Global Pachymeter Device Market

Market Size in USD Billion

USD

2.04 Billion

USD

3.14 Billion

2025

2033

USD

2.04 Billion

USD

3.14 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 2.04 Billion |

Market Size (Forecast Year) |

USD 3.14 Billion |

CAGR |

% |

Major Markets Players |

|

Pachymeter Device Market Size

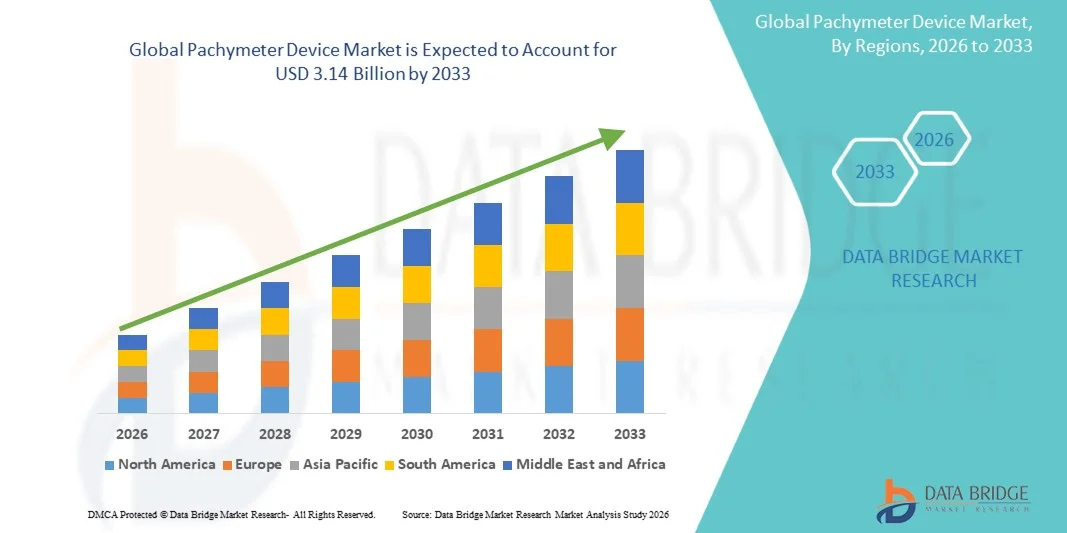

- The global pachymeter device market size was valued at USD 2.04 billion in 2025 and is expected to reach USD 3.14 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is largely fueled by the rising prevalence of corneal disorders such as glaucoma, keratoconus, and refractive errors, which are increasing the need for accurate corneal thickness measurement in ophthalmic diagnosis and surgical planning

- Furthermore, the growing number of refractive surgeries including LASIK and cataract procedures is strengthening the demand for pachymeters as essential pre-operative and post-operative assessment tools across hospitals and eye care clinics

Pachymeter Device Market Analysis

- Pachymeter devices, offering precise measurement of corneal thickness through ultrasound and optical technologies, are becoming integral components of modern ophthalmic diagnostic systems due to their high accuracy, non-invasive nature, and compatibility with advanced imaging platforms

- The escalating demand for early disease detection, increasing awareness of preventive eye care, and rapid adoption of advanced ophthalmic diagnostic equipment are collectively driving the uptake of pachymeter devices, thereby significantly boosting the industry's growth

- North America dominated the pachymeter device market with a share of 38.5% in 2025, due to strong adoption of advanced ophthalmic diagnostic technologies and increasing prevalence of corneal disorders such as glaucoma and keratoconus

- Asia-Pacific is expected to be the fastest growing region in the pachymeter device market during the forecast period due to increasing prevalence of eye diseases, expanding healthcare access, and rising awareness of preventive ophthalmic care

- Ultrasound method segment dominated the market with a market share of 62.9% in 2025, due to its long-standing clinical reliability and widespread availability in ophthalmic diagnostics. It provides accurate corneal thickness measurements and is extensively used in glaucoma evaluation and pre-surgical assessments. Cost-effectiveness and established clinical acceptance further support its dominance across healthcare facilities

Report Scope and Pachymeter Device Market Segmentation

|

Attributes |

Pachymeter Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Optovue Incorporated (U.S.) · DGH Technology, Inc. (U.S.) · Tomey Corporation (Japan) · Sonomed Escalon (U.S.) · Reichert Inc. (U.S.) · AMETEK Inc. (U.S.) · MicroMedical Devices (MMD) Inc. (U.S.) · OCULUS (Germany) · Topcon (Japan) · Ophtec BV (Netherlands) · NIDEK Co. Ltd. (U.S.) · CSO (Ireland) · Zeiss International (Germany) |

|

Market Opportunities |

· Expansion of Portable and Handheld Pachymeter Devices in Point-of-Care Settings · Integration of Pachymetry Systems with Multimodal Ophthalmic Imaging Platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pachymeter Device Market Trends

