Global Over The Top Market

Market Size in USD Billion

USD

263.16 Billion

USD

750.68 Billion

2024

2032

USD

263.16 Billion

USD

750.68 Billion

2024

2032

| 2025 - 2032 | |

| USD 263.16 Billion | |

| USD 750.68 Billion | |

| % | |

|

Over the Top Market Size

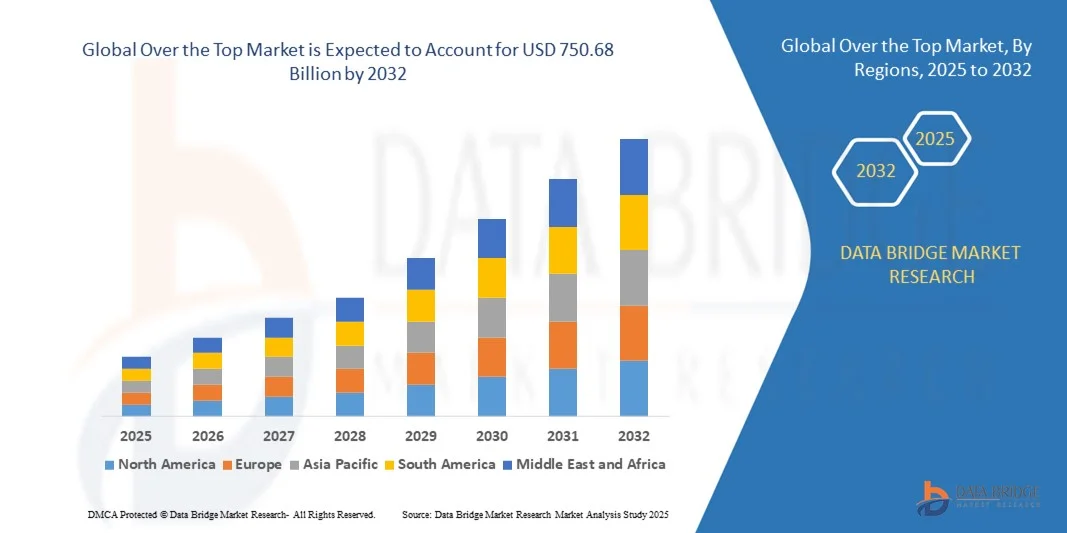

- The global over the top market size was valued at USD 263.16 billion in 2024 and is expected to reach USD 750.68 billion by 2032, at a CAGR of 14.00% during the forecast period

- The market growth is largely fueled by the rapid expansion of high-speed internet, widespread smartphone penetration, and increasing consumer preference for on-demand video and audio content, leading to higher OTT platform adoption across regions

- Furthermore, rising demand for personalized, ad-free, and multi-device streaming experiences, along with advancements in content delivery networks and AI-driven recommendation systems, is driving subscriber growth and expanding the OTT ecosystem, thereby significantly boosting the industry’s growth

Over the Top Market Analysis

- OTT platforms provide on-demand streaming services for movies, TV shows, music, and live content through internet-connected devices, offering personalized, flexible, and interactive viewing experiences for consumers across residential and commercial segments

- The escalating demand for OTT services is primarily fueled by changing media consumption habits, cord-cutting trends, and the growing preference for content accessibility anytime and anywhere, alongside continuous investments in original and localized content

- North America dominated the over the top market with a share of 42.6% in 2024, due to widespread internet penetration, high smartphone adoption, and a mature digital entertainment ecosystem

- Asia-Pacific is expected to be the fastest growing region in the over the top market during the forecast period due to increasing smartphone penetration, affordable data plans, and expanding broadband connectivity in countries such as China, India, and Japan

- Video segment dominated the market with a market share of 65.5% in 2024, due to the surging demand for video-on-demand and live streaming platforms. High-quality content production, rising investment in original programming, and consumer preference for visual entertainment have driven the dominance of video content. The expansion of global streaming platforms such as Netflix, Amazon Prime Video, and Disney+ has also accelerated this trend

Report Scope and Over the Top Market Segmentation

|

Attributes |

Over the Top Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Over the Top Market Trends

