Global Optical Transceiver Market

Market Size in USD Billion

USD

13.08 Billion

USD

41.17 Billion

2024

2032

USD

13.08 Billion

USD

41.17 Billion

2024

2032

| 2025 - 2032 | |

| USD 13.08 Billion | |

| USD 41.17 Billion | |

| % | |

|

Optical Transceiver Market Size

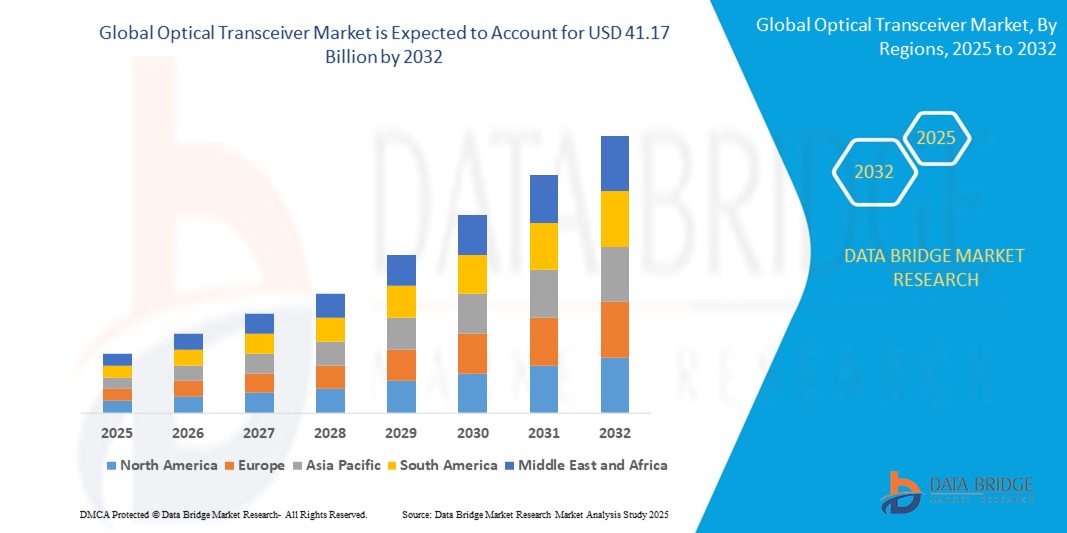

- The global optical transceiver market size was valued at USD 13.08 billion in 2024 and is expected to reach USD 41.17 billion by 2032, at a CAGR of 15.41% during the forecast period

- The market growth is largely fuelled by the increasing demand for high-speed internet, rapid expansion of data centers, and the rising adoption of 5G networks across various regions

- In addition, the growing shift from traditional copper-based networks to fiber-optic communication systems is accelerating the deployment of optical transceivers, especially in emerging economies aiming to modernize digital infrastructure

Optical Transceiver Market Analysis

- The market is witnessing a strong shift towards advanced optical modules such as QSFP-DD and CFP8, as network operators and cloud service providers upgrade their infrastructures to support higher bandwidths and faster data transmission

- Growing investments in broadband infrastructure, coupled with the proliferation of smart devices and IoT applications, are driving continuous innovation and expansion in the optical transceiver ecosystem across telecom, data centers, and enterprise applications

- North America dominated the optical transceiver market with the largest revenue share in 2024, driven by the widespread deployment of high-speed data centers and advanced telecommunications networks

- Asia-Pacific region is expected to witness the highest growth rate in the global optical transceiver market, driven by rapid urbanization, widespread 5G rollout, and expanding hyperscale data centers in countries such as China, Japan, South Korea, and India. The region’s strong manufacturing ecosystem and emphasis on digital infrastructure development are also critical growth enablers

- The QSFP and its variants segment dominated the market with the largest revenue share in 2024, primarily driven by its wide adoption in high-speed data center applications. These modules offer compact size, high port density, and support for up to 400G data rates, making them ideal for hyperscale cloud infrastructures and enterprise networks. Their compatibility with evolving standards and ability to handle increasing traffic demands contributes to their market leadership

