Global Optoelectronic Market

Market Size in USD Billion

USD

43.50 Billion

USD

123.41 Billion

2025

2033

USD

43.50 Billion

USD

123.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 43.50 Billion | |

| USD 123.41 Billion | |

| % | |

|

Optoelectronic Market Overview

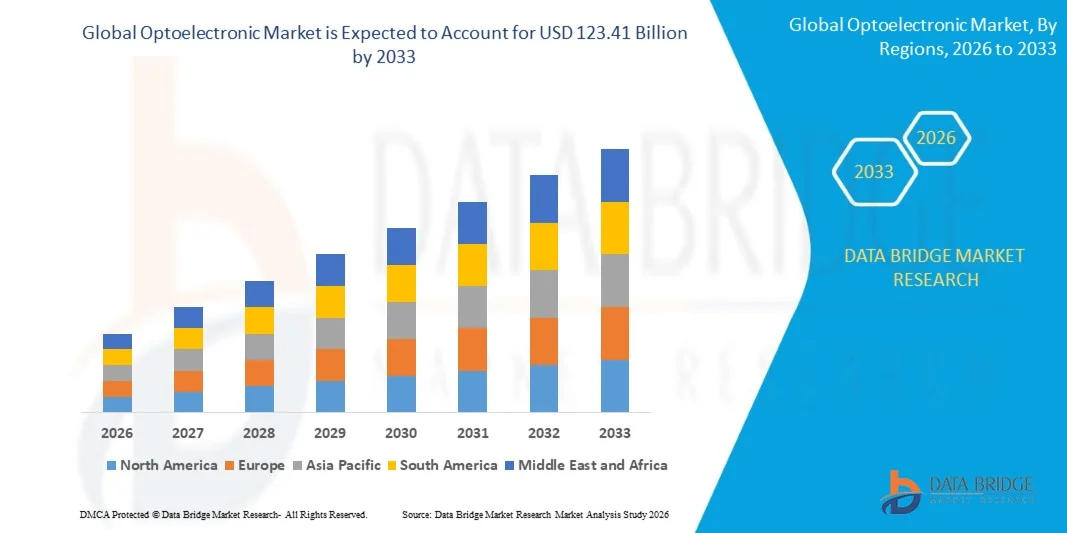

The Optoelectronic Market was valued at USD 43.50 billion in 2025 and is projected to reach USD 123.41 billion by 2033, growing at a CAGR of 13.92% from 2026 to 2033. The market is witnessing strong growth driven by increasing demand for high-speed data communication, rapid adoption of advanced consumer electronics, and expanding deployment of optoelectronic components across automotive, healthcare, industrial automation, and telecommunications applications.

The growing need for energy-efficient electronic systems, coupled with advancements in semiconductor technologies and optical communication networks, is accelerating the adoption of optoelectronic devices worldwide. Components such as LEDs, image sensors, laser diodes, optocouplers, and photodetectors are increasingly being integrated into smartphones, wearable devices, autonomous vehicles, medical imaging systems, and smart manufacturing equipment. In addition, the rapid expansion of 5G infrastructure, data centers, and fiber-optic communication networks is creating significant demand for high-performance optoelectronic solutions capable of supporting faster data transmission and improved connectivity. Continuous innovations in miniaturization, sensing technologies, and energy-efficient lighting systems are further enhancing market growth, while increasing investments in smart cities, artificial intelligence, and Internet of Things (IoT) ecosystems continue to expand the application scope of optoelectronic technologies across global industries.

Key Market Trends & Insights

- North America dominated the optoelectronic market with the largest revenue share of 37.85% in 2025, supported by strong investments in semiconductor technologies, widespread adoption of optical communication systems, rapid expansion of hyperscale data centers, and growing demand for advanced imaging and sensing technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 15.20% from 2026 to 2033. Growth is driven by expanding electronics manufacturing activities, increasing investments in telecommunications infrastructure, rising semiconductor production, and growing demand for consumer electronics and optical communication equipment across emerging economies.

- The Light Emitting Diodes (LED) segment held the largest market revenue share of approximately 32.7% in 2025, driven by its widespread adoption across general lighting, automotive lighting, display technologies, industrial equipment, and consumer electronics. LEDs are preferred due to their high energy efficiency, long operational life, compact design, and increasing integration into smart lighting and display applications worldwide.

