Global Oncolytic Virus Immunotherapy Market

Market Size in USD Billion

USD

3.71 Billion

USD

9.18 Billion

2025

2033

USD

3.71 Billion

USD

9.18 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.71 Billion | |

| USD 9.18 Billion | |

| % | |

|

Oncolytic Virus Immunotherapy Market Size

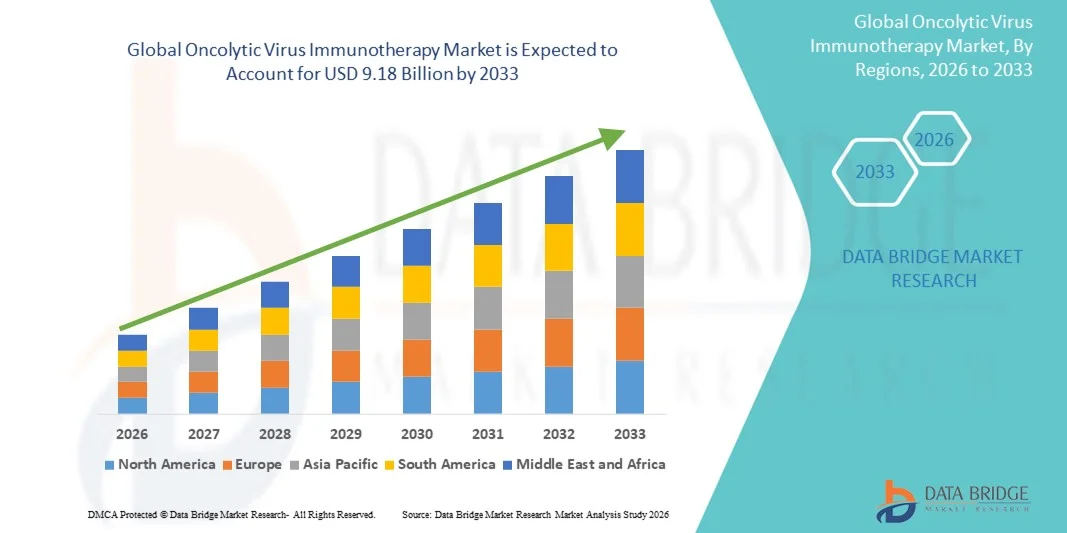

- The global oncolytic virus immunotherapy market size was valued at USD 3.71 billion in 2025 and is expected to reach USD 9.18 billion by 2033, at a CAGR of12.00% during the forecast period

- The market growth is largely fueled by increasing research and development in cancer immunotherapies, rising prevalence of various cancers, and growing adoption of advanced biologic treatments across hospitals and specialty clinics worldwide

- Furthermore, the expanding awareness among healthcare professionals and patients regarding the benefits of targeted therapies, coupled with government support for innovative cancer treatments, is accelerating the uptake of Oncolytic Virus Immunotherapy solutions, thereby significantly boosting the industry's growth

Oncolytic Virus Immunotherapy Market Analysis

- Oncolytic Virus Immunotherapy, leveraging genetically modified viruses to selectively infect and destroy cancer cells while stimulating the immune system, is becoming an increasingly vital component of modern oncology treatments due to its targeted efficacy, potential to enhance existing immunotherapies, and growing clinical adoption in hospitals and specialty cancer centers

- The escalating demand for oncolytic virus immunotherapy is primarily fueled by rising global cancer incidence, increased investments in cancer research, growing awareness among healthcare professionals and patients, and the advancement of clinical trials demonstrating its therapeutic benefits

- North America dominated the oncolytic virus immunotherapy market with the largest revenue share of 39.2% in 2025, supported by advanced healthcare infrastructure, strong R&D activities, high adoption of innovative cancer therapies, and the presence of leading biotechnology and pharmaceutical companies focusing on oncolytic virus treatments, with the U.S. contributing the majority share due to early access to novel therapies and robust clinical trial networks

