Global Olliers Disease Market

Market Size in USD Million

USD

825.00 Million

USD

1,191.31 Million

2024

2032

USD

825.00 Million

USD

1,191.31 Million

2024

2032

| 2025 - 2032 | |

| USD 825.00 Million | |

| USD 1,191.31 Million | |

| % | |

|

Ollier’s Disease Market Size

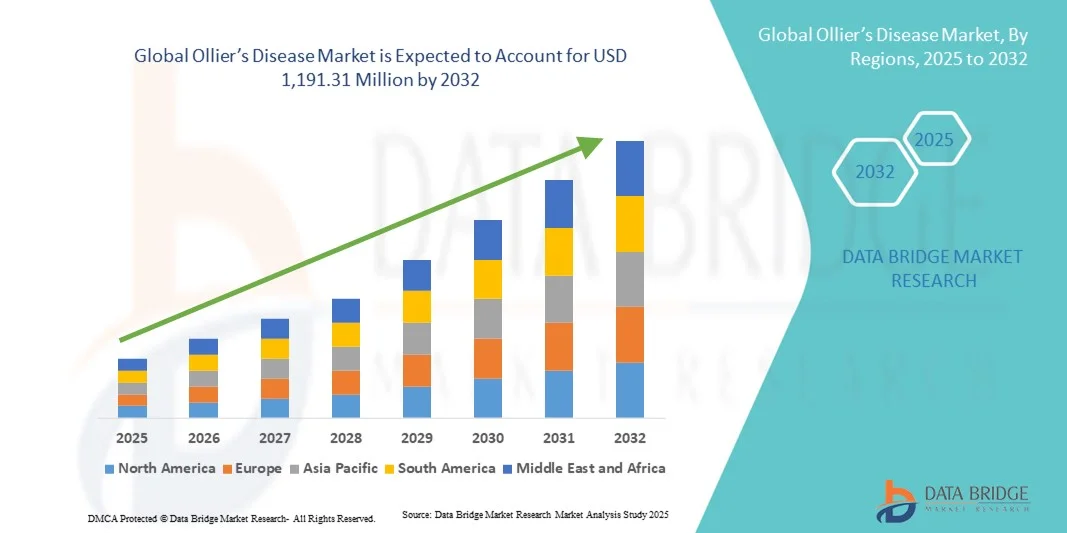

- The global Ollier’s disease market size was valued at USD 825.00 million in 2024 and is expected to reach USD 1,191.31 million by 2032, at a CAGR of 4.7% during the forecast period

- The market growth is largely fueled by the increasing prevalence of rare skeletal disorders, advancements in diagnostic imaging, and growing research initiatives aimed at developing targeted therapies for enchondromatosis

- Furthermore, rising awareness among healthcare providers, expanding genetic testing adoption, and the push for orphan drug development are establishing specialized treatments and management options as the core of this market. These converging factors are accelerating healthcare innovation in rare bone disorders, thereby significantly boosting the industry’s growth

Ollier’s Disease Market Analysis

- Ollier’s disease, a rare non-hereditary skeletal disorder characterized by multiple enchondromas, is increasingly recognized as a critical focus in rare bone disease management, with growing emphasis on early diagnosis, personalized treatment, and ongoing research into effective drug therapies and surgical interventions

- The escalating demand for Ollier’s disease management is primarily fueled by advancements in drug development, rising awareness among healthcare providers, and the increasing adoption of diagnostic imaging and genetic testing to monitor disease progression and prevent complications

- North America dominated the Ollier’s disease market with the largest revenue share of 55.9% in 2024. This dominance can be attributed to several factors such as robust healthcare infrastructure, advanced technological developments in disease management and treatment, along with an increasing prevalence of rare disorders prompting stronger regulatory support for research and therapies

- Asia-Pacific is expected to be the fastest-growing region in the Ollier’s disease market during the forecast period due to increasing healthcare access, rising awareness about rare bone disorders, and growing investments in specialized hospitals and clinics catering to rare diseases

- Medication segment dominated the Ollier’s disease market with a market share of 46.5% in 2024, driven by the use of drug classifications such as Denosumab, Dactinomycin, and Methotrexate Sodium, coupled with increasing availability through hospital pharmacies, retail pharmacies, and online pharmacy channels

Report Scope and Ollier’s Disease Market Segmentation

|

Attributes |

Ollier’s Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ollier’s Disease Market Trends

Advancements in Targeted Drug Therapies and Personalized Care

- A significant and accelerating trend in the global Ollier’s disease market is the development of targeted drug therapies and personalized treatment approaches, enhancing disease management and patient outcomes