- The Image Sensors segment is projected to register the fastest growth at a CAGR of 16.5% from 2026 to 2033, driven by rising demand for smartphone cameras, autonomous vehicle vision systems, medical imaging equipment, and AI-powered machine vision applications. Increasing deployment of advanced CMOS image sensors across consumer and industrial sectors is accelerating segment expansion.

- The Consumer Electronics segment held the largest market revenue share of approximately 36.9% in 2025, driven by extensive utilization of optoelectronic components in smartphones, tablets, wearable devices, smart televisions, gaming systems, and augmented reality products. Continuous innovation in display technologies, imaging systems, and optical sensing solutions is supporting strong demand across the segment.

- The Healthcare segment is projected to register the fastest growth at a CAGR of 15.8% from 2026 to 2033, driven by increasing adoption of optoelectronic technologies in medical imaging, diagnostic equipment, patient monitoring devices, and minimally invasive surgical systems. Growing healthcare digitization and demand for precision diagnostics are accelerating segment growth globally.

- The Light Emitting Diode segment held the largest market revenue share of approximately 34.4% in 2025, driven by strong demand from lighting, display panels, automotive systems, consumer electronics, and smart city infrastructure projects. The segment continues to benefit from increasing energy-efficiency regulations and the global transition toward sustainable lighting technologies.

- The Optical Fibers segment is projected to register the fastest growth at a CAGR of 17.2% from 2026 to 2033, driven by expanding fiber-optic communication networks, increasing 5G deployment, growing hyperscale data center investments, and rising demand for high-speed broadband connectivity. Ongoing digital transformation initiatives and network modernization programs are significantly contributing to segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 43.50 Billion

- Expected Market Value (2033): USD 123.41 Billion

- Forecast CAGR (2026–2033): 13.92%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Optoelectronic Market Segmentation

|

Attributes |

Optoelectronic Key Market Insights |

|

Segments Covered |

· By Component Type: Photo Voltaic (PV) Cells, Optocouplers, Image Sensors, Light Emitting Diodes (LED), Laser Diode (LD), Infra-Red Components (IR), Phototransistors, Photodiodes, Photo resistors, Different Visual Indicators, Light Emitters and Detectors, Sensors, Others · By End-User: Aerospace & Defense, Automotive, Consumer Electronics, Information Technology, Healthcare, Residential and Commercial, Industrial, and Others · By Devices: Photodiode, Solar Cells, Light Emitting Diode, Optical Fibers, Laser Diode, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Samsung Electronics Co., Ltd. (South Korea) • OSRAM Opto Semiconductors GmbH (Germany) • Koninklijke Philips N.V. (Netherlands) • Vishay Intertechnology, Inc. (U.S.) • OmniVision Technologies, Inc. (U.S.) • Panasonic Corporation (Japan) • Mouser Electronics, Inc. (U.S.) • STANLEY ELECTRIC CO., LTD. (Japan) • ROHM CO., LTD. (Japan) • Mitsubishi Electric Corporation (Japan) • General Electric Company (U.S.) • Broadcom Inc. (U.S.) • Magneti Marelli S.p.A. (Italy) • Renesas Electronics Corporation (Japan) • Excellence Optoelectronics Inc. (Taiwan) • Sharp Corporation (Japan) • Merck KGaA (Germany) |

|

Market Opportunities |

• Expansion Of 5G Infrastructure And Fiber Optic Communication Networks • Increasing Adoption Of Optoelectronic Components In Electric Vehicles And Autonomous Driving Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Optoelectronic Market Trends

Trend: Increasing Adoption Of High-Speed Optical Communication And Advanced Imaging Technologies

The growing demand for faster data transmission, enhanced connectivity, and high-resolution imaging solutions is accelerating the adoption of optoelectronic technologies across telecommunications, consumer electronics, automotive, and healthcare sectors. Traditional electrical transmission systems face limitations in bandwidth, energy efficiency, and signal integrity, encouraging industries to deploy optical components capable of supporting higher data rates and improved performance. As digital transformation initiatives expand globally, optoelectronic devices are becoming critical components in next-generation communication and sensing infrastructure.

