Global Otc Braces Market

Market Size in USD Million

USD

774.70 Million

USD

1,391.97 Million

2025

2033

USD

774.70 Million

USD

1,391.97 Million

2025

2033

| 2026 - 2033 | |

| USD 774.70 Million | |

| USD 1,391.97 Million | |

| % | |

|

Over the Counter (OTC) Braces Market Size

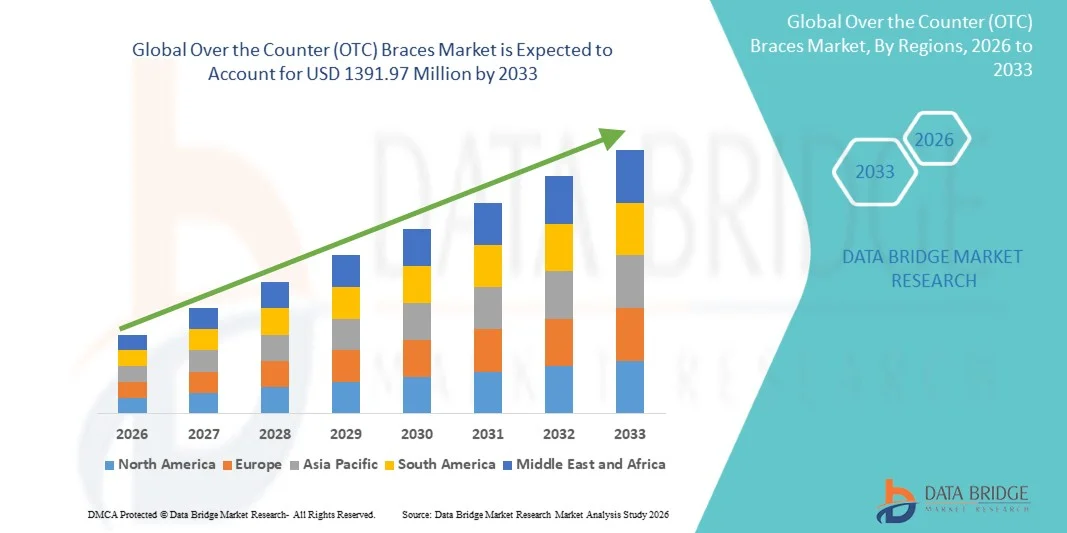

- The global over the counter (OTC) braces market size was valued at USD 774.7 Million in 2025 and is expected to reach USD 1391.97 Million by 2033, at a CAGR of 7.60% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within orthopedic and personal care solutions, leading to increased awareness and usage of OTC braces in both clinical and home settings.

- Furthermore, rising consumer demand for convenient, easy-to-use, and effective musculoskeletal support solutions is establishing OTC braces as a preferred choice for injury prevention, rehabilitation, and pain management. These converging factors are accelerating the uptake of OTC Braces solutions, thereby significantly boosting the industry's growth

Over the Counter (OTC) Braces Market Analysis

- Smart braces, offering easy-to-use orthopedic support for joints and muscles, are increasingly vital components of modern personal care and injury management in both clinical and home settings due to their enhanced comfort, accessibility, and versatility

- The escalating demand for OTC braces is primarily fueled by the widespread adoption of self-care and rehabilitation products, growing awareness of musculoskeletal health, and a rising preference for convenient, non-prescription solutions

- North America dominated the over the counter (OTC) braces market with the largest revenue share of 45.5% in 2025, characterized by advanced healthcare infrastructure, high consumer awareness, and a strong presence of key industry players, with the U.S. experiencing substantial growth in OTC braces adoption, particularly in homecare and sports-related applications, driven by innovations from both established medical brands and startups focusing on ergonomic and smart support designs

- Asia-Pacific is expected to be the fastest growing region in the over the counter (OTC) braces market during the forecast period with a projected CAGR of 12.3%, fueled by increasing urbanization, rising disposable incomes, and growing awareness of preventive and rehabilitative musculoskeletal care in countries such as China, India, and Japan

- The Post-Operative Rehabilitation segment dominated with a 44.3% share in 2025, supported by high rates of orthopedic surgeries, knee and shoulder replacements, and ligament repair procedures