- For instance, Denosumab and Methotrexate Sodium are increasingly used to manage enchondromas and prevent skeletal deformities, offering a pharmacological alternative to purely surgical interventions

- Personalized care through genetic testing and advanced imaging enables physicians to tailor treatment plans for individual patients, monitor disease progression more accurately, and optimize therapeutic outcomes

- Integration of multidisciplinary approaches, combining medication, surgery, and supportive therapies, is facilitating comprehensive management of Ollier’s disease, improving quality of life and reducing complications

- This trend towards targeted, patient-specific treatment strategies is fundamentally reshaping physician and patient expectations for rare bone disorder management. Consequently, companies and research institutes are increasingly focusing on drug development and clinical trials that support precision medicine approaches

- The demand for innovative therapies and personalized care solutions is growing rapidly across hospitals, specialty clinics, and homecare settings, as patients and providers prioritize effectiveness, safety, and improved long-term outcomes

Ollier’s Disease Market Dynamics

Driver

Rising Awareness and Adoption of Rare Disease Management

- The increasing prevalence of awareness programs and specialized healthcare initiatives for rare skeletal disorders is a significant driver for the heightened demand for Ollier’s disease management solutions

- For instance, in 2024, leading hospitals and rare disease foundations launched initiatives to improve early diagnosis and facilitate access to Denosumab and Methotrexate Sodium treatment options

- As healthcare providers become more aware of disease progression and potential complications, adoption of advanced diagnostic imaging, genetic testing, and early interventions is rising, enhancing treatment efficacy

- Furthermore, the growing emphasis on personalized medicine and integrated care is making Ollier’s disease management a priority in specialized hospitals and clinics, improving access to comprehensive treatment

- Increasing funding for rare disease research and orphan drug development is enabling the creation of new treatment options and expanding patient access, especially in North America and Europe

- Collaboration between hospitals, research institutes, and pharmaceutical companies is accelerating clinical trials and real-world studies, contributing to faster innovation and better therapeutic outcomes

- Availability of multiple distribution channels, including hospital pharmacy, retail pharmacy, and online pharmacy, along with increased patient education, is further propelling the adoption of pharmacological therapies in addition to surgical interventions

Restraint/Challenge

Limited Awareness and High Treatment Costs

- Low awareness about Ollier’s disease among general practitioners and patients poses a significant challenge to broader market adoption and early intervention

- For instance, delayed diagnosis due to misinterpretation of enchondromas or rare bone deformities often results in progression of skeletal complications before treatment begins

- High costs associated with specialized drug therapies, genetic testing, and surgical interventions limit accessibility, particularly in developing regions or for patients without comprehensive healthcare coverage

- While some initiatives aim to reduce costs and improve patient outreach, the overall affordability and accessibility of comprehensive care remain significant barriers to market expansion

- Variability in healthcare insurance coverage for rare disease treatments creates disparities in patient access to medication and surgery, affecting adoption rates

- Complex regulatory approvals for orphan drugs can delay the introduction of new therapies in key markets, hindering treatment innovation and availability

- Overcoming these challenges through awareness campaigns, patient support programs, and cost-effective treatment options will be vital for sustained market growth

Ollier’s Disease Market Scope

The market is segmented on the basis of drug classification, treatment, distribution channel, and end-users

- By Drug Classification

On the basis of drug classification, the Ollier’s disease market is segmented into dactinomycin, denosumab, doxorubicin hydrochloride, methotrexate sodium, trexall (methotrexate sodium), xgeva (denosumab), and others. The Denosumab segment dominated the market with the largest revenue share in 2024, driven by its proven efficacy in controlling enchondromas and preventing skeletal complications associated with Ollier’s disease. Denosumab is increasingly preferred in both pediatric and adult patients for its targeted mechanism of action and fewer side effects compared to traditional chemotherapeutic agents. Healthcare providers favor Denosumab for its ability to reduce bone lesions and improve mobility, and it is widely adopted in specialized hospitals and rare disease clinics. The availability of branded formulations such as Xgeva further strengthens market adoption. Growing awareness of pharmacological management options and ongoing clinical research supporting long-term safety also contribute to the dominance of this segment.

The Methotrexate Sodium segment is expected to witness the fastest CAGR during the forecast period, driven by its increasing adoption as an adjunct therapy in managing skeletal deformities. Methotrexate’s affordability and accessibility through hospital and retail pharmacies enhance its appeal, particularly in emerging regions. In addition, healthcare providers are integrating Methotrexate Sodium with multidisciplinary treatment plans, which supports faster uptake. Patient support programs and clinical initiatives promoting early intervention further fuel its rapid growth.

