Global Oncology Mobile Health Applications Market

Market Size in USD Billion

USD

3.20 Billion

USD

14.80 Billion

2025

2033

USD

3.20 Billion

USD

14.80 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.20 Billion | |

| USD 14.80 Billion | |

| % | |

|

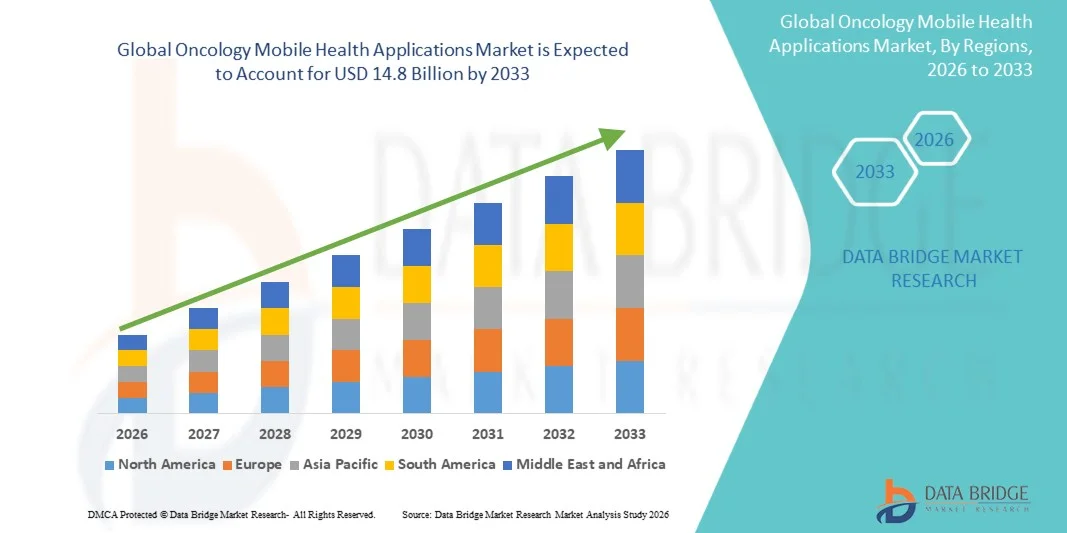

Oncology Mobile Health Applications Market Size

- The global Oncology Mobile Health Applications market size was valued at USD 3.2 billion in 2025 and is expected to reach USD 14.8 billion by 2033, at a CAGR of 2% during the forecast period.

- Market growth is primarily driven by rising global cancer incidence, accelerating adoption of smartphones and wearable health technologies, expanding telehealth ecosystems, and increasing demand for remote patient monitoring solutions that support oncology care outside traditional clinical settings.

- Additionally, growing investments in AI-powered oncology apps, supportive regulatory frameworks for digital therapeutics, increasing focus on medication adherence and post-treatment monitoring, and rising patient engagement with mobile health platforms are supporting strong global market expansion.

Oncology Mobile Health Applications Market Analysis

- Oncology mobile health applications, widely used for symptom tracking, medication reminders, teleconsultation, cancer screening support, and clinical trial management, enable patients, caregivers, and oncologists to achieve better care coordination, improve treatment adherence, and support continuous real-time health monitoring beyond clinical environments.

- The growing demand for oncology mHealth apps is driven by increasing global cancer burden, rising adoption of digital health technologies, expanding telehealth infrastructure, growing need for remote patient management during chemotherapy and post-treatment recovery, and increasing integration of AI and machine learning for personalized oncology care delivery.

- North America dominated the Oncology Mobile Health Applications market with a share of 37.70% in 2025, supported by strong digital health infrastructure, high smartphone penetration, favorable regulatory environment for health apps, and significant presence of major oncology digital health companies, particularly in the United States.

- Asia-Pacific is expected to be the fastest-growing with a cagr of 15.20% region, driven by rapid digital infrastructure expansion across China, India, Japan, and South Korea, surging cancer incidence rates, rising smartphone adoption, growing telemedicine acceptance, and increasing government investments in digital health ecosystems.

