Global Orthopedic Devices Market

Market Size in USD Billion

CAGR :

%

USD

52.75 Billion

USD

85.99 Billion

2024

2032

USD

52.75 Billion

USD

85.99 Billion

2024

2032

| 2025 - 2032 | |

| USD 52.75 Billion | |

| USD 85.99 Billion | |

| % | |

|

Orthopedic Devices Market Size

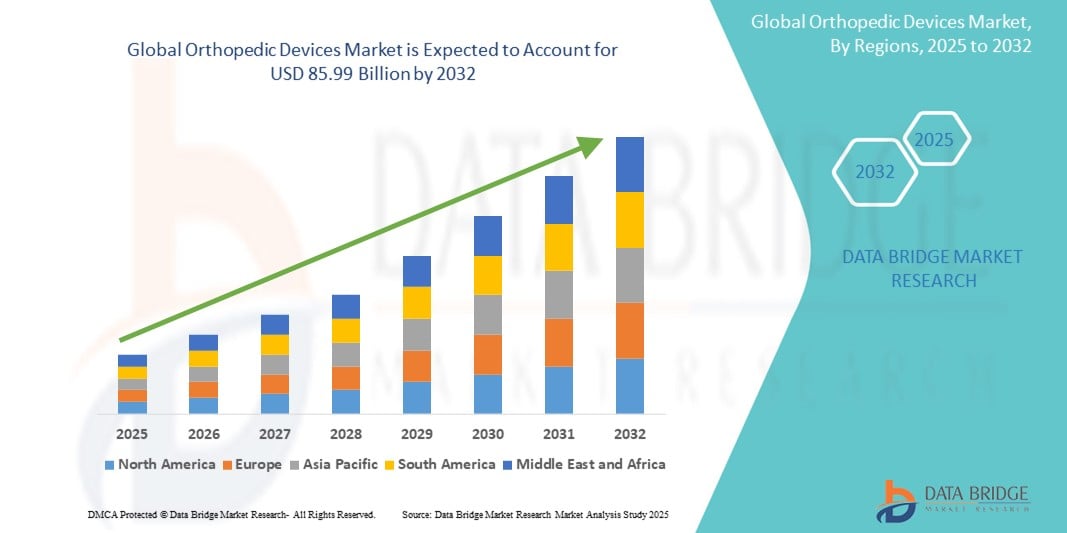

- The global orthopedic devices market size was valued at USD 52.75 billion in 2024 and is expected to reach USD 85.99 billion by 2032, at a CAGR of 6.30% during the forecast period

- This growth is driven by factors such as growing aging population, rising prevalence of orthopedic disorders and injuries, and increasing volumes of joint replacement and spinal surgeries

Orthopedic Devices Market Analysis

- Orthopedic devices are essential tools used in the diagnosis, treatment, and rehabilitation of musculoskeletal conditions, including fractures, joint disorders, spinal deformities, and soft tissue injuries. These devices play a vital role in restoring mobility, improving patient outcomes, and supporting surgical precision across orthopedic procedures

- The orthopedic devices market is witnessing steady growth driven by the increasing prevalence of bone and joint-related disorders, rising geriatric population, advancements in implant technologies, and growing demand for minimally invasive surgical techniques

- North America is expected to dominate the orthopedic devices market with a share of 45.5%, driven by the growing aging population and rising incidence of orthopedic disorders such as osteoarthritis and spinal conditions

- Asia-Pacific is expected to be the fastest growing region in the orthopedic devices market during the forecast period due to increasing healthcare expenditure, growing awareness of musculoskeletal health, and expanding access to medical care

- Orthopedic replacements devices segment is expected to dominate the market with a market share of 42.2% due to rising prevalence of joint-related disorders such as osteoarthritis and rheumatoid arthritis, increasing geriatric population globally, and the growing number of hip and knee replacement procedures driven by improved surgical techniques and implant technologies

Report Scope and Orthopedic Devices Market Segmentation

|

Attributes |

Orthopedic Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Orthopedic Devices Market Trends

“Increasing Prevalence of Musculoskeletal Disorders”

- One prominent trend in the global orthopedic devices market is the increasing prevalence of musculoskeletal disorders

