as an early clinical symptom, increasing demand for rapid diagnostic and monitoring solutions

- Furthermore, growing advancements in critical care monitoring systems, expanding ICU admissions, and increasing awareness among healthcare professionals regarding early-stage kidney dysfunction are strengthening the adoption of advanced urine output tracking and renal function assessment tools, thereby supporting overall market expansion

Oliguria Market Analysis

- Oliguria, characterized by reduced urine output, is a clinically significant condition often associated with acute kidney injury (AKI), heart failure, sepsis, and dehydration, and its management primarily relies on pharmacological intervention aimed at restoring renal perfusion and improving urine output in acute care settings

- The market growth is largely driven by the increasing incidence of kidney-related disorders, rising prevalence of critically ill patients requiring diuretic therapy, growing geriatric population, and expanding use of emergency and intensive care treatments where rapid fluid balance correction is essential

- North America dominated the oliguria market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high adoption of diuretics in hospital settings, strong clinical awareness of early kidney dysfunction, and the presence of established pharmaceutical manufacturers and critical care protocols

- Asia-Pacific is expected to be the fastest growing region in the oliguria market during the forecast period due to increasing burden of chronic diseases such as hypertension and diabetes, improving access to hospital care, rising healthcare expenditure, and expanding availability of essential diuretic drugs in emerging economies

- The furosemide segment dominated the oliguria market with the largest share of 62.4% in 2025, owing to its strong efficacy as a loop diuretic, widespread clinical use in managing acute fluid overload conditions, rapid onset of action, and its established role as a first-line therapy in hospital and emergency care settings

Report Scope and Oliguria Market Segmentation

|

Attributes |

Oliguria Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Growing adoption of point-of-care renal function monitoring and smart urine output tracking systems · Expanding use of combination diuretic therapies and personalized fluid management protocols in critical care patients |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Oliguria Market Trends

“Growing Adoption of Early Renal Monitoring and Digital Urine Output Tracking in Critical Care”

- A significant and accelerating trend in the global oliguria market is the increasing integration of advanced patient monitoring systems with digital urine output measurement tools in intensive care units to enable early detection of acute kidney injury and improve clinical decision-making

- For instance, modern ICU monitoring platforms are increasingly being equipped with automated urine output tracking modules that continuously record and alert clinicians in real time when oliguria thresholds are breached, improving response speed

- The integration of AI-based clinical decision support systems is enabling predictive identification of renal decline by analyzing vital signs, fluid balance, and patient history, helping clinicians intervene earlier in at-risk patients

- Furthermore, the use of connected hospital information systems allows seamless sharing of renal function data across departments, supporting coordinated critical care management and reducing delays in treatment escalation

- Increasing use of wearable and catheter-based smart sensors for continuous urine output monitoring is emerging as a new trend, enhancing accuracy in critically ill and post-surgical patients

- This trend toward digitalization and predictive monitoring is fundamentally reshaping critical care workflows, with companies and hospitals increasingly investing in smart ICU infrastructure to enhance early oliguria detection and management

Oliguria Market Dynamics

Driver

“Rising Burden of Critical Illness and Acute Kidney Injury Driving Demand for Rapid Intervention”

- The increasing prevalence of acute kidney injury, sepsis, cardiovascular disorders, and multi-organ failure is a major driver for the growing demand for oliguria management solutions in critical care settings

- For instance, rising ICU admissions due to severe infections and post-surgical complications are significantly increasing the incidence of oliguria cases requiring immediate pharmacological and fluid management intervention

- As clinicians prioritize early identification of renal dysfunction, the demand for diuretics, fluid resuscitation therapies, and continuous urine output monitoring systems is steadily increasing across hospitals worldwide

- Furthermore, the expanding geriatric population, which is more susceptible to kidney impairment and comorbid conditions, is further accelerating the need for effective oliguria treatment strategies

- Increasing burden of diabetes and hypertension globally is significantly contributing to chronic kidney dysfunction cases, indirectly driving higher oliguria incidence in hospital admissions

- Rising adoption of evidence-based critical care protocols emphasizing early kidney injury recognition is further strengthening the use of targeted oliguria management approaches