Rise of Personalized and Interactive Streaming Experiences

- The over-the-top (OTT) market is undergoing a transformation driven by the growing emphasis on personalized and interactive streaming experiences. Consumers increasingly expect content platforms to tailor recommendations, curate viewing options, and offer immersive engagement powered by artificial intelligence and analytics-driven personalization engines

- For instance, Netflix leverages its advanced AI recommendation algorithms to deliver personalized content suggestions based on user behavior, watch history, and preferences. Similarly, Disney+ integrates audience segmentation tools through its platform to enhance engagement by providing suggestions aligned with viewing patterns across age groups and genres

- The integration of interactive technologies such as live polls, multi-angle camera views, and choose-your-own-adventure content models is redefining how audiences engage with digital media. These features increase user participation and also create differentiated value for streaming service providers aiming to improve customer retention rates

- In addition, real-time analytics and adaptive streaming technologies are enabling platforms to dynamically adjust video quality and content recommendations based on individual user data. This ensures uninterrupted experiences while enhancing personalization across devices and network conditions

- OTT companies are also investing heavily in gamification and audience engagement tools such as loyalty rewards and interactive advertisements. These features transform passive content consumption into active participation, fostering stronger emotional connections between brands and audiences

- As personalization becomes a core pillar of competitive differentiation, the rise of AI-driven and interactive streaming experiences is expected to define the next stage of OTT market evolution. The trend signifies a shift toward consumer-centric viewing models where content ecosystems are designed around individual preferences and user involvement

Over the Top Market Dynamics

Driver

High Smartphone and Internet Adoption

- The global proliferation of smartphones and expanding high-speed internet connectivity are primary drivers fueling the growth of the OTT market. With the increasing affordability of smart devices and data plans, consumers are steadily transitioning from conventional broadcast models to on-demand digital streaming

- For instance, in 2025, Netflix and Amazon Prime Video reported substantial viewership growth in emerging markets such as India and Brazil, driven by improved 4G and expanding 5G adoption. Similarly, MX Player and Hotstar have leveraged widespread smartphone penetration to broaden access to regional content across both rural and urban populations

- The combination of mobile streaming capability and affordable broadband options has minimized barriers to entry for new users, allowing seamless access to OTT platforms across demographics. This digital accessibility is significantly expanding user bases and watch durations worldwide

- In addition, the availability of low-cost smart televisions and casting devices has further boosted OTT adoption, enabling consumers to easily connect mobile content streaming to large screens. This cross-device compatibility enhances flexibility and affordability for viewers globally

- The convergence of high internet speeds, mobile-first media consumption, and increasing content diversity is helping OTT players reach previously untapped audiences. As connectivity infrastructure continues to strengthen, the sustained expansion of smartphones and mobile networks will remain a central force propelling global OTT platform growth

Restraint/Challenge

Intense Competition and Content Saturation

- The OTT market is facing significant challenges due to intensifying competition and growing content oversaturation. With numerous players entering the space, platforms are under constant pressure to differentiate their content offerings and retain subscriber loyalty in an increasingly crowded environment

- For instance, platforms such as Hulu, Apple TV+, and Peacock have engaged in aggressive spending on original content to compete with established giants such as Netflix and Disney+. However, the resulting surge in content volume has made audience retention difficult, as consumers often churn between services seeking fresh and exclusive material

- As multiple platforms compete for market share, production and licensing costs have escalated sharply, impacting profitability across the sector. The constant requirement to produce high-quality, exclusive content has heightened financial pressure even for established streaming providers

- In addition, audience fatigue stemming from excessive subscription demands and repetitive content patterns is gradually reducing user engagement levels. The presence of similar genres and formats across competing platforms reduces perceived value and challenges subscriber retention

- While consolidation and regional specialization are strategies some players employ to navigate market saturation, sustaining distinctive value propositions remains a complex task. Achieving long-term stability will require strategic differentiation, localized content investments, and advanced engagement tools to retain audience loyalty in this competitive landscape

Over the Top Market Scope

The market is segmented on the basis of platform type, component, content type, deployment model, revenue model, service type, and end users.

