Global Oral Antidiabetic Drugs Market

Market Size in USD Billion

CAGR :

%

USD

50.64 Billion

USD

64.14 Billion

2025

2033

USD

50.64 Billion

USD

64.14 Billion

2025

2033

| 2026 –2033 | |

| USD 50.64 Billion | |

| USD 64.14 Billion | |

| % | |

|

Oral Antidiabetic Drugs Market Size

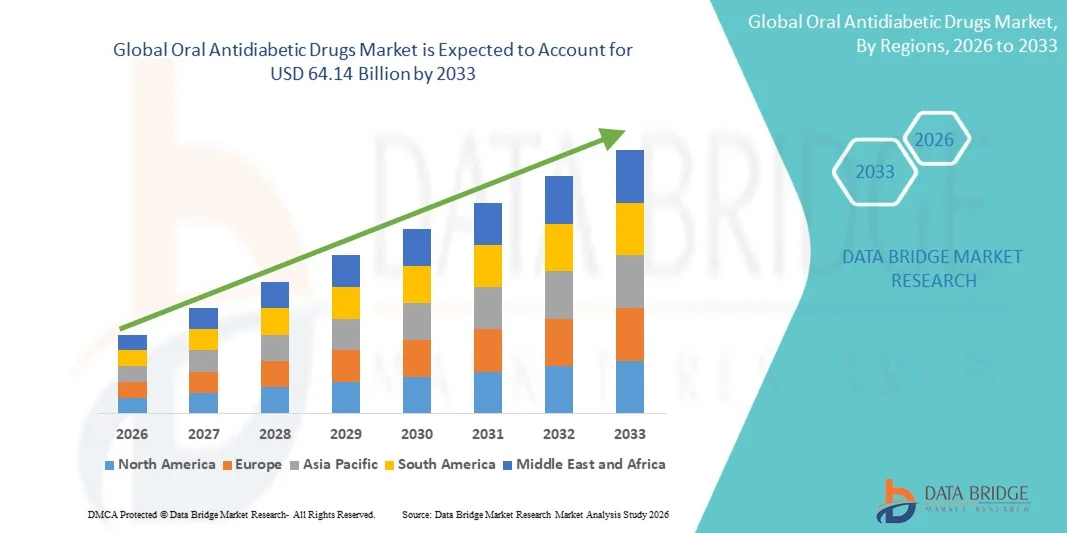

- The global oral antidiabetic drugs market size was valued at USD 50.64 billion in 2025 and is expected to reach USD 64.14 billion by 2033, at a CAGR of 3.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of diabetes, rising awareness regarding disease management, and growing adoption of oral antidiabetic medications for effective glycemic control across patient populations

- Furthermore, continuous advancements in drug formulations, increasing availability of combination therapies, and expanding access to healthcare services are accelerating the uptake of Oral Antidiabetic Drugs solutions, thereby significantly boosting the industry's growth

Oral Antidiabetic Drugs Market Analysis

- Oral antidiabetic drugs, used for the management of type 2 diabetes, are increasingly essential in modern healthcare due to their effectiveness in controlling blood glucose levels and improving long-term patient outcomes

- The escalating demand for oral antidiabetic drugs is primarily fueled by the rising global prevalence of diabetes, increasing awareness regarding disease management, and growing preference for convenient, non-injectable treatment options

- North America dominated the oral antidiabetic drugs market with the largest revenue share of 39.4% in 2025, driven by high diagnosis rates, strong healthcare infrastructure, and widespread adoption of advanced drug therapies, with the U.S. contributing significantly to market growth

- Asia-Pacific is expected to be the fastest growing region in the oral antidiabetic drugs market during the forecast period, registering a CAGR of 12.9%, supported by increasing diabetic population, rising healthcare expenditure, and improving access to medications in emerging economies

- The biguanides segment dominated the largest market revenue share of 38.6% in 2025, driven by metformin’s established efficacy, safety profile, and broad clinical acceptance as first-line therapy for type 2 diabetes

Report Scope and Oral Antidiabetic Drugs Market Segmentation

|

Attributes |

Oral Antidiabetic Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Novo Nordisk (Denmark) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Oral Antidiabetic Drugs Market Trends

“Rising Adoption of Novel and Combination Therapies”

- A significant and accelerating trend in the global oral antidiabetic drugs market is the increasing shift toward novel drug classes and combination therapies aimed at achieving better glycemic control and improved patient outcomes. This trend is driven by the growing need for more effective and safer long-term diabetes management solutions

- For instance, the widespread adoption of sodium-glucose co-transporter-2 (SGLT2) inhibitors and dipeptidyl peptidase-4 (DPP-4) inhibitors has significantly enhanced treatment efficacy compared to traditional monotherapies. Similarly, fixed-dose combination drugs are gaining popularity as they simplify treatment regimens and improve patient adherence

