Global Original Equipment Automotive Headliner Market

Market Size in USD Billion

USD

23.77 Billion

USD

34.46 Billion

2025

2033

USD

23.77 Billion

USD

34.46 Billion

2025

2033

| 2026 - 2033 | |

| USD 23.77 Billion | |

| USD 34.46 Billion | |

| % | |

|

Original Equipment Automotive Headliner Market Size

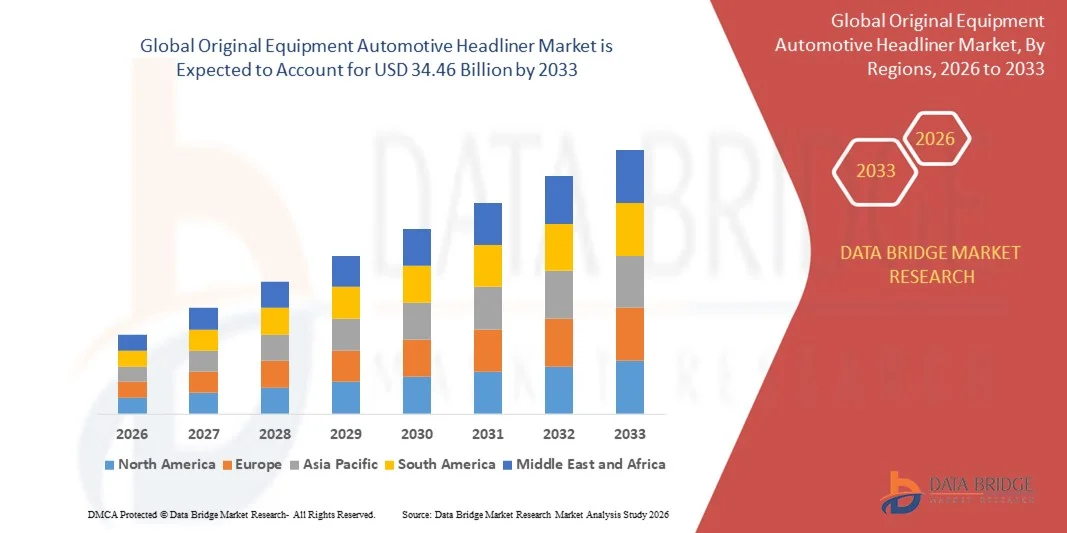

- The global original equipment automotive headliner market size was valued at USD 23.77 billion in 2025 and is expected to reach USD 34.46 billion by 2033, at a CAGR of 4 75% during the forecast period

- The market growth is largely fuelled by the increasing demand for lightweight and high-performance interior materials, rising automotive production, and consumer preference for enhanced cabin comfort and aesthetics

- Growing adoption of eco-friendly and sustainable materials in vehicle interiors is further supporting market expansion

Original Equipment Automotive Headliner Market Analysis

- Increasing focus on vehicle interior comfort and luxury features is prompting automakers to invest in advanced headliner solutions, enhancing passenger experience and cabin aesthetics

- Rising production of electric and premium vehicles globally, along with stricter regulatory standards for interior material safety and sustainability, is fueling demand for high-quality automotive headliners

- North America dominated the original equipment automotive headliner market with the largest revenue share of 38.45% in 2025, driven by increasing demand for lightweight and sustainable interior components, along with growing consumer preference for premium cabin comfort

- Asia-Pacific region is expected to witness the highest growth rate in the global original equipment automotive headliner market, driven by rapid urbanization, increasing vehicle production, rising disposable incomes, and growing adoption of advanced and lightweight automotive interior materials in countries such as China, India, and Japan

- The Built-In segment held the largest market revenue share in 2025, driven by its widespread adoption in passenger vehicles and luxury models for enhanced cabin aesthetics, comfort, and acoustic performance. Built-In headliners are often integrated during vehicle assembly, providing superior NVH (noise, vibration, and harshness) reduction and seamless interior design, making them highly preferred by OEMs

Report Scope and Original Equipment Automotive Headliner Market Segmentation

|

Attributes |

Original Equipment Automotive Headliner Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Original Equipment Automotive Headliner Market Trends