“Increasing Adoption of Non-Contact Optical Pachymetry Systems”

- A significant trend in the pachymeter device market is the rising shift toward non-contact optical pachymetry systems, driven by the growing need for faster, more comfortable, and infection-free corneal thickness measurement in ophthalmic diagnostics. This transition is improving patient experience while enhancing workflow efficiency in eye care settings

- For instance, companies such as Carl Zeiss Meditec and Optovue Incorporated have developed optical coherence tomography based pachymetry solutions that enable high-precision corneal mapping without physical contact. These systems are widely used in advanced ophthalmology clinics for refractive surgery evaluation and glaucoma screening

- The adoption of non-contact systems is increasing in hospitals and specialty eye care centers due to reduced risk of corneal injury and improved diagnostic accuracy. This is particularly relevant in high-volume clinical environments where patient throughput and hygiene standards are critical

- The integration of optical pachymetry with multimodal imaging platforms is further strengthening diagnostic capabilities by allowing simultaneous assessment of corneal structure and thickness. This is enhancing clinical decision-making in refractive and therapeutic procedures

- The shift toward portable and automated ophthalmic diagnostic devices is supporting the expansion of non-contact pachymeters in outpatient clinics. This trend is improving accessibility to advanced eye care diagnostics in both developed and emerging healthcare systems

- The market is also witnessing increased preference for digital ophthalmic workflows where non-contact pachymetry data is integrated into electronic medical records. This is driving greater efficiency in patient monitoring and long-term ophthalmic disease management

Pachymeter Device Market Dynamics

Driver

“Rising Prevalence of Glaucoma and Corneal Disorders”

- The growing prevalence of glaucoma, keratoconus, and other corneal disorders is a key driver of the pachymeter device market, as accurate corneal thickness measurement is essential for diagnosis, risk assessment, and treatment planning. Increasing patient burden is pushing healthcare providers to adopt advanced diagnostic tools for early detection and disease management

- For instance, organizations such as the World Health Organization and leading ophthalmic research institutes report a steady rise in glaucoma cases globally, driving higher demand for corneal diagnostic procedures supported by pachymeters. This has led to increased utilization of devices from companies such as NIDEK Co., Ltd. and Reichert Technologies in clinical practice

- The rising number of refractive surgeries such as LASIK and cataract operations is further strengthening the need for pachymetry as a mandatory pre-operative assessment tool. This ensures surgical safety and improves patient outcomes by accurately measuring corneal thickness

- Increasing awareness of preventive eye care and routine ophthalmic screening programs is also contributing to higher adoption of pachymeter devices. Early-stage diagnosis of corneal abnormalities is becoming a priority in modern eye care systems

- The continuous rise in age-related vision disorders is further reinforcing the demand for accurate corneal evaluation tools. This sustained clinical requirement is positioning pachymeters as essential devices in ophthalmic diagnostic workflows globally

Restraint/Challenge

“High Cost of Advanced Ophthalmic Diagnostic Equipment”

- The high cost of advanced pachymeter devices, particularly optical and integrated multimodal systems, remains a key challenge limiting widespread adoption, especially in cost-sensitive healthcare markets. The requirement for advanced technology and precision engineering contributes significantly to overall device pricing

- For instance, premium ophthalmic diagnostic systems offered by companies such as Carl Zeiss Meditec and Topcon Corporation involve high acquisition and maintenance costs, making them less accessible for smaller clinics and developing healthcare facilities

- The need for specialized training to operate advanced pachymetry systems further increases operational expenses for healthcare providers. This creates additional barriers for adoption in regions with limited skilled ophthalmic personnel

- Budget constraints in public healthcare systems often restrict procurement of high-end diagnostic equipment, slowing down market penetration in emerging economies. This impacts the overall accessibility of advanced eye care diagnostics

- The overall cost sensitivity in ophthalmic care delivery continues to challenge market expansion despite rising clinical demand. This creates a gap between technological advancement and affordability in the global pachymeter device market

Pachymeter Device Market Scope

The market is segmented on the basis of product type, type, and application.

- By Product Type

On the basis of product type, the pachymeter device market is segmented into handheld type and non-handheld type. The non-handheld type segment dominated the market with the largest revenue share in 2025, supported by its higher measurement precision and strong adoption in hospitals and specialized ophthalmic clinics. These devices are often integrated with slit lamps and diagnostic workstations, enabling consistent corneal thickness evaluation during comprehensive eye examinations. Their stability and accuracy make them suitable for high patient volume settings where reliability is critical. Growing preference for advanced diagnostic infrastructure in eye care centers further strengthens demand for non-handheld systems.