- This trend is driven by the growing aging population, an increase in sedentary lifestyles, and higher rates of bone and joint-related conditions such as osteoarthritis, osteoporosis, and sports injuries

- For instance, countries such as the U.S. and Japan are seeing a rise in joint replacement surgeries, while emerging markets such as India and China are experiencing higher demand for orthopedic solutions due to improving healthcare access and rising awareness

- The demand for orthopedic devices is particularly strong in both developed regions, where healthcare systems are well-established, and in emerging markets, where healthcare infrastructure is rapidly advancing

- As musculoskeletal disorders become more prevalent, the market for orthopedic devices is expected to grow significantly, with continued innovations in implant materials, surgical techniques, and post-surgery rehabilitation solutions enhancing treatment options

Orthopedic Devices Market Dynamics

Driver

“Increasing Sports Injuries”

- The rising incidence of sports injuries is a significant driver for the orthopedic devices market, as athletes and active individuals require advanced orthopedic solutions for the treatment and rehabilitation of bone fractures, ligament tears, and joint injuries

- This demand is accelerating worldwide, particularly with the growing participation in sports and physical activities, coupled with a greater focus on improving athletic performance and recovery

- As sports injuries become more prevalent, the emphasis is shifting toward developing more durable, high-performance implants and devices that support faster recovery and improved mobility for athletes

- Manufacturers are responding by innovating in advanced materials, such as bioresorbable implants and smart orthopedic devices, designed to enhance recovery times and prevent complications

- In addition, the increasing adoption of minimally invasive surgeries and the demand for customizable orthopedic solutions are further fueling market growth

For instance,

- Companies such as DePuy Synthes offer a range of orthopedic solutions specifically designed for sports-related injuries, including joint reconstruction and fracture fixation devices

- Zimmer Biomet develops specialized implants and tools for sports medicine, focusing on improving patient outcomes for athletes of all levels

- As sports participation continues to grow globally, the orthopedic devices market is expected to see sustained demand, with innovations in treatment options and surgical techniques driving market expansion

Opportunity

“Rising Patient Preference for Minimally Invasive Procedures”

- The growing preference for minimally invasive procedures presents a significant opportunity for the orthopedic devices market, as patients seek less invasive alternatives for joint replacement, spinal surgery, and fracture fixation

- Orthopedic device manufacturers are capitalizing on this shift by developing advanced implants and surgical tools that support minimally invasive techniques, offering benefits such as smaller incisions, faster recovery times, and reduced risk of complications.

- This opportunity aligns with the broader trend of improving surgical outcomes and patient experiences, as healthcare providers increasingly adopt technologies that enhance precision and reduce recovery times

For instance,

- Companies such as Stryker and Johnson & Johnson are leading innovations in robotic-assisted surgery systems and minimally invasive joint replacement implants

- Zimmer Biomet offers a range of specialized devices for minimally invasive spinal procedures, improving patient recovery and satisfaction

- As patient demand for minimally invasive surgeries continues to rise, especially in developed markets, the orthopedic devices market is well-positioned to benefit from this trend by offering innovative solutions that meet the growing demand for less invasive, more efficient treatment options

Restraint/Challenge

“High Cost of Orthopedic Devices”

- The high cost of orthopedic devices presents a significant challenge for the orthopedic devices market, as manufacturers face pressure to balance advanced technology, high-quality materials, and competitive pricing while maintaining profitability

- The need for advanced implants, such as custom-designed joint replacements and spinal devices, requires complex manufacturing processes, which can drive up production costs and limit accessibility for some patient groups

- The rising costs of materials, regulatory compliance, and research and development efforts to ensure device safety and efficacy can make it difficult to offer affordable solutions, particularly in emerging markets with lower healthcare budgets

For instance,

- The cost of advanced spinal implants and robotic-assisted surgery systems can be prohibitively high, limiting their adoption in certain regions or healthcare settings

- Without addressing these challenges through innovations in cost-effective manufacturing techniques, materials sourcing, and economies of scale, the high cost of orthopedic devices may restrict market growth and limit patient access to cutting-edge treatments

Orthopedic Devices Market Scope

The market is segmented on the basis of products, site, application, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Products |

|

|

By Site |

|

|

By Application |

|

|

By End User

|

|

In 2025, the orthopedic replacements devices is projected to dominate the market with a largest share in products segment

The orthopedic replacements devices segment is expected to dominate the orthopedic devices market with the largest share of 42.2% in 2025 due to rising prevalence of joint-related disorders such as osteoarthritis and rheumatoid arthritis, increasing geriatric population globally, and the growing number of hip and knee replacement procedures driven by improved surgical techniques and implant technologies.