Rise of Lightweight and Sustainable Headliner Materials

- The growing adoption of lightweight and sustainable headliner materials is transforming the automotive interior landscape by reducing vehicle weight, improving fuel efficiency, and meeting stricter emission standards. These materials enhance overall vehicle performance while maintaining comfort and safety, and they contribute to sustainability targets by reducing carbon footprints across the vehicle lifecycle. OEMs are increasingly incorporating bio-based and recyclable components, which further support environmental compliance and corporate responsibility initiatives

- The high demand for eco-friendly and premium-quality interiors is accelerating the use of non-woven fabrics, thermoplastics, and composite materials in headliners. These materials are particularly effective in luxury and electric vehicles, providing superior sound absorption, thermal insulation, and aesthetic appeal, while also meeting consumer expectations for modern and eco-conscious interiors. Adoption is further driven by increasing government regulations and industry standards promoting lightweight, low-emission components

- The affordability, versatility, and ease of installation of modern headliner materials are making them attractive for both OEMs and aftermarket applications. Manufacturers benefit from reduced production costs, shorter assembly times, and compliance with evolving regulatory standards, enabling faster time-to-market. In addition, modular designs and standardized materials allow scalability across multiple vehicle platforms, supporting economies of scale and operational efficiency

- For instance, in 2023, several automotive OEMs in North America and Europe reported improved vehicle weight distribution and enhanced passenger comfort after integrating advanced lightweight headliner materials in new car models. These initiatives also contributed to overall NVH (noise, vibration, and harshness) improvements, higher safety ratings, and positive customer feedback regarding interior quality and aesthetics

- While material innovation is driving adoption, market growth depends on continuous R&D, regulatory compliance, and manufacturing efficiency. Suppliers must focus on high-quality production, durability testing, and localized supply networks to fully capitalize on growing demand, while collaborating with OEMs to optimize material selection for performance, cost, and environmental sustainability

Original Equipment Automotive Headliner Market Dynamics

Driver

Rising Demand for Enhanced Vehicle Comfort and Fuel Efficiency

- Increasing consumer preference for premium interiors, coupled with stringent emission and fuel efficiency regulations, is driving the adoption of advanced headliner materials. These materials help reduce vehicle weight while improving noise, vibration, and harshness (NVH) performance, creating a more comfortable driving experience. OEMs are leveraging these innovations to meet customer expectations for quieter, thermally comfortable, and environmentally responsible vehicles

- Automotive manufacturers are increasingly focusing on lightweight components to optimize fuel consumption in internal combustion vehicles and extend the range in electric vehicles. The growing emphasis on comfort and interior aesthetics supports wider adoption of innovative headliner solutions, while enabling manufacturers to comply with evolving regulatory norms and reduce environmental impact. Integration with other interior components, such as soundproofing and thermal insulation systems, further enhances vehicle efficiency and occupant experience

- Technological advancements in polymer composites, non-woven fabrics, and thermoplastics are enabling OEMs to produce headliners with improved durability, thermal insulation, and acoustic performance. This fuels market expansion across both passenger and commercial vehicles, allowing for multifunctional applications such as integrated lighting, sensors, and infotainment mounts. Advanced manufacturing methods, including automated cutting and bonding, further improve production precision and scalability

- For instance, in 2022, leading OEMs in Europe and Japan implemented lightweight composite headliners in midsize and luxury vehicles, resulting in improved fuel efficiency, reduced material costs, and enhanced cabin comfort. These deployments also showcased better recyclability and reduced environmental footprint, aligning with corporate sustainability goals and regulatory requirements

- While demand for efficient and comfortable interiors is driving market growth, continuous innovation, material standardization, and scalability are essential to sustain adoption and meet evolving consumer expectations. Collaboration between material suppliers, OEMs, and research institutions is critical to accelerate development of next-generation headliner solutions

Restraint/Challenge

High Manufacturing Costs and Complex Production Processes

- The high cost of producing advanced headliner materials, including composites and thermoplastics, limits adoption among smaller OEMs and emerging automotive markets. Cost remains a significant barrier, particularly in developing regions, where price-sensitive segments may opt for conventional materials, reducing penetration of high-performance headliners. Investments in automated and precision manufacturing are often required to meet quality standards, further adding to expenses

- In many regions, limited access to advanced manufacturing technologies and skilled labor hinders the consistent production of high-quality headliners. This reduces supply reliability and may impact vehicle assembly timelines, especially when integrating multifunctional components such as soundproofing layers or embedded sensors. In addition, inadequate maintenance and calibration of production equipment can lead to defects, scrap, and increased operational costs

