Global Panuveitis Treatment Market

Market Size in USD Billion

USD

3.93 Billion

USD

8.12 Billion

2024

2032

USD

3.93 Billion

USD

8.12 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.93 Billion | |

| USD 8.12 Billion | |

| % | |

|

Panuveitis Treatment Market Size

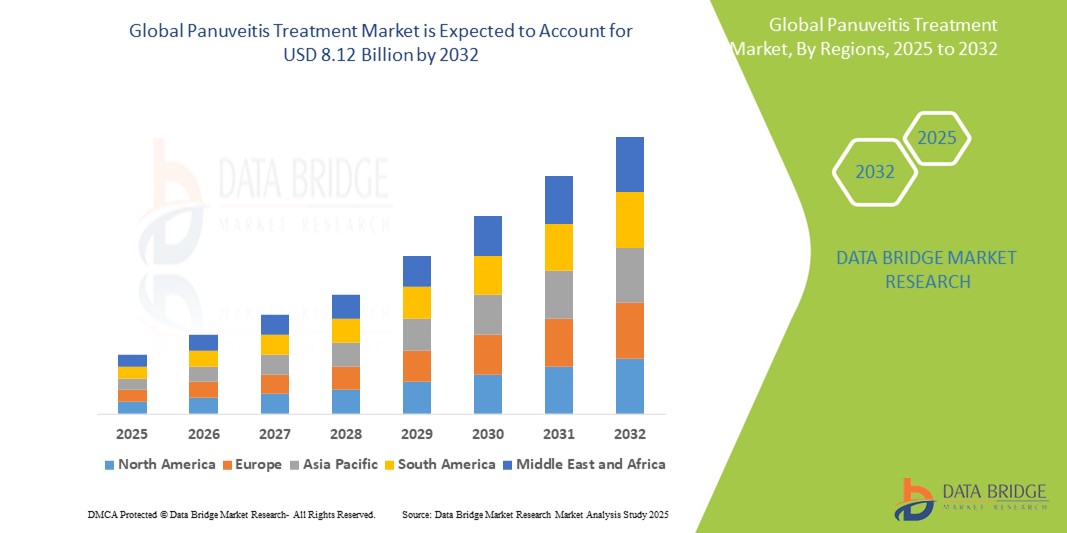

- The Global Panuveitis Treatment Market size was valued at USD 3.93 billion in 2024 and is expected to reach USD 8.12 billion by 2032, at a CAGR of 9.5% during the forecast period

- The market growth is largely driven by the increasing prevalence of autoimmune and inflammatory disorders affecting the eye, coupled with rising awareness and diagnosis of panuveitis globally. Advancements in biologics, corticosteroids, and immunosuppressive therapies have further contributed to treatment effectiveness and patient outcomes

- Additionally, the growing availability of specialized treatment options, expanding healthcare access in emerging markets, and an aging global population more susceptible to chronic eye diseases are fueling sustained demand. These factors together are strengthening the market outlook and supporting steady industry expansion

Panuveitis Treatment Market Analysis

- Panuveitis treatments, encompassing medications and surgical interventions, play a critical role in managing this severe and vision-threatening inflammatory eye condition, which affects all layers of the uveal tract and often requires long-term care and immune modulation

- The growing demand for panuveitis treatment is primarily fueled by the increasing global burden of autoimmune and infectious diseases, heightened awareness about early eye disease intervention, and advancements in biologics and immunosuppressive drug development

- North America dominates the global panuveitis treatment market, holding the largest revenue share of 38.7% in 2025, owing to a high prevalence of uveitis-related disorders, robust healthcare infrastructure, rapid adoption of advanced therapeutic options, and substantial R&D investments by pharmaceutical companies in the U.S. and Canada

- Asia-Pacific is expected to be the fastest-growing region in the panuveitis treatment market during the forecast period due to improving healthcare access, a growing geriatric population, and increasing incidence of infectious diseases contributing to intraocular inflammation

