Global Paragonimiasis Treatment Market

Market Size in USD Billion

USD

520.50 Billion

USD

706.87 Billion

2025

2033

USD

520.50 Billion

USD

706.87 Billion

2025

2033

| 2026 - 2033 | |

| USD 520.50 Billion | |

| USD 706.87 Billion | |

| % | |

|

Paragonimiasis Treatment Market Size

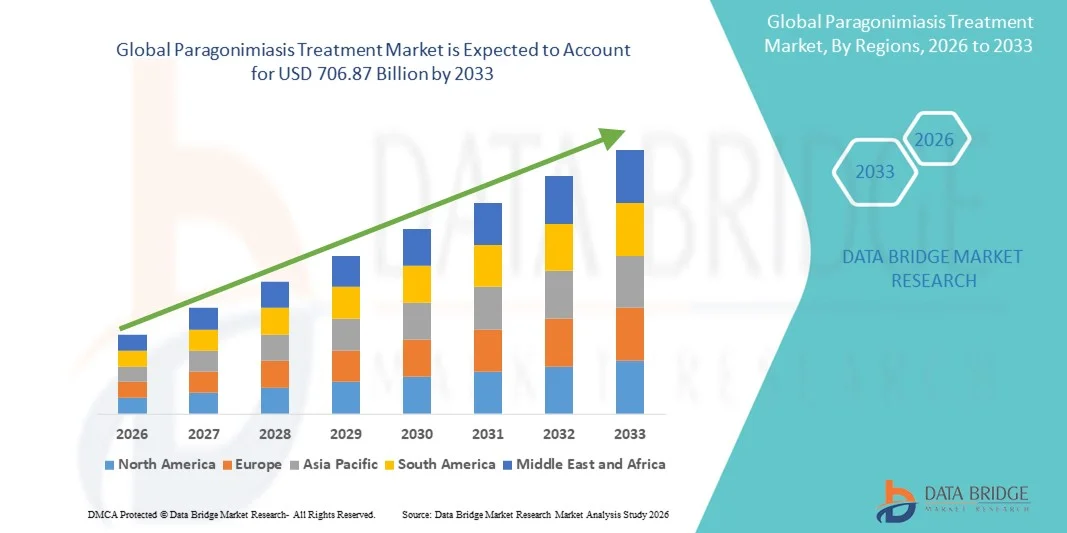

- The global paragonimiasis treatment market size was valued at USD 520.5 billion in 2025 and is expected to reach USD 706.87 billion by 2033, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by increasing awareness of parasitic infections, the rising prevalence of Paragonimiasis in endemic regions, and advancements in diagnostic technologies for early and accurate detection

- Furthermore, growing demand for effective, accessible, and integrated treatment options in both clinical and community healthcare settings is accelerating the uptake of Paragonimiasis Treatment solutions, thereby significantly boosting the industry's growth

Paragonimiasis Treatment Market Analysis

- Paragonimiasis Treatment, offering effective therapeutic options for parasitic lung infections, is increasingly vital in modern healthcare settings due to its efficacy, safety profile, and ability to improve patient outcomes in both endemic and non-endemic regions

- The escalating demand for paragonimiasis treatment is primarily fueled by rising awareness of parasitic infections, increasing prevalence in key regions, and a growing preference for early and reliable treatment interventions

- North America dominated the paragonimiasis treatment market with the largest revenue share of approximately 38.7% in 2025, supported by advanced healthcare infrastructure, high awareness of parasitic infections, and the presence of leading pharmaceutical companies offering specialized treatments. The U.S. accounted for the majority of this share due to early diagnosis, higher healthcare spending, and adoption of innovative treatment approaches

- Asia-Pacific is expected to be the fastest growing region in the Paragonimiasis Treatment market during the forecast period, registering a projected CAGR of around 9.5%, driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about parasitic infections, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia

- The Oral segment dominated with a 50.2% share in 2025, owing to its convenience, patient compliance, and suitability for both outpatient and home-based treatment

Report Scope and Paragonimiasis Treatment Market Segmentation

|

Attributes |

Paragonimiasis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Bayer AG (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Paragonimiasis Treatment Market Trends