In modern communication networks, manufacturers are integrating optical transceivers, laser diodes, and photodetectors, For instance in 5G base stations and hyperscale data centers, to support growing internet traffic and cloud computing requirements. In consumer electronics, advanced image sensors and LED technologies are increasingly used in smartphones, augmented reality devices, and wearable electronics to improve imaging performance and energy efficiency. The rapid expansion of artificial intelligence, machine vision, and autonomous driving systems is also increasing demand for highly precise sensing and imaging solutions. In addition, healthcare providers continue to adopt optoelectronic technologies in medical imaging and diagnostic equipment due to their accuracy and reliability. Industry deployments during 2025 showed that next-generation optical transceivers supporting 800G data transmission improved network throughput by nearly 40–50% compared with earlier-generation systems in large-scale data center environments.

Optoelectronic Market Dynamics

Key Market Driver: Rising Expansion Of 5G Networks And Data Center Infrastructure

Governments, telecommunications operators, and technology companies worldwide are investing heavily in digital infrastructure to support increasing data consumption, cloud computing, and connected device ecosystems. The deployment of 5G networks and expansion of hyperscale data centers are creating strong demand for optoelectronic components capable of enabling high-speed, low-latency communication and efficient signal transmission.

Industries such as telecommunications, cloud computing, and enterprise networking are increasingly deploying optical communication systems to handle rapidly growing bandwidth requirements. Network providers are actively adopting optical transceivers, For instance in fiber-optic backbone networks and 5G transport systems, to improve transmission efficiency and network reliability. Similarly, major data center operators are expanding the use of high-performance optical modules to support AI workloads and large-scale cloud services. Real-world infrastructure projects across North America and Asia-Pacific during 2024 integrated advanced optical networking equipment that increased transmission capacities by more than 30% while reducing energy consumption per transmitted bit.

Key Restraint/Challenge: High Manufacturing Complexity And Supply Chain Dependence

Optoelectronic devices require highly specialized semiconductor materials, precision fabrication processes, and advanced packaging technologies, making manufacturing complex and capital intensive. Components such as laser diodes, image sensors, and photonic integrated circuits require stringent quality control and sophisticated production facilities, creating barriers for new market entrants and increasing operational costs.

In addition, dependence on specialized raw materials, semiconductor wafers, and global supply chains exposes manufacturers to procurement risks and pricing volatility. Supply disruptions, geopolitical uncertainties, and fluctuations in semiconductor availability can affect production schedules and increase component costs. Limited access to advanced fabrication capabilities further constrains scalability in some regions. Industry assessments during 2024 indicated that lead times for certain advanced optoelectronic components extended by approximately 15–20% in selected markets due to supply chain constraints and strong demand from telecommunications and consumer electronics sectors.

Key Market Opportunity: Growing Integration In Autonomous Vehicles And Smart Consumer Electronics

Modern autonomous vehicles, smart devices, industrial automation systems, and healthcare technologies increasingly rely on optoelectronic components for sensing, communication, imaging, and display applications. Conventional electronic systems often struggle to deliver the speed, precision, and efficiency required by advanced digital applications, creating substantial opportunities for optoelectronic solutions.

Automotive manufacturers are increasingly integrating optoelectronic technologies, For instance LiDAR sensors, infrared cameras, and advanced LED lighting systems, to improve vehicle safety, navigation accuracy, and driver assistance capabilities. In consumer electronics, rising demand for smartphones, wearable devices, augmented reality products, and intelligent imaging systems is accelerating the adoption of high-performance image sensors and display technologies. In addition, advancements in silicon photonics, micro-LED displays, and optical sensing technologies are opening opportunities across healthcare, industrial automation, and AI-powered computing markets in Asia-Pacific and North America. Vehicle testing programs conducted in 2025 demonstrated that next-generation LiDAR systems enhanced object detection accuracy by approximately 20–25% under complex driving conditions, supporting broader deployment of autonomous mobility solutions.

Optoelectronic Market Scope

The market is segmented on the basis of component type, end-user, and devices.

- By Component Type

On the basis of component type, the optoelectronic market is segmented into Photo Voltaic (PV) Cells, Optocouplers, Image Sensors, Light Emitting Diodes (LED), Laser Diode (LD), Infra-Red Components (IR), Phototransistors, Photodiodes, Photoresistors, Different Visual Indicators, Light Emitters and Detectors, Sensors, and Others. The Light Emitting Diodes (LED) segment held the largest market revenue share of approximately 32.7% in 2025, driven by its widespread adoption across general lighting, automotive lighting, display technologies, industrial equipment, and consumer electronics. LEDs are preferred due to their high energy efficiency, long operational life, compact design, and increasing integration into smart lighting and display applications worldwide.