- The corticosteroids segment is expected to lead the panuveitis drug market with a market share of 41.3% in 2025, attributed to their widespread availability, rapid anti-inflammatory effects, and continued use as the first-line therapy in acute and chronic uveitis cases

Report Scope and Panuveitis Treatment Market Segmentation

|

Attributes |

Panuveitis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Panuveitis Treatment Market Trends

“Advancements in Biologics and Personalized Immunotherapy”

- A defining trend in the global panuveitis treatment market is the increasing adoption of biologics and targeted immunotherapies, particularly for non-infectious and chronic forms of panuveitis. These therapies are offering improved efficacy and better safety profiles compared to traditional corticosteroids or immunosuppressants.

- For instance, biologic agents such as adalimumab (Humira) have gained regulatory approval and are being widely prescribed for non-infectious intermediate, posterior, and panuveitis. Clinical trials for newer biologics and biosimilars are expanding the therapeutic pipeline and creating more tailored options for patients with refractory disease.

- Personalized treatment regimens are also emerging as physicians integrate genetic profiling, autoimmune biomarkers, and disease subtype classification to determine optimal therapies, reducing trial-and-error treatment cycles and enhancing patient outcomes.

- Moreover, sustained-release intravitreal implants, such as fluocinolone acetonide, are improving treatment compliance and reducing the need for frequent injections or systemic steroids. These innovations offer controlled and localized drug delivery, significantly benefiting patients with chronic or recurrent inflammation.

- This trend is reshaping clinical practice, leading to multidisciplinary approaches that combine ophthalmology, rheumatology, and immunology for holistic care. As a result, major players such as AbbVie, Johnson & Johnson, and Aldeyra Therapeutics are investing in biologic innovations and combination therapies that promise improved long-term disease control.

- The demand for biologic and precision therapies is rapidly growing, especially in developed countries where healthcare systems support advanced treatments and where patient awareness is higher. This trend is expected to significantly influence market dynamics over the next decade.

Panuveitis Treatment Market Dynamics

Driver

“Rising Prevalence of Autoimmune Disorders and Increasing Treatment Awareness”

- The increasing incidence of autoimmune diseases such as Behçet's disease, sarcoidosis, and Vogt-Koyanagi-Harada (VKH) syndrome—key contributors to panuveitis—has driven up demand for effective, long-term treatment options.

- For instance, a growing number of ophthalmology centers in North America and Europe are reporting a higher share of uveitis-related consultations, with non-infectious panuveitis accounting for a significant proportion of these visits. This has led to an expansion in research funding and clinical trials focused on novel anti-inflammatory and immunomodulatory therapies.

- Rising awareness campaigns by patient advocacy groups and improved diagnostic access in developing economies are enabling earlier detection and treatment initiation, preventing irreversible vision loss and improving patient quality of life.

- Additionally, as healthcare systems in Asia-Pacific and Latin America modernize, more patients are gaining access to specialty care and advanced therapeutics, supporting the broader market expansion.

Restraint/Challenge

“High Treatment Costs and Limited Access in Low-Income Regions”

- One of the key challenges restraining market growth is the high cost of biologics and advanced immunotherapies, which can be prohibitive in low- and middle-income countries. Treatments like adalimumab or fluocinolone acetonide implants often cost several thousand dollars per patient annually, limiting accessibility for uninsured or underinsured populations.

- Additionally, lack of specialist availability and diagnostic infrastructure in rural or underserved areas can delay diagnosis and contribute to under-treatment, particularly in emerging economies where ophthalmologic care is not uniformly distributed.

- While generic corticosteroids and systemic immunosuppressants remain affordable and widely available, they often come with severe long-term side effects, reducing their desirability for chronic treatment.

- Overcoming these barriers requires government support, international partnerships, and pricing strategies such as tiered pricing models or subsidy programs to improve access to effective treatment options globally.

- Companies focusing on affordable biosimilars, teleophthalmology solutions, and public-private partnerships will be better positioned to tap into these underserved segments and drive sustainable growth.