Rising Focus on Targeted Therapies and Combination Treatment Approaches

- A key and accelerating trend in the global paragonimiasis treatment market is the increasing development and adoption of targeted therapies and combination treatment regimens. Clinicians are prioritizing therapies that address the parasite directly while minimizing systemic side effects

- For instance, in March 2023, researchers reported that combination therapy using praziquantel alongside corticosteroid administration significantly improved patient recovery times and reduced inflammation in severe cases of lung paragonimiasis. Such studies highlight the shift toward evidence-based combination treatments

- Improved diagnostic capabilities, including imaging and serological testing, are facilitating more personalized treatment plans. Patients can now receive targeted dosing and follow-up therapies tailored to infection severity and symptom presentation

- Combination approaches also help mitigate treatment resistance in recurrent or chronic infections, enhancing clinical outcomes

- The trend is supported by increasing clinical awareness and guidelines recommending multi-drug therapy in endemic regions

- Healthcare providers are adopting structured treatment protocols to improve efficacy, safety, and patient adherence

- Growing pharmaceutical R&D investments in parasitic disease therapies continue to drive innovation in treatment modalities

Paragonimiasis Treatment Market Dynamics

Driver

Increasing Incidence and Awareness of Paragonimiasis Infections

- The rising prevalence of paragonimiasis in endemic regions is a major factor driving market growth. Global migration and increased consumption of undercooked freshwater crustaceans have contributed to higher case reporting

- For instance, in July 2024, the World Health Organization highlighted an uptick in paragonimiasis cases in Southeast Asia, prompting renewed public health campaigns and treatment awareness initiatives

- Improved epidemiological surveillance and mandatory reporting have raised awareness among healthcare providers and patients, resulting in earlier diagnosis and treatment

- The availability of effective anti-parasitic drugs such as praziquantel and triclabendazole supports rapid intervention and recovery

- Increased healthcare spending in emerging economies allows for better access to medications, strengthening treatment uptake

- Patient education programs focusing on proper food handling and hygiene are enhancing compliance with therapeutic regimens

- The growing adoption of combination therapies and supportive care options further contributes to rising demand

Restraint/Challenge

Limited Drug Availability and High Treatment Costs

- Despite market growth, limited access to anti-parasitic drugs and high treatment costs in certain regions pose challenges to wider adoption

- For instance, in November 2022, reports from rural hospitals in Sub-Saharan Africa indicated sporadic availability of praziquantel, resulting in treatment delays for infected patients

- The cost of combination therapies and extended treatment courses can be prohibitive for low-income patients, particularly in developing regions where paragonimiasis is endemic

- Side effects associated with anti-parasitic drugs, including gastrointestinal discomfort or neurological symptoms, may discourage some patients from completing full treatment courses

- Logistical challenges in distributing medications to remote areas further exacerbate access issues

- Healthcare providers are investing in training programs to optimize dosing strategies and improve patient adherence despite cost and availability constraints

- Addressing these challenges through government subsidies, generic drug availability, and international aid programs will be critical to ensure broad and equitable access to treatment and sustained market growth

Paragonimiasis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Paragonimiasis Treatment market is segmented into Anthelmintic Drugs, Anticonvulsants, Surgery, and Others. The Anthelmintic Drugs segment dominated the market with a 47.5% share in 2025, driven by their proven efficacy in eradicating the Paragonimus parasite. These drugs, including praziquantel and triclabendazole, are widely recommended as first-line therapy due to rapid symptom resolution and low hospitalization requirements. Strong clinical adoption, availability in both oral and injectable forms, and inclusion in WHO treatment guidelines reinforce their dominance. Physicians in endemic regions often prioritize anthelmintics for acute and chronic cases, increasing consistent prescription rates. Ongoing research to improve formulations and reduce side effects enhances their clinical preference. Anthelmintic drugs also benefit from extensive public health initiatives that promote early diagnosis and treatment. Healthcare infrastructure improvements in developing regions support wider accessibility. Repeat prescriptions for severe or recurring cases contribute to sustained revenue generation. The segment remains the backbone of paragonimiasis management globally, particularly in Asia and Africa, where incidence rates are highest.