- Asia-Pacific is expected to be the fastest-growing region in the oncolytic virus immunotherapy market during the forecast period, projected to expand at a CAGR of 11.8% from 2026 to 2033, driven by improving healthcare access, increasing government and private investments in oncology research, rising cancer prevalence, and growing adoption of advanced cancer treatment solutions in countries such as China, India, and Japan

- The Intratumoral segment dominated with a revenue share of 46.2% in 2025, as it allows high local virus concentration, enhanced tumor lysis, and reduced systemic toxicity

Report Scope and Oncolytic Virus Immunotherapy Market Segmentation

|

Attributes |

Oncolytic Virus Immunotherapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Bristol-Myers Squibb (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Oncolytic Virus Immunotherapy Market Trends

Emerging Focus on Targeted and Combination Therapies

- A significant and accelerating trend in the global oncolytic virus immunotherapy market is the shift toward combination therapies and precision-targeted oncolytic viruses. Researchers and pharmaceutical companies are increasingly developing therapies that selectively target tumor cells while minimizing impact on healthy tissues, thereby enhancing treatment efficacy

- There is growing interest in combining oncolytic virus therapy with immunotherapies such as checkpoint inhibitors, which has shown promise in preclinical and clinical studies for improving overall survival rates in certain cancers

- Biopharmaceutical companies are also exploring novel viral vectors engineered to enhance tumor selectivity, stimulate anti-tumor immunity, and overcome the tumor microenvironment’s immunosuppressive nature

- This trend is further driven by advancements in genetic engineering, allowing customization of viruses for specific cancer types, improving therapeutic outcomes and reducing side effects

- For instance, in March 2024, a Phase II clinical study by Amgen demonstrated that combining talimogene laherparepvec (T-VEC) with a PD-1 inhibitor significantly improved response rates in melanoma patients, reinforcing the potential of combination strategies

- The trend reflects a broader focus on precision oncology and immunotherapy integration, aligning with increasing regulatory approvals for targeted therapies and enhanced patient-centric care strategies

- Market participants are expected to continue investing in R&D to expand indications and optimize delivery mechanisms, ensuring therapies are both effective and safer for diverse patient populations

Oncolytic Virus Immunotherapy Market Dynamics

Driver

Rising Prevalence of Cancer and Growing Investment in Immunotherapy

- The rising global incidence of cancer is a primary driver for oncolytic virus therapy adoption, as conventional treatments often fail to address refractory or metastatic tumors. Increasing prevalence of melanoma, lung, colorectal, and head & neck cancers has generated strong demand for innovative therapeutic options

- Governments, private investors, and pharmaceutical companies are significantly investing in immunotherapy development, further accelerating market growth

- Supportive reimbursement policies and clinical trial funding in key regions, including North America and Europe, are also encouraging adoption of novel oncolytic virus therapies

- For instance, in August 2023, Pfizer announced an investment exceeding USD 200 million in immuno-oncology research, including oncolytic virus therapy programs, to expand clinical development pipelines for multiple tumor types

- Improved patient awareness about immunotherapy options and favorable clinical outcomes contribute to rising acceptance among oncologists and healthcare providers

- The combination of high unmet clinical needs, expanding pipeline therapies, and growing capital inflows is expected to sustain strong market growth over the forecast period

Restraint/Challenge

High Cost of Therapy and Complex Regulatory Approvals

- High treatment costs and the complex, time-consuming regulatory pathways pose significant barriers to market expansion. Oncolytic virus therapies often involve individualized manufacturing, sophisticated storage requirements, and specialized administration protocols, all of which contribute to elevated expenses

- Reimbursement limitations in certain regions can delay adoption, especially in emerging markets with constrained healthcare budgets

- For instance, in February 2022, a hospital in the United States reported delays in offering T-VEC therapy due to coverage restrictions and budget constraints, illustrating how cost remains a practical barrier