- By Platform Type

On the basis of platform type, the Over-the-Top (OTT) market is segmented into smartphones, smart TVs, laptops, desktops and tablets, gaming consoles, set-top boxes, and others. The smartphones segment dominated the largest market revenue share in 2024 owing to the widespread penetration of mobile devices and affordable data plans globally. Increasing demand for on-the-go entertainment and the rapid adoption of 5G connectivity have enhanced video streaming quality and reduced latency, making smartphones the primary medium for OTT content consumption. In addition, the availability of mobile-specific streaming apps and offline viewing options further strengthen this segment’s dominance.

The smart TVs segment is projected to witness the fastest growth rate from 2025 to 2032, fueled by the increasing shift toward home-based entertainment and the growing integration of OTT apps into television interfaces. Consumers are increasingly replacing traditional cable services with smart TVs that provide direct access to multiple streaming platforms. Enhanced picture quality, voice-enabled search, and the rise of affordable smart TV models have accelerated adoption, particularly across Asia-Pacific and Europe.

- By Component

On the basis of component, the OTT market is categorized into solutions and services. The solutions segment dominated the market in 2024, driven by the rising deployment of advanced content management and streaming platforms. Solutions provide critical infrastructure for encoding, transcoding, and content delivery, enabling OTT providers to maintain quality and scalability. The surge in video-on-demand (VOD) and live streaming platforms has further amplified the need for robust streaming solutions with enhanced security, analytics, and monetization capabilities.

The services segment is expected to grow at the fastest rate from 2025 to 2032 due to the increasing demand for managed and cloud-based support among OTT providers. As content distribution becomes more complex, companies rely on professional services for platform customization, integration, and performance optimization. The growing trend of outsourcing maintenance and support functions to enhance operational efficiency and focus on core streaming capabilities also contributes to this growth.

- By Content Type

On the basis of content type, the OTT market is segmented into voice over IP, text and images, video, and others. The video segment accounted for the largest revenue share of 65.5% in 2024, attributed to the surging demand for video-on-demand and live streaming platforms. High-quality content production, rising investment in original programming, and consumer preference for visual entertainment have driven the dominance of video content. The expansion of global streaming platforms such as Netflix, Amazon Prime Video, and Disney+ has also accelerated this trend.

The voice over IP (VoIP) segment is anticipated to register the fastest growth rate during the forecast period, supported by increasing use of internet-based calling and conferencing solutions. The growing integration of VoIP features in OTT communication platforms and the rise of remote working and online collaboration are fueling demand. Moreover, enterprises are adopting VoIP for cost-efficient, high-quality, and scalable communication, enhancing its penetration across business and individual users.

- By Deployment Model

On the basis of deployment model, the OTT market is bifurcated into on-premise and on-cloud. The on-cloud segment dominated the market in 2024 due to its scalability, flexibility, and cost efficiency. Cloud-based deployment enables seamless streaming across multiple regions with lower latency and facilitates real-time analytics and content personalization. OTT providers prefer cloud infrastructure for managing large volumes of data, reducing operational complexity, and ensuring faster service delivery.

The on-premise segment is expected to witness notable growth from 2025 to 2032, driven by enterprises and government organizations focusing on greater control over data and security. Some content providers and media firms prefer on-premise deployment to maintain proprietary rights and ensure compliance with data regulations. This approach is gaining traction particularly among premium content distributors managing confidential media assets.

- By Revenue Model

On the basis of revenue model, the OTT market is divided into subscription, procurement, rental, and others. The subscription segment dominated the market in 2024, owing to the popularity of subscription-based video-on-demand (SVOD) platforms that offer ad-free, high-quality content. Consumers prefer predictable monthly or annual payments, and the success of platforms such as Netflix and Disney+ has solidified the subscription model’s lead. In addition, subscription bundles and flexible pricing have increased consumer retention and loyalty.

The rental segment is expected to record the fastest growth from 2025 to 2032, supported by the growing preference for pay-per-view content. This model appeals to users seeking short-term access to premium or exclusive titles without long-term commitments. Increasing digital movie releases and event-based live streaming are key factors accelerating rental-based revenue growth across both developed and emerging economies.

