Global On Board Vehicle Control Market

Market Size in USD Billion

USD

27.56 Billion

USD

130.88 Billion

2025

2033

USD

27.56 Billion

USD

130.88 Billion

2025

2033

| 2026 - 2033 | |

| USD 27.56 Billion | |

| USD 130.88 Billion | |

| % | |

|

On-board Vehicle Control Market Size

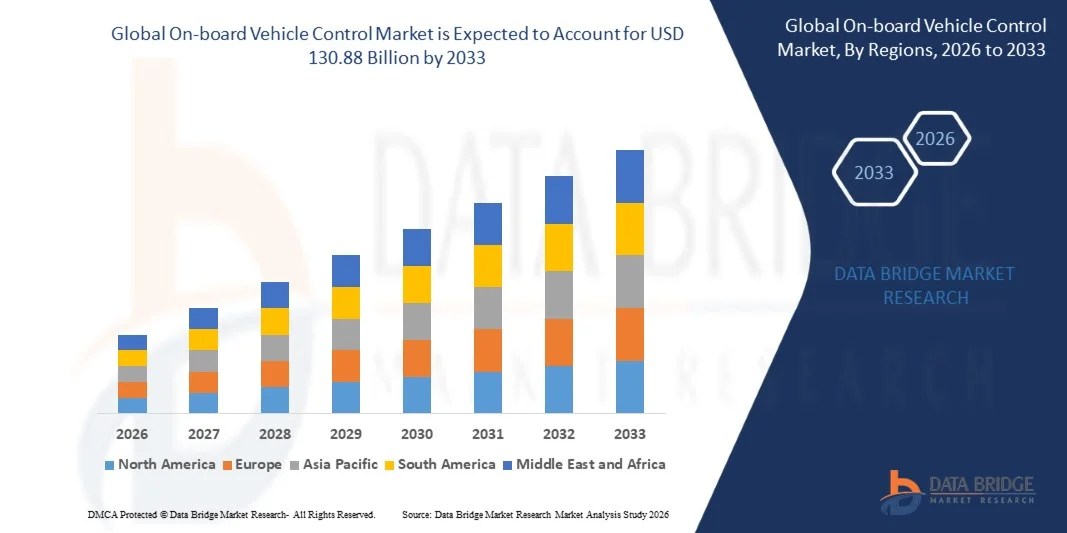

- The global on-board vehicle control market size was valued at USD 27.56 billion in 2025 and is expected to reach USD 130.88 billion by 2033, at a CAGR of 21.50% during the forecast period

- The market growth is largely fuelled by the increasing integration of advanced driver assistance systems, connected vehicle technologies, and electronic control units in modern vehicles

- Rising demand for vehicle automation, enhanced safety systems, and intelligent transportation technologies, combined with growing adoption of electric and autonomous vehicles, is further accelerating market expansion globally

On-board Vehicle Control Market Analysis

- The on-board vehicle control market is witnessing strong growth due to the increasing shift toward connected, autonomous, and software-defined vehicles across the global automotive industry

- Automotive manufacturers are increasingly investing in intelligent control systems, advanced telematics, and integrated vehicle management technologies to improve vehicle safety, operational efficiency, and driving performance

- North America dominated the on-board vehicle control market with the largest revenue share in 2025, driven by increasing adoption of connected vehicles, advanced driver assistance systems, and intelligent automotive technologies across passenger and commercial vehicle segments

- Asia-Pacific region is expected to witness the highest growth rate in the global on-board vehicle control market, driven by expanding automotive manufacturing activities, rising demand for electric and connected vehicles, and increasing investments in intelligent mobility infrastructure across emerging economies

- The BEV segment held the largest market revenue share in 2025 driven by the increasing adoption of fully electric vehicles and rising investments in vehicle electrification technologies. BEV-based on-board vehicle control systems often provide efficient power management, advanced battery monitoring, and seamless integration with intelligent mobility platforms, making them a preferred choice for modern electric vehicle architectures

