Global Olivopontocerebellar Atrophy Opca Market

Market Size in USD Million

USD

524.20 Million

USD

728.51 Million

2024

2032

USD

524.20 Million

USD

728.51 Million

2024

2032

| 2025 - 2032 | |

| USD 524.20 Million | |

| USD 728.51 Million | |

| % | |

|

Olivopontocerebellar Atrophy (OPCA) Market Size

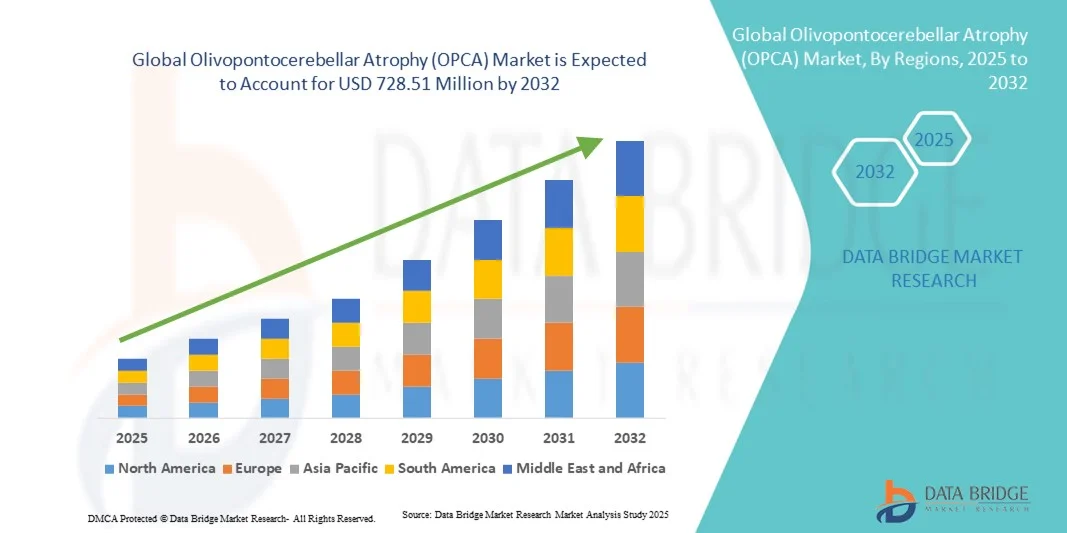

- The global Olivopontocerebellar Atrophy (OPCA) market size was valued at USD 524.20 million in 2024 and is expected to reach USD 728.51 million by 2032, at a CAGR of 4.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurodegenerative disorders and advancements in diagnostic imaging and molecular testing that enhance early detection and patient management of OPCA

- Furthermore, rising investments in neurological research, expanding clinical trials for targeted therapies, and heightened awareness regarding rare ataxia syndromes are driving market expansion. These combined developments are strengthening therapeutic innovation and significantly propelling the industry’s growth trajectory

Olivopontocerebellar Atrophy (OPCA) Market Analysis

- Olivopontocerebellar atrophy (OPCA), a rare neurodegenerative condition characterized by progressive cerebellar and brainstem atrophy, is witnessing growing clinical focus as advancements in neurological diagnostics and therapeutic management continue to evolve globally

- The market growth is primarily driven by the rising prevalence of neurodegenerative disorders, ongoing clinical research in ataxia-related conditions, and expanding access to advanced treatment and genetic testing technologies

- North America dominated the OPCA market with the largest revenue share of 40.2% in 2024, supported by robust healthcare infrastructure, extensive research funding for rare neurological diseases, and early adoption of advanced diagnostic and therapeutic approaches

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, attributed to improving healthcare access, growing awareness of rare disorders, and increasing government initiatives supporting neurological disease research and patient care

- The Hereditary OPCA segment dominated the market with a share of 46.9% in 2024, driven by the higher reported incidence of inherited ataxia cases, expanding genetic testing adoption, and ongoing studies exploring novel gene-targeted therapeutic interventions