- By Service Type

On the basis of service type, the OTT market is categorized into consulting, installation and maintenance, training and support, and managed services. The managed services segment held the largest market share in 2024, driven by the need for efficient content delivery, user management, and performance monitoring. OTT providers are outsourcing these operations to specialized partners to enhance uptime and service reliability. The rising complexity of OTT platforms and the need for continuous optimization further reinforce the demand for managed services.

The consulting segment is projected to witness the fastest growth rate from 2025 to 2032 as OTT companies seek strategic advice for expansion, digital transformation, and technology integration. Consulting services assist providers in adopting AI-based recommendations, optimizing monetization models, and ensuring regulatory compliance. The increasing competition among streaming platforms has intensified the need for expert consultation to improve user experience and operational scalability.

- By End Users

On the basis of end users, the OTT market is segmented into media and entertainment, education and training, health and fitness, IT and telecom, e-commerce, BFSI, government, and others. The media and entertainment segment dominated the market in 2024 due to the exponential growth of video streaming services and global investments in digital content creation. Viewers’ shift toward personalized and on-demand entertainment has transformed this segment into the core driver of OTT consumption. The integration of advanced recommendation algorithms and regional content expansion further enhances engagement.

The education and training segment is expected to grow at the fastest rate from 2025 to 2032, fueled by the adoption of OTT-based learning platforms and e-learning content. Growing demand for remote education, corporate training, and interactive video lessons has encouraged institutions and businesses to embrace OTT delivery models. The increasing use of AI-driven analytics to personalize learning experiences also supports this segment’s rapid expansion.

Over the Top Market Regional Analysis

- North America dominated the over the top market with the largest revenue share of 42.6% in 2024, driven by widespread internet penetration, high smartphone adoption, and a mature digital entertainment ecosystem

- Consumers in the region prefer on-demand streaming and personalized content experiences, boosting OTT platform usage across media, education, and corporate segments

- This growth is further supported by high disposable incomes, robust broadband infrastructure, and the increasing adoption of connected devices, establishing OTT services as a primary medium for entertainment and communication in both residential and commercial settings

U.S. Over the Top Market Insight

The U.S. over the top market captured the largest revenue share in North America in 2024, propelled by the growing consumption of video-on-demand, live streaming, and interactive content. The shift from traditional cable and satellite services to digital streaming platforms is accelerating, supported by a technology-savvy population and widespread availability of high-speed internet. Strong investments by global and local over the top providers, along with integration with smart TVs, smartphones, and voice assistants, further contribute to market growth.

Europe Over the Top Market Insight

The Europe over the top Market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing digital adoption, regulatory support for internet services, and a growing preference for personalized streaming content. Consumers are embracing Over the Top platforms for entertainment, education, and communication, while urbanization and higher smartphone penetration are boosting demand. The region witnesses significant growth across both subscription-based and ad-supported models, enhancing content accessibility across various devices.

U.K. Over the Top Market Insight

The U.K. over the top market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by rising demand for on-demand entertainment, high internet penetration, and the adoption of mobile and smart TV platforms. Increasing content consumption on smartphones and connected devices, combined with the popularity of subscription-based streaming services, is driving market expansion. Moreover, strong e-commerce infrastructure and digital payment adoption are facilitating seamless access to over the top services.

Germany Over the Top Market Insight

The Germany over the top market is expected to expand at a considerable CAGR during the forecast period, driven by rising awareness of digital content services and the demand for high-quality streaming experiences. Consumers increasingly prefer over the top platforms for entertainment, educational content, and corporate communications. The country’s robust IT infrastructure, high broadband availability, and growing investment in original and localized content further support market adoption, particularly across smart TVs, laptops, and mobile devices.

Asia-Pacific Over the Top Market Insight

The Asia-Pacific over the top market is poised to grow at the fastest CAGR from 2025 to 2032, fueled by increasing smartphone penetration, affordable data plans, and expanding broadband connectivity in countries such as China, India, and Japan. Rapid urbanization, rising disposable incomes, and government initiatives promoting digital literacy and smart infrastructure are accelerating over the top adoption. The region is also witnessing significant growth in regional content production and multilingual offerings, broadening the consumer base and driving platform engagement.