- The growing emphasis on early intervention protocols in emergency and intensive care medicine is making oliguria management an essential component of critical care treatment pathways globally

Restraint/Challenge

“Limited Awareness of Early Oliguria Detection and Challenges in Standardized Clinical Diagnosis”

- Lack of standardized awareness regarding early-stage oliguria identification among healthcare providers, particularly in low-resource settings, remains a significant challenge for timely diagnosis and treatment initiation

- For instance, inconsistent monitoring practices in some healthcare facilities can lead to delayed recognition of reduced urine output, resulting in progression to severe kidney injury before intervention

- Variability in clinical thresholds and diagnostic protocols for oliguria across hospitals and regions further complicates early detection and uniform treatment approaches

- In addition, limited access to advanced ICU monitoring infrastructure in developing regions restricts real-time urine output tracking, reducing the effectiveness of early intervention strategies

- High dependency on manual urine measurement in many hospitals increases the risk of human error, leading to underreporting or delayed identification of oliguria cases

- Limited training of frontline healthcare staff in recognizing early renal dysfunction signs further delays clinical response and impacts patient outcomes

- Addressing these challenges through improved clinical guidelines, physician training, and wider adoption of standardized renal monitoring systems will be essential for improving patient outcomes in oliguria management

Oliguria Market Scope

The market is segmented on the basis of drugs, route of administration, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the oliguria market is segmented into furosemide, mannitol, and others. The furosemide segment dominated the market with the largest revenue share of 62.4% in 2025, driven by its strong diuretic action, rapid onset, and extensive clinical use in treating acute fluid overload conditions associated with oliguria. It is widely preferred in hospital and emergency settings due to its effectiveness in increasing urine output in critically ill patients. Furosemide is also considered a first-line therapy in acute kidney injury-related oliguria management protocols. Its well-established safety profile and availability in multiple formulations further strengthen its dominance. In addition, its cost-effectiveness compared to newer therapies ensures high adoption across both developed and emerging healthcare systems. Strong physician familiarity and inclusion in critical care guidelines continue to support its leading market position.

The mannitol segment is expected to witness the fastest growth rate of 7.8% from 2026 to 2033, driven by its increasing use as an osmotic diuretic in specific clinical conditions such as intracranial pressure management and acute renal dysfunction cases. Mannitol is gaining traction in intensive care settings where rapid osmotic diuresis is required to improve renal perfusion. It is also being increasingly used in surgical and trauma cases where oliguria develops secondary to fluid imbalance. Expanding clinical research supporting its renal protective effects is further boosting adoption. Moreover, growing availability in hospital formularies and emergency protocols is supporting its rising usage. The increasing focus on adjunct therapies in complex critical care cases is expected to further accelerate its demand.

- By Route of Administration

On the basis of route of administration, the oliguria market is segmented into oral and parenteral. The parenteral segment dominated the market with the largest revenue share of 85.3% in 2025, driven by its rapid therapeutic action and suitability for critically ill patients in hospital and ICU settings. Parenteral administration ensures immediate drug bioavailability, which is crucial in emergency oliguria cases where delayed response can lead to worsening renal failure. Most diuretics used in acute oliguria management, including furosemide, are administered intravenously for faster effect. It is also preferred in patients who are unconscious or unable to take oral medication. The dominance of hospital-based treatment settings further supports the high adoption of parenteral routes. In addition, standardized ICU protocols strongly favor intravenous therapy for fluid and electrolyte management.

The oral segment is expected to witness the fastest growth rate of 6.9% from 2026 to 2033, driven by increasing use in mild and chronic conditions where outpatient management is possible. Oral diuretics are gaining traction in step-down care and home-based treatment settings for stable patients. Rising focus on reducing hospital stays and healthcare costs is further supporting oral administration adoption. Improved patient compliance with once-daily oral formulations is also contributing to growth. In addition, expanding homecare services for chronic kidney disease patients is boosting demand for oral therapies. The growing preference for non-invasive treatment options in long-term management is expected to further accelerate this segment.