In addition, regulatory approval timelines for genetically engineered viral therapies are longer than conventional drugs due to safety monitoring, biosafety compliance, and clinical trial complexities

- For instance, in February 2022, a hospital in the United States reported delays in offering T-VEC therapy due to coverage restrictions and budget constraints, illustrating how cost remains a practical barrier

- Manufacturers need to address scalability challenges and streamline production processes to make therapies more affordable and widely accessible

- Overcoming these restraints through government support, patient assistance programs, and innovative delivery solutions is crucial for achieving sustained market growth in the coming years

Oncolytic Virus Immunotherapy Market Scope

The market is segmented on the basis of type, application, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Oncolytic Virus Immunotherapy market is segmented into Vaccinia Virus, Herpes Simplex Virus, Reovirus, Adenovirus, and Others. The Herpes Simplex Virus (HSV) segment dominated the market with a revenue share of 41.8% in 2025, driven by its extensive clinical development, regulatory approvals, and proven efficacy in treating melanoma. Hospitals and cancer research institutes widely adopt HSV-based therapies due to their immunogenic properties and ability to stimulate systemic anti-tumor responses. The well-established manufacturing process, robust safety profile, and strong collaborations between biotech companies and academic institutions further reinforce market leadership. Additionally, HSV therapies have demonstrated durable clinical outcomes, encouraging physician and patient preference. Growing awareness about immune-oncology treatments, inclusion in clinical guidelines, and expanding product pipelines contribute to sustained dominance. Strong research funding, increased physician confidence, and established market presence also play key roles.

The Vaccinia Virus segment is expected to witness the fastest CAGR of 15.9% from 2026 to 2033, fueled by ongoing clinical trials exploring novel engineered viruses for multiple solid tumors. Vaccinia virus is favored for its high replication efficiency, flexibility in genetic modification, and capacity to deliver therapeutic genes effectively. Rising investments in combination therapies with checkpoint inhibitors are boosting its clinical potential. Expansion into emerging markets, increased research funding, and enhanced safety profiles drive rapid adoption. Portable and targeted delivery systems, along with supportive regulatory frameworks, further enable growth. Growing interest in off-the-shelf therapies and scalable manufacturing processes supports market expansion. Strategic collaborations and licensing agreements accelerate pipeline development and global availability.

- By Application

On the basis of application, the market is segmented into Non-small Cell Lung Cancer (NSCLC), Melanoma, Breast Cancer, Pancreatic Cancer, and Others. The Melanoma segment dominated with a revenue share of 38.5% in 2025, as HSV-based oncolytic therapies are already approved and widely adopted in melanoma treatment. Hospitals and cancer centers prefer these therapies for unresectable or advanced melanoma, given their proven systemic immune activation and manageable side effect profiles. Clinical trials have shown durable responses, increasing physician confidence. Awareness campaigns and inclusion in treatment guidelines reinforce adoption. Research institutes and hospitals collaborate for advanced studies, further strengthening market position. Patient preference for immunotherapy over conventional chemotherapy and growing reimbursement coverage in developed regions also contribute to dominance.

The NSCLC segment is expected to witness the fastest CAGR of 14.8% from 2026 to 2033, due to rising global incidence and increased focus on oncolytic virus therapy for lung cancer. Systemic and intratumoral delivery strategies are being optimized for metastatic tumors. Clinical trials exploring combination with immune checkpoint inhibitors and targeted therapies are increasing. Expanding healthcare infrastructure, growing physician awareness, and improved patient outcomes accelerate adoption. Funding for translational research and early-phase trials supports rapid expansion. Regulatory guidance facilitating clinical adoption in developed countries contributes to strong growth potential.

