Global Passive Fire Protection Coating Market

Market Size in USD Billion

USD

4.85 Billion

USD

6.95 Billion

2025

2033

USD

4.85 Billion

USD

6.95 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.85 Billion | |

| USD 6.95 Billion | |

| % | |

|

Passive Fire Protection Coatings Market Overview

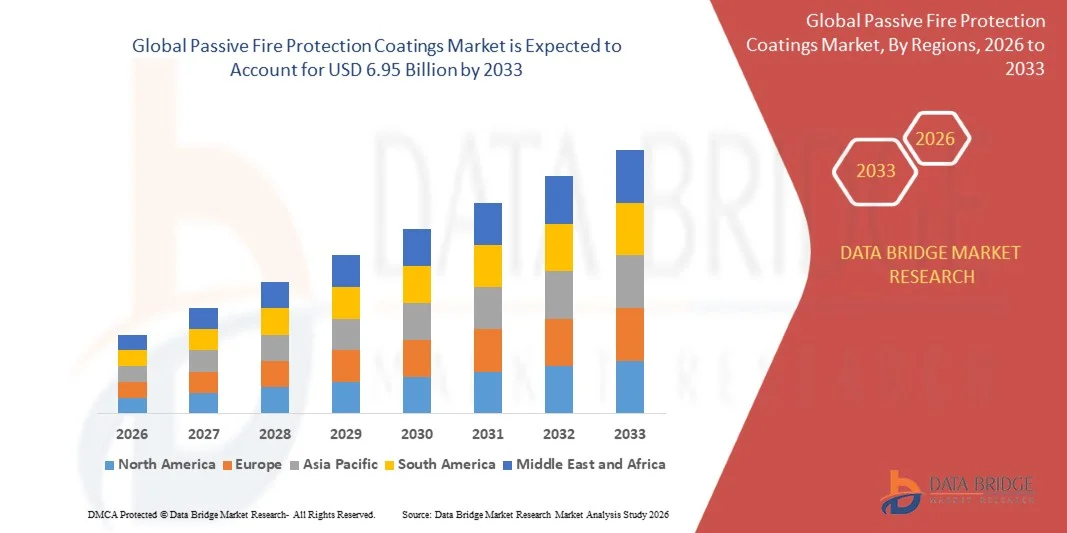

The Passive Fire Protection Coatings Market was valued at USD 4.85 billion in 2025 and is projected to reach USD 6.95 billion by 2033, growing at a CAGR of 4.6% from 2026 to 2033. The market is witnessing steady growth driven by increasing emphasis on fire safety regulations, rapid expansion of infrastructure and construction activities, and rising adoption of high-performance protective coatings across industrial, commercial, and residential sectors.

The growing frequency of fire-related incidents, along with stricter building safety codes and insurance requirements, is pushing governments, contractors, and asset owners to integrate advanced passive fire protection systems into structural steel and critical infrastructure. Intumescent and cementitious coatings are increasingly being used to enhance structural integrity during fire exposure, providing critical evacuation time and reducing property damage in high-risk environments such as oil & gas, marine, and industrial facilities.

Key Market Trends & Insights

- North America dominated the Passive Fire Protection Coatings Market with the largest revenue share of 35.62% in 2025, supported by strict fire safety regulations, large-scale industrial infrastructure, and strong adoption across oil & gas and commercial construction sectors.

- The Intumescent Coating segment led the market with a 52.14% share in 2025, driven by its superior expansion properties under high heat, ability to form an insulating char layer, and strong compatibility with structural steel in modern construction projects.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.1% from 2026 to 2033, fueled by rapid urbanization, infrastructure expansion, and increasing enforcement of fire safety standards across China, India, and Southeast Asia.

- Cementitious Material are the fastest-growing product type, projected to register a CAGR of 6.8%, reflecting the surge in cost-effective and highly durable fireproofing solutions in heavy industrial environments.

- The Solvent-Based Protection Coating segment dominated the technology category with a 57.63% revenue share in 2025, led by its superior adhesion properties, high durability, and strong resistance under extreme environmental and fire exposure conditions.

- Construction accounted for 44.85% of the market, preferred by rapid urbanization, expansion of high-rise infrastructure, and stringent fire safety regulations in commercial and residential buildings

- The Oil & Gas segment is the fastest-growing application category, with a CAGR of 6.9%, driven by increasing safety requirements in high-risk exploration, refining, and offshore operations.

Market Size & Forecast

- Global Market Value (2025): USD 4.85 Billion

- Expected Market Value (2033): USD 6.95 Billion

- Forecast CAGR (2026–2033): 4.6%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Passive Fire Protection Coatings Market Segmentation

|

Attributes |

Passive Fire Protection Coatings Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Akzo Nobel N.V., (Netherlands) · Jotun A/S, (Norway) · Hempel A/S, (Denmark) · The Sherwin-Williams Company, (U.S.) · PPG Industries, Inc., (U.S.) · RPM International Inc., (U.S.) · Carboline Company, (U.S.) · Sika AG, (Switzerland) · BASF SE, (Germany) · 3M (U.S.) · Hilti Aktiengesellschaft, (Liechtenstein) · Fosroc International Limited, (U.K.) · Promat International N.V. (Belgium) · Etex Group NV, (Belgium) · Isolatek International, (U.S.) · Contego International Inc., (U.S.) · Nullifire (Tremco CPG), (U.K.) · Tremco CPG Inc., (U.S.) · Teknos Group Oy, (Finland) · Flame Control Coatings LLC, (U.S.) |

|

Market Opportunities |

· Rapid expansion of large-scale infrastructure projects · Growing retrofit and renovation activities in aging commercial and industrial buildings · Increasing adoption of stringent fire safety regulations in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Passive Fire Protection Coatings Market Trends