Report Scope and Olivopontocerebellar Atrophy (OPCA) Market Segmentation

|

Attributes |

Olivopontocerebellar Atrophy (OPCA) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Olivopontocerebellar Atrophy (OPCA) Market Trends

Advancements in Genetic Research and Neuroimaging Technologies

- A significant and accelerating trend in the global olivopontocerebellar atrophy (OPCA) market is the growing emphasis on genetic and neuroimaging advancements, which are enhancing early diagnosis and enabling more precise differentiation between hereditary and sporadic forms of the disease

- For instance, recent developments in whole-exome sequencing and MRI-based volumetric imaging have improved clinicians’ ability to identify characteristic cerebellar and pontine atrophy patterns, facilitating earlier intervention and improved patient management

- Genetic insights are helping researchers uncover specific gene mutations associated with OPCA, supporting the emergence of targeted therapy pipelines and personalized medicine approaches that were previously unavailable for this rare condition. Furthermore, advanced imaging biomarkers are increasingly being adopted to monitor disease progression and evaluate treatment efficacy in clinical trials

- The integration of digital health tools and AI-based analytics into neurological diagnostics further enhances the precision of OPCA detection. Through machine learning, clinicians can now identify subtle changes in cerebellar structure and motor function, enabling better prognostic assessments and therapy planning

- This trend toward precision diagnostics and personalized treatment strategies is fundamentally reshaping the management landscape for neurodegenerative disorders. Consequently, research institutions and biotech firms are investing heavily in gene-focused studies and neuroimaging innovation to accelerate therapeutic discovery in OPCA

- The demand for advanced diagnostic platforms and precision-based neurological tools is growing rapidly across both clinical and research settings, as healthcare providers increasingly prioritize early detection and individualized patient management in rare neurodegenerative diseases

Olivopontocerebellar Atrophy (OPCA) Market Dynamics

Driver

Rising Prevalence of Neurodegenerative Disorders and Advancements in Therapeutic Research

- The increasing incidence of neurodegenerative diseases worldwide, coupled with growing awareness and diagnostic capability for rare ataxias such as OPCA, is a significant driver for the expanding market demand

- For instance, in March 2024, Biohaven Ltd. announced progress in clinical research for neurodegenerative ataxia treatment candidates, highlighting the growing industry focus on developing disease-modifying therapies for OPCA-related conditions. Such advancements are expected to drive market growth over the forecast period

- As the global population ages and the prevalence of genetic and sporadic ataxias rises, there is an increasing demand for improved diagnostic, therapeutic, and supportive care solutions that can manage progressive neurological deterioration effectively

- Furthermore, ongoing clinical trials, strong R&D investments in neuroprotective agents, and cross-collaborations between academic centers and biotech firms are accelerating therapeutic pipeline development for OPCA

- The growing availability of specialized diagnostic centers, improved patient registries, and digital data-sharing initiatives are enabling faster identification, better treatment monitoring, and stronger patient engagement globally, fueling overall market expansion

Restraint/Challenge

High Diagnostic Complexity and Limited Therapeutic Availability

- Challenges surrounding the accurate and timely diagnosis of OPCA due to its overlapping symptoms with other cerebellar ataxias pose a major restraint to effective disease management and market expansion

- For instance, studies have shown that many OPCA cases remain misclassified as idiopathic ataxias, delaying appropriate treatment initiation and clinical follow-up, thereby impacting patient outcomes and care optimization

- Addressing these diagnostic challenges through advanced neuroimaging, genetic testing, and increased clinician training is crucial to ensure accurate identification and management of OPCA patients. In addition, the limited number of approved disease-modifying therapies restricts the treatment landscape for patients and clinicians

- While supportive and symptomatic treatments exist, the absence of curative therapies continues to limit patient quality of life and long-term prognosis. The high cost of advanced diagnostic procedures and the scarcity of specialized treatment centers in developing regions further exacerbate accessibility challenges

- Overcoming these hurdles through continued research funding, increased global awareness, and development of targeted therapeutic interventions will be vital for improving diagnostic precision and expanding treatment opportunities in the OPCA market

Olivopontocerebellar Atrophy (OPCA) Market Scope

The market is segmented on the basis of type, gender, drug class, indication, route of administration, end user, and distribution channel.