- The Patient Monitoring & Symptom Tracking segment dominated with a share of 34.00% the market due to its critical role in real-time cancer symptom management, chemotherapy side effect tracking, and post-treatment recovery monitoring, supported by strong demand for continuous remote care in oncology.

Report Scope and Oncology Mobile Health Applications Market Segmentation

|

Attributes |

Oncology Mobile Health Applications Key Market Insights |

|

Segments Covered |

By Application Type: Patient Monitoring & Symptom Tracking, Medication Adherence & Reminder Apps, Teleconsultation & Virtual Oncology Care, Cancer Screening & Diagnostics, Clinical Trial Recruitment & Management By Cancer Type: Breast Cancer, Lung Cancer, Colorectal Cancer, Blood Cancer (Leukemia & Lymphoma), Prostate Cancer, Others By Platform: iOS, Android, Cross-Platform By End User: Patients & Caregivers, Oncologists & Healthcare Providers, Research Institutions & Clinical Trial Organizations |

|

Countries Covered |

North America: · U.S. · Canada · Mexico Europe: · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific: · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa: · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America: · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Flatiron Health (U.S.) · CancerSEEK / Exact Sciences Corporation (U.S.) · OncoPower (U.S.) · Belong.Life (Israel) · Navigating Cancer (U.S.) · Allscripts Healthcare Solutions (U.S.) · Pfizer Inc. (U.S.) · AstraZeneca PLC (U.K.) · F. Hoffmann-La Roche Ltd. (Switzerland) · Novartis AG (Switzerland) · Medidata Solutions (U.S.) · Caris Life Sciences (U.S.) |

|

Market Opportunities |

· Rising integration of AI and machine learning into oncology apps is enabling real-time symptom analysis and personalized treatment recommendations. · Expanding digital health infrastructure in emerging markets is creating significant untapped growth opportunities. · Growing focus on remote patient monitoring during and post-chemotherapy is driving adoption of specialized oncology mobile applications. |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Oncology Mobile Health Applications Market Trends

"Rising integration of artificial intelligence in oncology apps is transforming personalized cancer care and remote patient engagement"

- Rising integration of artificial intelligence and machine learning into oncology mobile health applications is creating significant opportunities by enabling real-time symptom analysis, predictive health insights, and personalized treatment adherence support for cancer patients.

- AI-powered apps are enabling oncologists to remotely monitor patient health metrics, predict adverse events from chemotherapy, and optimize treatment protocols based on real-time data collected through mobile platforms.

- Increasing deployment of natural language processing (NLP) in oncology chatbots and virtual health assistants is improving patient-provider communication, facilitating symptom reporting, and supporting remote triage for cancer-related complications.

- Growing adoption of wearable device integration with oncology apps is enabling continuous collection of vital signs, activity data, and biosignals that support oncology care teams in proactive patient management.

- Advancements in predictive analytics within oncology platforms are enhancing clinical decision support, enabling early detection of deteriorating patient conditions and reducing unplanned hospitalizations during cancer treatment.

- Rising focus on patient-reported outcome (PRO) collection via mobile platforms is accelerating adoption among oncology clinical trial organizations seeking real-world evidence and real-time patient data.

- Expansion of regulatory frameworks including FDA's Digital Health Center of Excellence and CE-marking pathways for digital health tools in Europe is reducing market entry barriers and encouraging innovation in oncology mobile health applications.

- Overall, AI-driven innovation in oncology mHealth is transforming the market toward a more proactive, data-centric, and patient-empowered cancer care delivery model.

Oncology Mobile Health Applications Market Dynamics

Driver

"Rising global cancer incidence combined with expanding smartphone penetration is accelerating oncology mHealth adoption"

- Rising global cancer burden is a primary driver of the oncology mobile health applications market, as increasing patient populations require continuous remote monitoring, adherence support, and digital engagement beyond traditional hospital visits.

- According to the International Agency for Research on Cancer (IARC), over 20 million new cancer cases were recorded globally in 2022, with projections indicating a rise to 35 million annually by 2050, significantly expanding the target patient base for oncology mHealth solutions.

