Global Oral Targeted Oncology Drug Market

Market Size in USD Billion

USD

20.73 Billion

USD

43.47 Billion

2025

2033

USD

20.73 Billion

USD

43.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.73 Billion | |

| USD 43.47 Billion | |

| % | |

|

What is the Oral Targeted Oncology Drug Market Size and Growth Rate?

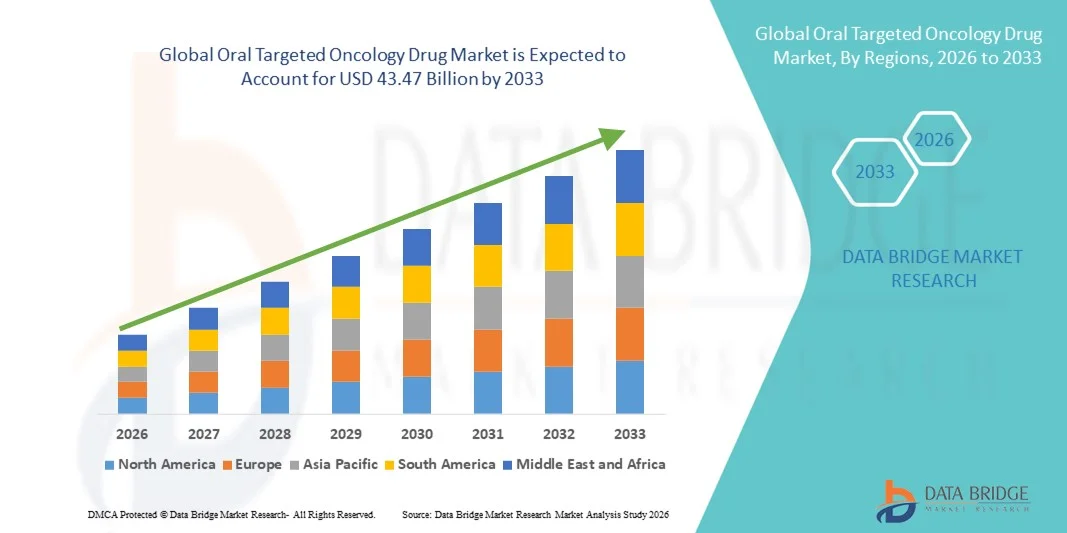

- As per Data Bridge Market Research Analysis the global oral targeted oncology drug market size was valued at USD 20.73 billion in 2025 and is expected to reach USD 43.47 billion by 2033, at a CAGR of 9.70% during the forecast period

- The market growth is primarily driven by the rising prevalence of cancer worldwide and the increasing shift toward precision medicine, with oral targeted therapies offering improved efficacy, better patient compliance, and reduced hospital dependency compared to conventional chemotherapy

- In addition, continuous advancements in molecular diagnostics, expanding approvals for novel oral targeted agents, and growing preference for home-based cancer treatment are positioning oral targeted oncology drugs as a cornerstone of modern cancer care. These combined factors are accelerating adoption and significantly strengthening the overall market growth

Market Size & Forecast

- Global Market Value (2025): USD 20.73 Billion

- Expected Market Value (2033): USD 43.47 Billion

- Forecast CAGR (2026–2033): 9.70%

Oral Targeted Oncology Drug Market Analysis

- Oral targeted oncology drugs, designed to selectively inhibit specific molecular pathways involved in cancer growth and progression, are becoming a critical component of modern cancer treatment across solid tumors and hematological malignancies due to their precision, improved safety profile, and convenient oral administration

- The growing demand for oral targeted oncology drugs is primarily driven by the increasing global cancer burden, rapid adoption of precision medicine, and rising preference for therapies that improve patient compliance while reducing hospital visits and infusion-related complications

- North America dominated the oral targeted oncology drug market with the largest revenue share of 42.5% in 2025, supported by strong oncology R&D infrastructure, early adoption of novel targeted therapies, favorable reimbursement frameworks, and a high rate of regulatory approvals, with the U.S. leading due to robust clinical trial activity and strong presence of major pharmaceutical innovators

- Asia-Pacific is expected to be the fastest-growing region during the forecast period driven by expanding healthcare infrastructure, increasing cancer incidence, improving access to advanced oncology treatments, and growing investments in targeted cancer drug development

- Tyrosine kinase inhibitors segment dominated the oral targeted oncology drug market with a market share of 46.3% in 2025, driven by their broad applicability across multiple cancer types, strong clinical efficacy, and continued approvals for new indications and next-generation molecules

Report Scope and Oral Targeted Oncology Drug Market Segmentation

|

Attributes |

Oral Targeted Oncology Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

What is the Key Trend in the Oral Targeted Oncology Drug Market?