- By Type

On the basis of type, the OPCA market is segmented into hereditary OPCA and sporadic OPCA. The Hereditary OPCA segment dominated the market with the largest revenue share of 46.9% in 2024, driven by the higher prevalence of genetically inherited ataxia syndromes. Hereditary OPCA patients are often diagnosed through family history assessment and genetic testing, which are increasingly accessible due to advancements in molecular diagnostics. The segment benefits from growing awareness among healthcare providers regarding early diagnosis and intervention. Furthermore, hereditary cases are frequently included in clinical trials, which boosts investment in supportive care and therapeutic development. Increasing funding for gene-targeted research and the development of novel therapeutics also strengthens the segment's dominance. Overall, hereditary OPCA remains the primary revenue contributor due to its established patient base and continuous R&D focus.

The Sporadic OPCA segment is anticipated to witness the fastest growth rate during the forecast period, attributed to the increasing recognition of non-genetic forms of the disorder and improved diagnostic capabilities. Sporadic cases are often linked to environmental and unknown etiologies, which drives demand for comprehensive diagnostic screening and disease monitoring. Rising awareness campaigns and adoption of advanced neuroimaging have enabled earlier identification of sporadic OPCA, fueling therapeutic uptake. In addition, expanding government initiatives supporting rare neurological disorders are helping improve detection rates. The entry of emerging biotech companies into sporadic OPCA research is also contributing to growth. These factors collectively position sporadic OPCA as the fastest-growing segment in the market.

- By Gender

On the basis of gender, the market is segmented into male and female patients. The Male segment dominated the market in 2024, primarily due to higher reported incidence rates of certain hereditary ataxias in males and early diagnostic uptake in clinical settings. Men often present with earlier or more pronounced symptoms in specific genetic variants, which has influenced the higher utilization of diagnostic and supportive therapies. Clinical research and treatment pipelines have historically included more male patients, further strengthening market dominance. In addition, male patients frequently access specialized neurology centers, increasing hospital revenue for this segment. Public health campaigns targeting male populations for rare neurological disorder screenings also contribute to segment growth.

The Female segment is expected to register the fastest growth over the forecast period, driven by increasing awareness of OPCA in women and improved access to diagnostic services. Advances in genetic counseling and neuroimaging techniques have enabled earlier identification of ataxia syndromes in females, boosting adoption of supportive care. Growing inclusion of female cohorts in clinical trials and rare disease research is expanding opportunities for targeted therapies. Awareness campaigns emphasizing female neurological health are also improving diagnosis rates. The rise of home-based monitoring and telemedicine services for women is further accelerating growth. Collectively, these factors are expected to position the female segment as the fastest-growing gender category in OPCA.

- By Drug Class

On the basis of drug class, the market is segmented into dopaminergic agents, serotonin 5-hydroxytryptophan (5HT) 1-a receptor agonists, antihypertensive agents, antianxiety agents, interferons, decarboxylase inhibitors, immunomodulators, and antidepressants. The Dopaminergic Agents segment dominated the market in 2024, as these drugs help manage motor dysfunction and coordination issues associated with OPCA. Dopaminergic therapy is widely prescribed due to its effectiveness in alleviating tremors, rigidity, and gait disturbances, which are common in hereditary and sporadic cases. Clinical adoption is supported by ongoing trials investigating optimized dosing and combination therapies. Physicians also favor dopaminergic agents due to well-established safety profiles and extensive clinical experience. The segment’s dominance is further enhanced by patient adherence, as oral dopaminergic formulations are convenient for long-term use. Overall, dopaminergic agents remain the largest revenue contributor in the drug class category.

The Immunomodulators segment is expected to witness the fastest growth during the forecast period, driven by increasing research on immune-related pathways in neurodegeneration and emerging therapies targeting inflammatory components of OPCA. Novel immunomodulatory agents are being investigated in clinical studies, creating significant opportunities for market expansion. Improved understanding of the role of inflammation in cerebellar atrophy has accelerated adoption of immunomodulatory therapy. Growing awareness among physicians about potential disease-modifying effects is encouraging broader prescription. In addition, collaborations between biotech firms and academic institutions are supporting pipeline development. These factors collectively position immunomodulators as the fastest-growing drug class segment.

