Global Osteomyelitis Drugs Market

Market Size in USD Billion

USD

1.74 Billion

USD

2.96 Billion

2025

2033

USD

1.74 Billion

USD

2.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.74 Billion | |

| USD 2.96 Billion | |

| % | |

|

Osteomyelitis Drugs Market Overview

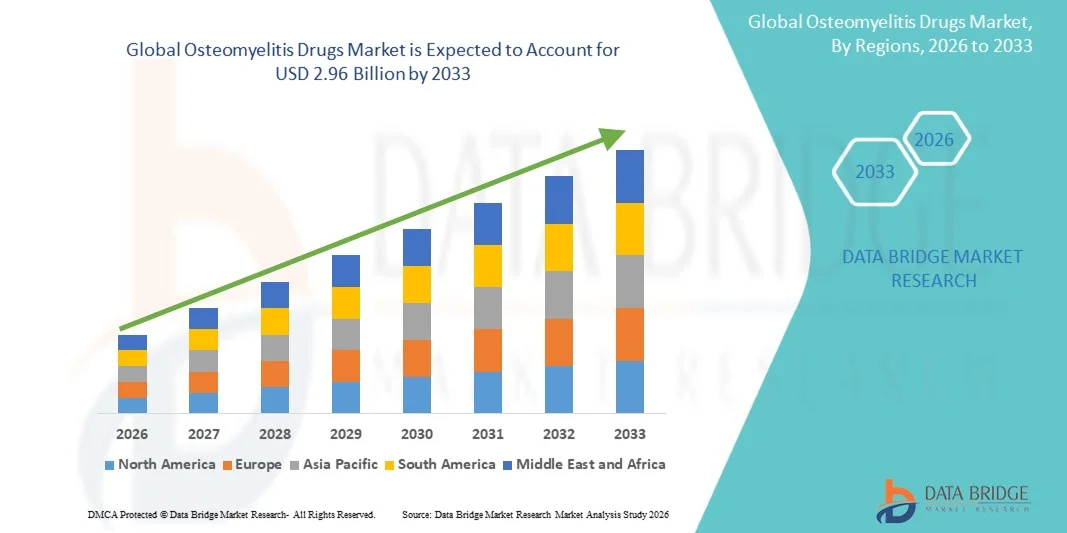

The Osteomyelitis Drugs Market was valued at USD 1.74 billion in 2025 and is projected to reach USD 2.96 billion by 2033, growing at a CAGR of 6.90% from 2026 to 2033. The market is witnessing steady growth driven by the increasing prevalence of bone infections, rising incidence of diabetes-related foot infections and orthopedic surgeries, and growing demand for targeted antimicrobial therapies.

The expanding burden of chronic diseases, aging populations, and trauma-related bone injuries worldwide, combined with improved diagnostic capabilities, is encouraging healthcare providers to adopt advanced treatment approaches for osteomyelitis management. Broad-spectrum antibiotics, combination antimicrobial regimens, and long-duration intravenous and oral therapies remain the cornerstone of treatment, while ongoing research into novel anti-infective agents and drug delivery systems is improving clinical outcomes and reducing recurrence rates across both acute and chronic osteomyelitis cases.

Key Market Trends & Insights

- North America dominated the Osteomyelitis Drugs Market with the largest revenue share of 38.26% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, and widespread availability of antimicrobial therapies.

- The Chronic Osteomyelitis segment led the market with a 44.83% share in 2025, driven by its high prevalence, recurrent nature, and requirement for prolonged antibiotic therapy.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.1% from 2026 to 2033, fueled by increasing healthcare expenditure, rising prevalence of diabetes-related infections, and expanding access to hospital care.

- Vertebral Osteomyelitis are the fastest-growing disease type, projected to register a CAGR of 7.1%, reflecting the surge in diagnosis rates and a growing elderly population.

- The Imaging Test segment dominated the diagnosis category with a 39.64% revenue share in 2025, led by its critical role in confirming infection location, severity, and disease progression.

- Medication accounted for 62.48% of the market, preferred by its role as the primary treatment option for both acute and chronic osteomyelitis cases.

- The Oral segment is the fastest-growing route of administration category, with a CAGR of 7.0%, driven by increasing preference for outpatient treatment and long-term disease management.