The Surgery segment is expected to witness the fastest CAGR of 12.1% from 2026 to 2033, driven by complex cases with pulmonary or neurological complications. Surgery is increasingly adopted in tertiary care centers to address cysts or lesions that do not respond to pharmacological therapy. Advances in minimally invasive thoracic and neurosurgical procedures reduce recovery time and improve outcomes. Rising awareness among specialists regarding early surgical intervention for severe cases is boosting adoption. Improved diagnostic imaging allows better case selection, minimizing risks. Patient preference for long-term resolution of chronic complications contributes to growth. Hospitals are increasingly equipped with specialized surgical units for parasitic infections. Training programs for surgeons in endemic regions further enhance availability. Technological innovations, such as video-assisted thoracoscopy, are enhancing procedural safety. Expansion of healthcare infrastructure in urban and semi-urban areas accelerates access to surgical treatment. Insurance coverage in emerging economies is gradually increasing reimbursement for such procedures. Overall, surgery is emerging as an important adjunct to drug-based therapy for targeted patient populations.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Biopsy, Serologic Testing, Blood Test, CT Scan, X-ray, Bronchoscopy, and Others. The Serologic Testing segment dominated the market with 44.8% share in 2025, as it allows early and accurate detection of Paragonimus infections. Serology tests detect antibodies in blood, enabling timely initiation of therapy. They are widely used in both hospital and clinic settings due to high sensitivity and minimal invasiveness. Availability of rapid test kits in endemic regions has increased adoption. Healthcare providers prioritize serologic testing for screening and epidemiological surveys. Integration with routine blood work facilitates comprehensive patient evaluation. Continuous advancements in immunoassay technology improve detection accuracy. Standardization of testing protocols enhances reliability and comparability of results. The cost-effectiveness of serology further supports its dominant position. Strong recommendations by global health organizations reinforce clinical adoption. Training programs for laboratory personnel improve test quality. Rising awareness of parasitic infections among physicians and patients drives consistent utilization.

The CT Scan segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, due to its ability to detect pulmonary cysts and neurological complications. High-resolution imaging supports precise diagnosis and guides surgical or pharmacological treatment plans. Increasing availability of CT scanners in hospitals and specialty centers enhances access. Technological improvements in imaging reduce radiation exposure while improving image clarity. Physicians prefer CT scans for complex or atypical cases. The rise of public-private diagnostic partnerships in endemic countries expands service reach. Patient awareness campaigns highlight the importance of imaging for early intervention. Training radiologists in parasite-specific imaging interpretation accelerates adoption. CT imaging complements serologic testing in comprehensive diagnostic workflows. Availability in urban healthcare centers increases patient uptake. Increasing demand for minimally invasive evaluation further supports growth. Overall, CT scans are becoming an integral component of paragonimiasis management.

- By Dosage

On the basis of dosage, the market is segmented into Tablet, Injection, and Others. The Tablet segment dominated with a 49.3% share in 2025, due to ease of administration and widespread use for both acute and chronic infections. Tablets allow outpatient treatment, improving patient compliance and reducing hospitalization. Praziquantel tablets are extensively recommended for their safety and efficacy profile. Physicians often favor tablets for first-line therapy due to standardized dosing and minimal monitoring requirements. Expanded distribution through retail pharmacies enhances accessibility. Tablets are preferred for pediatric and adult patients, allowing flexible dosing schedules. Public health initiatives distributing tablet regimens in endemic areas reinforce demand. Generic availability lowers treatment cost, supporting high adoption rates. Regular use in combination with adjunct therapies strengthens clinical outcomes. Growing awareness of paragonimiasis increases early treatment-seeking behavior. Pharmaceutical companies continue to develop new formulations to improve bioavailability and reduce side effects. Overall, tablets dominate the market due to convenience, efficacy, and affordability.

