Global Oropharyngeal Cancer Market

Market Size in USD Billion

USD

1.51 Billion

USD

2.17 Billion

2025

2033

USD

1.51 Billion

USD

2.17 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.51 Billion | |

| USD 2.17 Billion | |

| % | |

|

What is the Oropharyngeal Cancer Market Size and Overview?

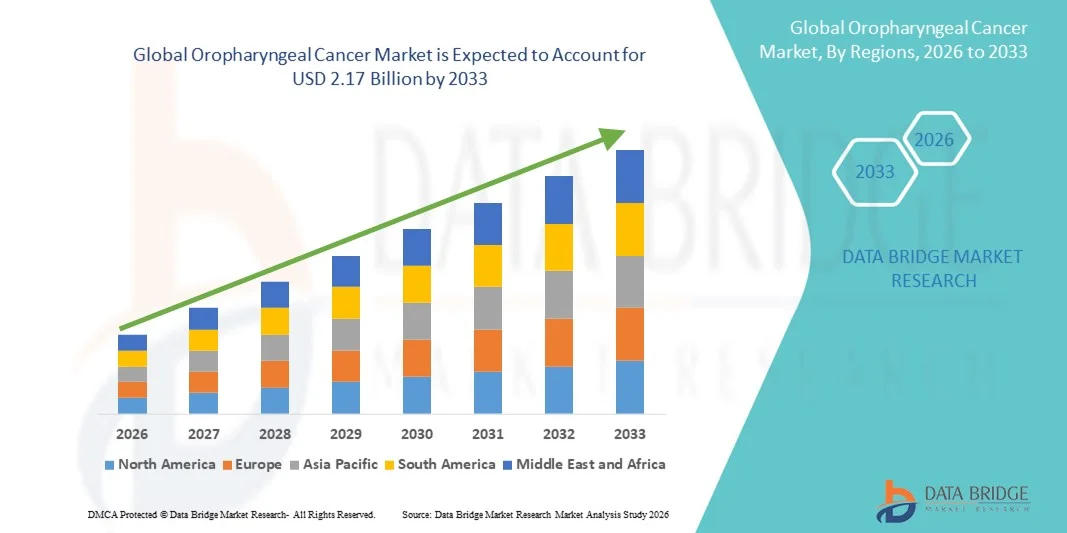

- As per Data Bridge Market Research Analysis the global oropharyngeal cancer market size was valued at USD 1.51 billion in 2025 and is expected to reach USD 2.17 billion by 2033, at a CAGR of 4.65% during the forecast period

- The market growth is largely fueled by the rising incidence of oropharyngeal cancer, particularly HPV-associated cases, along with increasing awareness, early diagnosis initiatives, and advancements in diagnostic imaging and molecular testing technologies across healthcare settings

- Furthermore, growing demand for effective and targeted treatment options including immunotherapy, targeted therapy, and advanced radiation techniques is accelerating the uptake of oropharyngeal cancer therapeutics and management solutions, thereby significantly boosting the overall market growth

Market Size & Forecast

- Global Market Value (2025): USD 1.51 billion

- Expected Market Value (2033): USD 2.17 billion

- Forecast CAGR (2026–2033): 4.65%

Oropharyngeal Cancer Market Analysis

- Oropharyngeal cancer, which affects the middle part of the throat including the tonsils and base of the tongue, is a growing concern in modern oncology due to its strong association with human papillomavirus (HPV) infection, tobacco use, and alcohol consumption. Advances in diagnostics, including imaging and biomarker-based testing, are improving early detection across hospital and specialty care settings

- The increasing demand for effective and personalized treatment options such as immunotherapy, targeted therapy, minimally invasive surgery, and advanced radiation techniques is a key factor driving the growth of the oropharyngeal cancer market, supported by rising healthcare expenditure and expanding oncology care infrastructure

- North America dominated the oropharyngeal cancer market with an estimated revenue share of approximately 38.5% in 2025, driven by a high prevalence of HPV-related cases, strong awareness programs, advanced healthcare systems, and the presence of leading pharmaceutical and biotechnology companies. The U.S. accounted for the majority of regional revenue due to widespread access to novel therapies and clinical trials

