Global Open Ran Market

Market Size in USD Billion

USD

5.28 Billion

USD

51.73 Billion

2025

2033

USD

5.28 Billion

USD

51.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.28 Billion | |

| USD 51.73 Billion | |

| % | |

|

Open RAN Market Size

- The global open RAN market size was valued at USD 5.28 billion in 2025 and is expected to reach USD 51.73 billion by 2033, at a CAGR of 33.01% during the forecast period

- The market growth is largely fuelled by the increasing deployment of 5G networks, growing demand for flexible and cost-efficient network architectures, and the push for vendor-neutral solutions in telecommunications

- In addition, rising adoption of cloud-native technologies, virtualization, and software-defined networking in mobile networks is further supporting the expansion of the open RAN market

Open RAN Market Analysis

- Open RAN technology is gaining traction as telecom operators seek to reduce dependency on traditional vendors while enabling multi-vendor interoperability and network customization

- The market is driven by the need for improved network efficiency, scalability, and automation, along with government and industry initiatives promoting open standards for 5G and future networks

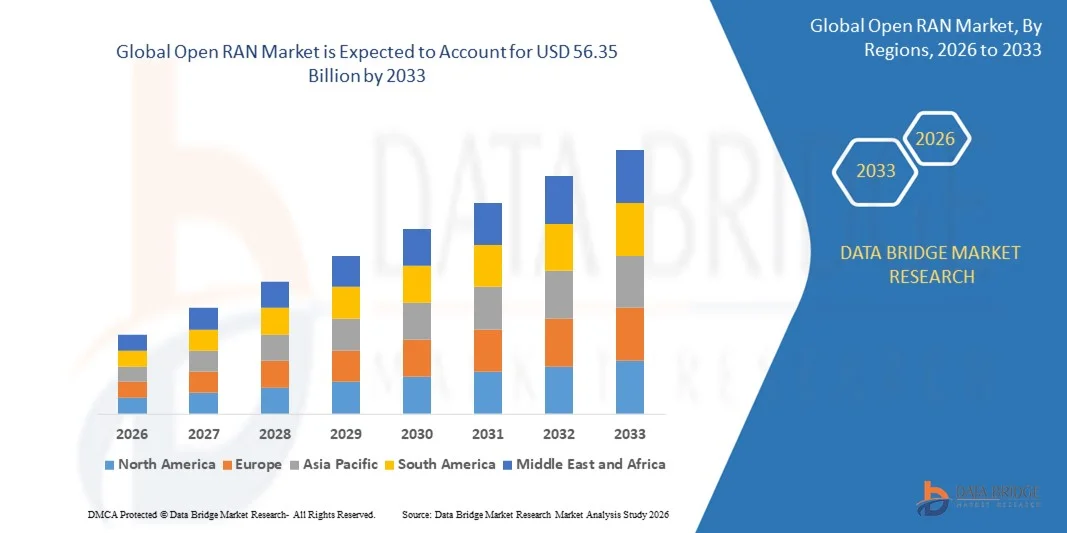

- North America dominated the open RAN market with the largest revenue share of 36.8% in 2025, driven by rapid 5G deployment, early adoption of virtualization technologies, and strong telecom infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global open RAN market, driven by rising 5G adoption, urbanization, government digitalization initiatives, and expanding enterprise and industrial network deployments

- The hardware segment held the largest market revenue share in 2025, driven by the growing need for multi-vendor radio units, servers, and networking equipment in 5G and virtualized networks. Hardware solutions enable operators to implement flexible and scalable RAN architectures while ensuring performance and reliability across large deployments

Report Scope and Open RAN Market Segmentation

|

Attributes |

Open RAN Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Open RAN Market Trends

Rising Adoption of 5G and Virtualized Network Architectures

- The growing deployment of 5G networks is significantly shaping the open RAN market, as telecom operators increasingly prefer flexible, vendor-neutral network architectures. Open RAN solutions allow multi-vendor interoperability, network customization, and cost optimization, encouraging operators to adopt disaggregated infrastructure. This trend strengthens market adoption across mobile network operators, service providers, and enterprise applications, driving investments in open standards and software-defined solutions