- By End-Users

On the basis of end-users, the oliguria market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share of 78.5% in 2025, driven by the high incidence of oliguria cases in intensive care units, emergency departments, and post-surgical wards. Hospitals are the primary setting for acute kidney injury management where continuous monitoring and intravenous therapy are required. The availability of advanced diagnostic and critical care infrastructure further strengthens hospital dominance. Most pharmacological interventions for oliguria are initiated in hospital settings due to the severity of the condition. The presence of trained healthcare professionals ensures accurate monitoring and timely intervention. Increasing ICU admissions globally further supports hospital-based demand.

The homecare segment is expected to witness the fastest growth rate of 8.2% from 2026 to 2033, driven by the rising trend of outpatient chronic disease management and post-discharge renal care. Homecare services are increasingly being used for stable patients requiring long-term fluid balance monitoring. Growing adoption of portable monitoring devices and telehealth platforms is enabling remote management of renal conditions. Cost-effectiveness and patient comfort are key factors driving homecare adoption. In addition, expanding aging population requiring long-term care is boosting demand. The shift toward decentralized healthcare delivery models is expected to further accelerate this segment.

- By Distribution Channel

On the basis of distribution channel, the oliguria market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share of 81.7% in 2025, driven by the high dependency on inpatient care for oliguria management and immediate drug availability requirements in critical care settings. Most diuretics and emergency renal drugs are dispensed directly within hospitals for rapid administration. Hospital pharmacies ensure strict inventory control and guideline-based drug dispensing, which is essential in ICU settings. The dominance of hospital-based treatment pathways further supports this segment. Integration with electronic medical records enhances efficient drug management. In addition, bulk procurement by hospitals contributes significantly to revenue share.

The online pharmacy segment is expected to witness the fastest growth rate of 10.4% from 2026 to 2033, driven by increasing digitalization of healthcare services and rising adoption of e-pharmacy platforms. Online pharmacies are gaining traction for chronic care medications used in post-hospitalization oliguria management. Convenience of home delivery and easy prescription access are key growth drivers. Expanding internet penetration and smartphone usage are further supporting adoption. Regulatory improvements in digital pharmacy frameworks are also encouraging growth. The shift toward telemedicine-based prescriptions is expected to significantly boost this segment.

Oliguria Market Regional Analysis

- North America dominated the oliguria market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high adoption of diuretics in hospital settings, strong clinical awareness of early kidney dysfunction, and the presence of established pharmaceutical manufacturers and critical care protocols

- Healthcare providers in the region highly prioritize early diagnosis and continuous monitoring of urine output in critically ill patients, supported by well-established clinical protocols, advanced hospital technologies, and strong availability of pharmacological treatment options such as diuretics and fluid management therapies

- This widespread dominance is further supported by high healthcare expenditure, a well-developed hospital network with advanced intensive care units, strong presence of key pharmaceutical companies, and increasing adoption of digital health solutions for real-time patient monitoring in both public and private healthcare systems

U.S. Oliguria Market Insight

The U.S. oliguria market captured the largest share within North America in 2025, driven by high ICU admission rates, advanced critical care infrastructure, and strong adoption of early-stage kidney injury monitoring technologies. Hospitals increasingly rely on automated urine output tracking systems and integrated electronic health records to improve early detection and management of oliguria in critically ill patients. The country’s strong focus on precision medicine and evidence-based critical care protocols further supports widespread use of diuretics and fluid management therapies. In addition, strong presence of leading pharmaceutical companies and continuous innovation in hospital monitoring technologies are significantly contributing to market growth in the U.S.

Europe Oliguria Market Insight

Europe is projected to expand at a substantial CAGR during the forecast period, primarily driven by rising incidence of chronic kidney disease, increasing ICU admissions, and strong regulatory emphasis on improving patient safety and treatment outcomes in hospital settings. The region benefits from well-structured healthcare systems that increasingly emphasize standardized critical care protocols, encouraging early detection and effective management of oliguria in hospitalized patients. In addition, growing adoption of automated monitoring technologies, increasing geriatric population, and continuous investments in hospital modernization are collectively supporting the expansion of oliguria diagnosis and treatment solutions across Europe.