- Asia-Pacific is expected to be the fastest-growing region in the oropharyngeal cancer market during the forecast period, with an anticipated CAGR exceeding 7.5%, supported by increasing cancer incidence, improving diagnostic capabilities, expanding oncology treatment centers, and rising healthcare investments in countries such as China, India, and Japan

- The radiation therapy segment dominated the largest market revenue share of 46.8% in 2025, driven by its central role in both early-stage and locally advanced oropharyngeal cancer management

Report Scope and Oropharyngeal Cancer Market Segmentation

Report Scope and Oropharyngeal Cancer Market Segmentation

|

Attributes |

Oropharyngeal Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

|

What is the Key Trend in the Oropharyngeal Cancer Market?

Advancements in Diagnostic and Treatment Approaches for Oropharyngeal Cancer

- A key and accelerating trend in the global oropharyngeal cancer market is the increasing adoption of advanced diagnostic techniques and personalized treatment approaches aimed at improving early detection and patient outcomes

- For instance, the growing use of HPV-specific diagnostic testing and molecular biomarkers is enabling clinicians to differentiate HPV-positive and HPV-negative oropharyngeal cancers, allowing for more targeted treatment strategies and improved prognostic accuracy

- Furthermore, there is a rising trend toward minimally invasive surgical techniques and precision radiotherapy, including transoral robotic surgery (TORS) and intensity-modulated radiation therapy (IMRT), which help reduce treatment-related morbidity while maintaining therapeutic effectiveness

- This shift toward patient-centric and precision-based oncology care is reshaping clinical practice and encouraging healthcare providers to adopt innovative treatment protocols

- The increasing focus on improving survival rates, reducing long-term complications, and enhancing quality of life is expected to drive continued innovation in the oropharyngeal cancer treatment landscape

Oropharyngeal Cancer Market Dynamics

Driver

Rising Incidence of HPV-Associated Oropharyngeal Cancer

- The increasing prevalence of human papillomavirus (HPV)-associated oropharyngeal cancer is a major driver of market growth, particularly in North America and Europe

- For instance, epidemiological studies published in recent years indicate a steady rise in HPV-related oropharyngeal cancer cases, prompting increased screening efforts and demand for effective therapeutic interventions

- Growing awareness of head and neck cancers, along with improved access to diagnostic services, is leading to earlier diagnosis and higher treatment adoption rates

- In addition, increasing investments in oncology research and the expansion of targeted therapies and immunotherapy options are supporting advancements in treatment outcomes

- The expanding aging population, combined with lifestyle risk factors such as tobacco and alcohol consumption in certain regions, further contributes to the rising demand for oropharyngeal cancer diagnostics and treatment solutions

Restraint/Challenge

High Treatment Costs and Limited Access to Advanced Care

- The high cost associated with advanced diagnostic procedures, targeted therapies, and radiation treatments poses a significant challenge to the widespread adoption of comprehensive oropharyngeal cancer care

- For instance, access to advanced treatment options such as robotic-assisted surgery and precision radiotherapy remains limited in low- and middle-income countries due to infrastructure and cost constraints

- Variability in healthcare reimbursement policies across regions can restrict patient access to innovative therapies, delaying treatment initiation and affecting outcomes

- In addition, treatment-related side effects, including swallowing difficulties and speech impairment, may discourage some patients from pursuing aggressive treatment regimens

- Overcoming these challenges through improved healthcare infrastructure, broader insurance coverage, early screening programs, and cost-effective treatment innovations will be essential for sustained growth in the global oropharyngeal cancer market

Oropharyngeal Cancer Market Scope

The market is segmented on the basis of symptoms and treatment.