- The development of drugs with additional cardiovascular and renal benefits is further transforming the treatment landscape, as healthcare providers increasingly prioritize therapies that address multiple complications associated with diabetes

- Furthermore, continuous advancements in pharmaceutical research are leading to the introduction of next-generation oral therapies with improved safety profiles and reduced side effects

- The growing emphasis on personalized treatment approaches, where therapies are tailored based on patient profiles, disease progression, and comorbidities, is also shaping market trends

- This shift toward more effective, convenient, and patient-centric treatment solutions is significantly influencing prescribing patterns and expanding the adoption of advanced oral antidiabetic drugs globally

- The demand for innovative oral therapies is rising across both developed and emerging markets, supported by increasing diabetes prevalence and improved access to healthcare services

Oral Antidiabetic Drugs Market Dynamics

Driver

“Rising Prevalence of Diabetes and Increasing Awareness Regarding Disease Management”

- The increasing global prevalence of diabetes, particularly type 2 diabetes, is a major driver propelling the demand for oral antidiabetic drugs. Sedentary lifestyles, unhealthy dietary habits, and rising obesity rates are significantly contributing to the growing patient population

- For instance, large-scale screening programs and public health initiatives in several countries have led to earlier diagnosis and treatment of diabetes, thereby increasing the adoption of oral medications. In addition, awareness campaigns by healthcare organizations are encouraging patients to seek timely medical intervention

- The growing aging population, which is more susceptible to metabolic disorders, further contributes to the rising demand for long-term diabetes management solutions

- Furthermore, improvements in healthcare infrastructure and increased access to medical services are enabling more patients to receive appropriate treatment, particularly in developing regions

- The availability of cost-effective generic drugs, along with favorable reimbursement policies in certain markets, is also supporting widespread adoption

- Increasing physician preference for oral medications as a first-line treatment for type 2 diabetes, due to their ease of administration and patient compliance, is further driving market growth

- Overall, the combination of rising disease burden, enhanced awareness, and improved treatment accessibility is significantly fueling the expansion of the market

Restraint/Challenge

“Side Effects, Treatment Limitations, and Pricing Pressures”

- The presence of side effects and limitations associated with certain oral antidiabetic drugs remains a key challenge for market growth. Some medications may cause gastrointestinal issues, weight gain, or hypoglycemia, which can affect patient adherence and treatment outcomes

- For instance, concerns regarding the long-term safety of certain drug classes have led to cautious prescribing practices among healthcare providers. In addition, variability in patient response to different medications may require frequent treatment adjustments

- The growing competition from alternative treatment options, including injectable therapies and insulin, can also limit the adoption of oral drugs in advanced stages of diabetes

- Furthermore, pricing pressures due to the availability of generic alternatives and strict regulatory policies can impact the profitability of pharmaceutical companies

- Limited access to advanced therapies in low-income regions, along with disparities in healthcare infrastructure, continues to restrict market penetration

- The need for continuous monitoring and combination therapy in some patients may increase the overall cost and complexity of treatment, posing additional challenges

- Addressing these issues through ongoing research, improved drug formulations, and enhanced patient education will be essential to ensure sustained growth and better treatment outcomes in the market

Oral Antidiabetic Drugs Market Scope

The market is segmented on the basis of drug class, end-users, and distribution channel.

• By Drug Class

On the basis of drug class, the Oral Antidiabetic Drugs market is segmented into biguanides, thiazolidinediones, dipeptidyl peptidase IV inhibitors, α-glucosidase inhibitors, insulin secretagogues, amylin analog, sodium-glucose cotransporter-2 (SGLT2) inhibitors, glucagon-like peptide-1 receptor agonists, and others. The biguanides segment dominated the largest market revenue share of 38.6% in 2025, driven by metformin’s established efficacy, safety profile, and broad clinical acceptance as first-line therapy for type 2 diabetes. Biguanides are widely prescribed in hospitals and specialty centers due to their ability to control blood glucose without significant risk of hypoglycemia. Healthcare providers favor biguanides for patients with coexisting conditions like obesity and cardiovascular risk. Continuous R&D and introduction of combination therapies further strengthen market dominance. Patient adherence is high due to oral convenience and affordable pricing. The segment benefits from extensive reimbursement coverage and government diabetes programs. Hospitals and homecare providers frequently stock biguanides due to widespread demand. Growing prevalence of type 2 diabetes globally is supporting expansion. Physician awareness programs and patient education initiatives drive adoption. Availability in multiple dosage forms enhances versatility.