The spine is expected to account for the largest share during the forecast period in site segment

In 2025, the spine segment is expected to dominate the market due to increasing incidence of spinal disorders such as degenerative disc disease and spinal stenosis, rising demand for minimally invasive spine surgeries, and technological advancements in spinal implants and navigation systems that improve surgical outcomes and recovery times.

Orthopedic Devices Market Regional Analysis

“North America Holds the Largest Share in the Orthopedic devices Market”

- North America dominates the orthopedic devices market with a share of 45.5%, driven by the growing aging population and rising incidence of orthopedic disorders such as osteoarthritis and spinal conditions

- U.S. holds a significant share of 93.8% due to its advanced healthcare infrastructure, early adoption of innovative orthopedic implants, and a strong presence of leading orthopedic device manufacturers

- Market strength is further supported by favorable reimbursement policies, increasing volume of joint replacement surgeries, and high healthcare spending

- Continued innovation in orthopedic technologies, including robotic-assisted surgery and 3D-printed implants, coupled with expanding outpatient orthopedic procedures, will help North America maintain its leadership through 2032

“Asia-Pacific is Projected to Register the Highest CAGR in the Orthopedic devices Market”

- Asia-Pacific is expected to witness the highest growth rate in the orthopedic devices market, driven by increasing healthcare expenditure, growing awareness of musculoskeletal health, and expanding access to medical care

- China holds a significant share due to its rapidly aging population, high prevalence of osteoporosis and joint disorders, and surge in local manufacturing of affordable orthopedic devices

- Government-backed R&D programs, infrastructure investments, and medical tourism are further accelerating regional market growth

- With rising demand for minimally invasive orthopedic procedures, stronger distribution networks, and growing penetration of smart implants, Asia-Pacific is poised to be the fastest-growing region through 2032

Orthopedic Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Zimmer Biomet (U.S)

- Smith+Nephew (Germany)

- Medtronic (Ireland)

- Stryker (U.S)

- B. Braun SE (Germany)

- NuVasive, Inc. (U.S)

- Enovis Corporation (U.S)

- Institut Straumann AG (Switzerland)

- OSSTEM IMPLANT CO., LTD. (South Korea)

- Narang Medical Limited (U.S)

- Globus Medical (U.S)

- Arthrex, Inc. (U.S)

- CONMED Corporation (U.S)

- Integra LifeSciences Corporation (U.S)

- RTI Surgical (U.S)

- W. L. Gore & Associates, Inc. (U.S)

- Corin Group (U.S)

- Johnson & Johnson Services, Inc. (U.S)

Latest Developments in Global Orthopedic Devices Market

- In March 2022, Exactech, Inc., a leading manufacturer of innovative orthopedic implants, introduced its Equinoxe Humeral Reconstruction Prosthesis to the European market. This advanced device, designed to address a wide range of proximal humeral bone loss, became available in major markets including Italy, France, Spain, Germany, and Great Britain, enhancing treatment options for patients in these countries

- In October 2020, Medtronic announced the availability of their Adaptix Interbody System in the United States. This system, distinguished as the first guided titanium implant featuring Titan nanoLOCK Surface Technology, significantly bolstered Medtronic’s market credibility and demand. The innovative product has contributed to increased revenue and a strengthened market presence in the region

- In September 2020, Smith & Nephew plc revealed the launch of its REDAPT System for revision total hip arthroplasty (rTHA) in the Chinese market. This introduction has markedly increased the company's sales and demand in the Asia-Pacific area, highlighting the growing acceptance and success of Smith & Nephew’s advanced orthopedic solutions in this significant market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.