- By Symptoms

On the basis of symptoms, the Global Oropharyngeal Cancer market is segmented into pain or difficulty with swallowing, trouble opening up your mouth fully or moving your tongue, unexplained weight loss, voice changes that do not go away, ear pain that doesn’t go away, a lump in the back of your throat or mouth, a lump in your neck, coughing up blood, and others. The pain or difficulty with swallowing segment dominated the largest market revenue share of 32.6% in 2025, driven by its high prevalence among patients diagnosed with advanced and locally progressed oropharyngeal cancer. Dysphagia is often one of the earliest and most clinically significant symptoms, prompting patients to seek medical evaluation and diagnostic imaging. This symptom is strongly associated with tumor growth affecting the tonsils, base of the tongue, and pharyngeal walls. Higher diagnosis rates lead to increased utilization of diagnostic procedures, imaging studies, and biopsy services. Hospitals and oncology centers prioritize treatment planning for patients presenting with swallowing difficulties due to quality-of-life implications. The symptom is frequently linked with HPV-associated oropharyngeal cancers, which are rising globally. Clinical awareness campaigns have improved early recognition. Increased referrals to ENT specialists further support dominance. Reimbursement coverage for symptom-driven diagnostics strengthens adoption. The segment benefits from strong physician attention in both developed and emerging markets. Continuous monitoring during treatment further adds to service utilization.

The lump in the neck segment is expected to witness the fastest growth, registering a CAGR of 17.9% from 2026 to 2033, due to its strong association with lymph node metastasis in oropharyngeal cancer patients. A palpable neck mass often indicates disease progression, driving urgent diagnostic intervention and oncology referral. Growing awareness about head and neck cancer symptoms among patients and primary care providers supports earlier detection. Advances in imaging technologies improve diagnostic accuracy for cervical lymphadenopathy. Rising incidence of HPV-positive cancers contributes significantly to this trend. Patients presenting with neck lumps often require multimodal treatment approaches, increasing healthcare utilization. Screening initiatives in high-risk populations boost detection rates. Expansion of oncology services in emerging economies supports growth. Increased patient education encourages earlier reporting of neck abnormalities. Technological integration in diagnostic workflows improves outcomes. Strong linkage with advanced disease management supports higher CAGR.

- By Treatment

On the basis of treatment, the Global Oropharyngeal Cancer market is segmented into radiation therapy, chemotherapy, and others. The radiation therapy segment dominated the largest market revenue share of 46.8% in 2025, driven by its central role in both early-stage and locally advanced oropharyngeal cancer management. Radiation therapy is widely used as a standalone treatment or in combination with chemotherapy, especially in HPV-positive cases. Technological advancements such as intensity-modulated radiation therapy (IMRT) and image-guided radiation therapy (IGRT) enhance precision and reduce damage to surrounding tissues. High adoption across hospitals and specialized cancer centers supports dominance. Radiation therapy offers organ preservation benefits, which is critical in head and neck cancers. Favorable clinical outcomes and improved survival rates strengthen physician preference. Reimbursement support in developed markets further accelerates usage. Increasing availability of advanced radiotherapy equipment in emerging regions contributes to revenue growth. Continuous innovation in treatment planning software improves efficiency. Long treatment durations generate sustained revenue streams. The segment remains integral to standard treatment protocols globally.

The chemotherapy segment is anticipated to witness the fastest growth, with a CAGR of 18.4% from 2026 to 2033, driven by its increasing use in combination regimens and concurrent chemoradiotherapy. Chemotherapy enhances radiation sensitivity, improving treatment effectiveness in advanced-stage disease. Rising adoption of targeted chemotherapeutic agents and platinum-based regimens supports growth. Expanding clinical trials for combination therapies increase utilization. Growing patient volumes in emerging markets contribute significantly to demand. Improved supportive care reduces chemotherapy-related toxicity, improving patient compliance. Integration with immunotherapy and novel agents accelerates treatment evolution. Pharmaceutical R&D investment in oncology fuels pipeline expansion. Government funding for cancer care strengthens access. Increasing diagnosis rates worldwide support higher treatment volumes. Oncologists increasingly favor multimodal treatment strategies. These factors collectively drive strong CAGR growth.