The SGLT2 inhibitors segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, fueled by rising adoption of newer therapies offering cardiovascular and renal benefits beyond glycemic control. SGLT2 inhibitors are increasingly recommended for patients at risk of heart failure or chronic kidney disease. Growing awareness among endocrinologists and diabetic patients is boosting adoption. Hospitals and specialty centers are expanding usage in treatment protocols. Insurance coverage and government support for innovative therapies are accelerating growth. Patient preference for oral agents with additional health benefits contributes to market expansion. Technological advancements in drug formulation are improving efficacy and tolerability. Increasing clinical studies demonstrating long-term benefits are reinforcing adoption. Rising prevalence of obesity and type 2 diabetes globally is supporting segment growth. Integration with combination therapies enhances therapeutic outcomes. Homecare and telemedicine integration further facilitate adoption. Emerging markets are witnessing rapid uptake due to accessibility and awareness.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty centers, and others. The hospitals segment dominated the largest market revenue share of 52.4% in 2025, driven by high patient volume, availability of trained medical staff, and direct access to medications. Hospitals provide comprehensive diabetes management including screening, medication administration, and patient counseling. Multidisciplinary care teams ensure adherence and treatment optimization. Hospitals stock a wide range of antidiabetic drugs, including new drug classes, ensuring continuity of care. Increasing hospitalization for diabetes complications is supporting growth. Government initiatives and insurance reimbursements enhance affordability. Hospitals serve as primary points of treatment for both acute and chronic diabetes cases. High infrastructure and diagnostic capabilities further reinforce market dominance. Frequent clinical visits enable monitoring and adjustments in therapy. Pharmaceutical collaborations and bulk procurement strengthen segment share. Patient trust in hospital care is another key driver.

The homecare segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, driven by rising patient preference for convenient, self-administered oral therapies. Homecare enables continuous monitoring with reduced hospital visits, enhancing patient compliance. Telemedicine integration supports remote consultation and dose adjustments. Increasing availability of oral antidiabetic drugs for self-administration drives adoption. Awareness campaigns for home-based diabetes management are further contributing. Cost savings and convenience make homecare attractive for chronic patients. Growing elderly population and rising diabetes prevalence boost demand. Digital health tools and mobile apps facilitate drug adherence. Pharmacies provide direct-to-home delivery of prescribed medications. Homecare reduces burden on hospitals while ensuring timely treatment. Government and private healthcare programs promote homecare solutions. Patient education on lifestyle management complements pharmacological therapy.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 47.8% in 2025, driven by direct access to medications for inpatients and outpatient prescriptions. Hospital pharmacies offer integrated services including counseling, adherence monitoring, and emergency availability. Bulk procurement by hospitals ensures cost efficiency and continuity of supply. Integration with hospital protocols ensures optimal patient outcomes. Hospitals prioritize stocking both standard and new-generation oral antidiabetic drugs. High patient trust in hospital pharmacies supports consistent demand. Hospitals facilitate prescription fulfillment and monitoring simultaneously. Government support and insurance coverage further reinforce dominance.

The online pharmacy segment is expected to witness the fastest CAGR of 12.1% from 2026 to 2033, driven by increasing digital adoption and convenience of home delivery. Patients prefer online pharmacies for easy refills, access to multiple brands, and competitive pricing. Rising smartphone penetration and e-commerce awareness fuel growth. Telehealth integration allows online prescription management and follow-ups. Online pharmacies enable access to both common and specialty oral antidiabetic drugs. Digital platforms reduce dependency on physical stores and expand reach to remote areas. Government regulations supporting online pharmacy operations enhance credibility. Growing preference for contactless medication delivery post-pandemic boosts adoption. Integration with mobile apps for reminders improves patient adherence.

Oral Antidiabetic Drugs Market Regional Analysis

- North America dominated the oral antidiabetic drugs market with the largest revenue share of 39.4% in 2025, driven by high diagnosis rates, strong healthcare infrastructure, and widespread adoption of advanced drug therapies. The U.S. contributed significantly to overall market growth, supported by robust clinical research, progressive regulatory frameworks, and early adoption of innovative antidiabetic treatments

- Consumers in the region increasingly prefer therapies that offer efficacy, safety, and convenience, contributing to the high uptake of both novel and combination oral antidiabetic drugs

- The presence of leading pharmaceutical companies and well-established distribution networks further reinforces North America’s market dominance

U.S. Oral Antidiabetic Drugs Market Insight

The U.S. oral antidiabetic drugs market captured the largest revenue share within North America in 2025, driven by rising prevalence of type 2 diabetes and increasing awareness of disease management. Physicians are increasingly prescribing advanced oral therapies, including SGLT2 inhibitors, DPP-4 inhibitors, and fixed-dose combination drugs, to improve glycemic control and patient adherence. In addition, robust healthcare infrastructure, high patient affordability, and widespread insurance coverage are fueling market expansion. Efforts to enhance patient education and digital healthcare initiatives are further contributing to growth.