Japan Over the Top Market Insight

The Japan over the top market is witnessing steady growth, supported by the country’s technologically advanced ecosystem, high-speed internet, and growing consumer preference for on-demand content. over the top platforms are increasingly integrated with smart TVs, mobile devices, and gaming consoles, catering to both entertainment and educational content. Japan’s aging population also favors convenient, personalized, and accessible streaming solutions for residential and commercial use, boosting demand for user-friendly Over the Top services.

China Over the Top Market Insight

The China over the top market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the rapid expansion of digital content consumption and a massive mobile-first population. The increasing number of internet users, adoption of smart devices, and investments in domestic over the top platforms have contributed to market growth. Strong government support for digital infrastructure, the rise of short-form and interactive video content, and competitive pricing of subscription services are key factors propelling Over the Top adoption across media, education, and corporate segments.

Over the Top Market Share

The over the top industry is primarily led by well-established companies, including:

- Amazon Web Services, Inc. (U.S.)

- Netflix (U.S.)

- Hulu, LLC (U.S.)

- Google, LLC (U.S.)

- Roku, Inc. (U.S.)

- Facebook (U.S.)

- Apple Inc. (U.S.)

- Kaltura, Inc. (U.S.)

- Twitter, Inc. (U.S.)

- Telestra (Australia)

- Rakuten, Inc. (Japan)

- Home Box Office, Inc. (U.S.)

- LinkedIn Corporation (U.S.)

- Evernote Corporation (U.S.)

- YouTube (U.S.)

- Advocado Pte. Ltd. (Singapore)

- LINE Corporation (Japan)

- Zype Inc. (U.S.)

- Fandango (U.S.)

- Dropbox (U.S.)

- Yahoo (U.S.)

- Microsoft (U.S.)

- Innovid (U.S.)

Latest Developments in Global Over the Top Market

- In May 2022, Mattel, Inc. announced a strategic partnership with HBO Max to launch a series of new live-action American Girl specials based on its hit doll and book franchise. This collaboration is expected to enhance Mattel’s content footprint in the OTT market by leveraging HBO Max’s streaming reach. The release of high-profile specials, such as American Girl: Corinne Tan, strengthens brand visibility, drives subscriber engagement, and positions the company to tap into both the children’s entertainment and family-focused streaming segments

- In June 2022, Amazon partnered with American entertainment company AMC Networks to distribute its content on Amazon Prime Video channels in India. This move allows Amazon Prime Video to expand its content library by offering AMC+ and Acorn TV subscriptions ad-free, thereby increasing its appeal in a competitive OTT market. The partnership enhances market penetration, attracts new subscribers, and reinforces Amazon’s position as a comprehensive streaming platform in India

- In October 2021, Netflix made its largest acquisition by purchasing Roald Dahl Story Company to create a slate of animated TV series and other related media content. This acquisition enables Netflix to strengthen its intellectual property portfolio, expand content offerings across animated and live-action films, TV, games, and consumer products, and drive subscriber growth globally. The strategic move also reinforces Netflix’s competitive positioning in the family and children’s OTT segment while diversifying its revenue streams

- In April 2021, The Walt Disney Company and Sony Pictures Entertainment announced a multi-year licensing agreement for U.S. streaming and TV rights to Sony Pictures’ theatrical releases. This agreement allows Disney’s streaming platforms, including Disney+ and Hulu, as well as its linear networks, to access Sony’s content, expanding Disney’s OTT content library. By offering a wider variety of movies and series, Disney strengthens subscriber retention, boosts platform engagement, and enhances its market share in the increasingly competitive OTT landscape

- In April 2020, Synamedia partnered with Google Cloud to expand its over-the-top offerings “as a service.” This collaboration allows Synamedia to deliver scalable, high-performance OTT solutions with reduced operational costs, particularly for live sports and high-demand content. The partnership improves content delivery efficiency, enhances user experience through low-latency streaming, and positions Synamedia as a leading technology enabler in the OTT infrastructure market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.