- By Route of Administration

On the basis of route of administration, the market is segmented into Intravenous, Intratumoral, and Other. The Intratumoral segment dominated with a revenue share of 46.2% in 2025, as it allows high local virus concentration, enhanced tumor lysis, and reduced systemic toxicity. Hospitals and cancer centers favor intratumoral injections for accessible tumors, such as melanoma, where direct administration improves efficacy. Clinical trials and real-world studies validate safety and effectiveness. Adoption is further supported by established treatment protocols, trained staff, and integration with combination therapies. The segment benefits from physician familiarity, regulatory approvals, and positive patient outcomes. Availability of commercial delivery devices and standardized formulations strengthen dominance.

The Intravenous segment is expected to witness the fastest CAGR of 16.5% from 2026 to 2033, driven by the need to target metastatic tumors and systemic cancer indications. Research into nanoparticle-based or encapsulated viral delivery improves circulation stability and therapeutic efficacy. Hospitals and specialty clinics are increasingly adopting intravenous routes for convenience and broader tumor reach. Technological advancements, combined with rising home healthcare programs, are enhancing patient access. Growing clinical trials and interest from oncology centers support rapid adoption. Expanding reimbursement coverage and regulatory support further facilitate market growth.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, Cancer Research Institutes, and Others. The Hospital segment dominated with a revenue share of 62.7% in 2025, due to advanced critical care infrastructure, availability of specialized staff, and high-volume patient treatment. Hospitals manage clinical trials, provide immunotherapy protocols, and ensure safety monitoring. Centralized procurement, cold-chain management, and integration with oncology departments reinforce leadership. Hospitals also act as primary sites for physician training, patient education, and regulatory compliance. Adoption is accelerated by strong partnerships with biopharma companies and inclusion in national treatment guidelines.

The Cancer Research Institutes segment is expected to witness the fastest CAGR of 17.1% from 2026 to 2033, driven by ongoing research in next-generation oncolytic virus therapy, novel virus engineering, and combination immunotherapy approaches. Research institutes actively conduct clinical trials, contribute to early-stage development, and test therapies in preclinical models. Funding from government, private foundations, and venture capital supports rapid growth. Collaborative initiatives with hospitals and biotech companies are increasing adoption. Expansion of specialized research programs, advanced laboratory facilities, and training for scientists enable faster uptake.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated with a market share of 58.9% in 2025, as hospitals procure therapies directly for inpatient administration, critical care, and clinical trials. High-volume usage, adherence to regulatory standards, and availability of specialized storage facilities reinforce segment leadership. Hospital pharmacies also ensure proper cold-chain management and timely supply to oncology units. Integration with hospital IT systems and treatment protocols strengthens adoption.

The Online Pharmacy segment is expected to witness the fastest CAGR of 18.3% from 2026 to 2033, fueled by digitalization of medical supply chains, increasing home healthcare adoption, and demand for remote procurement of consumables and delivery devices. Online platforms expand access to small clinics and research institutes. Expansion of e-commerce in emerging regions, rising trust in online medical supplies, and improved logistics support rapid adoption. Growth is also accelerated by integration with telehealth programs and specialty delivery services.

Oncolytic Virus Immunotherapy Market Regional Analysis

- North America dominated the oncolytic virus immunotherapy market with the largest revenue share of 39.2% in 2025

- Supported by advanced healthcare infrastructure, strong R&D activities, high adoption of innovative cancer therapies, and the presence of leading biotechnology and pharmaceutical companies focusing on oncolytic virus treatments

- The market contributed the majority share due to early access to novel therapies and robust clinical trial networks

U.S. Oncolytic Virus Immunotherapy Market Insight

The U.S. oncolytic virus immunotherapy market captured the largest revenue share within North America, driven by the country’s well-established oncology care infrastructure, high patient awareness, extensive access to specialized cancer treatment centers, and active participation in clinical trials for novel oncolytic virus therapies. The presence of major pharmaceutical and biotechnology companies developing innovative treatments further propels market growth, alongside rising adoption of combination therapies in oncology.