- Supply chain constraints, including scarcity of specialized raw materials and dependence on global suppliers, further restrict the availability of premium headliner components. Delays in production can affect OEM schedules and market competitiveness, particularly for electric vehicles and luxury segments with tight launch timelines. Fluctuating prices of polymers, composites, and non-woven fabrics also create financial uncertainty for manufacturers

- For instance, in 2023, several automotive plants in Southeast Asia reported challenges in sourcing high-performance composite headliners due to cost and logistical barriers, impacting production efficiency and delivery timelines. These constraints also affected aftermarket parts availability, leading to extended lead times and customer dissatisfaction in certain markets

- While manufacturing processes continue to evolve, addressing cost, supply chain, and technical challenges remains critical. Market stakeholders must focus on cost-effective production, process optimization, and strategic sourcing to unlock long-term growth potential, while investing in training programs and regional production facilities to enhance resilience and scalability

Original Equipment Automotive Headliner Market Scope

The market is segmented on the basis of headliner type, vehicle type, material type, and sales channel.

- By Headliner Type

On the basis of headliner type, the original equipment automotive headliner market is segmented into Built-In, Tilt and Slide, Top Mount, Solar Glass, Pop-up, Tilt, and Panoramic. The Built-In segment held the largest market revenue share in 2025, driven by its widespread adoption in passenger vehicles and luxury models for enhanced cabin aesthetics, comfort, and acoustic performance. Built-In headliners are often integrated during vehicle assembly, providing superior NVH (noise, vibration, and harshness) reduction and seamless interior design, making them highly preferred by OEMs.

The Solar Glass segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for energy-efficient and light-permeable interiors in electric and premium vehicles. Solar Glass headliners provide natural lighting, thermal insulation, and contribute to improved vehicle energy management. Their rising adoption is supported by growing consumer interest in panoramic and sunroof-equipped vehicles, particularly in Europe and Asia-Pacific.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles. The Passenger Vehicles segment held the largest revenue share in 2025 due to the high production volume of cars globally and the emphasis on comfort, aesthetics, and lightweight interiors. Manufacturers are integrating advanced headliner materials to enhance thermal insulation, sound absorption, and fuel efficiency in both mid-size and luxury models.

The Light Commercial Vehicles segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing use of delivery vans, mini-trucks, and utility vehicles in urban logistics and transportation. Lightweight and durable headliner materials are being incorporated to improve driver comfort, reduce vehicle weight, and comply with fuel efficiency standards, especially in regions with growing e-commerce and logistics demand.

- By Material Type

On the basis of material type, the market is segmented into Fabric, Polyester, and Plastic. The Fabric segment held the largest revenue share in 2025, attributed to its wide usage in passenger vehicles for superior aesthetics, NVH reduction, and thermal comfort. Fabric headliners are highly customizable, allowing OEMs to offer various textures, colors, and finishes to meet consumer preferences.

The Polyester segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by its lightweight, durability, and ease of installation. Polyester headliners are increasingly adopted in electric and hybrid vehicles to reduce vehicle weight, improve fuel efficiency, and meet sustainability goals. OEMs are also integrating polyester with sound-absorbing foams and recycled materials to enhance interior performance.

- By Sales Channel

On the basis of sales channel, the market is segmented into Original Equipment Manufacturer (OEM) and After Market. The OEM segment held the largest market share in 2025, driven by the high integration of headliners during vehicle production and the preference for factory-fitted interiors. OEM channels ensure quality, compatibility, and compliance with automotive safety and emission standards.

The After Market segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by rising vehicle customization trends, refurbishment projects, and the growing demand for replacement headliners. Aftermarket solutions provide flexibility, cost-effectiveness, and a range of materials and designs, appealing to consumers looking to upgrade interiors in both passenger and commercial vehicles.