Report Scope and Optical Transceiver Market Segmentation

|

Attributes |

Optical Transceiver Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Coherent Corp. (U.S.) |

|

Market Opportunities |

• Expansion of 5G Infrastructure Across Emerging Economies • Rising Demand for High-Speed Optical Modules in AI-Powered Data Centers |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Optical Transceiver Market Trends

“Rising Adoption of Co-Packaged Optics in Data Centers”

• Co-packaged optics is emerging as a transformative innovation by integrating optical engines directly with switch ASICs, reducing electrical signal loss and improving overall energy efficiency in high-speed data center environments. This approach supports compact and high-density designs, allowing data centers to keep pace with bandwidth-intensive applications and increasing interconnect demands without compromising performance or space. As data center architectures evolve to support next-gen speeds, the momentum behind CPO continues to accelerate among major cloud operators and equipment vendors

• One of the primary benefits of co-packaged optics is its ability to overcome limitations of traditional pluggable modules, such as excessive power consumption, higher latency, and cooling inefficiencies in dense setups. CPO enables direct optical integration, reducing the electrical path and simplifying signal transmission across shorter distances, which is critical for enabling seamless 800G and 1.6T interconnects. This technological leap addresses the future needs of hyperscale data centers focused on low-latency, high-throughput operations

• Major semiconductor and network technology providers, including Intel and Broadcom, have already begun introducing CPO-enabled prototypes and defining commercial product roadmaps. These developments indicate significant industry commitment toward co-packaged optics, pushing it closer to widespread commercialization. With growing demand for higher speeds, lower power, and improved thermal performance, CPO adoption is likely to become mainstream in next-generation data center deployments within the coming years

• Collaborative initiatives such as the Open Compute Project (OCP) are playing a crucial role in advancing CPO by establishing technical standards and fostering ecosystem-wide collaboration. These efforts lower barriers to entry, encourage innovation, and help cloud and enterprise customers adopt CPO-based infrastructure more efficiently. As standardized interfaces and interoperable designs mature, broader market participation is expected to fuel faster growth and diversification in the CPO landscape

• For instance, in 2023, Broadcom unveiled its Tomahawk 5 switch chip with native support for co-packaged optics, targeting hyperscale cloud environments seeking performance scalability. Similarly, Intel demonstrated a working 1.6T CPO engine, showcasing the feasibility of this integration at terabit-level bandwidths. These examples underscore the increasing traction and investment in CPO as a future-proof optical transceiver solution

Optical Transceiver Market Dynamics

Driver

“Growing Deployment of 5G and Hyperscale Data Centers”

• The global rollout of 5G infrastructure is significantly boosting demand for optical transceivers as they provide the high-speed, low-latency data transmission required to support 5G networks. These components play a crucial role in fronthaul, midhaul, and backhaul segments, ensuring reliable connectivity between base stations and network cores. Countries such as the U.S., China, and South Korea are investing heavily in 5G, accelerating market demand for advanced optical modules

• The rise of hyperscale data centers driven by cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud is further expanding the market for optical transceivers. These facilities require large volumes of high-bandwidth transceivers to manage massive data loads and support real-time processing needs. To meet sustainability targets, hyperscalers are adopting energy-efficient transceivers such as QSFP-DD and OSFP form factors

• The increase in remote work, video conferencing, and data consumption during and post-pandemic has amplified the need for scalable internet infrastructure. This growth is pushing telecom and broadband providers to modernize their optical networks with higher capacity transceivers. For instance, Verizon and AT&T are upgrading their backbone networks using 400G optical modules to meet future data requirements

• Technological advancements in transceiver design, such as the integration of silicon photonics and pluggable coherent optics, are enabling higher data rates with reduced power consumption. These innovations are helping vendors deliver cost-effective and compact solutions suitable for 5G and cloud applications. Companies such as Intel and Cisco are leading developments in this space with integrated optics platforms

• In May 2023, Nokia launched a 400G optical transceiver based on silicon photonics for 5G and metro deployments, reducing cost per bit and power usage. This strategic development enhances network efficiency and scalability, directly contributing to the rapid global adoption of high-speed fiber infrastructure for next-gen connectivity

Restraint/Challenge

“High Cost of Advanced Optical Modules and Integration Barriers”

