Global Orthopedic Trauma Devices Market

Market Size in USD Billion

USD

11.90 Billion

USD

18.71 Billion

2025

2033

USD

11.90 Billion

USD

18.71 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.90 Billion | |

| USD 18.71 Billion | |

| % | |

|

Orthopedic Trauma Devices Market Size

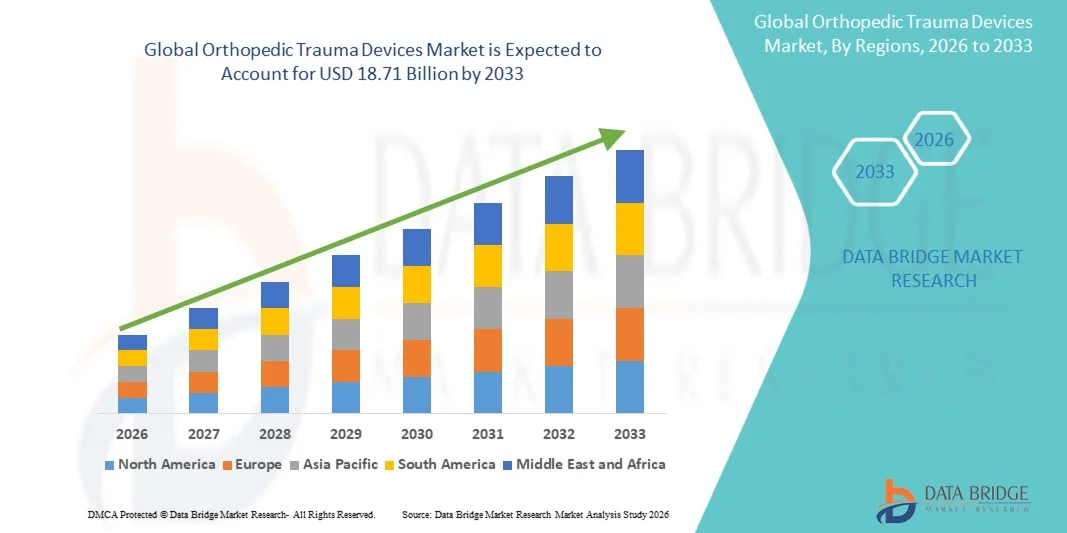

- The global orthopedic trauma devices market size was valued at USD 11.90 billion in 2025 and is expected to reach USD 18.71 billion by 2033, at a CAGR of 5.82% during the forecast period

- The market growth is largely fueled by the rising incidence of fractures due to road traffic accidents, sports injuries, and an aging population, which is increasing the demand for advanced fixation systems and trauma care solutions

- Furthermore, technological advancements in trauma devices, growing healthcare expenditure in emerging economies, and continuous R&D efforts to improve clinical outcomes are driving the adoption of orthopedic trauma solutions globally

Orthopedic Trauma Devices Market Analysis

- Orthopedic trauma devices, including internal and external fixators, are essential for the surgical management of fractures and musculoskeletal injuries, enabling faster recovery, better mobility, and improved clinical outcomes in hospital and specialized trauma care settings

- The rising demand for orthopedic trauma devices is primarily driven by the increasing incidence of fractures due to road traffic accidents, sports injuries, and an aging population, alongside advancements in implant materials and surgical techniques that enhance patient safety and recovery

- North America dominated the orthopedic trauma devices market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong presence of leading device manufacturers, with the U.S. witnessing significant adoption of both internal and external fixators in hospitals and orthopedic centers

- Asia-Pacific is expected to be the fastest-growing region in the orthopedic trauma devices market during the forecast period driven by increasing healthcare access, rising medical tourism, expanding hospital networks, and growing awareness of advanced orthopedic trauma treatments in countries such as China and India

- Internal fixators segment dominated the market with a market share of 62.5% in 2025 due to their versatility in stabilizing complex fractures, widespread clinical adoption, and proven efficacy in trauma fixation procedures

Report Scope and Orthopedic Trauma Devices Market Segmentation

|

Attributes |

Orthopedic Trauma Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Orthopedic Trauma Devices Market Trends

“Advancements in Minimally Invasive Surgical Techniques”

- A significant and accelerating trend in the global orthopedic trauma devices market is the growing adoption of minimally invasive surgical procedures, which reduce recovery times, minimize scarring, and improve overall patient outcomes

- For instance, percutaneous fracture fixation systems allow surgeons to stabilize complex fractures with smaller incisions, resulting in faster patient rehabilitation and shorter hospital stays

- Integration of advanced imaging, navigation systems, and robotic-assisted technologies enhances precision during fracture fixation, reducing surgical errors and improving alignment for optimal healing