The Injection segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by severe or complicated cases requiring rapid therapeutic response. Injectable formulations, including intravenous praziquantel, provide immediate systemic absorption. Hospitals and tertiary care centers prioritize injections for patients with neurological or pulmonary complications. Rising incidence of acute symptomatic infections fuels demand for fast-acting injectable therapy. Improved safety profiles and formulation innovations enhance adoption. Expansion of hospital-based infectious disease units increases availability. Injectable therapy is critical for patients unable to tolerate oral medication. Integration into standardized treatment protocols ensures consistent use. Growing physician preference for parenteral therapy in complex cases contributes to growth. Awareness campaigns highlight the benefits of early intervention with injections. Insurance reimbursement in certain regions supports adoption of injectable regimens.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intravenous, and Others. The Oral segment dominated with a 50.2% share in 2025, owing to its convenience, patient compliance, and suitability for both outpatient and home-based treatment. Oral administration is widely preferred for first-line therapy using anthelmintic drugs such as praziquantel and triclabendazole. Physicians favor oral therapy due to standardized dosing, minimal monitoring, and ease of administration across different age groups. Public health programs in endemic regions extensively use oral regimens for mass treatment campaigns. Tablets and suspensions facilitate easy storage and transport, particularly in resource-limited areas. Oral drugs reduce hospitalization time and overall treatment costs, supporting wider adoption. Integration with telemedicine services allows prescription refills and remote adherence monitoring. The availability of generic oral formulations enhances affordability, ensuring higher penetration. Continuous patient education campaigns on proper dosage improve clinical outcomes. Pharmaceutical companies focus on improving bioavailability and palatability for oral drugs. Overall, oral therapy remains the backbone of paragonimiasis management globally.

The Intravenous segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by severe pulmonary, neurological, or systemic cases requiring immediate therapeutic action. IV administration allows rapid drug absorption and precise dosing for critical patients. Hospitals and tertiary care centers prioritize IV therapy for complicated infections. Increasing incidence of acute symptomatic infections in endemic regions fuels adoption. Technological advances in infusion protocols improve safety and reduce adverse effects. Injectable therapy is crucial for patients who cannot tolerate oral medications due to vomiting or gastrointestinal issues. Specialized hospital units in Asia and Africa are expanding availability. Physicians increasingly recommend IV administration for severe or complicated cases. Integration into standardized treatment guidelines ensures consistent use. Rising healthcare infrastructure investment supports growth in tertiary care facilities. Patient monitoring during infusion further ensures clinical efficacy. Overall, IV administration is gaining traction in complex paragonimiasis treatment.

- By Symptoms

On the basis of symptoms, the market is segmented into Headache, Seizures, Bloody Diarrhea, Chest Pain, Shortness of Breath, Malaise, and Others. The Seizures segment dominated with a 38.7% share in 2025, as neurological manifestations of paragonimiasis prompt urgent medical attention. Seizures often indicate cerebral involvement, which is a severe complication requiring specialized treatment. Hospitals with neurology and infectious disease departments handle the majority of such cases. Early detection and treatment prevent long-term complications and improve prognosis. The visible severity of neurological symptoms encourages higher patient engagement with healthcare services. Rising awareness among physicians and caregivers about parasitic neurological complications contributes to higher diagnosis rates. Combination therapy, including anthelmintics and anticonvulsants, is standard for seizure management. Public health campaigns emphasize recognizing neurological symptoms for prompt care. Availability of diagnostic tools such as CT scans and MRI facilitates accurate evaluation. Physicians prefer hospital-based treatment for close monitoring. Overall, seizures represent the most critical and treated symptom in paragonimiasis.

The Chest Pain segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by pulmonary involvement in Paragonimus infections. Chest pain is often associated with pulmonary cysts, pleuritis, or secondary infections. Rising prevalence in endemic regions, especially in Asia, drives the need for effective symptom management. Physicians recommend integrated therapy combining anthelmintic drugs with supportive care for pulmonary manifestations. Increased adoption of imaging technologies such as CT scans aids early detection and treatment planning. Hospitals and specialized clinics are expanding services to manage pulmonary complications. Patient awareness campaigns highlight the importance of early reporting of chest pain symptoms. Improved drug formulations reduce treatment duration and improve compliance. Home-based monitoring programs facilitate adherence and symptom tracking. Training programs for clinicians improve recognition and treatment of pulmonary symptoms. Overall, the chest pain symptom segment is rapidly gaining focus in clinical practice.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated with a 47.5% share in 2025, owing to the availability of specialized infectious disease departments, diagnostic tools, and intensive care facilities. Hospitals manage severe or complicated cases with pulmonary or neurological involvement. The presence of trained infectious disease specialists ensures accurate diagnosis and effective treatment. Combination therapy involving oral and IV medications is commonly administered in hospital settings. High patient inflow, particularly in endemic regions, further reinforces hospital dominance. Public healthcare programs often route patients through hospitals for effective treatment coverage. Hospitals provide continuous monitoring and follow-up for complex cases. Advanced imaging, laboratory services, and supportive care enhance treatment outcomes. Government and private hospitals actively participate in awareness and screening campaigns. Integrated care, including surgery if required, is more readily available in hospitals. Insurance coverage for hospital treatment further strengthens revenue share. Overall, hospitals remain the primary treatment hub for paragonimiasis.