• The production of high-speed optical transceivers involves costly materials, precision engineering, and advanced fabrication processes that drive up the final product price. Modules supporting 400G and beyond often require expensive technologies such as digital signal processors (DSPs) and multi-core fiber alignment systems, making them unaffordable for small-scale deployments. This pricing barrier limits widespread adoption in cost-sensitive regions

• Compatibility and standardization issues between different vendors’ hardware make integration of optical modules into existing networks challenging. Telecom operators and data center providers must ensure interoperability between new and legacy systems, which can require extensive testing and custom configurations. These integration challenges delay deployment and increase operational complexity

• The supply chain for optical components is vulnerable to disruptions due to dependence on specialized manufacturing hubs, such as those in East Asia. Geopolitical tensions, raw material shortages, or production halts—as seen during the COVID-19 pandemic—can lead to delays and inflated prices. Such disruptions can severely impact project timelines in telecom and cloud infrastructure

• A shortage of skilled engineers and optical networking experts is also impeding the pace of innovation and deployment. Designing, installing, and maintaining high-speed transceiver systems requires advanced knowledge, and the talent pool in this field is relatively limited. This human resource gap creates bottlenecks in scaling next-gen optical networks

• In 2022, several hyperscalers including Meta and Microsoft reported delays in the rollout of 800G transceivers due to thermal design challenges and integration complexities. These technical hurdles highlight how the transition to ultra-high-speed optics remains an ongoing challenge, impacting product timelines and deployment schedules in critical applications

Optical Transceiver Market Scope

The market is segmented on the basis of form factor, data rate, fiber type, distance, wavelength, connector, protocol, and application.

- By Form Factor

On the basis of form factor, the optical transceiver market is segmented into SFF and SFP, SFP+ and SFP28, QSFP, QSFP+, QSFP-DD, QSFP28, and QSFP56, CFP, CFP2, CFP4, and CFP8, XFP, and CXP. The QSFP and its variants segment dominated the market with the largest revenue share in 2024, primarily driven by its wide adoption in high-speed data center applications. These modules offer compact size, high port density, and support for up to 400G data rates, making them ideal for hyperscale cloud infrastructures and enterprise networks. Their compatibility with evolving standards and ability to handle increasing traffic demands contributes to their market leadership.

The CFP series is expected to witness the fastest growth rate from 2025 to 2032, owing to its suitability for ultra-high bandwidth applications in telecom and data centers. These transceivers offer scalability, long-distance transmission, and support for coherent modulation formats, making them highly preferred for next-generation networks. Their use in metro and long-haul optical transport networks is expected to increase significantly with the roll-out of 800G and 1.6T solutions.

- •By Data Rate

On the basis of data rate, the market is segmented into Less Than 10 Gbps, 10 Gbps to 40 Gbps, 41 Gbps to 100 Gbps, and More Than 100 Gbps. The 41 Gbps to 100 Gbps segment accounted for the largest share in 2024 due to growing demand from cloud service providers, content delivery networks, and telecom operators upgrading to 100G infrastructure. These transceivers strike a balance between speed, power efficiency, and cost, making them ideal for mainstream adoption.

The More Than 100 Gbps segment is expected to witness the fastest growth rate from 2025 to 2032, supported by increasing adoption of AI, edge computing, and next-gen data center architectures. As traffic continues to scale rapidly, demand for 200G, 400G, and 800G modules is rising, especially across hyperscale and AI-intensive computing environments.

- By Fiber Type

On the basis of fiber type, the market is segmented into Single-Mode Fiber (SMF) and Multimode Fiber (MMF). The Single-Mode Fiber (SMF) segment held the dominant market share in 2024, due to its long-distance transmission capabilities and low signal attenuation, ideal for telecom and metro networks. SMF’s scalability and compatibility with coherent transmission technologies make it the preferred choice for high-capacity backbone links.

Multimode Fiber (MMF) is expected to witness the fastest growth rate from 2025 to 2032, particularly in short-reach data center applications. Its cost-effectiveness, ease of deployment, and compatibility with vertical-cavity surface-emitting lasers (VCSELs) support its adoption in enterprise and edge computing environments.