Report Scope and On-board Vehicle Control Market Segmentation

|

Attributes |

On-board Vehicle Control Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Robert Bosch GmbH (Germany) |

|

Market Opportunities |

• Expansion Of Autonomous And Connected Vehicle Technologies |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis |

On-board Vehicle Control Market Trends

“Growing Integration of Connected And Autonomous Vehicle Technologies”

• The increasing focus on connected mobility, autonomous driving, and intelligent transportation systems is significantly shaping the on-board vehicle control market, as automotive manufacturers increasingly integrate advanced electronic control technologies into modern vehicles. On-board vehicle control systems are gaining traction due to their ability to improve vehicle safety, driving efficiency, real-time monitoring, and communication capabilities without compromising operational performance. This trend is strengthening their adoption across passenger and commercial vehicle segments, encouraging manufacturers to invest in advanced software-defined vehicle architectures and intelligent mobility platforms

• Rising awareness regarding vehicle safety, driver assistance technologies, and smart mobility solutions has accelerated the demand for on-board vehicle control systems across developed and emerging economies. Automotive manufacturers and consumers are actively prioritizing advanced control technologies that support autonomous driving, connected vehicle communication, and efficient vehicle management systems. This has also led to collaborations between automotive OEMs, semiconductor companies, and software developers to improve system integration, real-time analytics, and vehicle automation capabilities

• Connected mobility and intelligent transportation trends are influencing purchasing decisions, with manufacturers emphasizing advanced sensor integration, AI-enabled vehicle monitoring, and enhanced driver assistance functionalities. These factors are helping companies differentiate products in a competitive automotive market while also driving investments in advanced telematics, cloud-based vehicle management, and vehicle-to-everything communication technologies. Companies are increasingly using innovation-focused strategies and technology partnerships to strengthen brand positioning and improve consumer confidence in connected mobility solutions

• For instance, in 2024, Robert Bosch GmbH in Germany and Continental AG in Germany expanded their advanced on-board vehicle control solutions for connected and autonomous vehicle platforms. These developments were introduced in response to rising demand for intelligent vehicle management systems and real-time automotive data processing technologies across passenger and commercial vehicles. The companies also emphasized safety enhancement, vehicle automation, and AI-powered mobility solutions to strengthen competitiveness and accelerate technology adoption

• While demand for on-board vehicle control systems is growing, sustained market expansion depends on continuous advancements in semiconductor technologies, cybersecurity systems, and software integration capabilities. Manufacturers are also focusing on improving system scalability, real-time data processing efficiency, and supply chain reliability to support wider adoption across global automotive markets

On-board Vehicle Control Market Dynamics

Driver

“Increasing Adoption of Advanced Driver Assistance And Connected Vehicle Systems”

• Rising demand for advanced driver assistance systems, connected mobility technologies, and intelligent vehicle management solutions is a major driver for the on-board vehicle control market. Automotive manufacturers are increasingly integrating electronic control units, AI-enabled monitoring systems, and vehicle communication technologies to improve vehicle safety, operational efficiency, and driving performance. This trend is also encouraging research into autonomous driving systems, sensor fusion technologies, and software-defined vehicle architectures, supporting long-term market growth and innovation

• Expanding applications in passenger vehicles, commercial fleets, electric vehicles, and autonomous transportation systems are influencing market growth. On-board vehicle control systems help enhance vehicle communication, driver assistance, fuel efficiency, and operational monitoring while enabling real-time decision-making capabilities. The increasing adoption of connected and electric vehicles globally further reinforces this trend

• Automotive manufacturers and technology providers are actively promoting on-board vehicle control technologies through product innovation, strategic collaborations, and investments in connected mobility ecosystems. These efforts are supported by growing consumer preference for safer and smarter transportation solutions, while also encouraging partnerships between semiconductor manufacturers, automotive OEMs, and software developers to improve system reliability and vehicle intelligence

• For instance, in 2023, DENSO CORPORATION in Japan and ZF Friedrichshafen AG in Germany reported increased investments in AI-enabled vehicle control systems and advanced automotive electronics for connected vehicle applications. This expansion followed growing demand for intelligent mobility solutions, enhanced vehicle safety technologies, and autonomous driving capabilities, driving technological advancements and product differentiation. Both companies also emphasized innovation and software integration strategies to strengthen market competitiveness and support future mobility transformation