Panuveitis Treatment Market Scope

The market is segmented on the basis of treatment type, drug class, route of administration, end user, and distribution channel.

• By Treatment Type

On the basis of treatment type, the panuveitis treatment market is segmented into medication and surgery. The medication segment dominates the market with the largest revenue share of 85.6% in 2025, driven by its non-invasive nature and the availability of a wide range of therapeutic options including corticosteroids, immunosuppressants, and biologics. Medications are often the first line of treatment for both infectious and non-infectious panuveitis due to their ability to rapidly control inflammation and preserve vision. This segment is expected to continue its dominance owing to growing adoption of biologics and sustained-release therapies.

The surgery segment is anticipated to witness a CAGR of 7.2% from 2025 to 2032, primarily used in chronic or severe cases where drug therapy fails or complications such as cataracts, vitreous opacities, or glaucoma arise. Surgical interventions, including vitrectomy and cataract extraction, are increasingly supported by advanced imaging and laser technologies, improving outcomes in refractory or vision-threatening cases. While it accounts for a smaller portion of the market, its growth is fueled by increased clinical precision and better postoperative success rates.

• By Drug Class

On the basis of drug class, the market is segmented into corticosteroids, anti-TNF alpha monoclonal antibodies, and others. The corticosteroids segment held the largest market revenue share in 2025, due to their widespread use as a frontline treatment for controlling intraocular inflammation in both acute and chronic settings. Available in multiple forms—topical, oral, injectable, and intravitreal implants—corticosteroids remain a cornerstone of panuveitis management.

The anti-TNF alpha monoclonal antibodies segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing adoption of biologic therapies such as adalimumab in non-infectious, steroid-resistant cases. Biologics offer targeted immune modulation with fewer systemic side effects, making them an emerging choice in complex or relapsing uveitis.

• By Route of Administration

The market is segmented by route of administration into oral, injectable, and others. The injectable segment held the largest revenue share in 2025, driven by the growing use of intravitreal steroid implants and biologics that deliver sustained therapeutic effects directly to the posterior segment of the eye. Injectable treatments are preferred in moderate to severe cases due to their efficacy and localized action.

The oral route is expected to grow steadily, favored for its convenience and systemic control, particularly when bilateral eye involvement or associated systemic disease is present. Oral corticosteroids and immunosuppressants are commonly prescribed as maintenance therapy to prevent flare-ups.

• By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. Hospitals accounted for the largest market share in 2025, owing to the availability of advanced diagnostic tools, experienced ophthalmologists, and access to specialized treatments, including biologics and surgical interventions. Hospitals also manage cases involving complications and require multidisciplinary care.

Specialty clinics are projected to witness the fastest CAGR from 2025 to 2032, driven by the growing preference for focused uveitis centers and private ophthalmology practices offering personalized care, shorter wait times, and continuity of treatment.

• By Distribution Channel

The market is segmented into hospital pharmacies, retail pharmacies, and others. Hospital pharmacies held the largest market revenue share in 2025, largely due to the dispensing of prescription-only biologics and intravitreal steroids that are administered under clinical supervision.

Retail pharmacies are expected to witness significant growth, especially in developing regions, as awareness increases and access to oral corticosteroids and immunosuppressants expands. Over-the-counter options and convenience of local purchase also support this growth.

Panuveitis Treatment Market Regional Analysis

- North America dominates the global panuveitis treatment market with the largest revenue share of 38.7% in 2025, driven by a high prevalence of autoimmune disorders and widespread access to advanced ophthalmic care and biologic therapies.

- The region benefits from a strong presence of major pharmaceutical players, a well-established healthcare infrastructure, and high awareness levels among both physicians and patients regarding early diagnosis and treatment of uveitis-related conditions.

- Additionally, the adoption of cutting-edge treatment options such as intravitreal implants and monoclonal antibodies, along with favorable reimbursement policies, positions North America as the leading hub for innovation and therapeutic adoption in panuveitis management.