Shift Toward Precision Medicine and Biomarker-Driven Oral Therapies

- A significant and accelerating trend in the global oral targeted oncology drug market is the growing shift toward precision medicine, with therapies designed to target specific genetic mutations and molecular pathways driving cancer progression, thereby improving treatment efficacy and patient outcomes

- For instance, the increasing clinical adoption of oral EGFR, ALK, and CDK4/6 inhibitors across lung and breast cancer indications reflects the market’s movement toward mutation-specific, orally administered targeted therapies supported by companion diagnostics

- Advancements in genomic profiling and next-generation sequencing are enabling oncologists to better identify eligible patient populations, supporting wider use of oral targeted drugs that offer personalized dosing, reduced systemic toxicity, and improved quality of life compared to traditional chemotherapy

- The integration of molecular diagnostics with oral targeted oncology drugs facilitates a more streamlined and individualized treatment approach, allowing clinicians to select therapies based on tumor biology while minimizing unnecessary treatment exposure

- This trend toward highly selective, mechanism-driven oral therapies is reshaping treatment paradigms in oncology, with pharmaceutical companies increasingly prioritizing targeted oral drug development across multiple cancer types and disease stages

- The demand for oral targeted oncology drugs aligned with precision medicine strategies continues to rise across both developed and emerging healthcare markets, as providers and patients increasingly value efficacy, convenience, and personalized cancer care

Oral Targeted Oncology Drug Market Dynamics

Driver

Rising Cancer Burden and Growing Preference for Oral Therapies

- The increasing global incidence of cancer, coupled with a growing preference for convenient and patient-friendly treatment options, is a major driver accelerating demand for oral targeted oncology drugs

- For instance, in recent years, several pharmaceutical companies have expanded indications for existing oral targeted therapies into earlier lines of treatment, supporting broader adoption across solid tumors and hematological malignancies

- As cancer prevalence continues to rise, healthcare systems are increasingly prioritizing therapies that offer sustained efficacy with fewer hospital visits, positioning oral targeted drugs as an attractive alternative to intravenous treatments

- Furthermore, the ability of oral targeted oncology drugs to be administered at home reduces treatment burden on healthcare facilities while improving patient adherence and long-term disease management

- The growing availability of reimbursement support and favorable regulatory pathways for innovative oncology drugs further strengthens market growth, particularly in high-income regions

- Rising investments in oncology drug R&D and strong clinical trial pipelines for oral targeted agents are accelerating innovation and expanding treatment options across cancer indications

- Growing awareness among patients and clinicians regarding the benefits of targeted oral therapies, including improved tolerability and long-term disease control, is further supporting market demand

- Collectively, these factors are driving widespread adoption of oral targeted oncology drugs across hospitals, specialty clinics, and outpatient care settings

Restraint/Challenge

High Treatment Costs and Resistance Development Concerns

- The high cost of oral targeted oncology drugs, driven by complex R&D processes and patent-protected innovations, remains a significant challenge limiting accessibility in price-sensitive markets

- For instance, long-term treatment regimens involving novel targeted agents can impose substantial financial burdens on patients and healthcare systems, particularly in regions with limited insurance coverage

- In addition, the emergence of drug resistance over time presents a clinical challenge, as cancer cells may adapt to targeted therapies, reducing long-term treatment effectiveness

- Addressing resistance often requires combination therapies or next-generation drugs, further increasing treatment complexity and overall costs

- While ongoing research is focused on overcoming resistance mechanisms and improving affordability, disparities in access to advanced oral targeted therapies persist across regions

- Strict regulatory requirements and lengthy approval timelines for oncology drugs can delay market entry of novel oral targeted therapies, impacting commercial growth potential

- Limited availability of advanced molecular diagnostic infrastructure in low- and middle-income regions restricts patient identification and slows adoption of targeted oral oncology treatments

- Overcoming these challenges through expanded generic availability, combination treatment strategies, and supportive reimbursement policies will be critical for sustained market growth

Oral Targeted Oncology Drug Market Scope

The market is segmented on the basis of drug type, indication, molecular target, and distribution channel.