- By Diagnosis

On the basis of diagnosis, the Global Oropharyngeal Cancer market is segmented into X-rays, magnetic resonance imaging (MRI), computed tomography (CT) scans, positron emission tomography (PET) scans, biopsy, endoscopy, and others. The biopsy segment dominated the market with a revenue share of 41.2% in 2025, driven by its critical role in confirming oropharyngeal cancer diagnosis and determining tumor histopathology. Biopsy remains the gold standard for tissue-based diagnosis, providing definitive evidence of cancer type, stage, and HPV status. Hospitals, specialized cancer centers, and diagnostic laboratories widely adopt biopsy procedures due to their high accuracy and reliability. Technological innovations such as fine-needle aspiration, core-needle biopsy, and image-guided biopsy enhance precision and reduce procedural risks. Rising prevalence of head and neck cancers globally supports consistent demand. Pathology laboratories benefit from recurring revenue streams due to multiple tests per patient. Integration with immunohistochemistry and molecular testing provides deeper insights into tumor characteristics. Biopsy results guide personalized treatment planning, including decisions on surgery, radiation, and chemotherapy. Physician preference and clinical guidelines strongly support biopsy as the primary diagnostic tool. Reimbursement support in developed markets facilitates access. Increasing healthcare infrastructure in emerging countries drives broader adoption. The segment’s dominance is reinforced by its indispensable role in accurate, early-stage diagnosis.

The PET scan segment is anticipated to witness the fastest CAGR of 17.6% from 2026 to 2033, driven by its superior ability to detect metabolic activity and early-stage tumor progression. PET scans are increasingly combined with CT or MRI for hybrid imaging, improving staging accuracy and treatment planning. Rising adoption of PET imaging in oncology centers and tertiary care hospitals accelerates growth. Technological advancements, such as PET/CT and PET/MRI scanners, enhance sensitivity and reduce scan times. The growing prevalence of HPV-positive oropharyngeal cancers supports demand for functional imaging to guide therapy. PET scans are critical for monitoring treatment response, detecting recurrence, and planning radiotherapy fields. Integration with advanced software for 3D tumor mapping improves clinical decision-making. Expanding healthcare infrastructure in Asia-Pacific and Latin America increases accessibility. Insurance coverage and reimbursement policies are improving adoption rates. Research institutions are incorporating PET imaging in clinical trials to evaluate novel therapies. Patient preference for non-invasive and highly accurate imaging supports adoption. Increasing awareness among oncologists regarding PET’s prognostic and diagnostic advantages further drives growth.

Oropharyngeal Cancer Market Regional Analysis

- North America dominated the oropharyngeal cancer market with an estimated revenue share of approximately 38.5% in 2025

- Driven by the high prevalence of HPV-related oropharyngeal cancers, strong public awareness initiatives, and the availability of advanced diagnostic and treatment options

- The region benefits from a well-established healthcare infrastructure, widespread access to specialized oncology care, and the presence of leading pharmaceutical and biotechnology companies actively developing novel therapies for head and neck cancers

U.S. Oropharyngeal Cancer Market Insight

The U.S. oropharyngeal cancer market accounted for the majority of revenue share within North America in 2025, supported by widespread access to advanced treatment modalities, including targeted therapies, immunotherapies, and combination treatment approaches. High participation in clinical trials, early adoption of innovative cancer treatments, and strong reimbursement frameworks continue to drive market growth. In addition, robust screening programs and heightened awareness of HPV-associated cancers contribute significantly to early diagnosis and treatment uptake in the country.

Europe Oropharyngeal Cancer Market Insight

The Europe oropharyngeal cancer market is projected to grow at a steady CAGR during the forecast period, supported by increasing cancer incidence, improving early diagnostic practices, and expanding access to multidisciplinary cancer care. Government-led cancer control programs, coupled with rising adoption of advanced radiotherapy and surgical techniques, are supporting market expansion across the region.

U.K. Oropharyngeal Cancer Market Insight

The U.K. oropharyngeal cancer market is expected to witness notable growth during the forecast period, driven by rising awareness of HPV-related cancers, improving screening initiatives, and the availability of comprehensive cancer care services through the public healthcare system. Ongoing research activities and increasing adoption of innovative treatment approaches further support market growth

Germany Oropharyngeal Cancer Market Insight

Germany oropharyngeal cancer market is anticipated to experience considerable growth in the oropharyngeal cancer market, supported by a strong healthcare infrastructure, high diagnostic accuracy, and increasing investments in oncology research. The country’s focus on advanced treatment technologies and personalized medicine approaches is contributing to improved patient outcomes and market expansion.