- Increasing interest in virtualization, cloud-native deployments, and network automation is accelerating the demand for open RAN solutions. Operators are prioritizing efficiency, scalability, and simplified operations while reducing dependency on proprietary hardware. This is driving collaborations between network equipment providers and software vendors to develop interoperable, open-standard RAN platforms that enhance network performance and reduce operational costs

- Open RAN is also gaining attention for its potential to support emerging applications such as private 5G networks, industrial IoT, and smart cities. Telecom providers are investing in R&D to improve spectrum utilization, radio access flexibility, and AI-based network optimization. These developments are reinforcing the market’s growth prospects and attracting new entrants focused on software, radio units, and integration services

- For instance, in 2025, Rakuten Mobile in Japan and Telefónica in Spain expanded open RAN deployments in commercial 5G networks, enabling multi-vendor integration and enhanced network efficiency. These deployments were introduced to reduce operational costs, improve service flexibility, and accelerate 5G rollout timelines. The projects also highlighted open RAN’s role in accelerating innovation in mobile network infrastructure

- While adoption is increasing, sustained market growth depends on standardization, ecosystem maturity, and operator readiness for disaggregated and software-driven networks. Vendors are focusing on improving interoperability, providing end-to-end solutions, and educating operators on performance and security benefits to drive broader adoption

Open RAN Market Dynamics

Driver

Growing Demand for Flexible and Vendor-Neutral Networks

- Rising operator interest in open, disaggregated RAN architectures is a major driver for the open RAN market. Network operators are replacing traditional proprietary solutions to reduce CAPEX/OPEX, improve scalability, and enable multi-vendor integration. This trend is also encouraging investment in software-defined radio units and orchestration platforms, expanding the ecosystem and promoting standardization

- Expansion of 5G deployments and private network initiatives is further supporting market growth. Open RAN enables operators to meet diverse application requirements while optimizing network performance and cost. Increased adoption by telecom providers across North America, Europe, and Asia-Pacific is accelerating ecosystem development and solution maturity

- Operators and vendors are actively promoting open RAN through pilot projects, interoperability testing, and partnerships with software and hardware providers. These efforts highlight the operational and financial advantages of open RAN, enhancing market confidence and encouraging large-scale commercial adoption

- For instance, in 2025, Rakuten Mobile in Japan and Vodafone in Europe reported significant cost savings and deployment flexibility by implementing open RAN in select urban and rural regions. These deployments validated the efficiency and scalability of vendor-neutral solutions, attracting further interest from global telecom operators

- Although rising adoption supports growth, wider market penetration depends on technology maturity, standardization, and ecosystem readiness. Investments in R&D, interoperability testing, and open-source software development will be critical for supporting large-scale deployment and sustaining competitive advantage

Restraint/Challenge

Integration Complexity and Performance Concerns

- Open RAN faces challenges in terms of integration complexity, as multi-vendor solutions require rigorous interoperability and performance testing. Ensuring seamless communication between hardware and software components remains a key barrier for operators, particularly in dense 5G networks

- Limited ecosystem maturity and uneven operator experience can slow adoption, especially in emerging markets where technical expertise and infrastructure are still developing. Vendors must provide comprehensive support, training, and managed services to overcome these barriers

- Security and reliability concerns also impact market growth, as disaggregated architectures may introduce additional attack surfaces. Operators are cautious about potential performance variations and network downtime when integrating new vendors or software components

- For instance, in 2024, several telecom operators in Southeast Asia and Latin America reported delays in open RAN rollout due to interoperability testing challenges and concerns over network latency. These issues highlighted the need for standardized solutions, vendor collaboration, and thorough performance validation before large-scale deployment

- Overcoming these challenges will require enhanced standardization, ecosystem collaboration, and robust testing frameworks. Operators and vendors must focus on interoperability, security, and performance optimization to enable widespread adoption of open RAN solutions and fully realize its cost and flexibility benefits

Open RAN Market Scope

The market is segmented on the basis of component, unit, deployment, network, and frequency.