• Although rising adoption of connected and autonomous vehicle technologies supports market growth, wider commercialization depends on cost optimization, cybersecurity enhancement, and scalable semiconductor manufacturing capabilities. Investment in AI technologies, automotive software platforms, and intelligent communication systems will be critical for meeting future mobility demand and maintaining competitive advantage

Restraint/Challenge

“High System Complexity And Cybersecurity Concerns”

• The increasing complexity of on-board vehicle control systems compared to conventional automotive electronics remains a key challenge, limiting seamless integration and increasing overall vehicle development costs. Advanced software architectures, semiconductor requirements, and sophisticated electronic control systems contribute to elevated production and maintenance expenses. In addition, rapid technological evolution and compatibility requirements can further affect system reliability and deployment timelines

• Consumer and manufacturer concerns regarding cybersecurity and data privacy remain significant, particularly as connected vehicles become more dependent on cloud-based communication and real-time data exchange technologies. Limited standardization and increasing risks of cyberattacks restrict adoption across certain automotive applications and connected mobility platforms. This also leads to slower implementation in markets where cybersecurity regulations and digital infrastructure are still developing

• Supply chain and semiconductor-related challenges also impact market growth, as on-board vehicle control systems require advanced chips, sensors, and electronic components for efficient operation. Rising semiconductor shortages, component sourcing complexities, and software integration challenges increase operational costs and production delays for manufacturers. Companies must invest in localized semiconductor production, cybersecurity frameworks, and robust software validation systems to maintain operational efficiency and product reliability

• For instance, in 2024, automotive manufacturers and technology suppliers in Europe and Asia reported delays in connected vehicle production due to semiconductor shortages and increasing cybersecurity compliance requirements for advanced vehicle control systems. Rising costs associated with automotive-grade chips and secure software integration were additional barriers affecting market expansion. These factors also prompted some manufacturers to delay product launches and technology deployment timelines across connected mobility projects

• Overcoming these challenges will require cost-efficient semiconductor production, stronger cybersecurity frameworks, and improved automotive software standardization. Collaboration among automotive OEMs, semiconductor manufacturers, software developers, and regulatory authorities can help unlock the long-term growth potential of the global on-board vehicle control market. Furthermore, enhancing data security, improving system interoperability, and strengthening intelligent mobility infrastructure will be essential for widespread market adoption

On-board Vehicle Control Market Scope

The market is segmented on the basis of propulsion type, capacity type, voltage type, offering type, communication technology, and function.

• By Propulsion Type

On the basis of propulsion type, the on-board vehicle control market is segmented into BEV, HEV, and PHEV. The BEV segment held the largest market revenue share in 2025 driven by the increasing adoption of fully electric vehicles and rising investments in vehicle electrification technologies. BEV-based on-board vehicle control systems often provide efficient power management, advanced battery monitoring, and seamless integration with intelligent mobility platforms, making them a preferred choice for modern electric vehicle architectures.

The PHEV segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for fuel-efficient mobility solutions and the growing transition toward electrified transportation systems. PHEV-based control systems are particularly popular for their ability to optimize both electric and internal combustion power sources, often improving driving efficiency and operational flexibility.

• By Capacity Type

On the basis of capacity type, the on-board vehicle control market is segmented into 16-Bit, 32-Bit, and 64-Bit. The 32-Bit segment held the largest market revenue share in 2025 driven by its balanced processing capability, cost efficiency, and widespread integration across automotive electronic control units. 32-Bit control systems often provide enhanced computational performance, efficient data processing, and compatibility with advanced vehicle functions, making them highly suitable for connected and intelligent vehicles.

The 64-Bit segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for high-performance computing and advanced software-defined vehicle architectures. 64-Bit systems are particularly popular for supporting autonomous driving technologies, artificial intelligence applications, and real-time data analytics, often enabling improved vehicle intelligence and system scalability.