- By Distance

On the basis of distance, the market is segmented into Less Than 1 km, 1 to 10 km, 11 to 100 km, and More Than 100 km. The 1 to 10 km segment held the largest market share in 2024, as it aligns with most intra-city and campus-level telecom and enterprise applications. This segment benefits from the deployment of 5G networks, metro aggregation, and cloud edge infrastructure.

The More Than 100 km segment is expected to witness the fastest growth rate from 2025 to 2032, driven by surging demand for long-haul transport and submarine cable systems. These transceivers enable high-capacity data transmission across continents, supporting global connectivity and digital infrastructure.

- By Wavelength

On the basis of wavelength, the market is segmented into 850 nm Band, 1310 nm Band, 1550 nm Band, and Other Wavelengths. The 1310 nm Band segment dominated the market in 2024 due to its optimal performance in intermediate distance and metro access networks. It offers low dispersion and attenuation over standard SMF, making it ideal for most carrier-grade deployments.

The 1550 nm Band segment is expected to witness the fastest growth rate from 2025 to 2032, particularly for long-distance, high-capacity optical communication. Its low signal loss and compatibility with erbium-doped fiber amplifiers (EDFAs) support its use in backbone and long-haul networks.

- By Connector

On the basis of connector, the market is segmented into LC, SC, MPO, and RJ-45. The LC connector segment held the largest market share in 2024, supported by its compact form factor, high precision, and popularity in modern fiber-optic systems. LC connectors are widely used in data centers, enterprise networks, and telecom facilities for both SMF and MMF deployments.

MPO connectors is expected to witness the fastest growth rate from 2025 to 2032, due to their high-density capabilities, enabling parallel transmission in 100G, 400G, and 800G transceivers. Their efficiency in managing multiple fiber strands in compact enclosures makes them essential for high-bandwidth, space-constrained applications.

- By Protocol

On the basis of protocol, the market is segmented into Ethernet, Fiber Channels, CWDM/DWDM, FTTx, and Other Protocols. The Ethernet segment led the market in 2024, driven by its widespread deployment across data centers, enterprise backbones, and internet exchanges. The continuous evolution of Ethernet standards supports faster transceiver speeds and scalability.

CWDM/DWDM is expected to witness the fastest growth rate from 2025 to 2032, due to rising adoption in telecom and metro networks requiring dense, high-capacity wavelength multiplexing. These protocols allow efficient use of fiber infrastructure, making them critical for long-distance and high-traffic environments.

- By Application

On the basis of application, the market is segmented into Telecommunication, Data Center, and Enterprise. The Telecommunication segment dominated the market in 2024, as operators expanded their fiber footprint to meet growing mobile and broadband demands. Optical transceivers play a crucial role in enabling high-speed, scalable, and cost-efficient networks.

The Data Center segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by exponential growth in data traffic, AI workloads, and cloud computing services. The demand for low-latency, high-throughput transceivers across hyperscale facilities is a key driver of this trend.

Optical Transceiver Market Regional Analysis

- North America dominated the optical transceiver market with the largest revenue share in 2024, driven by the widespread deployment of high-speed data centers and advanced telecommunications networks

- The region benefits from significant investments in cloud computing infrastructure and the rapid adoption of 5G services

- The increasing demand for high-bandwidth, low-latency data transmission across industries such as enterprise IT, healthcare, and media & entertainment further propels market growth

- Major technology companies based in the U.S. are also continuously innovating to improve transceiver capabilities, enhancing the region's competitive advantage

U.S. Optical Transceiver Market Insight

The U.S. optical transceiver market captured the largest share within North America in 2024, supported by robust growth in hyperscale data centers and the continued expansion of fiber optic networks. Companies such as Amazon, Google, and Meta are investing heavily in next-generation optical technologies to support massive data traffic volumes. In addition, the federal government’s focus on improving digital infrastructure through initiatives such as the Broadband Equity Access and Deployment (BEAD) program is contributing to wider fiber optic deployment, thereby boosting demand for optical transceivers across the country.