Market Size & Forecast

- Global Market Value (2025): USD 1.74 Billion

- Expected Market Value (2033): USD 2.96 Billion

- Forecast CAGR (2026–2033): 6.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Osteomyelitis Drugs Market Segmentation

|

Attributes |

Osteomyelitis Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Merck & Co., Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · AbbVie Inc. (U.S.) · Bristol Myers Squibb (U.S.) · Eli Lilly and Company (U.S.) · Gilead Sciences, Inc. (U.S.) · Amgen Inc. (U.S.) · Viatris Inc. (U.S.) · Baxter (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Novartis AG (Switzerland) · Sanofi (France) · AstraZeneca (U.K.) · GSK plc (U.K.) · Bayer AG (Germany) · Boehringer Ingelheim International GmbH (Germany) · Teva Pharmaceutical Industries Ltd. (Israel) · Astellas Pharma Inc. (Japan) · Daiichi Sankyo Company, Limited (Japan) |

|

Market Opportunities |

· Development of long-acting injectable and localized antibiotic delivery systems · Rising incidence of diabetic foot infections · Expansion of novel anti-biofilm and antimicrobial resistance-focused drug pipelines |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Osteomyelitis Drugs Market Trends

Trend: Rising Adoption of Targeted and Combination Antimicrobial Therapies

Healthcare providers are increasingly adopting targeted antibiotic regimens and combination antimicrobial therapies to improve treatment outcomes, minimize recurrence risks, and address complex bone infections caused by resistant pathogens. The growing use of culture-guided treatment approaches enables precise pathogen identification and optimized drug selection. Hospitals and specialty centers are similarly incorporating multidisciplinary infection management programs to treat osteomyelitis through coordinated, evidence-based care pathways, while advances in oral antibiotic formulations and localized drug delivery technologies are improving patient compliance and long-term disease management.

Osteomyelitis Drugs Market Dynamics

Key Market Driver: Increasing Incidence of Diabetes-Associated Bone Infections

The rising prevalence of diabetes and diabetic foot complications has created substantial demand for osteomyelitis drugs that can effectively manage severe bone infections and prevent long-term disability. Healthcare systems, hospitals, and infectious disease specialists are increasingly utilizing advanced antimicrobial therapies as a core component of treatment protocols, reducing hospitalization burdens, improving patient outcomes, and supporting earlier intervention strategies. The growing global burden of chronic wounds and post-surgical infections continues to expand the need for effective osteomyelitis management solutions.

For instance, in January 2024, the International Diabetes Federation reported continued growth in the global diabetic population, reinforcing the importance of therapies addressing diabetes-related bone and soft tissue infections.

Key Restraint/Challenge: Prolonged Treatment Duration and Antimicrobial Resistance Concerns

A significant restraint in the Osteomyelitis Drugs Market is the extended duration of therapy required for effective infection control. Modern treatment protocols often involve weeks or months of intravenous and oral antibiotic administration, creating challenges related to patient adherence, healthcare costs, and monitoring requirements. The burden of treatment is further intensified by the emergence of antimicrobial-resistant organisms and recurrent infections, making disease management increasingly complex for healthcare providers and patients across both developed and emerging markets.

For instance, ongoing reports from the World Health Organization on antimicrobial resistance continue to highlight the growing challenge of treating persistent bacterial infections, including osteomyelitis-causing pathogens.

Key Market Opportunity: Development of Novel Anti-Biofilm and Localized Drug Delivery Therapies

The development of innovative anti-biofilm therapies in osteomyelitis treatment presents a significant market opportunity. Advanced drug delivery systems can provide sustained local antibiotic concentrations, improve infection eradication rates, and support more effective management of chronic bone infections. The introduction of bioactive implants, antibiotic-loaded biomaterials, and next-generation antimicrobial agents is further expanding treatment possibilities, opening growth opportunities across hospitals, orthopedic centers, and specialized infection management facilities worldwide.

For instance, in 2024, multiple clinical and research programs across leading orthopedic and infectious disease institutions advanced investigations into localized antimicrobial delivery technologies designed to improve outcomes in chronic osteomyelitis treatment.

Osteomyelitis Drugs Market Scope

The osteomyelitis drugs market is segmented on the basis of disease type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the Osteomyelitis Drugs Market is segmented into acute osteomyelitis, chronic osteomyelitis, and vertebral osteomyelitis. The Chronic Osteomyelitis segment dominated the market with a 44.83% share in 2025, owing to its high prevalence, recurrent nature, and requirement for prolonged antibiotic therapy. Chronic cases often arise from untreated infections, diabetic foot ulcers, or post-surgical complications, creating sustained demand for treatment. Patients frequently require long-term antimicrobial management and repeated clinical monitoring. The segment generates substantial healthcare expenditure due to extended treatment durations and higher hospitalization rates. Growing incidence of diabetes and orthopedic implant-related infections is further supporting demand. Its complex clinical management continues to make it the leading disease type segment globally.