- By Drug Type

On the basis of drug type, the global oral targeted oncology drug market is segmented into tyrosine kinase inhibitors, cyclin-dependent kinase (CDK) inhibitors, PARP inhibitors, proteasome inhibitors, mTOR inhibitors, BCL-2 inhibitors, and other targeted small-molecule drugs. The tyrosine kinase inhibitors segment dominated the market with the largest revenue share of 46.3% in 2025, driven by their extensive clinical use across multiple cancer types, including lung, breast, colorectal, and hematological malignancies. These drugs have benefited from early regulatory approvals and long-term clinical validation, making them a cornerstone of targeted cancer therapy. The availability of multiple generations of TKIs has helped address resistance mechanisms, further strengthening their clinical relevance. Oral administration allows for long-term treatment with improved patient convenience and adherence. Strong physician familiarity and inclusion in standard treatment guidelines continue to support widespread adoption. In addition, ongoing R&D efforts focused on next-generation TKIs are sustaining the segment’s leadership position.

The PARP inhibitors segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing adoption in genetically defined cancers such as BRCA-mutated breast, ovarian, and prostate cancers. Growing awareness and uptake of companion diagnostics are enabling better patient identification for PARP inhibitor therapy. Expanding regulatory approvals into earlier lines of treatment and maintenance therapy are accelerating usage. These drugs also demonstrate favorable safety profiles compared to traditional chemotherapy. Increasing clinical evidence supporting improved progression-free survival is boosting physician confidence. Continued pipeline development and combination strategies with other targeted agents are further driving rapid segment growth.

- By Indication

On the basis of indication, the market is segmented into breast cancer, lung cancer, colorectal cancer, prostate cancer, gastric cancer, hematological malignancies, and other cancers. The lung cancer segment held the largest market revenue share in 2025, supported by the high global prevalence of lung cancer and the widespread adoption of oral targeted therapies as standard-of-care treatments. Molecular testing for EGFR and ALK mutations is now routine, enabling precise patient selection for targeted drugs. The availability of multiple oral inhibitors targeting different resistance mutations has strengthened long-term treatment outcomes. Oral therapy also reduces the burden of frequent hospital visits for patients requiring prolonged treatment. Strong clinical guideline support further reinforces segment dominance. Continuous product launches and indication expansions are sustaining growth in this segment.

The breast cancer segment is anticipated to register the fastest growth during the forecast period, driven by rising use of CDK4/6 and PARP inhibitors in hormone receptor-positive and genetically stratified patients. Expanding approvals for early-stage, adjuvant, and metastatic breast cancer are broadening the treatment population. Improved survival outcomes and manageable safety profiles are increasing physician preference for oral targeted therapies. Growing screening programs and early diagnosis rates are also supporting market expansion. Patient demand for convenient oral treatment options is further accelerating adoption. Ongoing clinical trials evaluating new combinations are expected to maintain strong growth momentum.

- By Molecular Target

On the basis of molecular target, the market is segmented into EGFR inhibitors, HER2 inhibitors, ALK inhibitors, MEK inhibitors, mTOR pathway inhibitors, and other targets. The EGFR inhibitors segment dominated the market in 2025, owing to their extensive use in non-small cell lung cancer and strong alignment with molecular diagnostic practices. High prevalence of EGFR mutations in certain patient populations has driven sustained demand for these therapies. Multiple generations of EGFR inhibitors have improved efficacy while reducing adverse effects. Strong clinical evidence and guideline recommendations support long-term use. Oral dosing enables continuous treatment and improved patient compliance. Favorable reimbursement policies in major markets further reinforce segment leadership.