- By Indication

On the basis of indication, the market is segmented into multiple sclerosis, Parkinson’s Disease, Alzheimer’s Disease, Spinal Muscular Atrophy (SMA), And Others. The Parkinson’s Disease segment dominated the market in 2024, as OPCA shares overlapping motor symptoms with Parkinsonian syndromes, leading to higher prescription of symptomatic therapies commonly used for Parkinson’s disease. Treatment protocols and physician familiarity with motor symptom management have contributed to this dominance. In addition, research in Parkinsonian neurodegeneration has helped improve supportive therapies for OPCA patients. Market growth is supported by increasing patient diagnosis rates and rising adoption of dopaminergic agents. The segment also benefits from inclusion in clinical trials focusing on overlapping neurodegenerative pathways. Overall, Parkinson’s Disease indication drives the largest revenue share in OPCA therapeutics.

The SMA and Others segment is expected to grow the fastest during the forecast period, fueled by increasing identification of less common ataxia-related indications and expansion of orphan drug pipelines. Advances in genetic screening and neuromuscular diagnostics are allowing earlier detection of SMA and related disorders in OPCA patients. Clinical trial participation for rare indications is increasing, creating significant market opportunities. Government initiatives supporting rare neurological disorder treatment are helping expand access. Patient advocacy groups are raising awareness and improving early intervention rates. Collectively, these factors are expected to make SMA and Others the fastest-growing indication segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The Oral segment dominated in 2024, driven by patient preference for non-invasive, convenient administration and the availability of most symptomatic and supportive therapies in oral formulations. Oral drugs improve adherence to long-term treatment plans, especially for chronic management of motor and cognitive symptoms. Physicians prefer oral therapy due to ease of administration and established dosing protocols. Oral administration also reduces hospital visits and associated costs, benefiting healthcare systems. Established supply chains ensure ready availability of oral medications. Overall, oral route remains the largest contributor to revenue.

The Parenteral segment is expected to witness the fastest growth during the forecast period, owing to the development of novel biologics, immunomodulators, and targeted therapies requiring intravenous or subcutaneous delivery. Parenteral formulations allow precise dosing and better bioavailability for advanced therapies under clinical investigation. Specialty hospitals and clinics are increasingly adopting parenteral therapy to optimize outcomes. Patient adherence is supported through professional administration and monitoring. Clinical trial pipelines focusing on biologics and immunotherapies are driving adoption. These factors position the parenteral route as the fastest-growing segment.

- By End User

On the basis of end user, the market is segmented into hospitals, home care, and specialty clinics. The Hospitals segment dominated the market in 2024, attributed to higher patient inflow, access to advanced diagnostics, and availability of multidisciplinary care teams for rare neurological disorders. Hospitals also serve as primary sites for clinical trials, therapeutic interventions, and ongoing patient monitoring. Revenue generation is supported by both inpatient and outpatient services. Hospitals also play a key role in patient education and genetic counseling. Overall, hospitals remain the dominant end user segment.

The Specialty Clinics segment is expected to grow the fastest during the forecast period, as increased awareness of rare ataxias and expansion of neurology-focused centers are improving access to targeted therapies. Specialty clinics provide personalized care, early diagnosis, and long-term disease management. They often participate in clinical trials, which drives therapy adoption. Growing patient preference for specialized centers improves market penetration. Technological integration, such as telemedicine and digital monitoring, supports rapid growth. Collectively, specialty clinics are emerging as the fastest-growing end user segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated in 2024, due to administration of specialized therapies and availability of prescription drugs for rare neurological disorders directly within hospital settings. Hospitals coordinate treatment plans, monitor therapy efficacy, and provide patient education. Hospital pharmacies also benefit from bulk procurement and established supply chains. Physician preference for hospital-based dispensing supports revenue generation. Access to advanced therapies and clinical trials reinforces hospital pharmacy dominance.