• By Voltage Type

On the basis of voltage type, the on-board vehicle control market is segmented into 12/24V and 36/48V. The 12/24V segment held the largest market revenue share in 2025 driven by its extensive use in conventional passenger and commercial vehicles and compatibility with existing automotive electrical systems. 12/24V systems often offer reliable power distribution and cost-effective integration across a wide range of automotive electronic components and vehicle control applications.

The 36/48V segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of electrified powertrain technologies and growing demand for energy-efficient vehicle architectures. 36/48V systems are particularly popular for supporting advanced driver assistance systems, electric turbochargers, and hybrid vehicle technologies, often improving overall vehicle efficiency and power management capabilities.

• By Offering Type

On the basis of offering type, the on-board vehicle control market is segmented into hardware and software. The hardware segment held the largest market revenue share in 2025 driven by the increasing deployment of electronic control units, sensors, processors, and communication modules across connected and autonomous vehicles. Hardware-based solutions often provide reliable system performance, real-time processing capabilities, and integration with advanced automotive electronics, making them essential for vehicle control operations.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for software-defined vehicles and AI-enabled automotive platforms. Software solutions are particularly popular for supporting over-the-air updates, predictive diagnostics, and autonomous driving functionalities, often enabling improved vehicle intelligence and operational efficiency.

• By Communication Technology

On the basis of communication technology, the on-board vehicle control market is segmented into CAN (Controller Area Network), LIN (Local Interconnect Network), FlexRay, and Ethernet. The CAN (Controller Area Network) segment held the largest market revenue share in 2025 driven by its widespread adoption in automotive electronic control systems and its ability to provide reliable real-time communication between vehicle components. CAN-based systems often offer improved fault tolerance, cost efficiency, and seamless integration with multiple electronic control units, making them a preferred communication protocol for modern passenger and commercial vehicles.

The Ethernet segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for high-speed data transmission and advanced connectivity solutions in connected and autonomous vehicles. Ethernet-enabled vehicle control systems are particularly popular for supporting advanced driver assistance systems, real-time data processing, and over-the-air software updates, often serving as a critical communication backbone for next-generation intelligent mobility platforms.

• By Function

On the basis of function, the on-board vehicle control market is segmented into autonomous driving/ADAS and predictive technology. The autonomous driving/ADAS segment held the largest market revenue share in 2025 driven by increasing consumer demand for enhanced vehicle safety, driver assistance features, and connected mobility technologies. ADAS-based control systems often provide lane-keeping assistance, adaptive cruise control, collision avoidance, and automated parking functionalities, making them highly valuable across passenger and commercial vehicle applications.

The predictive technology segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of artificial intelligence, machine learning, and predictive maintenance solutions in modern vehicles. Predictive technologies are particularly popular for enabling real-time vehicle diagnostics, intelligent performance monitoring, and proactive maintenance scheduling, often improving operational efficiency and reducing vehicle downtime.

On-board Vehicle Control Market Regional Analysis

• North America dominated the on-board vehicle control market with the largest revenue share in 2025, driven by increasing adoption of connected vehicles, advanced driver assistance systems, and intelligent automotive technologies across passenger and commercial vehicle segments

• Consumers and automotive manufacturers in the region highly value the enhanced safety, real-time monitoring, and operational efficiency offered by on-board vehicle control systems integrated with connected mobility platforms and autonomous driving technologies

• This widespread adoption is further supported by strong investments in automotive electronics, a technologically advanced transportation ecosystem, and growing demand for software-defined and autonomous vehicles, establishing on-board vehicle control systems as critical components in modern automotive infrastructure

U.S. On-board Vehicle Control Market Insight

The U.S. on-board vehicle control market captured the largest revenue share in 2025 within North America, fueled by the rapid adoption of connected mobility solutions and the increasing integration of advanced automotive electronics. Automotive manufacturers are increasingly prioritizing intelligent vehicle management systems, autonomous driving technologies, and AI-enabled driver assistance features to enhance safety and driving efficiency. The growing preference for connected vehicles, combined with strong investments in electric and autonomous vehicle development, further propels the on-board vehicle control market. Moreover, the increasing deployment of cloud-based vehicle communication systems and over-the-air software update technologies is significantly contributing to market expansion.