U.S. Panuveitis Treatment Market Insight

The U.S. panuveitis treatment market captured the largest revenue share of 79% within North America in 2025, driven by a high prevalence of autoimmune diseases, robust healthcare infrastructure, and access to advanced therapeutics such as biologics and intravitreal implants. Increasing awareness campaigns and the availability of specialized uveitis centers further support early diagnosis and effective management. The integration of multidisciplinary care models involving ophthalmology, immunology, and rheumatology is also contributing to improved patient outcomes and growing treatment adoption.

Europe Panuveitis Treatment Market Insight

The European panuveitis treatment market is projected to expand at a steady CAGR throughout the forecast period, supported by rising cases of chronic inflammatory diseases and strong reimbursement structures for biologic therapies. A growing emphasis on early diagnosis, combined with access to advanced imaging technologies, is fostering effective treatment strategies across the region. Increasing clinical research, especially in countries like Germany, France, and Italy, is further enhancing the availability of innovative treatment options for non-infectious uveitis.

U.K. Panuveitis Treatment Market Insight

The U.K. panuveitis treatment market is expected to grow at a notable CAGR over the forecast period, driven by heightened disease awareness and a well-established public healthcare system supporting early intervention and specialized eye care. Investments in biologic drug trials and strategic collaborations between the NHS and private pharmaceutical firms are enhancing patient access to targeted therapies. Furthermore, the country’s focus on reducing preventable blindness is aligning with improved panuveitis management.

Germany Panuveitis Treatment Market Insight

The German panuveitis treatment market is anticipated to expand considerably during the forecast period, fueled by a strong healthcare infrastructure, access to immunology-based therapeutics, and a high number of practicing ophthalmologists. Government support for orphan drug development and national health initiatives for vision care are accelerating market penetration. The country’s focus on innovative diagnostic modalities is also improving accuracy in panuveitis classification and individualized treatment approaches.

Asia-Pacific Panuveitis Treatment Market Insight

The Asia-Pacific panuveitis treatment market is projected to grow at the fastest CAGR of over 10.2% in 2025, driven by an increasing burden of infectious and autoimmune diseases, a rising geriatric population, and improving access to ophthalmic care in countries such as India, China, and Japan. Government-led health reforms and the expansion of tertiary eye hospitals are facilitating earlier diagnosis and broader treatment availability. The growing adoption of cost-effective generics and the rising number of specialty clinics are also contributing to market growth.

Japan Panuveitis Treatment Market Insight

The Japan panuveitis treatment market is witnessing growth due to the country’s aging population and increasing prevalence of systemic autoimmune conditions like sarcoidosis and Behçet’s disease. Advanced research capabilities and widespread use of imaging diagnostics such as OCT and fluorescein angiography are enabling more precise disease monitoring. Japan’s pharmaceutical industry is also investing in developing and localizing targeted biologic therapies tailored to regional needs, supporting market expansion.

China Panuveitis Treatment Market Insight

The China panuveitis treatment market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid healthcare infrastructure development and increasing awareness of eye diseases. Government programs aimed at enhancing rural eye care access and screening initiatives are boosting early detection rates. Additionally, the growth of domestic pharmaceutical manufacturing and biosimilar production is making advanced treatments more accessible and affordable for a broader patient base.

Panuveitis Treatment Market Share

The Panuveitis Treatment industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Mylan N.V. (U.S.)

- Aldeyra Therapeutics, Inc. (U.S.)

- Bausch Health (Canada)

- Daiichi Sankyo Company (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Allergan plc (Ireland)

- EyePoint Pharmaceuticals, Inc. (U.S.)

- XOMA Corporation (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- HanAll Biopharma (South Korea)

- Vintage Labs (India)

- Jubilant Life Sciences Ltd (India)

- Hikma Pharmaceuticals PLC (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Horizon Therapeutics plc (Ireland)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.