The handheld type segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising demand for portable and point-of-care diagnostic solutions. These devices offer flexibility in outpatient clinics and remote screening environments where fixed installations are limited. Increasing awareness of early glaucoma detection and expanding outreach eye care programs support adoption of handheld systems. Their lightweight design and ease of use improve workflow efficiency for ophthalmologists. Expanding usage in mobile clinics and small healthcare facilities continues to accelerate segment growth.

- By Type

On the basis of type, the pachymeter device market is segmented into ultrasound method and optical method. The ultrasound method segment dominated the market with the largest share of 62.9% in 2025 due to its long-standing clinical reliability and widespread availability in ophthalmic diagnostics. It provides accurate corneal thickness measurements and is extensively used in glaucoma evaluation and pre-surgical assessments. Cost-effectiveness and established clinical acceptance further support its dominance across healthcare facilities. Continuous use in routine ophthalmic examinations reinforces its strong market position.

The optical method segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing preference for non-contact and advanced imaging technologies. Optical pachymetry offers improved patient comfort and reduced risk of infection, making it suitable for modern clinical environments. Integration with technologies such as optical coherence tomography enhances diagnostic precision and workflow efficiency. Rising adoption in premium eye care centers and research institutions supports its expansion. Technological advancements in high-resolution imaging continue to drive segment growth.

- By Application

On the basis of application, the pachymeter device market is segmented into glaucoma diagnosis and refractive surgery. The glaucoma diagnosis segment dominated the market in 2025, driven by the increasing global burden of glaucoma and the critical role of corneal thickness measurement in accurate intraocular pressure assessment. Pachymetry is widely used as a standard diagnostic step in glaucoma screening and monitoring. Strong emphasis on early detection and preventive eye care supports sustained demand in this segment. High patient inflow in ophthalmic clinics further reinforces its leading position.

The refractive surgery segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of procedures such as LASIK and other vision correction surgeries. Pachymeter devices play a key role in preoperative evaluation to ensure surgical safety and effectiveness. Increasing demand for cosmetic and corrective vision procedures supports segment expansion. Advancements in refractive surgical technologies have increased the need for precise corneal mapping. Growing patient awareness regarding vision correction options continues to accelerate growth in this segment.

Pachymeter Device Market Regional Analysis

- North America dominated the pachymeter device market with the largest revenue share of 38.5% in 2025, driven by strong adoption of advanced ophthalmic diagnostic technologies and increasing prevalence of corneal disorders such as glaucoma and keratoconus

- Healthcare providers in the region prioritize high-precision diagnostic tools for pre-operative refractive surgery evaluations and routine ophthalmic screenings, boosting demand for pachymeters across hospitals and specialty eye clinics

- This dominance is further supported by well-established healthcare infrastructure, high healthcare expenditure, and rapid integration of digital ophthalmic devices into clinical workflows

U.S. Pachymeter Device Market Insight

The U.S. pachymeter device market captured the largest revenue share in North America in 2025, driven by the high burden of eye-related disorders and increasing demand for early and accurate corneal thickness measurement. The growing volume of refractive surgeries such as LASIK and cataract procedures is further accelerating the use of pachymeters in pre-surgical assessments. Strong presence of advanced ophthalmology centers, combined with rapid adoption of handheld and ultrasound-based pachymeters, is supporting market expansion. In addition, integration of pachymetry data with electronic health records and digital imaging systems is improving diagnostic efficiency and strengthening clinical decision-making.

Europe Pachymeter Device Market Insight

The Europe pachymeter device market is projected to expand at a steady CAGR during the forecast period, driven by increasing geriatric population and rising incidence of ophthalmic diseases. Strong regulatory focus on early diagnosis and preventive eye care is encouraging wider adoption of pachymetry devices in clinical practice. Demand is further supported by the expansion of outpatient eye care services and growing preference for minimally invasive diagnostic tools. Adoption is also increasing across hospitals and specialty clinics due to advancements in portable and non-contact pachymeters.

U.K. Pachymeter Device Market Insight

The U.K. pachymeter device market is expected to grow at a notable CAGR, driven by rising awareness of eye health and increasing screening programs for glaucoma and corneal disorders. Growing demand for advanced diagnostic accuracy in pre-operative ophthalmic procedures is supporting the adoption of pachymeters in both public and private healthcare facilities. Expansion of private eye care clinics and increasing investment in modern ophthalmic equipment are further strengthening market growth.