- By Treatment

On the basis of treatment, the Ollier’s disease market is segmented into medication, surgery, and others. The Medication segment dominated the Ollier’s disease market with a market share of 46.5% in 2024, driven by the increasing adoption of drug therapies such as Denosumab and Methotrexate Sodium for managing enchondromas and preventing skeletal deformities. Medications are preferred for their non-invasive nature and ability to complement surgical interventions, improving overall patient outcomes. Growing awareness among healthcare providers and patients regarding pharmacological management options further supports market dominance. Availability through multiple distribution channels including hospital, retail, and online pharmacies enhances accessibility. Patient support programs, clinical trials, and orphan drug incentives also encourage the adoption of medication-based therapies.

The Surgery segment is expected to witness the fastest growth rate during the forecast period, driven by advancements in minimally invasive procedures and corrective orthopedic surgeries. Integration with pharmacological treatment plans improves post-operative outcomes. Increasing investment in specialized orthopedic and rare disease centers globally supports rapid adoption. The rising number of early-diagnosed patients seeking corrective surgeries, along with innovations in surgical technology and imaging, further fuels segment growth

- By Distribution Channel

On the basis of distribution channel, the Ollier’s disease market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2024, driven by the direct availability of specialized medications such as Denosumab and Methotrexate Sodium for rare disease management. Hospitals provide comprehensive care including diagnosis, drug administration, monitoring, and follow-up, making hospital pharmacies a preferred channel for both pediatric and adult patients. Access to trained healthcare professionals and integrated patient support programs further strengthens the segment’s dominance. Frequent hospital visits for imaging and treatment monitoring enhance reliance on hospital pharmacies. Government hospitals and rare disease centers also contribute significantly to the revenue share.

The Online Pharmacy segment is expected to witness the fastest growth during the forecast period, driven by increasing patient preference for home delivery of medications. Online pharmacies improve access to specialty drugs in regions with limited hospital or retail facilities. Integration of telemedicine platforms with online pharmacies allows patients to consult specialists and receive prescriptions seamlessly. The convenience, affordability, and increasing adoption of digital healthcare solutions are key factors driving this segment’s rapid growth.

- By End-Users

On the basis of end-users, the Ollier’s disease market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with the largest revenue share in 2024, as hospitals provide the complete spectrum of care from diagnosis and treatment to follow-up management. Hospitals are preferred due to their infrastructure, availability of specialized surgeons, access to rare disease medications, and multidisciplinary care teams. Pediatric and orthopedic departments in hospitals manage complex Ollier’s disease cases, reinforcing their dominant position. Collaboration with pharmaceutical companies and participation in clinical trials further strengthen the hospital segment.

The Homecare segment is expected to witness the fastest growth rate during the forecast period, driven by increasing adoption of home-based monitoring, telemedicine, and remote drug delivery services. Patients prefer homecare for convenience, reduced travel, and personalized attention, especially for long-term medication adherence. Rising awareness among caregivers, patient support programs, and integration with online pharmacies are fueling this rapid growth. Homecare services also enable closer monitoring of therapy responses and early detection of complications, contributing to their accelerating adoption.

Ollier’s Disease Market Regional Analysis

- North America dominated the Ollier’s disease market with the largest revenue share of 55.9% in 2024. This dominance can be attributed to several factors such as robust healthcare infrastructure, advanced technological developments in disease management and treatment, along with an increasing prevalence of rare disorders prompting stronger regulatory support for research and therapies

- Healthcare providers and patients in the region highly value early diagnosis, access to specialized medications such as Denosumab and Methotrexate Sodium, and integrated treatment approaches combining surgery and pharmacological interventions

- This widespread adoption is further supported by the presence of leading hospitals, rare disease centers, high disposable incomes, and the growing preference for personalized care, establishing North America as the primary market for Ollier’s disease management

U.S. Ollier’s Disease Market Insight

The U.S. Ollier’s disease market captured the largest revenue share in 2024 within North America, fueled by advanced healthcare infrastructure, widespread awareness of rare skeletal disorders, and strong investment in orphan drugs and targeted therapies. Patients and healthcare providers increasingly prioritize early diagnosis and access to medications such as Denosumab and Methotrexate Sodium. The growing trend of integrated care combining pharmacological and surgical interventions further propels the market. Moreover, participation in clinical trials, patient support programs, and the availability of specialized rare disease centers significantly contribute to market expansion.