The Clinic segment is expected to witness the fastest CAGR of 11.9% from 2026 to 2033, driven by the increasing number of specialized infectious disease and general practice clinics. Clinics provide easier access for routine diagnosis, follow-up treatment, and medication distribution. Private clinics in urban and semi-urban areas enhance convenience for outpatient care. Telemedicine adoption allows remote consultations and prescription management, improving patient adherence. Early detection programs encourage patients to visit clinics before severe complications develop. Growing awareness of paragonimiasis symptoms supports clinic utilization. Clinics often provide combination therapies under physician supervision. Increased investment in private healthcare infrastructure expands clinic capacity. Flexible appointment scheduling improves patient compliance. Clinics also contribute to public health screening and community outreach programs. Overall, clinics are becoming a fast-growing channel for paragonimiasis management.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated with a 44.3% share in 2025, due to direct availability of prescription medications for severe and complex cases. Hospital pharmacies provide both oral and injectable drugs under physician supervision, ensuring proper dosing and monitoring. Availability of specialized drugs for neurological or pulmonary complications reinforces dominance. Controlled dispensing reduces the risk of misuse or improper administration. Integration with hospital inventory systems ensures consistent supply. Public and private hospitals in endemic regions rely heavily on in-house pharmacies. High patient inflow and prescription volumes contribute to sustained revenue. Hospital pharmacies also support patient education on correct medication use. Government programs often channel essential drugs through hospital pharmacies. Hospitals provide follow-up and refill management for long-term treatment. Overall, hospital pharmacies remain the primary distribution channel for paragonimiasis treatment.

The Online Pharmacy segment is expected to witness the fastest CAGR of 13.6% from 2026 to 2033, driven by convenience, growing internet penetration, and the preference for home delivery of medications. Online platforms enable patients in remote or rural areas to access both oral and injectable therapies. Integration with telemedicine services allows prescription verification and automatic refills. Competitive pricing, doorstep delivery, and discreet packaging enhance adoption. Awareness campaigns highlight the benefits of online pharmacies for chronic or follow-up treatment. Smartphone and internet adoption in emerging markets accelerates segment growth. Specialty drugs, including rare formulations, are increasingly available online. Logistics partnerships improve delivery speed and reliability. Patients benefit from automated reminders for dosage and refill schedules. Expanding e-pharmacy networks improve access in non-urban regions. Online pharmacy adoption supports patient adherence and continuity of care. Overall, online pharmacies are becoming a rapidly growing channel in paragonimiasis treatment.

Paragonimiasis Treatment Market Regional Analysis

- North America dominated the paragonimiasis treatment market with the largest revenue share of approximately 38.7% in 2025

- Supported by advanced healthcare infrastructure, high awareness of parasitic infections, and the presence of leading pharmaceutical companies offering specialized treatments

- The market accounted for the majority of this share due to early diagnosis, higher healthcare spending, and adoption of innovative treatment approaches

U.S. Paragonimiasis Treatment Market Insight

The U.S. paragonimiasis treatment market captured the largest revenue share within North America, driven by high adoption of advanced diagnostic techniques, access to cutting-edge therapeutics, and strong government and private healthcare initiatives targeting parasitic infections. Early intervention programs, awareness campaigns, and investment in infectious disease research further contribute to market growth.