The Online Pharmacy segment is expected to witness the fastest growth during the forecast period, driven by the increasing acceptance of telemedicine, e-prescriptions, and home delivery services for rare disease therapies. Online platforms improve accessibility for patients in remote or underserved areas. Digital platforms also enhance convenience and support long-term adherence. Growth is accelerated by increased e-commerce penetration and patient comfort with digital health solutions. Collaboration with specialty pharmacies and patient support programs further fuels adoption. Online pharmacy is poised to be the fastest-growing distribution channel segment.

Olivopontocerebellar Atrophy (OPCA) Market Regional Analysis

- North America dominated the OPCA market with the largest revenue share of 40.2% in 2024, supported by robust healthcare infrastructure, extensive research funding for rare neurological diseases, and early adoption of advanced diagnostic and therapeutic approaches

- Patients and clinicians in the region benefit from widespread availability of specialized diagnostic centers, cutting-edge neuroimaging technologies, and access to innovative therapeutic options, which support early diagnosis and effective disease management

- This widespread adoption is further supported by well-established rare disease registries, high patient awareness, and collaborations between academic institutions and biotechnology companies, establishing North America as a key hub for OPCA research, clinical trials, and treatment solutions

U.S. Olivopontocerebellar Atrophy (OPCA) Market Insight

The U.S. OPCA market captured the largest revenue share of 80.6% in 2024 within North America, fueled by advanced healthcare infrastructure, widespread availability of genetic testing, and high awareness of rare neurodegenerative disorders. Patients and clinicians increasingly prioritize early diagnosis through cutting-edge neuroimaging and molecular diagnostics. The growing trend of personalized medicine and participation in clinical trials for gene-targeted therapies further propels market growth. In addition, strong R&D investments by biotech firms and collaborations with academic institutions are expanding therapeutic options. The U.S. also benefits from well-established rare disease registries, which enhance patient identification and long-term disease management, reinforcing its dominant market position.

Europe Olivopontocerebellar Atrophy (OPCA) Market Insight

The Europe OPCA market is projected to expand at a substantial CAGR throughout the forecast period, driven by increased awareness of rare neurological disorders and the rising adoption of advanced diagnostic technologies. The presence of specialized neurology centers, coupled with government initiatives supporting rare disease management, fosters early diagnosis and therapy adoption. European healthcare systems emphasize patient registries and genetic counseling, which strengthens disease monitoring and clinical research. The region is witnessing significant growth across hospitals, specialty clinics, and research institutions, with OPCA management being integrated into multidisciplinary care approaches. Furthermore, collaborations between biotech companies and healthcare providers are accelerating the development of novel therapeutic interventions.

U.K. Olivopontocerebellar Atrophy (OPCA) Market Insight

The U.K. OPCA market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of hereditary and sporadic ataxias and the desire for early, precise diagnosis. Concerns regarding progressive neurological impairment encourage patients and caregivers to seek timely intervention and specialized care. In addition, the U.K.’s advanced healthcare infrastructure and emphasis on genetic testing are promoting wider adoption of diagnostic and therapeutic solutions. The integration of OPCA management into academic hospitals and specialty clinics supports clinical research and treatment optimization. Public and private funding for rare neurological disorders further stimulates market expansion.

Germany Olivopontocerebellar Atrophy (OPCA) Market Insight

The Germany OPCA market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of neurodegenerative disorders and the demand for advanced, precise diagnostic solutions. Germany’s robust healthcare infrastructure, focus on innovation, and well-established neurology centers promote adoption of molecular diagnostics and early intervention strategies. The integration of OPCA management into specialized hospitals and research facilities ensures better patient care and monitoring. Furthermore, participation in international clinical trials and government initiatives supporting rare diseases are accelerating therapy development. The preference for personalized treatment approaches aligns with local patient expectations, supporting sustained market growth.