Report Scope and Over the Counter (OTC) Braces Market Segmentation

|

Attributes |

Over the Counter (OTC) Braces Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Breg, Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Over the Counter (OTC) Braces Market Trends

“Rising Adoption of Preventive and Supportive Orthopedic Solutions”

- A prominent trend in the global OTC Braces market is the growing emphasis on preventive care and non-invasive management of musculoskeletal conditions. Consumers are increasingly seeking braces to support joints, prevent injuries during sports or daily activities, and manage chronic conditions such as arthritis, tendonitis, or ligament weakness. The focus has shifted from purely reactive treatment to proactive joint care, encouraging early intervention at home

- For instance, in 2025, multiple orthopedic product manufacturers introduced ergonomically designed knee, ankle, wrist, and elbow braces featuring adjustable support levels, lightweight materials, and enhanced comfort. These products allow both athletes and everyday users to maintain mobility while protecting vulnerable joints, reducing dependency on clinical treatment for minor injuries

- Another emerging trend is the integration of advanced materials such as breathable fabrics, flexible supports, and moisture-wicking liners, which improve user comfort and promote longer-term use. The aesthetic appeal of braces, with designs that can be worn discreetly under clothing, is also encouraging adoption among adults and older populations who may have been reluctant to wear visible support devices in the past

- There is also an increasing shift toward consumer education and awareness campaigns emphasizing the importance of joint protection, posture correction, and injury prevention, particularly for active lifestyles and aging populations

Over the Counter (OTC) Braces Market Dynamics

Driver

“Growing Prevalence of Musculoskeletal Disorders and Sports Injuries”

- The rising incidence of musculoskeletal disorders, including knee osteoarthritis, wrist strain, ligament injuries, and ankle sprains, is a primary driver for the OTC Braces market

- With the increasing number of people engaging in physical activities, competitive sports, and high-intensity workouts, the demand for supportive and protective braces is accelerating globally

- For instance, in 2025, reports from orthopedic associations highlighted a significant rise in knee and ankle injuries among recreational athletes in North America and Europe. This surge prompted both retail pharmacies and online platforms to expand their OTC brace offerings to meet immediate consumer needs, particularly in post-injury support and rehabilitation

- In addition, the growing prevalence of workplace-related musculoskeletal disorders among professionals in labor-intensive and sedentary jobs is increasing demand for braces that provide lumbar support, wrist stabilization, and posture correction

- These devices help reduce absenteeism, improve comfort, and enhance overall productivity

- Furthermore, increasing awareness of the benefits of preventive care and rehabilitation, combined with rising consumer willingness to invest in personal health, is boosting the market. Easy availability of OTC braces in pharmacies, specialty orthopedic stores, and e-commerce platforms ensures accessibility, supporting the broader adoption trend

Restraint/Challenge

“High Costs of Premium Products and Lack of Standardization”

- Despite the market’s strong growth, the relatively high cost of advanced OTC braces with specialized designs, reinforced supports, or integrated compression features can limit adoption among price-sensitive consumers. Premium braces with superior materials or adjustable multi-joint support systems are often more expensive than basic models, creating barriers in emerging markets and for first-time users

- For instance, braces offering enhanced stability for post-surgical recovery or high-impact sports protection carry a price premium, making them less accessible to the average consumer seeking everyday joint support

- Another challenge is the lack of standardized sizing, performance metrics, and quality guidelines across manufacturers. Inconsistent fit or inadequate support can result in discomfort, improper usage, or limited therapeutic benefit, which may discourage repeat purchases

- In addition, limited awareness of preventive brace use in certain regions, particularly among older adults or populations unfamiliar with self-care orthopedic solutions, hinders overall adoption. Misconceptions that braces are only for post-injury rehabilitation rather than proactive support also reduce market penetration

- Addressing these challenges through consumer education, affordable product innovations, standardized sizing, and increased availability in pharmacies and online channels will be critical to sustaining growth in the OTC Braces market

Over the Counter (OTC) Braces Market Scope

The market is segmented on the basis of Product, Indication, Type, Application, Distribution Channel, and End-User.