U.K. Oliguria Market Insight

The U.K. oliguria market is expected to witness steady growth during the forecast period, driven by increasing burden of hospital-acquired acute kidney injury and strong focus on improving critical care outcomes within the National Health Service (NHS) framework. The country is witnessing rising adoption of advanced ICU monitoring systems and standardized renal care pathways aimed at early detection of oliguria in high-risk patients. Furthermore, increasing awareness among healthcare professionals regarding fluid balance management and growing integration of digital health tools in hospitals are supporting overall market expansion in the U.K.

Germany Oliguria Market Insight

The Germany oliguria market is projected to grow at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high adoption of advanced medical technologies, and increasing emphasis on precision-based critical care. The country’s focus on early diagnosis and structured hospital protocols supports effective monitoring and treatment of oliguria, particularly in intensive care and post-surgical recovery settings. In addition, rising investment in healthcare digitalization and strong presence of research-driven clinical practices are enhancing adoption of innovative renal monitoring solutions across German healthcare facilities.

Asia-Pacific Oliguria Market Insight

Asia-Pacific is expected to be the fastest growing region in the oliguria market during the forecast period, driven by rising prevalence of diabetes, hypertension, and kidney-related disorders, along with rapid expansion of healthcare infrastructure. Increasing ICU admissions, improving access to critical care services, and growing awareness regarding early detection of acute kidney injury are significantly boosting demand for oliguria management solutions. Furthermore, rising healthcare expenditure, expanding hospital networks, and increasing adoption of modern diagnostic and monitoring technologies are accelerating market growth across emerging economies in the region

Japan Oliguria Market Insight

Japan oliguria market is witnessing strong growth driven by its advanced healthcare system, rapidly aging population, and increasing incidence of renal dysfunction cases requiring intensive monitoring. The country places strong emphasis on precision healthcare and early diagnosis, leading to widespread adoption of advanced ICU monitoring systems for urine output and kidney function assessment. In addition, integration of digital health technologies and increasing use of automated hospital systems are improving efficiency in oliguria detection and management across Japanese healthcare institutions.

India Oliguria Market Insight

India accounted for the largest market share in Asia-Pacific in 2025, supported by rapid urbanization, growing burden of chronic diseases, and increasing hospital admissions for critical care conditions. Expanding healthcare infrastructure, rising awareness of kidney health, and increasing availability of affordable critical care therapies are driving adoption of oliguria management solutions. Furthermore, government initiatives promoting healthcare modernization, expansion of ICU facilities, and development of smart hospitals are significantly contributing to market growth across the country.

Oliguria Market Share

The Oliguria industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Sanofi (France)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Baxter (U.S.)

- B. Braun SE (Germany)

- Fresenius Kabi AG (Germany)

- AstraZeneca (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Limited (Israel)

- Sun Pharmaceutical Industries Limited (India)

- Cipla Limited (India)

- Dr. Reddy’s Laboratories Limited (India)

- Sandoz Group AG (Switzerland)

- Amgen Inc. (U.S.)

- Viatris Inc. (U.S.)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

What are the Recent Developments in Global Oliguria Market?

- In June 2025, a clinical meta-analysis published in the Journal of Intensive Care highlighted that prophylactic use of diuretics may significantly reduce the incidence of acute kidney injury (AKI) in high-risk patients, although it showed no benefit in established AKI cases, influencing evolving oliguria management approaches in critical care settings

- In April 2025, a multicenter ICU cohort study published in Journal of Clinical Medicine found that furosemide administration significantly improves urine output and resolves oliguria more effectively than no intervention or fluid bolus, reinforcing its role as a key pharmacological agent in acute oliguria management

- In May 2025, a prospective observational study published in Critical Care reported that combining spontaneous diuresis assessment with the furosemide stress test improves prediction of kidney recovery and discontinuation of renal replacement therapy in critically ill patients, strengthening evidence for dynamic urine output monitoring in oliguria care

- In February 2025, a clinical study published in the Journal of Critical Care demonstrated that the furosemide stress test can help predict renal recovery and successful discontinuation of continuous renal replacement therapy (CRRT) in ICU patients with AKI, supporting better decision-making in oliguria-related kidney failure management

- In January 2024, a machine-learning-based ICU study published in Scientific Reports demonstrated that electronic health record–driven predictive models can effectively forecast oliguria in critically ill patients before clinical onset, enabling earlier intervention for acute kidney injury risk management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.