Germany Pachymeter Device Market Insight

The Germany pachymeter device market is anticipated to expand at a considerable CAGR during the forecast period, supported by strong emphasis on precision diagnostics and technologically advanced healthcare systems. Rising cases of age-related eye conditions and increasing surgical interventions are boosting demand for corneal thickness measurement devices. The country’s focus on high-quality medical imaging and integration of digital ophthalmology solutions is further promoting adoption across hospitals and specialized eye care centers.

Asia-Pacific Pachymeter Device Market Insight

The Asia-Pacific pachymeter device market is poised to grow at the fastest CAGR during 2026 to 2033, driven by increasing prevalence of eye diseases, expanding healthcare access, and rising awareness of preventive ophthalmic care. Growing healthcare investments in countries such as China, India, and Japan are supporting the expansion of eye care infrastructure. In addition, rising adoption of advanced diagnostic devices in urban hospitals and ophthalmic clinics is accelerating market penetration. The region is also benefiting from increasing availability of cost-effective pachymetry devices, improving accessibility for a broader patient base.

Japan Pachymeter Device Market Insight

The Japan pachymeter device market is gaining momentum due to a rapidly aging population and high demand for advanced ophthalmic diagnostics. Strong focus on precision healthcare and early disease detection is driving adoption of pachymeters in both hospital and specialized eye care settings. Integration of pachymetry systems with advanced imaging technologies and electronic diagnostic platforms is further enhancing clinical efficiency and supporting market growth.

China Pachymeter Device Market Insight

The China pachymeter device market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, expanding healthcare infrastructure, and rising prevalence of vision disorders. Increasing government support for healthcare modernization and growing investment in ophthalmic diagnostic equipment are accelerating adoption. Strong domestic manufacturing capabilities and availability of affordable diagnostic devices are further expanding the use of pachymeters across hospitals, eye clinics, and vision screening programs.

Pachymeter Device Market Share

The pachymeter device industry is primarily led by well-established companies, including:

- Optovue Incorporated (U.S.)

- DGH Technology, Inc. (U.S.)

- Tomey Corporation (Japan)

- Sonomed Escalon (U.S.)

- Reichert Inc. (U.S.)

- AMETEK Inc. (U.S.)

- MicroMedical Devices (MMD) Inc. (U.S.)

- OCULUS (Germany)

- Topcon (Japan)

- Ophtec BV (Netherlands)

- NIDEK Co. Ltd. (U.S.)

- CSO (Ireland)

- Zeiss International (Germany)

Latest Developments in Global Pachymeter Device Market

- In March 2025, Topcon Healthcare expanded its ophthalmic diagnostics ecosystem by enhancing non-contact pachymetry integration within its multimodal imaging platforms. This development improved clinical workflow by enabling simultaneous assessment of corneal thickness and anterior segment parameters in a single system. It is expected to accelerate adoption in hospitals and specialty eye clinics by increasing diagnostic efficiency, reducing examination time, and strengthening demand for integrated pachymetry-enabled imaging solutions globally

- In August 2024, Carl Zeiss Meditec advanced its ophthalmic imaging capabilities by strengthening pachymetry integration within anterior segment optical coherence tomography systems. This enhancement enabled more precise corneal evaluation by combining high-resolution imaging with corneal thickness measurement in a unified diagnostic workflow. The development is likely to boost preference for multifunctional ophthalmic platforms in high-volume clinical environments and support broader adoption of advanced pachymeter-based diagnostic systems across developed markets

- In November 2023, Occuity partnered with Indo Optical by appointing it as the primary distributor for the PM1 Pachymeter, strengthening global distribution of handheld non-contact diagnostic devices. This collaboration enhanced market reach for advanced optical pachymetry solutions and supported improved accessibility for eye care professionals. The initiative is expected to reinforce Indo Optical’s position in vision care technology while accelerating adoption of portable pachymeters across clinics and ophthalmology practices

- In 2022, NIDEK Co., Ltd. introduced the NT-1p non-contact pachymeter as part of its ophthalmic diagnostic equipment portfolio expansion. This product launch strengthened the company’s position in precision eye care devices by offering improved accuracy and patient comfort during corneal thickness measurement. The introduction is anticipated to support global market expansion by increasing availability of advanced non-contact pachymetry solutions in hospitals and diagnostic centers

- In November 2021, Occuity Ltd. launched the PM1 handheld non-contact pachymeter at MEDICA 2021, marking a significant advancement in portable ophthalmic diagnostics. The device enabled micrometer-level precision in corneal thickness measurement without physical contact, improving patient comfort and clinical efficiency. This innovation is expected to drive increased demand for handheld pachymeters across the U.K. and Europe, supporting broader adoption of compact and easy-to-use ophthalmic diagnostic technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.