The HER2 inhibitors segment is expected to witness the fastest CAGR from 2026 to 2033, driven by expanding applications in breast and gastric cancers. Emerging recognition of HER2-low and HER2-mutant patient populations is significantly increasing the addressable market. Advances in molecular diagnostics are improving patient identification and treatment precision. Growing clinical validation of oral HER2-targeted agents is accelerating physician adoption. These therapies also offer improved convenience compared to injectable alternatives. Continued research into novel HER2 inhibitors is expected to sustain high growth rates.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and specialty pharmacies. The hospital pharmacies segment accounted for the largest market revenue share in 2025, as most oral targeted oncology drugs are initiated and monitored within hospital and oncology center settings. These pharmacies play a critical role in therapy initiation, dose management, and patient education. Close coordination with oncologists ensures proper treatment monitoring and adverse event management. Hospital pharmacies are often the first point of access for newly approved oncology drugs. Their involvement in clinical trials further strengthens their dominance. Established infrastructure and reimbursement integration also support continued leadership.

The specialty pharmacies segment is expected to grow at the fastest rate during the forecast period, driven by the increasing complexity of oral oncology therapies. Specialty pharmacies provide tailored services such as adherence monitoring, reimbursement support, and patient counseling. Long-term oral cancer treatments require ongoing support, which specialty pharmacies are well equipped to deliver. Growing emphasis on value-based care is increasing reliance on these distribution channels. Improved logistics and cold-chain capabilities further enhance their role. As personalized oncology treatments expand, specialty pharmacies are expected to gain greater market importance.

Oral Targeted Oncology Drug Market Regional Analysis

- North America dominated the oral targeted oncology drug market with the largest revenue share of 42.5% in 2025, supported by strong oncology R&D infrastructure, early adoption of novel targeted therapies, favorable reimbursement frameworks, and a high rate of regulatory approvals, with the U.S. leading due to robust clinical trial activity and strong presence of major pharmaceutical innovators

- Healthcare providers in the region place strong emphasis on molecular diagnostics, personalized treatment approaches, and the use of oral targeted drugs that improve patient adherence while reducing hospitalization and infusion-related burdens

- This widespread adoption is further supported by robust reimbursement frameworks, high healthcare spending, and the presence of leading pharmaceutical innovators and clinical research centers, establishing oral targeted oncology drugs as a preferred treatment option across both solid tumors and hematological malignancies

U.S. Oral Targeted Oncology Drug Market Insight

The U.S. oral targeted oncology drug market captured the largest revenue share within North America in 2025, fueled by the high prevalence of cancer, strong adoption of precision medicine, and rapid uptake of novel oral targeted therapies. Healthcare providers increasingly prioritize personalized, mutation-specific treatments that improve clinical outcomes and patient quality of life. The widespread availability of advanced molecular diagnostics and companion testing strongly supports targeted drug utilization. Moreover, favorable reimbursement policies and early regulatory approvals accelerate market penetration. The presence of leading pharmaceutical companies and extensive clinical trial activity further propels market growth. As oral therapies reduce hospital visits and infusion burdens, their adoption continues to expand across oncology care settings.

Europe Oral Targeted Oncology Drug Market Insight

The Europe oral targeted oncology drug market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing cancer incidence and strong emphasis on personalized healthcare. Stringent clinical guidelines and growing adoption of molecular diagnostics are fostering demand for targeted oral therapies. European healthcare systems increasingly favor treatments that improve long-term disease management while reducing inpatient care costs. The region is witnessing rising use of oral targeted drugs across breast, lung, and hematological cancers. Growth is supported by expanding oncology research initiatives and cross-border clinical collaborations. Adoption is increasing across hospitals, specialty clinics, and outpatient oncology centers.

U.K. Oral Targeted Oncology Drug Market Insight

The U.K. oral targeted oncology drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on precision oncology within the National Health Service (NHS). Rising cancer prevalence and strong adoption of biomarker-driven treatment pathways are supporting market expansion. The U.K. benefits from robust genomic testing programs that enable accurate patient selection for oral targeted therapies. Growing preference for home-based cancer treatment is further boosting demand. In addition, strong academic research and clinical trial participation contribute to early access to innovative therapies. These factors collectively support sustained market growth in the country.