Europe Ollier’s Disease Market Insight

The Europe Ollier’s disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government support for rare disease research and the establishment of patient registries. Increasing urbanization and better access to specialized healthcare facilities are fostering adoption of both pharmacological and surgical treatments. European patients value early intervention, personalized care, and multidisciplinary approaches. The region is witnessing significant growth across hospitals, specialty clinics, and homecare services, with enhanced access to targeted therapies and imaging technologies facilitating improved patient outcomes.

U.K. Ollier’s Disease Market Insight

The U.K. Ollier’s disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of rare bone disorders and the demand for specialized care. Healthcare providers and patients increasingly focus on timely diagnosis, drug therapy adoption, and corrective surgical interventions. The country’s well-established healthcare system, coupled with robust research initiatives and clinical trial networks, is expected to continue stimulating market growth. Patient advocacy programs and access to orphan drugs further support the expanding adoption of both medication and surgery treatments.

Germany Ollier’s Disease Market Insight

The Germany Ollier’s disease market is expected to expand at a considerable CAGR during the forecast period, fueled by the presence of advanced healthcare infrastructure, high research funding, and increasing awareness of rare skeletal disorders. Patients benefit from early diagnosis, specialized surgical interventions, and access to targeted medications such as Denosumab. Germany’s emphasis on innovation in medical care and the integration of multidisciplinary approaches promote the adoption of comprehensive disease management. The availability of genetic testing and advanced imaging also contributes to improved patient outcomes and faster market growth.

Asia-Pacific Ollier’s Disease Market Insight

The Asia-Pacific Ollier’s disease market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare awareness, urbanization, and increasing investment in specialized hospitals and rare disease centers across countries such as China, Japan, and India. Growing adoption of pharmacological therapies, advanced imaging, and surgical interventions is enhancing patient outcomes. In addition, government initiatives supporting rare disease care, telemedicine, and online pharmacy access are expanding treatment availability. The region’s developing healthcare infrastructure and rising patient awareness are key factors propelling market growth.

Japan Ollier’s Disease Market Insight

The Japan Ollier’s disease market is gaining momentum due to the country’s high healthcare standards, advanced medical technology, and focus on rare disease management. The market growth is driven by increased diagnosis rates, the adoption of targeted medications, and specialized surgical care. Integration of genetic testing, advanced imaging, and multidisciplinary treatment approaches is improving patient outcomes. In addition, patient support programs and research initiatives targeting rare skeletal disorders are fueling demand. Japan’s aging population further emphasizes the need for accessible, effective, and non-invasive treatment options.

India Ollier’s Disease Market Insight

The India Ollier’s disease market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare access, growing awareness of rare bone disorders, and increasing availability of pharmacological therapies and surgical interventions. Hospitals, specialty clinics, and homecare services are increasingly offering integrated care for patients. Government initiatives promoting rare disease management, rising urbanization, and affordability of treatment options are key factors driving adoption. Growing patient advocacy, telemedicine platforms, and online pharmacy access further support market expansion across India.

What are the Recent Developments in Global Ollier’s Disease Market?

- In June 2025, A multicentric retrospective study published in SICOT-J demonstrated the therapeutic effect of intramedullary reaming and nailing for long bone lengthening in children with Ollier’s disease and Maffucci syndrome. The study highlighted that this technique not only corrected limb length discrepancy and axial deformities but also treated enchondromas by exerting a curettage-like effect during the reaming process. This approach offers a safer and more effective alternative to traditional methods, with fewer complications

- In August 2024, study published in Cancers identified the IDH1-R132H gene mutation as a common etiopathogenetic factor among Ollier’s disease, brain glioma, and acute myeloid leukemia. This finding suggests that IDH1 inhibitors could potentially serve as a therapeutic solution for patients affected by these conditions, highlighting the need for further clinical trials to confirm this hypothesis

- In May 2023, A study registered on ClinicalTrials.gov, sponsored by Dr. Luca Sangiorgi, detailed the establishment of the Registry of Ollier Disease and Maffucci Syndrome (ROM). This long-term observational cohort study, with a projected completion date in 2049, is designed to collect comprehensive clinical, genetic, and functional data from patients

- In July 2022, The American Association for Cancer Research (AACR) Childhood Cancer Predisposition Workshop provided updated consensus guidelines on cancer surveillance for patients with Ollier's disease and other rare syndromes. This is a significant development in patient care, as it provides a framework for proactive monitoring to improve early detection and intervention for potential malignant transformations, such as chondrosarcoma

- In November 2021, A systematic review published in the Journal of Orthopaedic Case Reports highlighted the connection between Ollier's disease, acute myeloid leukemia (AML), and gliomas, all of which can affect the same patient. The study confirmed that mutations in the IDH1 or IDH2 genes are a common factor in the pathogenesis of these diseases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.