- These advancements also enable surgeons to perform complex orthopedic trauma procedures in outpatient or ambulatory surgical centers, expanding access to high-quality care outside traditional hospital settings

- Increasing development of smart implants and sensor-enabled fixators allows real-time monitoring of bone healing, improving post-surgical care and reducing complications

- Adoption of 3D-printed patient-specific implants is gaining traction, offering customized solutions for complex fractures and enhancing surgical accuracy

- This trend towards more precise, less invasive, and technology-enabled orthopedic trauma interventions is reshaping surgical practices and patient expectations globally

- The demand for devices compatible with minimally invasive techniques, including specialized internal and external fixators, is increasing rapidly across both developed and emerging markets, driven by clinical benefits and improved patient satisfaction

Orthopedic Trauma Devices Market Dynamics

Driver

“Increasing Incidence of Fractures and Aging Population”

- The rising prevalence of fractures due to road traffic accidents, sports injuries, and osteoporosis, combined with the aging global population, is a major driver for the orthopedic trauma devices market

- For instance, hospitals are witnessing higher demand for trauma fixation procedures, particularly in geriatric patients prone to hip and spine fractures, driving adoption of advanced fixators and implants

- Orthopedic trauma devices provide improved stabilization, faster recovery, and reduced complications compared to conservative treatment methods, making them a preferred clinical choice

- The expansion of healthcare infrastructure in emerging economies is further enabling access to trauma care solutions, supporting increased adoption of both internal and external fixation systems

- Growing awareness among patients and surgeons regarding the benefits of modern trauma devices, along with rising elective orthopedic procedures, is bolstering the global market demand

- Increasing collaborations between manufacturers and hospitals for device training programs are enhancing surgeon expertise, thereby accelerating adoption of advanced orthopedic trauma solutions

- Government initiatives to improve trauma care services and emergency response infrastructure are driving higher utilization of orthopedic trauma devices across public and private hospitals

Restraint/Challenge

“High Device Costs and Regulatory Hurdles”

- The relatively high cost of advanced orthopedic trauma devices, including bio-absorbable and metallic fixators, poses a challenge for adoption, particularly in price-sensitive markets

- For instance, smaller hospitals or ambulatory surgical centers may delay procurement of advanced internal fixation systems due to budget constraints, limiting market penetration

- Regulatory compliance and lengthy approval processes in multiple countries can slow down the launch of new trauma devices, impacting growth for manufacturers seeking global distribution

- Variations in healthcare reimbursement policies and procedural coverage also create uncertainties for hospitals and trauma centers when investing in high-cost trauma implants

- Limited availability of trained surgeons and specialists in certain regions can reduce adoption rates of complex orthopedic trauma devices, restricting market expansion

- Competition from low-cost, generic, or locally manufactured trauma devices may impact pricing strategies and profit margins for leading global manufacturers

- Overcoming these challenges through cost-effective device development, streamlining regulatory approvals, and expanding insurance coverage will be crucial for sustained market growth

Orthopedic Trauma Devices Market Scope

The market is segmented on the basis of product type, material, end-users, and application.

- By Product Type

On the basis of product type, the orthopedic trauma devices market is segmented into internal fixators and external fixators. The internal fixators segment dominated the market with the largest market revenue share of 62.5% in 2025, driven by their versatility in stabilizing complex fractures, widespread clinical adoption, and proven efficacy in trauma fixation procedures. Internal fixators, such as plates and screws or intramedullary nails, are preferred by surgeons for providing rigid stabilization and facilitating early mobility, which improves patient outcomes. The segment also benefits from continuous R&D leading to advanced designs, minimally invasive implantation techniques, and compatibility with imaging and navigation systems.

The external fixators segment is anticipated to witness the fastest growth rate of 7.8% CAGR from 2026 to 2033, fueled by their increasing use in severe trauma cases, open fractures, and emergency settings. External fixators offer flexibility in adjusting alignment during the healing process, making them ideal for complex and multi-fragment fractures. Growth is also driven by rising adoption in emerging economies, expansion of trauma care centers, and innovations in lightweight and modular designs that enhance patient comfort and clinical outcomes.

- By Material

On the basis of material, the market is segmented into non-absorbable, bio-absorbable, and metallic fixators. The metallic fixators segment dominated the market with a 55% share in 2025, owing to their high strength, durability, and long-established clinical preference among orthopedic surgeons. Metallic fixators, typically made from stainless steel or titanium, provide superior load-bearing capacity and are suitable for a wide range of fracture types, including long bones and load-bearing regions. The segment benefits from continuous innovation in corrosion-resistant coatings and lightweight alloys, which enhance patient comfort and post-operative outcomes.