The Image Sensors segment is projected to register the fastest growth at a CAGR of 16.5% from 2026 to 2033, driven by rising demand for smartphone cameras, autonomous vehicle vision systems, medical imaging equipment, and AI-powered machine vision applications. Increasing deployment of advanced CMOS image sensors across consumer and industrial sectors is accelerating segment expansion.

- By End-User

On the basis of end-user, the optoelectronic market is segmented into Aerospace & Defense, Automotive, Consumer Electronics, Information Technology, Healthcare, Residential and Commercial, Industrial, and Others. The Consumer Electronics segment held the largest market revenue share of approximately 36.9% in 2025, driven by extensive utilization of optoelectronic components in smartphones, tablets, wearable devices, smart televisions, gaming systems, and augmented reality products. Continuous innovation in display technologies, imaging systems, and optical sensing solutions is supporting strong demand across the segment.

The Healthcare segment is projected to register the fastest growth at a CAGR of 15.8% from 2026 to 2033, driven by increasing adoption of optoelectronic technologies in medical imaging, diagnostic equipment, patient monitoring devices, and minimally invasive surgical systems. Growing healthcare digitization and demand for precision diagnostics are accelerating segment growth globally.

- By Devices

On the basis of devices, the optoelectronic market is segmented into Photodiode, Solar Cells, Light Emitting Diode, Optical Fibers, Laser Diode, and Others. The Light Emitting Diode segment held the largest market revenue share of approximately 34.4% in 2025, driven by strong demand from lighting, display panels, automotive systems, consumer electronics, and smart city infrastructure projects. The segment continues to benefit from increasing energy-efficiency regulations and the global transition toward sustainable lighting technologies.

The Optical Fibers segment is projected to register the fastest growth at a CAGR of 17.2% from 2026 to 2033, driven by expanding fiber-optic communication networks, increasing 5G deployment, growing hyperscale data center investments, and rising demand for high-speed broadband connectivity. Ongoing digital transformation initiatives and network modernization programs are significantly contributing to segment expansion.

Optoelectronic Market Regional Analysis

North America Optoelectronic Market Insight

North America dominated the optoelectronic market with the largest revenue share of 37.85% in 2025, supported by strong investments in advanced semiconductor technologies, widespread adoption of optical communication systems, and the rapid expansion of hyperscale data centers. The region benefits from a highly developed technology ecosystem, significant R&D spending, and strong demand for optoelectronic components across telecommunications, healthcare, aerospace, and consumer electronics industries. Increasing deployment of AI infrastructure and next-generation networking technologies continues to strengthen market growth across the region.

U.S. Optoelectronic Market Insight

The U.S. optoelectronic market captured the largest revenue share in 2025 within North America, fueled by growing demand for high-speed communication networks, advanced imaging systems, and semiconductor innovation. Technology companies are increasingly investing in optical transceivers, image sensors, laser technologies, and photonic integrated circuits to support cloud computing and artificial intelligence applications. Moreover, the presence of major semiconductor manufacturers, strong defense spending, and increasing adoption of autonomous vehicle technologies are significantly contributing to market expansion.

Europe Optoelectronic Market Insight

The Europe optoelectronic market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing investments in fiber-optic infrastructure, automotive electronics, and industrial automation technologies. The growing adoption of energy-efficient lighting systems, advanced sensing technologies, and smart manufacturing solutions is supporting market development across the region. European industries are increasingly integrating optoelectronic components into automotive, healthcare, and industrial applications to improve operational efficiency and digital connectivity.

U.K. Optoelectronic Market Insight

The U.K. optoelectronic market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in telecommunications infrastructure, data centers, and advanced healthcare technologies. Rising demand for optical communication systems, high-performance imaging devices, and smart electronic solutions is supporting market growth. The country's growing focus on digital transformation and innovation in photonics technologies is expected to further stimulate demand across multiple industries.

Germany Optoelectronic Market Insight

The Germany optoelectronic market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country's strong manufacturing base, advanced automotive sector, and leadership in industrial automation. Germany's emphasis on Industry 4.0 initiatives and smart factory deployment is increasing demand for optical sensors, imaging systems, and laser technologies. The integration of optoelectronic components into electric vehicles and industrial robotics is also becoming increasingly prevalent, supporting long-term market growth.