The Vertebral Osteomyelitis segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing diagnosis rates and a growing elderly population. Rising prevalence of spinal infections associated with bloodstream infections and immunocompromised conditions is accelerating market expansion. Improved imaging technologies and diagnostic awareness are enabling earlier detection. The segment is benefiting from increasing healthcare access and specialized infectious disease management programs. Growing incidence of hospital-acquired infections and invasive procedures is further contributing to demand. Expanding availability of advanced antimicrobial therapies is expected to support future growth.

- By Diagnosis

On the basis of diagnosis, the Osteomyelitis Drugs Market is segmented into blood test, imaging test, bone biopsy, and others. The Imaging Test segment dominated the market with a 39.64% share in 2025 due to its critical role in confirming infection location, severity, and disease progression. MRI, CT scans, and X-rays are routinely used for diagnosis and treatment planning. These technologies provide detailed visualization of affected bone structures and surrounding tissues. Increasing adoption of advanced imaging systems in hospitals is supporting segment growth. Physicians rely heavily on imaging results to determine therapeutic strategies and monitor outcomes. Continuous technological advancements are further strengthening the segment’s market position.

The Bone Biopsy segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing emphasis on pathogen-specific treatment approaches. Bone biopsy remains the gold standard for identifying infectious organisms and guiding targeted antimicrobial therapy. Growing concerns regarding antibiotic resistance are increasing demand for precise diagnostic methods. Healthcare providers are increasingly utilizing biopsy procedures to improve treatment effectiveness and reduce recurrence. Advancements in minimally invasive biopsy techniques are improving patient acceptance. Rising adoption of personalized infection management strategies is further accelerating growth.

- By Treatment

On the basis of treatment, the Osteomyelitis Drugs Market is segmented into surgery, medication, and others. The Medication segment led the market with a 62.48% share in 2025, driven by its role as the primary treatment option for both acute and chronic osteomyelitis cases. Antibiotics remain the foundation of disease management and are extensively prescribed across healthcare settings. Continuous development of broad-spectrum and targeted antimicrobial agents is enhancing treatment outcomes. The segment benefits from growing awareness regarding early infection management. Increased availability of oral and intravenous treatment options is supporting widespread adoption. Its essential role in infection control ensures continued market dominance.

The Surgery segment is anticipated to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, owing to increasing cases of severe and treatment-resistant infections. Surgical procedures are often required to remove infected bone tissue, drain abscesses, and improve treatment success rates. Rising incidence of chronic osteomyelitis and implant-associated infections is driving demand for surgical intervention. Advances in orthopedic surgical techniques are improving patient outcomes and recovery times. Growing adoption of reconstructive procedures and bone grafting solutions is further supporting growth. The segment is also benefiting from increasing investments in specialized orthopedic care.

- By Route of Administration

On the basis of route of administration, the Osteomyelitis Drugs Market is segmented into oral, parenteral, topical, and others. The Parenteral segment dominated the market with a 51.37% share in 2025, supported by the widespread use of intravenous antibiotics in severe osteomyelitis treatment. Parenteral administration enables rapid drug delivery and higher bioavailability, making it suitable for acute infections. Hospitals frequently prefer intravenous therapies during the initial treatment phase. The segment is strongly supported by established clinical treatment guidelines. Growing hospitalization rates for bone infections continue to sustain demand. Its effectiveness in managing complex infections reinforces its leadership position.

The Oral segment is projected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by increasing preference for outpatient treatment and long-term disease management. Oral therapies offer improved patient convenience and reduced hospitalization costs. Advances in oral antibiotic formulations are enhancing treatment efficacy and adherence. Healthcare providers are increasingly transitioning suitable patients from intravenous to oral regimens. The segment benefits from growing emphasis on cost-effective healthcare delivery. Rising patient preference for home-based treatment is further accelerating adoption.