The bio-absorbable fixators segment is expected to witness the fastest growth rate of 8.5% CAGR from 2026 to 2033, driven by increasing demand for implants that reduce the need for secondary removal surgeries. Bio-absorbable materials, such as polylactic acid (PLA) and polyglycolic acid (PGA), gradually degrade in the body, offering significant advantages for pediatric patients, minimally invasive procedures, and post-operative recovery. Advancements in bio-composite materials and surgical techniques are further accelerating adoption in developed and emerging regions.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, orthopedic and trauma centers, and ambulatory surgical centers. The hospitals segment dominated the market with a 70% revenue share in 2025, driven by the availability of comprehensive surgical infrastructure, advanced imaging and operating theaters, and access to skilled orthopedic surgeons. Hospitals handle the majority of fracture cases, including complex trauma and elective orthopedic procedures, making them the primary consumers of internal and external fixation devices. The segment also benefits from strong reimbursement policies, well-established procurement systems, and ongoing investments in trauma care facilities.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest growth rate of 9.2% CAGR from 2026 to 2033, fueled by the increasing shift toward outpatient and minimally invasive fracture surgeries. ASCs provide cost-effective treatment, faster patient turnover, and reduced hospital stay durations, making them attractive for routine orthopedic trauma procedures. Rising healthcare awareness, increasing insurance coverage for outpatient surgeries, and technological advances in compact surgical instruments are further driving adoption of trauma devices in ASCs.

- By Application

On the basis of application, the market is segmented into hip orthopedic, joint reconstruction, knee orthopedic, spine orthopedic, trauma fixation, craniomaxillofacial orthopedic, dental orthopedic, and others. The trauma fixation segment dominated the market with a 40% share in 2025, due to the high incidence of fractures from accidents, sports injuries, and osteoporosis, which require immediate and effective surgical intervention. Trauma fixation applications encompass a wide range of fracture types, benefiting from advanced internal and external fixators, minimally invasive techniques, and post-operative monitoring devices. Surgeons and hospitals prioritize this segment for its clinical importance and the critical role it plays in reducing long-term disability and improving patient outcomes.

The spine orthopedic segment is expected to witness the fastest growth rate of 8.0% CAGR from 2026 to 2033, driven by rising prevalence of spinal injuries, degenerative disorders, and trauma-related fractures. Increasing demand for spinal fixation systems, interbody devices, and minimally invasive spinal surgery solutions is fueling market expansion. Growth is also supported by the aging population, rising healthcare expenditure in emerging economies, and continuous innovations in spinal implant materials and surgical navigation systems.

Orthopedic Trauma Devices Market Regional Analysis

- North America dominated the orthopedic trauma devices market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and strong presence of leading device manufacturers

- Consumers in the region highly value the convenience, advanced security features, and seamless integration offered by Orthopedic Trauma Devices with other smart devices such as thermostats and lighting systems.

- This widespread adoption is further supported by high disposable incomes, a technologically inclined population, and the growing preference for remote monitoring and control, establishing Orthopedic Trauma Devices as a favored solution for both residential and commercial properties

U.S. Orthopedic Trauma Devices Market Insight

The U.S. orthopedic trauma devices market captured the largest revenue share of 37% in 2025 within North America, driven by the presence of advanced healthcare infrastructure, high healthcare expenditure, and a strong prevalence of road traffic accidents and sports injuries. Hospitals and trauma centers are increasingly adopting advanced internal and external fixators for faster fracture stabilization and improved patient outcomes. The growing emphasis on minimally invasive surgical techniques, coupled with continuous R&D in implant materials and designs, further propels the market. Moreover, collaborations between manufacturers and healthcare providers for surgeon training programs are accelerating the adoption of modern trauma devices.

Europe Orthopedic Trauma Devices Market Insight

The Europe orthopedic trauma devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing incidences of fractures, aging populations, and well-established healthcare systems. Rising investments in trauma care infrastructure and stringent safety regulations are fostering the adoption of advanced fixation systems. Countries such as Germany, France, and Italy are witnessing significant growth across hospitals and orthopedic centers, with both new and renovated facilities incorporating modern internal and external fixators. In addition, the growing preference for minimally invasive procedures is enhancing demand for technologically advanced implants and instruments.

U.K. Orthopedic Trauma Devices Market Insight

The U.K. orthopedic trauma devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing fracture cases and the rising geriatric population. Hospitals and orthopedic centers are increasingly adopting internal and external fixation devices to improve patient recovery and reduce post-operative complications. The U.K.’s focus on modernizing trauma care infrastructure, along with growing awareness of advanced treatment options, is expected to stimulate market growth. Furthermore, government initiatives supporting orthopedic healthcare and training programs for surgeons are encouraging wider adoption of trauma fixation devices.