Asia-Pacific Optoelectronic Market Insight

The Asia-Pacific optoelectronic market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding electronics manufacturing activities, and increasing investments in telecommunications infrastructure. The region's strong position in semiconductor production, coupled with rising demand for smartphones, consumer electronics, and optical communication systems, is accelerating market growth. Furthermore, government initiatives promoting digitalization and advanced manufacturing are encouraging wider adoption of optoelectronic technologies across multiple sectors.

Japan Optoelectronic Market Insight

The Japan optoelectronic market is expected to witness the fastest growth rate from 2026 to 2033 due to the country's advanced electronics industry, strong innovation capabilities, and growing demand for precision sensing technologies. Japanese manufacturers are actively developing high-performance image sensors, optical communication components, and laser technologies for applications across automotive, healthcare, and consumer electronics sectors. Moreover, increasing investments in robotics, automation, and smart manufacturing systems are contributing to market expansion.

China Optoelectronic Market Insight

The China optoelectronic market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's extensive electronics manufacturing ecosystem, large consumer base, and significant investments in semiconductor and telecommunications industries. China remains one of the largest markets for LEDs, image sensors, optical communication equipment, and consumer electronic devices. The expansion of 5G infrastructure, smart city projects, and domestic semiconductor manufacturing capabilities, alongside strong government support for technology development, are key factors propelling the market in China.

Optoelectronic Market Share

The Optoelectronic industry is primarily led by well-established companies, including:

- Samsung Electronics Co., Ltd. (South Korea)

- OSRAM Opto Semiconductors GmbH (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Vishay Intertechnology, Inc. (U.S.)

- OmniVision Technologies, Inc. (U.S.)

- Panasonic Corporation (Japan)

- Mouser Electronics, Inc. (U.S.)

- STANLEY ELECTRIC CO., LTD. (Japan)

- ROHM CO., LTD. (Japan)

- Mitsubishi Electric Corporation (Japan)

- General Electric Company (U.S.)

- Broadcom Inc. (U.S.)

- Magneti Marelli S.p.A. (Italy)

- Renesas Electronics Corporation (Japan)

- Excellence Optoelectronics Inc. (Taiwan)

- Sharp Corporation (Japan)

- Merck KGaA (Germany)

Latest Developments in Optoelectronic Market

- In May 2025, Jenoptik, product launch and facility expansion, introduced a Modular Beam Splitting System designed to increase laser structuring throughput in solar cell manufacturing and simultaneously opened a new micro-optics production facility in Dresden. The development strengthens the company’s semiconductor equipment capabilities, improves manufacturing efficiency, and supports growing demand for advanced photonics solutions, contributing to innovation across the global optoelectronics market.

- In March 2025, Coherent Corp., product launch, unveiled next-generation 400G, 800G, and 1.6T pluggable optical transceivers along with a 2×400G-FR4 Lite silicon-photonics module optimized for AI-driven data centers. The new solutions are intended to enhance network bandwidth, improve data transmission efficiency, and support rapidly expanding cloud and AI infrastructure, accelerating growth in the high-speed optical communications segment.

- In October 2024, Infineon Technologies, acquisition, acquired a semiconductor company specializing in laser technologies to strengthen its optoelectronic product portfolio. The acquisition enhances the company's expertise in laser-based industrial applications, expands technological capabilities, and supports the development of advanced photonic solutions, reinforcing competitive positioning within the global optoelectronics industry.

- In August 2024, Lumentum Holdings, strategic partnership, partnered with a leading telecommunications provider to develop advanced optical networking solutions by combining photonic technologies with large-scale network infrastructure. The collaboration is expected to improve high-speed data transmission capabilities, expand optical networking deployments, and support increasing global demand for next-generation communication systems.

- In June 2023, STMicroelectronics, strategic partnership, signed an agreement with Sanan Optoelectronics to accelerate the development and manufacturing of silicon carbide technologies across China. The partnership aims to strengthen the regional semiconductor ecosystem, increase production capacity for advanced electronic components, and support growing demand from electric vehicles, industrial automation, and power electronics applications.

- In December 2022, Microsoft, acquisition, acquired Lumensity, a company specializing in hollow-core optical fiber technology, to advance next-generation communication infrastructure. The acquisition is expected to improve ultra-high-speed data transmission capabilities, support future optical networking innovations, and contribute to the long-term development of advanced telecommunications and data center technologies worldwide.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Optoelectronic Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Optoelectronic Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Optoelectronic Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.