• By Product

On the basis of product, the OTC Braces market is segmented into Knee Braces, Ankle Braces, Foot Walkers and Orthoses, Back, Hip and Spine Braces, Shoulder Braces, Elbow Braces, Hand and Wrist Braces, and Facial Braces. The Knee Braces segment dominated with a revenue share of 38.6% in 2025, driven by the high prevalence of knee injuries and osteoarthritis across global populations. Knee braces provide support, stabilization, and pain relief, enhancing mobility and post-injury recovery. Hospitals and orthopedic clinics frequently prescribe them. Rising participation in sports and an aging population contribute to steady demand. Advanced designs with adjustable hinges and elastic supports improve patient adherence. Insurance coverage in some regions supports adoption. E-commerce availability further facilitates consumer access. Clinical guidelines recommend knee braces for post-surgical rehabilitation and ligament injuries. Public awareness campaigns on knee health strengthen usage. Product innovation, including lightweight materials, enhances comfort. Urban hospitals and homecare setups show higher prescription rates. Sports medicine centers also report increasing demand. Telehealth physiotherapy programs encourage remote usage.

The Ankle Braces segment is expected to witness the fastest CAGR of 15.8% from 2026 to 2033, fueled by growing sports participation and injury prevention initiatives. Increasing awareness among athletes, preventive care programs, and adoption in home rehabilitation accelerate growth. Lightweight and elastic ankle braces are preferred for comfort. Telemedicine consultations guide brace selection. High adoption is observed in professional sports clubs. E-commerce platforms expand reach to rural areas. Insurance support enhances affordability. Orthopedic clinics emphasize use post-fracture and sprains. Integration with physiotherapy programs drives clinical adoption. Sports academies promote prophylactic brace use. Rising incidence of ankle ligament injuries globally supports sustained growth. Innovative materials and ergonomic designs enhance compliance. Hospitals and homecare users increasingly rely on portable ankle supports.

• By Indication

On the basis of indication, the market is segmented into Osteoarthritis, Injury, Prophylactic, and Others. The Osteoarthritis segment dominated with a 42.1% share in 2025, driven by rising prevalence of degenerative joint diseases among aging populations. Knee, hip, and wrist braces help reduce pain, provide joint support, and improve daily activity performance. Hospitals, orthopedic centers, and homecare setups prescribe them extensively. Awareness campaigns on osteoarthritis management enhance early adoption. Insurance coverage for chronic conditions supports sales. Product innovation in soft and hinged braces increases patient comfort. Rehabilitation programs integrate braces for post-operative recovery. Sports medicine and physiotherapy clinics recommend osteoarthritis braces. Urban centers report higher adoption due to accessibility. Advanced designs improve compliance. Government initiatives promoting musculoskeletal health support market growth. Clinical guidelines encourage brace usage for conservative management. Telehealth guidance enhances homecare utilization.

The Prophylactic segment is projected to witness the fastest CAGR of 14.7% from 2026 to 2033, due to increasing awareness for injury prevention in sports and occupational activities. Professional athletes, trainers, and fitness enthusiasts are key users. Soft and elastic braces are widely preferred for mobility. E-commerce and retail channels expand product reach. Integration with wearable monitoring devices aids preventive care. Schools and colleges encourage prophylactic brace use. Insurance coverage in sports-related programs supports adoption. Physical therapists promote preventive braces. Homecare users increasingly adopt prophylactic braces for joint protection. Government campaigns on workplace safety enhance awareness. Clinical physiotherapy programs reinforce usage. Product innovation with breathable materials improves comfort. Growth is fueled by rising sports participation and active lifestyle trends.

• By Type

On the basis of type, the market is segmented into Soft and Elastic Braces, Hard and Rigid Braces, and Hinged Braces. The Soft and Elastic Braces segment dominated with a 39.5% share in 2025, offering comfort, flexibility, and easy wearability for chronic and post-operative patients. Hospitals and homecare users prefer them for day-to-day support. Ease of cleaning and adjustable straps improve adherence. Integration with rehabilitation programs ensures sustained use. E-commerce and retail channels enhance accessibility. Sports medicine applications encourage daily wear. Physiotherapists recommend soft braces for gradual recovery. Aging populations and injury-prone adults drive demand. Insurance coverage in some countries supports adoption. Market players focus on breathable and hypoallergenic materials. Clinical guidelines emphasize patient comfort and mobility. Urban adoption rates are higher due to awareness.