Germany Orthopedic Trauma Devices Market Insight

The Germany orthopedic trauma devices market is expected to expand at a considerable CAGR during the forecast period, fueled by the rising prevalence of orthopedic injuries, strong healthcare infrastructure, and focus on high-quality surgical care. Germany’s emphasis on innovation and research promotes the development and adoption of advanced metallic and bio-absorbable fixators. Hospitals and trauma centers are increasingly integrating minimally invasive surgical techniques and patient-specific implants into treatment protocols. The growing demand for safe, effective, and durable orthopedic trauma solutions aligns with local consumer and healthcare expectations.

Asia-Pacific Orthopedic Trauma Devices Market Insight

The Asia-Pacific orthopedic trauma devices market is poised to grow at the fastest CAGR of 8.5% from 2026 to 2033, driven by rising incidences of fractures, growing hospital infrastructure, and increasing awareness of advanced orthopedic care. Countries such as China, India, and Japan are witnessing rapid adoption of both internal and external fixators in hospitals, orthopedic centers, and ambulatory surgical facilities. Government initiatives promoting healthcare accessibility, coupled with expanding medical tourism, are boosting market growth. Furthermore, the availability of cost-effective trauma devices and rising R&D investments in the region are enhancing adoption rates among patients and healthcare providers.

Japan Orthopedic Trauma Devices Market Insight

The Japan orthopedic trauma devices market is gaining momentum due to the country’s aging population, increasing orthopedic injury cases, and high standards of healthcare delivery. Hospitals and trauma centers are increasingly using internal fixation devices and minimally invasive systems to improve surgical outcomes. The integration of advanced imaging and navigation technologies with trauma fixation devices is fueling growth. In addition, Japan’s strong emphasis on patient safety and rapid adoption of medical innovations is supporting the expansion of orthopedic trauma solutions across both residential and commercial healthcare settings.

India Orthopedic Trauma Devices Market Insight

The India orthopedic trauma devices market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising fracture incidences, expanding healthcare infrastructure, and increasing awareness of advanced trauma care. Hospitals and orthopedic centers are adopting both internal and external fixators to improve clinical outcomes and reduce recovery times. The push towards affordable healthcare, combined with growing medical tourism and domestic manufacturing of trauma devices, is further propelling market growth. Moreover, the increasing number of trauma care facilities in urban and semi-urban regions is driving higher adoption of modern orthopedic implants.

Orthopedic Trauma Devices Market Share

The Orthopedic Trauma Devices industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Smith & Nephew (U.K.)

- B. Braun SE (Germany)

- CONMED Corporation (U.S.)

- Citieffe s.r.l. (Italy)

- Acumed LLC (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Orthofix Holdings Inc. (U.S.)

- Biotek (Italy)

- Wright Medical Group N.V. (U.S./Netherlands)

- Invibio Ltd (U.K.)

- Auxein Medical (India)

- Medtronic (Ireland)

- NuVasive Inc (U.S.)

- OsteoMed (U.S.)

- Globus Medical (U.S.)

- Medartis AG (Switzerland)

What are the Recent Developments in Orthopedic Trauma Devices Market?

- In February 2026, Stryker announced the launch of its T2 Alpha Humerus Nailing System, a new trauma fixation solution designed to streamline surgical workflow and improve care for complex humeral fractures, offering surgeons a unified platform for consistent, high‑quality treatment

- In October 2025, Stryker revealed it would feature an expanding trauma portfolio at the Orthopaedic Trauma Association Annual Meeting 2025, showcasing enhanced nailing and plating platforms aimed at improving orthopedic trauma care and outcomes globally

- In September 2025, Stryker launched the Incompass™ Total Ankle System at the American Orthopaedic Foot & Ankle Society (AOFAS) meeting, introducing an advanced implant system that supports improved stabilization and performance in trauma and reconstructive ankle surgery

- In March 2025, Johnson & Johnson MedTech showcased a new era of digital orthopedic innovations at the American Academy of Orthopaedic Surgeons (AAOS) 2025 meeting, with a spotlight on data‑driven technologies and advanced implants across orthopedics, including trauma solutions, to improve surgical precision and efficiency

- In March 2023, Bioretec Ltd. received FDA Breakthrough Device designation and market authorization in the U.S. for its RemeOs™ trauma screws, enabling the company to bring its innovative bioresorbable trauma fixation product to clinical use for ankle fractures, marking a significant regulatory milestone in the orthopedic trauma segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.