Original Equipment Automotive Headliner Market Regional Analysis

- North America dominated the original equipment automotive headliner market with the largest revenue share of 38.45% in 2025, driven by increasing demand for lightweight and sustainable interior components, along with growing consumer preference for premium cabin comfort

- Consumers in the region highly value the combination of aesthetic appeal, thermal and acoustic insulation, and enhanced safety offered by advanced headliner materials

- This widespread adoption is further supported by high disposable incomes, stringent fuel efficiency regulations, and the growing production of electric and luxury vehicles, establishing innovative headliners as a preferred choice for both passenger and commercial vehicles

U.S. Original Equipment Automotive Headliner Market Insight

The U.S. automotive headliner market captured the largest revenue share in 2025 within North America, fueled by rising vehicle production and demand for lightweight, eco-friendly interior solutions. Manufacturers are increasingly prioritizing headliner materials that enhance passenger comfort, reduce vehicle weight, and improve NVH (noise, vibration, and harshness) performance. The adoption of thermoplastics, composites, and non-woven fabrics, along with integration in luxury and electric vehicles, is significantly contributing to market expansion.

Europe Original Equipment Automotive Headliner Market Insight

The Europe automotive headliner market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent emission standards, rising vehicle production, and increasing consumer preference for premium interiors. Growing urbanization and the expansion of electric and hybrid vehicle segments are fostering the adoption of lightweight, sustainable headliner materials. The market is experiencing substantial growth across passenger cars, light commercial vehicles, and luxury vehicle segments.

U.K. Original Equipment Automotive Headliner Market Insight

The U.K. automotive headliner market is expected to witness robust growth from 2026 to 2033, driven by rising adoption of lightweight materials and the demand for high-quality, sustainable vehicle interiors. Concerns regarding fuel efficiency, emissions compliance, and vehicle aesthetics are encouraging OEMs to integrate advanced headliner solutions. The region’s strong automotive manufacturing infrastructure and growing EV production are expected to further stimulate market growth.

Germany Original Equipment Automotive Headliner Market Insight

The Germany automotive headliner market is expected to witness significant growth from 2026 to 2033, fueled by increasing awareness of eco-friendly and lightweight materials, along with the rising demand for technologically advanced vehicles. Germany’s well-developed automotive ecosystem and focus on innovation, sustainability, and high-performance interiors promote adoption of advanced headliners across passenger and commercial vehicles. Integration with NVH optimization and thermal insulation solutions is increasingly prevalent.

Asia-Pacific Original Equipment Automotive Headliner Market Insight

The Asia-Pacific automotive headliner market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and increasing vehicle production in countries such as China, Japan, and India. The region’s growing automotive manufacturing base, along with government initiatives promoting electric and lightweight vehicles, is driving the adoption of sustainable and high-performance headliner materials. Increased affordability and availability of advanced components are expanding market penetration.

Japan Original Equipment Automotive Headliner Market Insight

The Japan automotive headliner market is expected to witness robust growth from 2026 to 2033 due to the country’s advanced automotive technology, focus on lightweight materials, and high demand for comfortable and efficient vehicle interiors. Japanese manufacturers are increasingly integrating thermoplastics and composite materials to enhance NVH performance and cabin aesthetics. The growing EV segment and aging population’s preference for comfort-friendly vehicles are further driving demand.

China Original Equipment Automotive Headliner Market Insight

The China automotive headliner market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid vehicle production, expansion of the EV segment, and high rates of technological adoption. China is one of the largest automotive markets globally, and advanced headliner materials are increasingly preferred in passenger, commercial, and luxury vehicles. Government policies promoting lightweight and fuel-efficient vehicles, coupled with strong domestic suppliers, are key factors propelling market growth.

Original Equipment Automotive Headliner Market Share

The Original Equipment Automotive Headliner industry is primarily led by well-established companies, including:

• Adient plc (U.K.)

• Atlas Roofing Corporation (U.S.)

• Grupo Antolin (Spain)

• Harodite Industries, LLC (U.S.)

• IAC Group (U.S.)

• Yanfeng Automotive Interiors (China)

• Magna International Inc. (Canada)

• Marelli Corporation (Italy)

• TACHI-S CO., LTD (Japan)

• Tata Sons Private Limited (India)

• Lear Corporation (U.S.)

• SMS Auto Fabrics (India)

• Sage Automotive Interiors (U.S.)

• TOYOTA BOSHOKU CORPORATION (Japan)

• Freudenberg Performance Materials (Germany

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Original Equipment Automotive Headliner Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Original Equipment Automotive Headliner Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Original Equipment Automotive Headliner Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.