- Increasing global smartphone penetration, with over 7.3 billion users projected by 2025, is creating an unprecedented infrastructure base for scalable deployment of oncology mobile health applications across diverse geographies.

- Growing preference among cancer patients for remote monitoring and teleconsultation services is reducing reliance on in-person visits and driving adoption of specialized oncology apps for symptom management, medication tracking, and treatment guidance.

- Expansion of 5G network infrastructure is enabling real-time, high-quality video consultations, wearable data integration, and AI-powered health analytics within mobile oncology platforms, significantly improving user experience and clinical utility.

- Increasing investments from pharmaceutical companies in digital companion apps that support oncology drug therapies are creating new revenue streams and accelerating commercial adoption of oncology mHealth solutions globally.

- Growing awareness among oncology patients and caregivers regarding the clinical benefits of mobile health tools for improving treatment outcomes and quality of life is further accelerating market-wide adoption.

Restraint/Challenge

"Data privacy concerns and complex regulatory compliance requirements are creating significant barriers for oncology mHealth adoption"

- Stringent data privacy regulations including HIPAA in the United States, GDPR in Europe, and equivalent frameworks across Asia-Pacific are creating complex compliance burdens for developers and deployers of oncology mobile health applications, increasing development costs and time-to-market.

- Sensitive nature of cancer patient data, including treatment histories, genetic information, and behavioral health records, makes oncology mHealth platforms high-priority targets for cybersecurity threats, requiring significant investment in data security infrastructure.

- Limited digital literacy among older cancer patient populations, who constitute a substantial proportion of the oncology patient base, restricts widespread adoption and increases need for human-assisted onboarding support.

- Fragmented regulatory landscapes across different countries for digital health applications create challenges in achieving multi-market deployment at scale, particularly for startups and mid-sized oncology digital health companies.

- Concerns about clinical validation and evidence-based efficacy of oncology apps among oncologists and healthcare providers remain a significant adoption barrier, as many mobile health tools lack robust clinical trial evidence supporting their therapeutic value.

- Reimbursement challenges for digital health services in many healthcare systems further constrain monetization opportunities and long-term commercial sustainability for oncology mHealth application developers.

- These combined factors create a complex operating environment requiring developers to balance innovation speed with rigorous clinical validation, data security, and regulatory compliance requirements.

Oncology Mobile Health Applications Market Scope

The market is segmented on the basis of application type, cancer type, platform, and end user.

By Application Type

On the basis of Application Type, the global Oncology Mobile Health Applications market is segmented into Patient Monitoring & Symptom Tracking, Medication Adherence & Reminder Apps, Teleconsultation & Virtual Oncology Care, Cancer Screening & Diagnostics, and Clinical Trial Recruitment & Management. The Patient Monitoring & Symptom Tracking segment dominated the market with the largest revenue share of 34.00% in 2025, driven by its critical role in managing chemotherapy side effects, monitoring post-treatment recovery, and enabling real-time communication between patients and oncology care teams. The widespread adoption of wearable devices and continuous remote health monitoring during active cancer treatment further supports segment dominance.

The Clinical Trial Recruitment & Management segment is expected to witness the fastest growth of 18.10% during the forecast period, fueled by the lasting shift toward telemedicine accelerated by the COVID-19 pandemic, increasing patient preference for remote oncology consultations, and growing investments in telehealth infrastructure by cancer centers and hospital networks globally.

By Cancer Type

On the basis of Cancer Type, the global Oncology Mobile Health Applications market is segmented into Breast Cancer, Lung Cancer, Colorectal Cancer, Blood Cancer (Leukemia & Lymphoma), Prostate Cancer, and Others. The Breast Cancer segment dominated the market with a share of 32.40% in 2025, as it represents one of the most prevalent cancer types globally and benefits from strong patient community engagement, high smartphone adoption among affected demographics, and the availability of numerous dedicated breast cancer mobile health platforms supporting treatment adherence and survivorship care.