- By Component

On the basis of component, the open RAN market is segmented into hardware, software, and services. The hardware segment held the largest market revenue share in 2025, driven by the growing need for multi-vendor radio units, servers, and networking equipment in 5G and virtualized networks. Hardware solutions enable operators to implement flexible and scalable RAN architectures while ensuring performance and reliability across large deployments.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of network orchestration, virtualization, and AI-enabled optimization tools. Software-driven solutions allow telecom operators to manage, configure, and automate open RAN networks efficiently, providing enhanced network flexibility and reduced operational costs.

- By Unit

On the basis of unit, the market is segmented into radio unit, distributed unit, and centralized unit. The radio unit segment held the largest share in 2025, as it forms the critical interface between the core network and end-users, supporting high-speed connectivity and multi-band spectrum deployment.

The distributed unit segment is projected to witness the fastest growth from 2026 to 2033, driven by the need for low-latency, edge-computing capabilities, and efficient handling of traffic in dense urban networks. Distributed units enable operators to optimize performance and reduce backhaul costs while supporting 5G services.

- By Deployment

On the basis of deployment, the market is segmented into private, hybrid cloud, and public cloud. The hybrid cloud segment held the largest market revenue share in 2025, owing to its ability to combine on-premises control with cloud scalability, enabling operators to balance cost, flexibility, and security.

The private cloud segment is projected to witness steady growth from 2026 to 2033, driven by enterprise adoption of secure and dedicated networks for industrial automation, IoT, and mission-critical applications. Private cloud deployments provide enhanced control, security, and performance for specialized use cases.

- By Network

On the basis of network, the market is segmented into 2G/3G, 4G, and 5G. The 5G segment dominated in 2025 due to the rapid global rollout of next-generation mobile networks and the increasing demand for high-speed, low-latency connectivity across commercial and consumer applications.

The 4G segment is projected to witness steady growth from 2026 to 2033, driven by ongoing upgrades in emerging markets and the need for backward compatibility to support legacy services alongside 5G deployments.

- By Frequency

On the basis of frequency, the market is segmented into sub-6 GHz and mmWave. The sub-6 GHz segment held the largest share in 2025, owing to its wide coverage, better signal propagation, and suitability for urban and suburban deployments.

The mmWave segment is projected to witness steady growth from 2026 to 2033, driven by the deployment of ultra-high-speed 5G networks in dense urban areas and enterprise campuses. MmWave frequencies provide enhanced bandwidth and support advanced applications such as AR/VR, autonomous systems, and private networks.

Open RAN Market Regional Analysis

- North America dominated the open RAN market with the largest revenue share of 36.8% in 2025, driven by rapid 5G deployment, early adoption of virtualization technologies, and strong telecom infrastructure

- Operators in the region highly value the flexibility, cost-efficiency, and multi-vendor interoperability offered by open RAN solutions, enabling optimized network performance and easier integration of new software and hardware components

- This widespread adoption is further supported by high technology investments, supportive regulatory policies, and growing interest in private and hybrid network deployments, establishing open RAN as a preferred solution for telecom operators and enterprises

U.S. Open RAN Market Insight

The U.S. open RAN market captured the largest revenue share in 2025 within North America, fueled by increasing investments in 5G networks and software-defined radio access solutions. Operators are prioritizing cost reduction, network flexibility, and interoperability between vendors. The rising adoption of private and hybrid cloud deployments, combined with AI-enabled orchestration and automation tools, further propels the market. In additionally, telecom operators are leveraging open RAN to accelerate rollout timelines and enhance service reliability across urban and rural networks.