The Hinged Braces segment is expected to witness the fastest CAGR of 16.2% from 2026 to 2033, attributed to post-surgical ligament repair, joint stabilization, and advanced orthopedic procedures. Hinged designs provide adjustable range of motion and controlled movement. Hospitals and orthopedic centers drive clinical adoption. Sports medicine clinics integrate hinged braces for preventive and rehabilitative care. Homecare users adopt hinged braces for comfort and mobility. E-commerce platforms improve reach to rural patients. Insurance coverage for post-operative braces boosts uptake. Material innovations enhance durability and patient compliance. Physiotherapy programs emphasize hinged brace usage. Government health initiatives promote post-injury rehabilitation. Professional athletes drive prophylactic adoption. Rising incidence of ligament injuries globally supports growth. Clinical and home monitoring programs improve adherence.

• By Application

On the basis of application, the market is segmented into Ligament Injury Repair, Preventive Care, Post-Operative Rehabilitation, Osteoarthritis, Compression Therapy, and Others. The Post-Operative Rehabilitation segment dominated with a 44.3% share in 2025, supported by high rates of orthopedic surgeries, knee and shoulder replacements, and ligament repair procedures. Braces improve functional recovery, reduce complications, and support physiotherapy. Hospitals and homecare centers prioritize post-operative brace availability. Awareness among surgeons and physiotherapists drives prescription. Integration into rehabilitation protocols improves adherence. Insurance coverage supports usage. Patient education enhances correct application. Urban orthopedic centers report higher adoption. Advanced brace designs improve comfort and recovery outcomes. Telehealth guidance supports home rehabilitation. Clinical trials and R&D reinforce product adoption.

The Preventive Care segment is expected to witness the fastest CAGR of 15.5% from 2026 to 2033, due to rising sports participation and workplace injury prevention initiatives. Athletes, fitness enthusiasts, and physically active populations increasingly adopt preventive braces. Elastic and soft braces are preferred for mobility. E-commerce channels expand reach. Occupational health programs integrate brace usage. Sports medicine clinics promote daily preventive wear. Physiotherapists recommend braces for high-risk patients. Government campaigns on injury prevention support awareness. Material innovations enhance comfort and compliance. Homecare users adopt braces for joint protection. Insurance coverage in sports and preventive programs supports adoption. Integration with physiotherapy and wearable monitoring systems drives growth.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Pharmacies and Retailers, E-Commerce, and Orthopedic Clinics. The Pharmacies and Retailers segment dominated with 55.4% share in 2025, due to easy accessibility, in-store guidance, and repeat purchases. Marketing campaigns and brand visibility drive adoption. Hospitals and clinics also source small quantities. Awareness programs enhance consumer education. Retail presence in urban and semi-urban regions supports penetration. Insurance coverage in some markets improves affordability. Homecare users rely on pharmacy purchases. Online ordering complements retail availability. Product variety attracts repeat buyers. Sales promotions and discounts increase uptake. Retail staff training supports proper selection. Urban pharmacies report higher sales volume.

The E-Commerce segment is projected to witness the fastest CAGR of 16.8% from 2026 to 2033, driven by growing digital penetration, convenience of home delivery, and increased awareness among online consumers. Telemedicine consultations often recommend online purchases. Subscription-based refill programs enhance adherence. Rural and semi-urban penetration expands via online marketplaces. Product variety and reviews influence purchasing decisions. Price comparison improves adoption. Insurance-supported online sales increase convenience. Social media campaigns promote awareness. Specialty braces for sports and rehabilitation see online adoption. Integration with physiotherapy programs drives repeat orders. Improved logistics reduce delivery times. Online platforms offer personalized recommendations.

• By End-User

On the basis of end-user, the market is segmented into Hospitals, Home Healthcare, and Others. The Hospitals segment dominated with 61.4% share in 2025, due to high patient footfall, orthopedic surgery rates, and availability of rehabilitation facilities. Hospitals integrate braces into treatment protocols. Awareness campaigns and insurance coverage enhance adoption. Multidisciplinary teams ensure correct brace application. Clinical trials and R&D support product uptake. Urban hospitals report higher adoption rates. Telehealth guidance supports home rehabilitation. Hospital pharmacies ensure immediate availability. Government initiatives encourage post-operative brace use. Physiotherapists and surgeons drive prescription.