Germany Oral Targeted Oncology Drug Market Insight

The Germany oral targeted oncology drug market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong investment in oncology research. Germany’s emphasis on evidence-based medicine and early adoption of innovative therapies supports widespread use of targeted oral drugs. High utilization of molecular diagnostics enables precise treatment selection across multiple cancer types. The country also benefits from favorable reimbursement mechanisms and strong physician awareness. Growing demand for therapies that reduce hospital stays aligns well with oral oncology drugs. As a result, adoption is increasing across both hospital and outpatient oncology settings.

Asia-Pacific Oral Targeted Oncology Drug Market Insight

The Asia-Pacific oral targeted oncology drug market is poised to grow at the fastest CAGR during the forecast period, driven by rising cancer incidence, expanding healthcare access, and increasing adoption of precision medicine. Countries such as China, Japan, and India are witnessing rapid improvements in diagnostic capabilities and oncology infrastructure. Growing healthcare expenditure and government initiatives supporting cancer care are accelerating market growth. Increasing awareness of targeted therapies among clinicians and patients is also boosting adoption. The expansion of local pharmaceutical manufacturing is improving drug availability and affordability. These factors collectively position Asia-Pacific as the fastest-growing regional market.

Japan Oral Targeted Oncology Drug Market Insight

The Japan oral targeted oncology drug market is gaining momentum due to the country’s advanced healthcare system, strong focus on innovation, and high adoption of precision medicine. Japan places significant emphasis on early cancer diagnosis and targeted treatment approaches. The integration of genomic testing into routine oncology practice supports widespread use of oral targeted therapies. An aging population with rising cancer prevalence further drives demand for effective and convenient treatment options. Oral drugs are particularly valued for their ease of administration and suitability for long-term therapy. These factors continue to support steady market growth in Japan.

India Oral Targeted Oncology Drug Market Insight

The India oral targeted oncology drug market accounted for a significant revenue share in Asia-Pacific in 2025, driven by rapid urbanization, increasing cancer burden, and expanding access to advanced treatments. India is emerging as a key market due to growing adoption of precision oncology in major urban centers. Rising awareness, improving diagnostic infrastructure, and increasing availability of targeted oral therapies are supporting market growth. The expansion of domestic pharmaceutical manufacturing is enhancing affordability and accessibility. Government initiatives aimed at strengthening cancer care infrastructure further support adoption. As a result, oral targeted oncology drugs are gaining traction across hospitals and specialty oncology clinics in India.

Which are the Top Companies in Oral Targeted Oncology Drug Market?

The Oral Targeted Oncology Drug industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Merck & Co., Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Eli Lilly and Company (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Amgen Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- Gilead Sciences, Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Incyte Corporation (U.S.)

- Astellas Pharma Inc. (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

What are the Recent Developments in Global Oral Targeted Oncology Drug Market?

- In September 2025, the U.S. Food and Drug Administration (FDA) approved imlunestrant (Inluriyo), a novel oral selective estrogen receptor degrader (SERD), for the treatment of adult patients with ER-positive, HER2-negative, ESR1-mutated advanced or metastatic breast cancer following progression on endocrine therapy, marking an important oral targeted therapy option in precision breast oncology

- In August 2025, the FDA granted accelerated approval to zongertinib (Hernexeos) an oral HER2 tyrosine kinase inhibitor for adults with unresectable or metastatic non-squamous non-small cell lung cancer (NSCLC) harboring HER2 tyrosine kinase domain activating mutations, expanding precision targeted therapy options in lung cancer

- In July 2025, the U.S. FDA granted accelerated approval to ZEGFROVY® (sunvozertinib), the first targeted oral therapy for adult patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) harboring EGFR exon 20 insertion mutations, addressing a long-standing unmet treatment need with an effective once-daily oral option

- In June 2025, the FDA approved IBTROZI™ (taletrectinib), a next-generation oral ROS1 tyrosine kinase inhibitor (TKI), for adults with locally advanced or metastatic ROS1-positive NSCLC, offering a novel targeted oral option for a genetically defined rare lung cancer subgroup

- In January 2023, the FDA approved elacestrant (Orserdu), an oral targeted estrogen receptor degrader, for the treatment of ER-positive, HER2-negative, ESR1-mutated advanced or metastatic breast cancer a landmark oral targeted therapy that underscored the shift toward mutation-guided treatment approaches

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.