Europe Paragonimiasis Treatment Market Insight

The Europe paragonimiasis treatment market is projected to expand at a steady CAGR throughout the forecast period, driven by increasing healthcare expenditure, growing awareness about parasitic diseases, and improving access to diagnostic and treatment facilities. Countries like Germany, France, and the U.K. are focusing on early detection and specialized care, supporting the adoption of Paragonimiasis Treatment solutions.

U.K. Paragonimiasis Treatment Market Insight

The U.K. paragonimiasis treatment market is expected to grow moderately during the forecast period, supported by robust healthcare infrastructure, increasing investments in infectious disease management, and rising awareness of parasitic infections among clinicians and patients. Public health initiatives and access to specialized treatment centers are further boosting market growth.

Germany Paragonimiasis Treatment Market Insight

The Germany paragonimiasis treatment market is anticipated to expand steadily, fueled by advanced healthcare systems, availability of modern diagnostics, and increasing prevalence of parasitic infections among travelers and immigrant populations. Focus on preventive care and research-driven therapeutics supports the adoption of effective treatment solutions.

Asia-Pacific Paragonimiasis Treatment Market Insight

The Asia-Pacific paragonimiasis treatment market is poised to grow at the fastest CAGR of around 9.5% during the forecast period, driven by increasing healthcare investments, improving access to infectious disease services, rising awareness about parasitic infections, and expanding availability of treatment options in emerging economies such as China, India, and Southeast Asia.

Japan Paragonimiasis Treatment Market Insight

The Japan paragonimiasis treatment market is witnessing growth due to increasing awareness of parasitic infections, government initiatives to improve infectious disease management, and advanced diagnostic capabilities. High healthcare standards and focus on early intervention are contributing to the adoption of effective treatment solutions.

China Paragonimiasis Treatment Market Insight

The China paragonimiasis treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rising healthcare expenditure, increasing prevalence of parasitic infections, improved diagnostic infrastructure, and expanding availability of specialized treatment options. Government programs promoting infectious disease control and strong domestic pharmaceutical capabilities are key growth drivers.

Paragonimiasis Treatment Market Share

The Paragonimiasis Treatment industry is primarily led by well-established companies, including:

• Bayer AG (Germany)

• GlaxoSmithKline (U.K.)

• Pfizer Inc. (U.S.)

• Novartis AG (Switzerland)

• Sanofi S.A. (France)

• Johnson & Johnson (U.S.)

• Takeda Pharmaceutical Company (Japan)

• Merck & Co., Inc. (U.S.)

• AbbVie Inc. (U.S.)

• Boehringer Ingelheim (Germany)

• Lupin Limited (India)

• Cipla Limited (India)

• Sun Pharmaceutical Industries Ltd. (India)

• Hainan Poly Pharm Co., Ltd. (China)

• Zydus Cadila (India)

• F. Hoffmann-La Roche AG (Switzerland)

Latest Developments in Global Paragonimiasis Treatment Market

- In October 2022, a cluster of pulmonary paragonimiasis cases was reported in a native community in Ecuador. After two laborers were diagnosed, health authorities conducted active surveillance — examining sputum and stool samples from dozens of residents — and found eight additional infected individuals. Treatment with Praziquantel was administered, highlighting the continuing endemic risk of paragonimiasis and the need for community‑level awareness and screening

- In March 2023, a case was documented in which pulmonary paragonimiasis was conclusively diagnosed using a newer method: transbronchial lung cryobiopsy (TBLC). This marked the first reported use of TBLC to confirm a Paragonimus westermani infection, offering a more definitive diagnostic alternative for patients with ambiguous or persistent pulmonary symptoms

- In July 2024, researchers published a case report from China describing a patient initially misdiagnosed with a liver abscess — but later found to have extrapulmonary (liver) paragonimiasis. This drawn‑out journey to correct diagnosis underscores the disease’s ability to mimic other conditions and reinforces the necessity for broader clinical vigilance for parasitic infections in endemic areas

- In August 2025, a rare but severe presentation — massive empyema in an adolescent — due to pulmonary paragonimiasis was reported from Korea. The patient required surgical decortication after antiparasitic therapy because of persistent pleural effusion and lung collapse, underlining that paragonimiasis can lead to serious complications and may demand invasive treatment when diagnosis is delayed

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.