The Blood Cancer segment is expected to witness the fastest growth with a cagr of 16.80% during the forecast period, driven by its position as the leading cause of cancer-related mortality globally, rising investments in early detection mobile solutions, and increasing development of AI-powered symptom tracking and diagnostic support applications for respiratory oncology.

By Platform

On the basis of Platform, the global Oncology Mobile Health Applications market is segmented into iOS, Android, and Cross-Platform. The Android segment dominated the market with a share of 41.50% in 2025, supported by its significantly higher global smartphone market share, particularly across Asia-Pacific, Latin America, and Africa, making Android-based oncology apps critical for reaching the largest possible patient population across diverse income levels and geographies.

The cross-platform segment is expected to witness the fastest growth of 15.20% during the forecast period, fueled by increasing developer preference for cross-platform frameworks that reduce development costs, enable simultaneous deployment across iOS and Android ecosystems, and support broader patient reach for oncology digital health solutions.

By End User

On the basis of End User, the global Oncology Mobile Health Applications market is segmented into Patients & Caregivers, Oncologists & Healthcare Providers, and Research Institutions & Clinical Trial Organizations. The Patients & Caregivers segment dominated the market with a share of 62.90% in 2025, as this group represents the largest and most direct user base for oncology mobile health applications, driven by increasing health awareness, demand for self-management tools, and growing reliance on digital platforms for treatment adherence, symptom tracking, and remote communication with oncology care teams.

The Research Institutions & Clinical Trial Organizations segment is expected to witness the fastest growth of 16.80% during the forecast period, fueled by the rapidly growing use of oncology mHealth applications for patient recruitment, electronic consent management, remote clinical trial participation, and real-world evidence collection, significantly reducing trial timelines and expanding geographic access for oncology research.

Oncology Mobile Health Applications Market Regional Analysis

- North America dominated the Oncology Mobile Health Applications market with the largest revenue share in 2025, supported by high cancer incidence rates, strong digital health infrastructure, robust telehealth adoption, and a favorable regulatory environment that accelerates innovation and commercialization of oncology digital health solutions. The presence of major digital health companies such as Flatiron Health, Navigating Cancer, and OncoPower further reinforces the region's leadership in the global oncology mHealth market.

- Industries and healthcare providers across the region place strong emphasis on patient-centered care, remote monitoring, and AI-driven personalized treatment support, driving widespread adoption of oncology mobile health platforms for symptom tracking, medication management, teleconsultation, and clinical trial support across major cancer centers and community oncology networks.

- This strong market position is further supported by high healthcare expenditure, increasing investment from pharmaceutical companies in digital companion therapeutics, expansion of value-based care models that reward remote patient engagement, and continuous development of oncology-specific AI and data analytics capabilities within mobile health platforms.

U.S. Oncology Mobile Health Applications Market Insight

The U.S. Oncology Mobile Health Applications market holds a dominant global position, driven by the highest cancer incidence among major economies, widespread smartphone adoption, mature telehealth infrastructure, and strong regulatory support from FDA's Digital Health Center of Excellence. Increasing integration of oncology apps with electronic health record (EHR) systems, growing use of AI-powered symptom tracking during chemotherapy, and expanding pharmaceutical investment in digital therapeutic companions are significantly supporting market growth. Additionally, rising adoption of remote clinical trial platforms and increasing demand for survivorship care applications are further strengthening market expansion.

Europe Oncology Mobile Health Applications Market Insight

The Europe Oncology Mobile Health Applications market is witnessing steady growth, driven by strong demand from healthcare providers and oncology centers across Germany, the United Kingdom, France, and the Netherlands, where digital health adoption is accelerating rapidly. Supportive policy frameworks including the EU's European Health Data Space initiative, increasing reimbursement pathways for digital therapeutics, and growing investments in AI-powered oncology tools are supporting market expansion. Additionally, the region's focus on patient privacy, data protection under GDPR, and high standards of clinical evidence for digital health tools is encouraging the development of robust, clinically validated oncology mobile health platforms.