Asia-Pacific Oropharyngeal Cancer Market Insight

Asia-Pacific oropharyngeal cancer market is expected to be the fastest-growing region in the oropharyngeal cancer market during the forecast period, registering a CAGR exceeding 7.5%. Growth is driven by rising cancer incidence, improving diagnostic capabilities, expanding oncology treatment centers, and increasing healthcare investments across emerging economies such as China, India, and Japan.

Japan Oropharyngeal Cancer Market Insight

The Japan oropharyngeal cancer market is gaining momentum due to advancements in diagnostic technologies, a growing focus on early cancer detection, and increasing adoption of modern treatment modalities. An aging population and rising awareness of head and neck cancers are further contributing to market growth.

China Oropharyngeal Cancer Market Insight

China oropharyngeal cancer market accounted for a significant share of the Asia-Pacific oropharyngeal cancer market in 2025, supported by a large patient population, increasing healthcare expenditure, and rapid expansion of oncology treatment infrastructure. Government initiatives to improve cancer care access and growing adoption of advanced diagnostic and therapeutic technologies are key factors driving market growth in the country.

Which are the Top Companies in Oropharyngeal Cancer Market?

The Oropharyngeal Cancer industry is primarily led by well-established companies, including:

• Merck & Co., Inc. (U.S.)

• Bristol Myers Squibb (U.S.)

• F. Hoffmann-La Roche Ltd. (Switzerland)

• AstraZeneca plc (U.K.)

• Pfizer Inc. (U.S.)

• Novartis AG (Switzerland)

• Johnson & Johnson (U.S.)

• Sanofi S.A. (France)

• Eli Lilly and Company (U.S.)

• Bayer AG (Germany)

• GlaxoSmithKline plc (U.K.)

• AbbVie Inc. (U.S.)

• Amgen Inc. (U.S.)

• Takeda Pharmaceutical Company Limited (Japan)

• Boehringer Ingelheim (Germany)

• Eisai Co., Ltd. (Japan)

• Regeneron Pharmaceuticals, Inc. (U.S.)

• BeiGene, Ltd. (China)

Latest Developments in Global Oropharyngeal Cancer Market

- In January 2023, AstraZeneca initiated a clinical trial studying the combination of its immunotherapy Imfinzi with chemotherapy for recurrent or metastatic oropharyngeal cancer, aiming to improve treatment efficacy by enhancing immune-mediated tumor control alongside standard cytotoxic therapy. This launch reflected growing exploration of immunotherapy combinations for head and neck cancers

- In August 2024, Merck & Co. expanded the clinical use of Keytruda (pembrolizumab) for HPV-positive oropharyngeal cancer based on accumulating evidence of improved tumor response and survival outcomes in advanced cases. Keytruda has been studied extensively and is now a key immunotherapy backbone for oropharyngeal cancer treatment protocols

- In June 2025, the U.S. Food and Drug Administration granted approval for pembrolizumab as a neoadjuvant and adjuvant therapy for resectable locally advanced head and neck squamous cell carcinoma (including oropharyngeal cancer), enabling its use before and after surgery to increase the likelihood of long-term disease control. This was the first perioperative approval of its kind for head and neck cancers

- In June 2025, a novel blood-based HPV whole genome sequencing liquid biopsy assay demonstrated early detection capability for HPV-associated oropharyngeal cancer, identifying circulating tumor HPV DNA up to approximately 7.8 years before clinical diagnosis. This research advancement highlights emerging non-invasive diagnostic potential for earlier cancer detection and monitoring

- In June 2025, PDS Biotechnology hosted a key opinion leader (KOL) event to discuss unmet needs and evolving treatment landscapes for recurrent/metastatic HPV16-positive head and neck squamous cell carcinoma, including oropharyngeal cancer, in context with emerging therapies such as Versamune HPV (PDS0101) in Phase III trials. This event underscored accelerated interest in HPV-targeted immunotherapy combinations that could transform standard care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.