Asia-Pacific Olivopontocerebellar Atrophy (OPCA) Market Insight

The Asia-Pacific OPCA market is poised to grow at the fastest CAGR during the forecast period, driven by increasing awareness of rare neurological disorders, rising healthcare spending, and improving diagnostic capabilities in countries such as China, Japan, and India. The growing inclination toward early disease detection and access to specialized neurology care is expanding the patient base. Furthermore, government initiatives supporting rare disease research and patient registries are facilitating clinical trials and therapeutic adoption. The region’s expanding healthcare infrastructure and rising number of specialty clinics and hospitals are improving accessibility for both urban and semi-urban populations. Collaborations between local and global biotech firms are also contributing to market growth.

Japan Olivopontocerebellar Atrophy (OPCA) Market Insight

The Japan OPCA market is gaining momentum due to the country’s advanced healthcare system, high patient awareness, and strong focus on neurodegenerative research. Early diagnosis is increasingly emphasized through the adoption of genetic testing and neuroimaging, enhancing treatment planning and disease monitoring. The growing elderly population, combined with rising healthcare expenditure, is driving demand for specialized care and supportive therapies. Integration of OPCA management into hospitals and specialty clinics ensures comprehensive treatment approaches. Clinical trials focusing on gene-targeted and immunomodulatory therapies further support market expansion. Patient-centric initiatives and public awareness campaigns are also contributing to steady market growth.

India Olivopontocerebellar Atrophy (OPCA) Market Insight

The India OPCA market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to increasing awareness of rare neurological disorders, rising healthcare access, and the growth of specialty clinics and hospitals. India is witnessing a rise in genetic testing adoption and improved diagnostic services for hereditary and sporadic OPCA cases. Expansion of neurology centers, government programs supporting rare diseases, and growing patient advocacy are key factors propelling market growth. The affordability of diagnostic services and therapies, along with collaborations between local and international biotech firms, further enhances accessibility. Increasing clinical research activities and patient registries are also strengthening market development.

Olivopontocerebellar Atrophy (OPCA) Market Share

The Olivopontocerebellar Atrophy (OPCA) industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Vertex Pharmaceuticals Incorporated (U.S.)

- Biogen Inc. (U.S.)

- Horizon Therapeutics plc (Ireland)

- AstraZeneca (U.K.)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Sanofi (France)

- AbbVie Inc. (U.S.)

- Amneal Pharmaceuticals Inc. (U.S.)

- Boehringer Ingelheim GmbH (Germany)

- GSK plc (U.K.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

What are the Recent Developments in Global Olivopontocerebellar Atrophy (OPCA) Market?

- In October 2025, Ono Pharmaceutical announced encouraging efficacy signals from an interim analysis of its ongoing Phase 2 clinical trial of ONO-2808, a S1P5 receptor agonist, in patients with Multiple System Atrophy. This collaboration with Bristol-Myers Squibb KK aims to explore new therapeutic avenues for MSA, which shares pathophysiological features with OPCA

- In October 2025, At the American Conference on Pharmacometrics (ACoP) 2025, Certara unveiled two major innovations transforming the future of modeling and simulation in drug development. These advancements aim to empower teams with speed, scalability, and scientific precision, potentially accelerating the development of therapies for OPCA and related disorders

- In August 2025, a collaborative initiative focused on spinocerebellar ataxia research in the United States highlighted the progress toward clinical trials targeting the underlying genetic causes of cerebellar ataxias, including OPCA. The collaboration emphasizes the importance of addressing challenges such as obtaining large cohort sizes and developing sensitive biomarkers for rare neurodegenerative diseases

- In January 2025, Alterity Therapeutics announced positive results from its Phase 2 clinical trial of ATH434 for the treatment of Multiple System Atrophy (MSA), a condition related to OPCA. The trial demonstrated robust clinical efficacy, leading to the granting of Fast Track Designation by the U.S. FDA. This development underscores the company's commitment to advancing treatments for neurodegenerative disorders

- In February 2024, Alterity Therapeutics presented new data at the American Academy of Neurology (AAN) Annual Meeting, showcasing the potential of ATH434 in treating MSA. This presentation highlighted the company's ongoing commitment to addressing the unmet needs in neurodegenerative diseases related to OPCA

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.