U.K. Oncology Mobile Health Applications Market Insight

The U.K. Oncology Mobile Health Applications market is experiencing steady growth, driven by the National Health Service's (NHS) active investment in digital health transformation and expanding telehealth programs within oncology care. Rising demand for remote monitoring apps for cancer patients undergoing chemotherapy and radiotherapy, increasing smartphone penetration among oncology patient populations, and growing focus on digital survivorship care are supporting market development. Additionally, government-backed initiatives such as the NHS App and digital oncology pilot programs are accelerating adoption of mobile health solutions across cancer care pathways in the country.

Germany Oncology Mobile Health Applications Market Insight

The Germany Oncology Mobile Health Applications market is expected to grow steadily during the forecast period, driven by Germany's Digital Health Applications (DiGA) regulatory framework — one of Europe's most advanced digital health approval pathways — which is enabling faster market access for clinically validated oncology mobile health tools. Strong demand from oncology centers and comprehensive cancer care networks, increasing investment in digital health startups, and growing adoption of remote patient monitoring solutions during cancer treatment are further supporting growth. Germany's advanced healthcare system, high digital literacy, and emphasis on evidence-based digital therapeutics are contributing to sustained market expansion.

Japan Oncology Mobile Health Applications Market Insight

The Japan Oncology Mobile Health Applications market is witnessing steady growth, driven by the country's rapidly aging population, high cancer prevalence, and increasing government focus on digital health transformation within the healthcare system. Strong technological innovation culture, high smartphone penetration, and growing adoption of remote monitoring and AI-powered health tools are supporting market expansion. Additionally, Japan's Ministry of Health, Labour and Welfare's active push for digital health adoption and increasing use of oncology apps in cancer screening, treatment adherence, and survivorship care are further driving demand growth.

India Oncology Mobile Health Applications Market Insight

The India Oncology Mobile Health Applications market is experiencing strong growth, driven by rapidly rising cancer incidence, surging smartphone adoption across urban and semi-urban populations, and expanding digital health infrastructure supported by government initiatives such as the National Digital Health Mission (Ayushman Bharat Digital Mission). Growing awareness of cancer screening and treatment options, expanding telehealth platforms, and increasing investments from domestic and international digital health companies in oncology-specific mobile solutions are significantly boosting market growth. Rising demand for affordable, mobile-first healthcare solutions that bridge the gap between patients and oncologists in tier-2 and tier-3 cities is further strengthening market expansion across the country.

Oncology Mobile Health Applications Market Share

The Oncology Mobile Health Applications industry is primarily led by well-established companies, including:

- Flatiron Health (U.S.)

- OncoPower (U.S.)

- Life (Israel)

- Navigating Cancer (U.S.)

- Allscripts Healthcare Solutions (U.S.)

- Pfizer Inc. (U.S.)

- AstraZeneca PLC (U.K.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Novartis AG (Switzerland)

- Medidata Solutions / Dassault Systemes (U.S.)

- Caris Life Sciences (U.S.)

- Exact Sciences Corporation (U.S.)

Latest Developments in Global Oncology Mobile Health Applications Market

- In April 2026, AstraZeneca partnered with a leading digital health platform to launch an integrated oncology patient monitoring application enabling real-time symptom tracking and medication adherence support for patients undergoing targeted therapy regimens across the U.S. and Europe, aimed at improving treatment compliance and early identification of adverse events.

- In January 2026, Roche introduced an enhanced version of its AI-powered oncology insights mobile platform, integrating predictive analytics for personalized chemotherapy side effect management and providing oncologists with actionable real-time patient health data to support proactive treatment adjustments.

- In November 2025, Flatiron Health expanded its oncology data and analytics capabilities through a new mobile-first patient engagement module, enabling cancer patients to report symptoms, track treatment milestones, and communicate directly with care teams through a secure HIPAA-compliant application integrated with electronic health records.

- In September 2025, Belong.Life, a leading oncology social health platform, launched an AI-powered cancer care companion application incorporating personalized treatment insights, clinical trial matching, and community support features, reaching over 3 million cancer patients globally across iOS and Android platforms.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.