- By End-Users

On the basis of end-users, the Osteomyelitis Drugs Market is segmented into hospitals, specialty clinics, home healthcare, and others. The Hospitals segment accounted for the largest market share of 56.92% in 2025 due to the high volume of osteomyelitis diagnosis, treatment, and surgical procedures performed in hospital settings. Hospitals provide access to multidisciplinary teams, advanced diagnostics, and intravenous treatment facilities. Complex and severe infections often require inpatient care and continuous monitoring. Increasing hospitalization associated with diabetic foot infections is supporting demand. Availability of specialized orthopedic and infectious disease departments further strengthens the segment. Hospitals remain the primary treatment centers for osteomyelitis management globally.

The Home Healthcare segment is expected to be the fastest-growing end-user category at a CAGR of 7.3% from 2026 to 2033, driven by the shift toward outpatient care and home-based antibiotic administration. Advances in portable infusion technologies are enabling effective treatment outside traditional hospital settings. Patients increasingly prefer home healthcare due to convenience and reduced medical expenses. Growing emphasis on minimizing hospital stays is supporting segment expansion. Healthcare providers are adopting home-based treatment programs to improve resource utilization. The segment is gaining momentum as healthcare systems focus on patient-centered care models.

- By Distribution Channel

On the basis of distribution channel, the Osteomyelitis Drugs Market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated the market with a 57.34% share in 2025 owing to the extensive use of intravenous antibiotics and prescription-based treatment protocols. Hospital pharmacies ensure timely access to specialized antimicrobial drugs required for infection management. They play a crucial role in supporting inpatient treatment and post-surgical care. Strong coordination between physicians and hospital pharmacists improves therapeutic outcomes. Increasing hospitalization rates for severe bone infections continue to support segment growth. The segment remains central to osteomyelitis drug distribution worldwide.

The Online Pharmacy segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by rising digital healthcare adoption and increasing demand for convenient medicine procurement. Online platforms provide easy access to prescription medications and home delivery services. Growing internet penetration and expanding e-pharmacy networks are supporting market expansion. Patients undergoing long-term antibiotic therapy increasingly prefer digital purchasing channels. Improved regulatory frameworks in several countries are enhancing consumer confidence. The segment is expected to benefit from the ongoing transformation of healthcare distribution systems.

Osteomyelitis Drugs Market Regional Analysis

North America dominated the Osteomyelitis Drugs Market with the largest revenue share of 38.26% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates, and widespread availability of antimicrobial therapies. The region also benefits from a strong presence of leading pharmaceutical companies, increasing prevalence of diabetes-related foot infections, and well-established reimbursement frameworks. Growing adoption of targeted antibiotic treatments, rising orthopedic surgical procedures, and expanding infectious disease management programs continue to support market growth. Increasing investments in antimicrobial research and improved clinical awareness further strengthen North America’s leadership position in the global market.

U.S. Osteomyelitis Drugs Market Insight

The U.S. osteomyelitis drugs market is witnessing strong growth due to rising prevalence of diabetes-related bone infections, increasing orthopedic surgical procedures, and growing adoption of advanced antimicrobial therapies. The country’s mature healthcare infrastructure, along with strong pharmaceutical innovation and extensive infectious disease management programs, is driving demand across hospitals, specialty clinics, and home healthcare settings. In addition, growing emphasis on early diagnosis, antimicrobial stewardship, and improved patient outcomes is accelerating the adoption of osteomyelitis treatment solutions across the healthcare system.

Europe Osteomyelitis Drugs Market Insight

The Europe osteomyelitis drugs market remains a major contributor to global revenue, driven by strong healthcare systems, technological advancements, and high demand for effective infection management solutions. The widespread use of advanced diagnostic techniques, targeted antimicrobial therapies, and multidisciplinary treatment approaches is supporting market expansion across the region. Increasing investments in infectious disease research, coupled with favorable reimbursement policies and growing awareness regarding bone infection management, continue to enhance the adoption of osteomyelitis drugs throughout Europe.

U.K. Osteomyelitis Drugs Market Insight

The U.K. osteomyelitis drugs market is experiencing steady growth, supported by rising incidence of chronic bone infections, increasing healthcare expenditure, and growing adoption of evidence-based treatment protocols. Increasing investments in advanced diagnostic infrastructure and growing demand for effective, long-term antimicrobial therapies are contributing to market growth. Furthermore, integration of precision diagnostics, antimicrobial stewardship initiatives, and specialized infection management programs is improving treatment outcomes, positioning the U.K. as a key market within the osteomyelitis drugs industry.