Europe Optical Transceiver Market Insight

The Europe optical transceiver market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing demand for high-speed internet, rapid expansion of cloud services, and the digital transformation of key industries. Countries such as Germany, France, and the U.K. are leading the charge in upgrading their telecommunications infrastructure with high-capacity optical links. The adoption of green data center strategies across Europe is also influencing the demand for energy-efficient optical transceiver solutions, particularly those supporting 100G and 400G speeds.

Germany Optical Transceiver Market Insight

The Germany optical transceiver market is expected to witness the fastest growth rate from 2025 to 2032, as the country continues to invest in upgrading its internet backbone and rolling out 5G networks. Demand is rising from industries such as automotive, manufacturing, and healthcare, where real-time data processing is crucial. The integration of smart manufacturing technologies and Industrial Internet of Things (IIoT) across factories is further pushing the need for low-latency, high-throughput fiber optic communication systems, strengthening the outlook for optical transceivers in Germany.

Asia-Pacific Optical Transceiver Market Insight

The Asia-Pacific region is expected to witness the fastest growth rate from 2025 to 2032, led by rapid digitization, increasing internet penetration, and growing demand for bandwidth across densely populated countries such as China, India, Japan, and South Korea. The surge in smart city developments, the expansion of 5G networks, and the construction of new data centers by both global and regional providers are major contributors to market growth. Local production capabilities and supportive government policies are also helping the region emerge as a key manufacturing and consumption hub for optical transceivers.

China Optical Transceiver Market Insight

The China optical transceiver market held the largest share in the Asia-Pacific region in 2024, supported by the country's leadership in telecom infrastructure and large-scale cloud service deployment. Major domestic players, coupled with strong government backing for fiber-optic upgrades and 5G rollouts, are driving demand. The growing e-commerce, online education, and video streaming sectors are also increasing the need for high-speed data transmission, making China a critical market for both domestic and international optical transceiver vendors.

Japan Optical Transceiver Market Insight

Japan’s optical transceiver market is expected to witness the fastest growth rate from 2025 to 2032, driven by rising investments in high-speed internet infrastructure and the rapid adoption of digital services. With a strong emphasis on research and innovation, Japanese firms are advancing compact, energy-efficient optical components to meet the evolving needs of data center operators and telecom service providers. In addition, the ongoing transition to 5G and the proliferation of IoT devices are accelerating the adoption of high-performance optical transceivers across both enterprise and consumer networks.

Optical Transceiver Market Share

The Optical Transceiver industry is primarily led by well-established companies, including:

• Coherent Corp. (U.S.)

• Hisense Broadband, Inc. (China)

• Broadcom Inc. (U.S.)

• INNOLIGHT (China)

• Lumentum Operations LLC (U.S.)

• Fujitsu Optical Components Limited (Japan)

• Accelink Technology Co. Ltd. (China)

• Sumitomo Electric Industries, Ltd. (Japan)

• Intel Corporation (U.S.)

• Cisco Systems, Inc. (U.S.)

Latest Developments in Global Optical Transceiver Market

- In October 2023, Lumentum Operations LLC (U.S.) announced the launch of its 800G ZR+ and OdBm 400G ZR+ transceivers, aimed at enhancing seamless connectivity between data centers. These transceivers deliver data rates of up to 800 Gbps on a single wavelength, offering significant improvements in bandwidth efficiency. This development is expected to meet the growing data transmission demands of hyperscale networks and support the global scale-up of cloud infrastructure

- In July 2023, Coherent Corp. (U.S.) introduced its 800G ZR/ZR+ transceivers in ultracompact QSFP-DD and OSFP form factors, specifically designed for high-capacity optical communications networks. These devices can be directly inserted into IP routers, streamlining integration and reducing infrastructure complexity. The advancement boosts optical performance while enabling cost-effective deployment of high-speed data transmission in metro and long-haul network applications

- In March 2023, Hisense Broadband, Inc. (China) launched its 800G QSFP-DD BiDi SR4.2 transceiver, which supports 800 Gbps over 100 meters of multimode fiber using dual-wavelength BiDi technology. This innovation enables efficient short-reach data center interconnects and helps reduce fiber usage and installation costs. The product is set to accelerate the adoption of next-generation high-speed optical solutions in large-scale data environments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Optical Transceiver Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Optical Transceiver Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Optical Transceiver Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.