Europe On-board Vehicle Control Market Insight

The Europe on-board vehicle control market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent automotive safety regulations and rising demand for connected and autonomous mobility solutions. The increasing focus on reducing road accidents, improving vehicle efficiency, and advancing intelligent transportation systems is fostering the adoption of on-board vehicle control technologies across the region. European consumers and automotive manufacturers are also attracted to the operational efficiency and safety benefits offered by advanced automotive control systems. The region is experiencing significant growth across passenger vehicles, commercial fleets, and electric mobility applications, with intelligent vehicle technologies increasingly integrated into both new vehicle production and mobility infrastructure projects.

U.K. On-board Vehicle Control Market Insight

The U.K. on-board vehicle control market is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing transition toward connected and autonomous transportation technologies and rising investments in smart mobility infrastructure. In addition, growing demand for advanced vehicle safety systems and intelligent driving technologies is encouraging automotive manufacturers and fleet operators to adopt sophisticated on-board vehicle control solutions. The U.K.’s strong automotive innovation ecosystem, alongside its increasing focus on autonomous vehicle testing and connected mobility platforms, is expected to continue stimulating market growth.

Germany On-board Vehicle Control Market Insight

The Germany on-board vehicle control market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for advanced automotive electronics and the country’s strong emphasis on engineering innovation and vehicle automation technologies. Germany’s well-established automotive manufacturing ecosystem, combined with its leadership in connected and autonomous vehicle development, promotes the adoption of on-board vehicle control systems across passenger and commercial vehicles. The integration of AI-enabled vehicle management systems, advanced sensors, and real-time communication technologies is also becoming increasingly prevalent, aligning with consumer and industry demand for safer and more intelligent mobility solutions.

Asia-Pacific On-board Vehicle Control Market Insight

The Asia-Pacific on-board vehicle control market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, increasing automotive production, and growing investments in connected vehicle technologies across countries such as China, Japan, and India. The region’s increasing adoption of electric vehicles, intelligent transportation systems, and autonomous driving technologies is driving the deployment of advanced on-board vehicle control systems. Furthermore, as APAC emerges as a major automotive electronics manufacturing hub, the affordability and accessibility of intelligent vehicle technologies are expanding to a wider consumer base.

Japan On-board Vehicle Control Market Insight

The Japan on-board vehicle control market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s strong technological capabilities, increasing adoption of autonomous mobility technologies, and focus on advanced automotive innovation. The Japanese market places significant emphasis on intelligent transportation systems and vehicle safety, and the adoption of on-board vehicle control systems is driven by growing demand for connected vehicles and AI-powered automotive technologies. The integration of advanced driver assistance systems, real-time vehicle monitoring, and autonomous driving functionalities is fueling growth. Moreover, Japan’s strong presence of automotive and semiconductor manufacturers is further supporting market expansion.

China On-board Vehicle Control Market Insight

The China on-board vehicle control market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive industry, rapid adoption of connected vehicle technologies, and increasing investments in intelligent transportation infrastructure. China stands as one of the largest automotive and electric vehicle markets globally, and on-board vehicle control systems are becoming increasingly popular across passenger, commercial, and autonomous vehicle applications. The push toward smart mobility ecosystems, strong government support for autonomous driving technologies, and the presence of major automotive electronics manufacturers are key factors propelling the market in China.

On-board Vehicle Control Market Share

The On-board Vehicle Control industry is primarily led by well-established companies, including:

• Robert Bosch GmbH (Germany)

• Continental AG (Germany)

• Texas Instruments Incorporated (U.S.)

• STMicroelectronics (Switzerland)

• PI Innovo (U.S.)

• Embitel (India)

• PUES Corporation (U.S.)

• Aim Technologies (U.K.)

• Ecotron LLC (U.S.)

• Thunderstruck Motors (U.S.)

• HiRain Technologies Co., Ltd (China)

• Mitsubishi Electric Corporation (Japan)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.