Germany Osteomyelitis Drugs Market Insight

The Germany osteomyelitis drugs market is expanding steadily due to the country’s advanced healthcare infrastructure, strong pharmaceutical industry presence, and increasing adoption of innovative infection treatment strategies. Hospitals, specialty clinics, and orthopedic centers are increasingly utilizing advanced antimicrobial therapies for osteomyelitis management and post-surgical infection control. Continuous advancements in diagnostic imaging, targeted antibiotic therapies, and clinical treatment protocols, along with strong government focus on healthcare quality and patient safety, are further driving market growth in Germany.

Asia-Pacific Osteomyelitis Drugs Market Insight

The Asia-Pacific osteomyelitis drugs market is expected to witness rapid growth, driven by increasing healthcare expenditure, rising prevalence of diabetes and trauma-related infections, and expanding healthcare infrastructure across countries such as China, India, and Japan. Growing awareness regarding bone infection management, rising adoption of advanced diagnostic technologies, and increasing demand for accessible and cost-effective treatment options are supporting regional market expansion. In addition, the growing presence of pharmaceutical manufacturing capabilities and improving healthcare access are accelerating osteomyelitis drug adoption across the region.

Japan Osteomyelitis Drugs Market Insight

The Japan osteomyelitis drugs market is witnessing consistent growth due to rising investments in advanced healthcare technologies, increasing prevalence of age-related bone infections, and growing focus on patient safety initiatives. Healthcare providers, research institutions, and pharmaceutical companies are increasingly adopting advanced antimicrobial therapies for infection management, treatment optimization, and clinical care improvement. Moreover, increasing integration of precision medicine approaches and the country’s focus on efficient and high-quality healthcare delivery are further contributing to market growth.

China Osteomyelitis Drugs Market Insight

The China osteomyelitis drugs market is growing rapidly, driven by increasing healthcare modernization, expanding hospital infrastructure, and rising government focus on infection prevention and treatment. Growing adoption of advanced antibiotics and diagnostic technologies across hospitals, specialty clinics, and healthcare networks is significantly boosting market demand. In addition, rising investments in pharmaceutical research, increasing awareness regarding bone infection treatment, and rapid healthcare advancements are positioning China as one of the fastest-growing markets for osteomyelitis drugs globally.

Osteomyelitis Drugs Market Share

The osteomyelitis drugs industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

- Eli Lilly and Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Amgen Inc. (U.S.)

- Viatris Inc. (U.S.)

- Baxter (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Sanofi (France)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

Latest Developments in Osteomyelitis Drugs Market

- In June 2024, Osteal Therapeutics announced the successful closure of a USD 50 million Series D financing round led by Zimmer Biomet to support regulatory approval and commercialization of VT-X7, a novel combination drug-device therapy for orthopedic infections. The funding is expected to accelerate development of advanced treatments targeting bone and joint infections, including osteomyelitis, while expanding therapeutic options for difficult-to-treat musculoskeletal infections

- In September 2024, researchers published findings in the journal Antimicrobial Agents and Chemotherapy demonstrating that a gentamicin- and clindamycin-eluting depot technology successfully eradicated implant-associated osteomyelitis in a preclinical model without requiring systemic antibiotics. The study highlighted the potential of localized antimicrobial delivery systems to improve treatment outcomes and reduce systemic antibiotic exposure in chronic bone infections

- In February 2024, investigators published a comparative clinical study in Infectious Diseases and Therapy evaluating the use of oritavancin versus daptomycin following surgical debridement for osteomyelitis treatment. The research provided additional clinical evidence supporting the use of long-acting antimicrobial therapies in bone infection management and highlighted evolving treatment strategies for reducing hospitalization and improving patient adherence

- In February 2024, Biocomposites announced the launch of two-Phase II clinical trials in the United States evaluating STIMULAN VG, a calcium-matrix antibiotic carrier containing vancomycin and gentamicin. The BLADE-VG2 study specifically focuses on diabetic foot osteomyelitis, aiming to assess the safety and efficacy of localized antibiotic delivery for improving infection control and reducing treatment complications

- In May 2022, BONESUPPORT received U.S. FDA market authorization for CERAMENT G, an antibiotic-eluting bone graft substitute indicated for the treatment of osteomyelitis. The product became the first injectable combination antibiotic bone graft substitute approved in the United States, enabling localized gentamicin delivery while simultaneously supporting bone healing in patients with bone infections

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.