The Home Healthcare segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, driven by self-management of injuries, availability of OTC braces, and growing awareness of preventive care. Telemedicine consultations guide patients on proper use. Convenience for chronic patients supports adoption. E-commerce channels improve accessibility. Subscription programs support long-term use. Insurance coverage facilitates affordability. Home physiotherapy programs integrate brace usage. Awareness campaigns target rural populations. Wearable monitoring encourages compliance. Patient education enhances correct application. Urban and semi-urban homecare users adopt braces rapidly. Rising sports participation drives demand.

Over the Counter (OTC) Braces Market Regional Analysis

- North America dominated the over the counter (OTC) braces market with the largest revenue share of 45.5% in 2025, driven by advanced healthcare infrastructure, high consumer awareness, and the strong presence of key industry players. The region benefits from well-established medical distribution channels, high adoption of homecare solutions, and widespread use of preventive and rehabilitative orthopedic products

- Consumers in North America are increasingly aware of the importance of musculoskeletal health and injury prevention, which has boosted demand for OTC braces across various applications, including sports, post-surgical recovery, and chronic condition management

- High disposable income and urbanized populations support the adoption of ergonomically designed and technologically advanced braces, including adjustable, lightweight, and breathable products, which improve comfort and compliance. Increased availability through retail pharmacies, e-commerce platforms, and healthcare providers ensures easy access for consumers, reinforcing market growth

U.S. Over the Counter (OTC) Braces Market Insight

The U.S. over the counter (OTC) braces market captured the largest revenue share of 82% within North America in 2025, reflecting substantial growth due to high adoption in homecare, sports-related applications, and preventive musculoskeletal care. Consumers are increasingly seeking ergonomic, easy-to-use braces for knee, wrist, ankle, and back support, not only for rehabilitation but also for injury prevention during daily activities and athletic performance. Innovations from both established medical brands and startups are driving adoption, including products with adjustable compression, lightweight supports, and designs tailored to specific joints or conditions. Smart support features, like improved fit and mobility, are being integrated to enhance user comfort and effectiveness. High consumer awareness, coupled with frequent physician recommendations and growing online retail penetration, supports market expansion. Homecare programs, sports clinics, and physiotherapy centers increasingly recommend OTC braces for injury prevention and rehabilitation, further boosting adoption. Rising participation in sports and fitness activities, alongside an aging population seeking support for chronic conditions, is contributing to a diverse consumer base for OTC braces across the country.

Europe Over the Counter (OTC) Braces Market Insight

The Europe over the counter (OTC) braces market is projected to expand at a substantial CAGR during the forecast period, driven by increasing prevalence of musculoskeletal disorders, rising sports participation, and an aging population seeking preventive care solutions. Strict healthcare standards, combined with growing awareness of rehabilitation and ergonomic practices, are promoting OTC braces adoption in residential, clinical, and sports settings. European consumers are drawn to high-quality, ergonomic, and eco-friendly designs, with innovations such as adjustable supports, lightweight braces, and integrated cushioning enhancing comfort and usability.

U.K. Over the Counter (OTC) Braces Market Insight

The U.K. OTC Braces market is anticipated to grow at a noteworthy CAGR over the forecast period, fueled by rising awareness of injury prevention, increasing participation in fitness activities, and focus on post-surgical and chronic condition support. Convenient access to OTC braces through retail pharmacies, e-commerce platforms, and physiotherapy clinics supports consumer adoption. Consumers are increasingly relying on braces for minor musculoskeletal issues to reduce hospital visits and improve mobility at home.

Germany Over the Counter (OTC) Braces Market Insight

Germany’s over the counter (OTC) braces market is expected to expand significantly during the forecast period, fueled by high consumer awareness, advanced healthcare infrastructure, and emphasis on innovation and sustainability. Braces designed for preventive and rehabilitative purposes, suitable for sports enthusiasts, elderly populations, and post-operative care, are seeing high adoption. Integration with physiotherapy protocols and adherence to medical recommendations further drive market penetration.