Europe Oncolytic Virus Immunotherapy Market Insight

The Europe oncolytic virus immunotherapy market is projected to expand at a substantial CAGR during the forecast period, supported by increasing healthcare expenditure, well-developed clinical research networks, and growing patient awareness of advanced cancer treatments. Countries such as the U.K. and Germany are leading the adoption of oncolytic virus therapies in both hospitals and specialized cancer research centers.

U.K. Oncolytic Virus Immunotherapy Market Insight

The U.K. oncolytic virus immunotherapy market is anticipated to grow at a notable CAGR, driven by a well-developed healthcare system, strong presence of oncology-focused biotechnology firms, increasing clinical trial activities, and high awareness of advanced cancer treatment options. The country’s robust regulatory framework and patient access programs are further supporting the adoption of innovative therapies.

Germany Oncolytic Virus Immunotherapy Market Insight

The Germany oncolytic virus immunotherapy market is expected to expand at a considerable CAGR, fueled by rising healthcare expenditure, increasing prevalence of cancer, strong clinical research infrastructure, and growing adoption of advanced treatment solutions. The integration of oncolytic virus therapies into standard oncology care and research-driven hospitals is strengthening market growth in the region.

Asia-Pacific Oncolytic Virus Immunotherapy Market Insight

The Asia-Pacific oncolytic virus immunotherapy market is poised to grow at the fastest CAGR of 11.8% during the forecast period of 2026 to 2033, driven by improving healthcare access, increasing government and private investments in oncology research, rising cancer prevalence, and growing adoption of advanced cancer treatment solutions. Countries such as China, India, and Japan are key contributors to this rapid growth.

Japan Oncolytic Virus Immunotherapy Market Insight

The Japan oncolytic virus immunotherapy market is gaining momentum due to the country’s high awareness of oncology innovations, strong clinical research framework, and increasing adoption of advanced treatment options in hospitals and cancer research institutes. The aging population and rising incidence of cancer are also key factors driving demand.

China Oncolytic Virus Immunotherapy Market Insight

The China oncolytic virus immunotherapy market accounted for the largest market revenue share in Asia-Pacific in 2025, supported by its large patient population, increasing cancer prevalence, growing investments in oncology research, and improving access to specialized cancer care facilities. The development of domestic biotechnology firms focusing on oncolytic virus therapies further strengthens the market’s expansion.

Oncolytic Virus Immunotherapy Market Share

The Oncolytic Virus Immunotherapy industry is primarily led by well-established companies, including:

• Bristol-Myers Squibb (U.S.)

• Merck & Co., Inc. (U.S.)

• Genelux Corporation (U.S.)

• Oncolys BioPharma (Canada)

• Amgen (U.S.)

• Virttu Biologics (U.K.)

• Replimune Group, Inc. (U.S.)

• Cytovir, Inc. (U.S.)

• Transgene S.A. (France)

• OncoVEX (U.S.)

• HSV Therapeutics (U.S.)

• Advaxis, Inc. (U.S.)

• PSI Oncology (U.S.)

• OncoSec Medical Incorporated (U.S.)

• Therapeutic Oncolytic Viruses Ltd. (U.K.)

• Replimmune Biopharma (U.S.)

• ImmunoViro Solutions (Australia)

• Viron Therapeutics (U.S.)

• SillaJen, Inc. (South Korea)

Latest Developments in Global Oncolytic Virus Immunotherapy Market

- In May 2025, a pre‑print study explored the oncolytic and immunotherapeutic potential of the Newcastle Disease Virus (NDV), showing potent tumor specificity, immune activation, and apoptosis in cancers such as breast, colorectal, and melanoma. This supports renewed interest in NDV as a versatile oncolytic platform

- In June 2024, Calidi Biotherapeutics was granted a U.S. patent (No. 12,036,278) for its “SuperNova” technology platform, which uses mesenchymal stem cells loaded with an oncolytic vaccinia virus. This strengthens its intellectual property for its CLD-201 program, supporting future clinical development

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.