Europe Open RAN Market Insight

The Europe open RAN market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by government initiatives promoting open standards, spectrum liberalization, and increased demand for flexible, cost-efficient networks. Rising urbanization, industrial automation, and smart city projects are fostering open RAN adoption. European telecom operators are also drawn to the energy efficiency, scalability, and vendor-neutral advantages offered by these networks. The region is experiencing significant deployments across public 5G and private enterprise networks.

U.K. Open RAN Market Insight

The U.K. open RAN market is expected to witness the fastest growth rate from 2026 to 2033, driven by aggressive 5G rollout plans, government support for open network initiatives, and rising demand for private 5G networks in enterprises. In additionally, operators are adopting open RAN to reduce dependence on legacy proprietary solutions. The U.K.’s robust telecom ecosystem, alongside extensive R&D and collaboration between vendors and operators, is expected to continue stimulating market expansion.

Germany Open RAN Market Insight

The Germany open RAN market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s focus on network modernization, industrial automation, and digitalization initiatives. Germany’s advanced telecom infrastructure and strong adoption of 5G technologies promote the implementation of open RAN, particularly in urban and industrial environments. Integration of open RAN with AI-enabled network orchestration is becoming increasingly prevalent, helping operators optimize cost, performance, and energy efficiency.

Asia-Pacific Open RAN Market Insight

The Asia-Pacific open RAN market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising 5G adoption, urbanization, and digital transformation initiatives in countries such as China, Japan, India, and South Korea. The region's increasing telecom investments, supportive government policies, and private network deployments are accelerating open RAN adoption. Furthermore, APAC is emerging as a manufacturing and software hub for open RAN components, improving affordability and availability across diverse markets.

Japan Open RAN Market Insight

The Japan open RAN market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high-tech infrastructure, emphasis on automation, and early adoption of advanced network technologies. Telecom operators are integrating open RAN with 5G networks, cloud-native architectures, and AI-driven optimization tools to enhance flexibility, reduce costs, and improve service quality. Japan’s focus on industrial IoT and smart city applications is further fueling market demand.

China Open RAN Market Insight

The China open RAN market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid 5G deployment, government initiatives for network openness, and increasing adoption of virtualization and cloud-native technologies. China is one of the largest markets for telecom infrastructure, and open RAN solutions are becoming increasingly popular among mobile operators and enterprises. The push for smart cities, private 5G networks, and multi-vendor integration, along with strong domestic vendors, are key factors driving market growth in China.

Open RAN Market Share

The Open RAN industry is primarily led by well-established companies, including:

- Mavenir (U.S.)

- NEC Corporation (Japan)

- Fujitsu Limited (Japan)

- Nokia Corporation (Finland)

- Samsung Electronics Co., Ltd. (South Korea)

- Radisys Corporation (U.S.)

- Parallel Wireless (U.S.)

- ZTE Corporation (China)

- AT&T Inc. (U.S.)

- Casa Systems, Inc. (U.S.)

- Broadcom, Inc. (U.S.)

- Juniper Networks, Inc. (U.S.)

- Rakuten (Japan)

- Amdocs (U.S.)

- Comba Telecom (Hong Kong)

Latest Developments in Global Open RAN Market

- In March 2025, Airspan Networks completed the acquisition of Jabil’s open RAN radio products, including associated intellectual property, former radio researchers, developers, and advanced testing facilities at New Jersey. This development strengthens Airspan’s R&D capabilities, accelerates product innovation, and enhances its competitiveness in the open RAN market. The integration of Jabil’s expertise and infrastructure is expected to improve deployment efficiency, reduce time-to-market, and support broader adoption of open RAN solutions globally

- In February 2024, Ericsson, Nokia, Samsung Electronics, Microsoft, SoftBank Corp., and T-Mobile US jointly established the AI-RAN Alliance, aimed at integrating artificial intelligence into radio access networks. This strategic collaboration focuses on advancing network automation, improving efficiency, and enabling smarter, adaptive 5G and future network deployments. The initiative is expected to drive innovation, foster interoperability, and accelerate adoption of AI-driven open RAN technologies across global telecom networks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.