Europe Oral Antidiabetic Drugs Market Insight

The Europe oral antidiabetic drugs market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by increasing prevalence of diabetes, well-developed healthcare systems, and rising patient awareness regarding disease management. Urbanization, the availability of modern healthcare facilities, and growing adoption of advanced oral therapies are fostering market growth. Key countries such as Germany, France, and Italy are witnessing high demand for combination therapies and novel antidiabetic drugs, supported by favorable reimbursement policies.

U.K. Oral Antidiabetic Drugs Market Insight

The U.K. oral antidiabetic drugs market is expected to grow at a notable CAGR during the forecast period, fueled by rising diabetes prevalence and patient preference for convenient, effective oral therapies. Increasing government initiatives promoting early diagnosis and management of diabetes, combined with strong healthcare infrastructure and robust pharmaceutical distribution networks, are driving growth. In addition, the market benefits from high awareness among patients and physicians regarding the advantages of combination therapies.

Germany Oral Antidiabetic Drugs Market Insight

The Germany oral antidiabetic drugs market is anticipated to expand steadily during the forecast period, supported by rising diabetes prevalence, advanced healthcare infrastructure, and growing adoption of innovative oral therapies. Patient preference for treatments with enhanced efficacy, safety, and reduced side effects, alongside favorable reimbursement policies, is boosting market growth. The increasing focus on personalized treatment plans and comprehensive disease management further strengthens market adoption.

Asia-Pacific Oral Antidiabetic Drugs Market Insight

The Asia-Pacific oral antidiabetic drugs market is expected to grow at the fastest CAGR of 12.9% during the forecast period, driven by the increasing diabetic population, rising healthcare expenditure, and improving access to medications in emerging economies such as China, India, and Japan. Rapid urbanization, growing awareness of diabetes management, and government initiatives supporting healthcare infrastructure development are accelerating market adoption. The expansion of pharmaceutical manufacturing and affordable therapy options are also contributing to broader accessibility.

Japan Oral Antidiabetic Drugs Market Insight

The Japan oral antidiabetic drugs market is witnessing steady growth due to the country’s aging population, high diabetes prevalence, and emphasis on early diagnosis and effective management. The demand for patient-friendly oral therapies, including fixed-dose combinations and novel drug classes, is increasing. The integration of advanced healthcare services, digital monitoring, and strong patient adherence programs are supporting market expansion.

China Oral Antidiabetic Drugs Market Insight

The China oral antidiabetic drugs market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the rising diabetic population, increasing healthcare awareness, and growing adoption of advanced oral therapies. Government programs promoting diabetes screening and management, along with improving healthcare infrastructure, are key growth drivers. Affordable therapy options, domestic pharmaceutical production, and rising urban healthcare access are further boosting market adoption across both urban and semi-urban regions.

Oral Antidiabetic Drugs Market Share

The Oral Antidiabetic Drugs industry is primarily led by well-established companies, including:

• Novo Nordisk (Denmark)

• Sanofi (France)

• Eli Lilly and Company (U.S.)

• Boehringer Ingelheim (Germany)

• AstraZeneca (U.K.)

• Merck & Co., Inc. (U.S.)

• Pfizer Inc. (U.S.)

• GlaxoSmithKline (U.K.)

• Mylan N.V. (U.S.)

• Johnson & Johnson (U.S.)

• Sun Pharmaceutical Industries Ltd. (India)

• Bristol-Myers Squibb (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Zhejiang Huahai Pharmaceutical Co., Ltd. (China)

• Abbott Laboratories (U.S.)

• Fresenius Kabi (Germany)

• Biocon Ltd. (India)

• Cipla Limited (India)

• Hetero Drugs Ltd. (India)

• Dr. Reddy’s Laboratories (India)

Latest Developments in Global Oral Antidiabetic Drugs Market

- In May 2023, the U.S. Food and Drug Administration (FDA) approved Brenzavvy (bexagliflozin), developed by TheracosBio, as a new oral SGLT2 inhibitor for the treatment of type 2 diabetes. This approval expanded the class of oral therapies that not only improve glycemic control but also provide cardiovascular and renal benefits, reflecting the evolving therapeutic focus in diabetes care

- In January 2023, Eli Lilly and Company received FDA approval for Mounjaro (tirzepatide) label expansion for type 2 diabetes management, which, although primarily injectable, significantly influenced the oral antidiabetic landscape by accelerating development of next-generation metabolic therapies and combination regimens. This development highlighted the shift toward more effective glucose-lowering agents with additional metabolic benefits

- In April 2024, AstraZeneca announced expanded clinical evidence supporting its oral SGLT2 inhibitor Farxiga (dapagliflozin) for broader cardiometabolic indications, including heart failure and chronic kidney disease. This development strengthened the role of oral antidiabetic drugs beyond glucose control, reinforcing their importance in comprehensive disease management

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.