Asia-Pacific Over the Counter (OTC) Braces Market Insight

The Asia-Pacific over the counter (OTC) braces market is poised to grow at the fastest CAGR of 12.3% during the forecast period, supported by increasing urbanization, rising disposable incomes, and growing awareness of preventive and rehabilitative musculoskeletal care in countries such as China, India, and Japan. Rising sports participation, workplace ergonomics, and increasing incidence of musculoskeletal injuries are driving demand. Government health initiatives and rising healthcare expenditure are also enabling broader access to OTC braces across urban and semi-urban regions. Manufacturers are introducing cost-effective, ergonomic braces to cater to a wide consumer base, while premium products target urban and sports-active populations. Online retail expansion is contributing to wider availability and convenience for consumers.

Japan Over the Counter (OTC) Braces Market Insight

Japan’s over the counter (OTC) braces market is gaining momentum due to the aging population, high health awareness, and preference for proactive musculoskeletal care. Braces providing lumbar, knee, ankle, and wrist support are increasingly used for daily activity assistance, post-injury recovery, and preventive care. The combination of high-tech design, user-friendly features, and availability through pharmacies and online platforms is promoting adoption, with younger populations adopting braces for sports and fitness activities as well.

China Over the Counter (OTC) Braces Market Insight

China over the counter (OTC) braces market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, rising middle-class income, and growing awareness of joint and musculoskeletal health. Demand is increasing for both preventive and rehabilitative OTC braces, particularly for knee, wrist, and back support among athletes, office workers, and the elderly. The expansion of e-commerce, affordability of braces, and strong domestic manufacturers are key factors driving market growth. The emphasis on workplace ergonomics, sports, and fitness culture also contributes to sustained adoption across various consumer segments.

Over the Counter (OTC) Braces Market Share

The Over the Counter (OTC) Braces industry is primarily led by well-established companies, including:

• Breg, Inc. (U.S.)

• DJO Global (U.S.)

• Össur (Iceland)

• Medi (Germany)

• DeRoyal Industries (U.S.)

• Hanger, Inc. (U.S.)

• Bauerfeind AG (Germany)

• Sam Medical (U.S.)

• DonJoy (U.S.)

• FlexiMed (U.S.)

• Orthomen (India)

• Thuasne (France)

• BSN Medical (Germany)

• Zimmer Biomet Holdings, Inc. (U.S.)

• Mueller Sports Medicine (U.S.)

• McDavid (U.S.)

• Futuro (U.S.)

• BioSkin (U.S.)

• ORTHOCARE (U.S.)

• Ossur Americas (U.S.)

Latest Developments in Global Over the Counter (OTC) Braces Market

- In January 2024, Enovis, through its subsidiary DJO Global, launched the DonJoy ROAM Advanced Knee Brace, designed for patients with osteoarthritis and chronic knee instability. This OTC brace combined targeted compression, adjustable support structures, and user-friendly design to enhance mobility and reduce pain. The launch reinforced the trend of developing specialized braces addressing age-related joint degeneration in the consumer market

- In March 2025, Medi GmbH & Co. KG partnered with Medline Industries to expand distribution of Medi OTC braces in North America. This strategic alliance enhanced availability across retail, clinical, and e-commerce channels, ensuring that consumers had easier access to ergonomic, high-quality joint supports designed for both injury prevention and post-injury rehabilitation

- In May 2025, Bauerfeind AG completed the acquisition of BioSkin’s orthotics business, a move that expanded Bauerfeind’s product portfolio of over-the-counter braces and supports. This acquisition provided access to innovative brace designs, advanced materials, and established distribution channels, positioning the company to meet growing global demand for high-performance, user-friendly orthopedic solutions

- In June 2025, Ottobock expanded its retail and clinical distribution network for soft OTC braces across Southeast Asia, targeting both sports rehabilitation clinics and general consumer markets. The expansion aimed to meet rising demand in emerging regions and improve accessibility for preventive and rehabilitative orthopedic care

- In July 2025, Ottobock unveiled the SmartKnee Flex Orthotic Brace, a next-generation OTC brace featuring integrated sensors and app-based monitoring. The system allowed users to track joint movement, receive feedback on activity levels, and adjust support in real-time. This innovation highlighted the growing trend of merging wearable technology with orthopedic supports for enhanced rehabilitation and personalized care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.