Trend: Increasing Adoption in High-Rise and Mega Infrastructure Projects

Passive fire protection coatings are witnessing strong uptake in large-scale infrastructure developments, especially in high-rise commercial towers, airports, industrial plants, and transport hubs, where structural steel fire resistance is a critical safety requirement. These coatings, particularly intumescent and cementitious systems, are being increasingly specified at the design stage to ensure compliance with evolving fire safety standards and building codes. Their ability to expand under high heat and form an insulating char layer helps maintain load-bearing capacity during fire incidents, significantly improving evacuation time and minimizing structural collapse risk. This trend is further reinforced by urbanization-driven construction booms and the need for faster, safer construction methodologies.

For instance, major metro rail corridors and skyscraper developments in rapidly growing urban centers are increasingly integrating certified passive fire protection coating systems as a mandatory safety layer.

Passive Fire Protection Coatings Market Dynamics

Key Market Driver: Strengthening Global Fire Safety Regulations and Industrial Compliance

The global demand for passive fire protection coatings is strongly driven by increasingly stringent fire safety regulations across construction, oil & gas, marine, and industrial sectors, where failure to comply can result in severe legal, financial, and human safety consequences. Regulatory bodies are continuously upgrading fire resistance standards for structural steel, hydrocarbon fire scenarios, and critical infrastructure protection, pushing developers and operators to adopt certified coating systems as a standard safety measure. In addition, insurance requirements and risk mitigation strategies are playing a major role in encouraging proactive investment in fireproofing technologies. Industries such as offshore oil platforms, petrochemical plants, and power generation facilities are particularly reliant on these coatings due to their high-risk operational environments.

For instance, updated offshore safety frameworks and revised commercial building fire codes in major economies are accelerating large-scale deployment of advanced intumescent coating systems across both new construction and retrofit projects.

Key Restraint/Challenge: High Cost of Advanced Fire Protection Coating Systems

Despite strong demand, the market faces a notable restraint in the form of high overall lifecycle costs associated with advanced passive fire protection coating systems, which include material procurement, surface preparation, specialized application techniques, and skilled labor requirements. Intumescent coatings, especially those designed for long fire-resistance durations, require precise thickness control and certified application processes, which significantly increase installation complexity and project timelines. In addition, periodic inspection, maintenance, and potential re-coating over the asset lifecycle further increase total ownership costs, making adoption challenging for small and mid-scale construction projects. These cost barriers are more pronounced in developing regions where budget constraints often lead to preference for conventional fireproofing methods.

For instance, large offshore oil and gas installations and high-spec industrial facilities often incur substantial expenditures due to the need for certified applicators and stringent compliance testing during coating application and inspection phases.

Key Market Opportunity: Expansion in Sustainable and High-Performance Coating Technologies

A major growth opportunity in the passive fire protection coatings market lies in the rapid shift toward sustainable, low-emission, and high-efficiency coating technologies that align with global green building initiatives and environmental regulations. Manufacturers are increasingly focusing on developing water-based, low-VOC, and halogen-free formulations that reduce environmental impact while maintaining or improving fire resistance performance. At the same time, advancements in nanotechnology and polymer chemistry are enabling thinner coatings with higher thermal stability, faster curing times, and improved durability under harsh environmental conditions. These innovations are expanding application possibilities beyond traditional sectors into green-certified buildings, renewable energy infrastructure, and smart industrial facilities.

For instance, adoption of eco-friendly intumescent coatings is rising in LEED-certified commercial complexes and modern infrastructure projects aiming to meet sustainability and carbon reduction targets.

Passive Fire Protection Coatings Market Scope

The passive fire protection coatings market is segmented on the basis of product type, technology, application, and end user.

- By Product Type

On the basis of product type, the Passive Fire Protection Coatings Market is segmented into cementitious material, intumescent coating, fireproofing cladding, and others. The Intumescent Coating segment dominated the market with a 52.14% share in 2025, owing to its superior expansion properties under high heat, ability to form an insulating char layer, and strong compatibility with structural steel in modern construction projects. These coatings are widely preferred in commercial buildings, industrial facilities, and offshore structures due to their lightweight nature and aesthetic flexibility compared to bulky fireproofing alternatives. They also enable architects to maintain exposed steel designs without compromising fire safety compliance. Increasing demand for high-rise infrastructure and stringent fire resistance regulations further strengthens their dominance. Continuous advancements in thin-film intumescent technologies are improving durability, weather resistance, and application efficiency. The segment remains the most widely specified solution across global fire safety engineering projects.

The Cementitious Material segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by rising demand for cost-effective and highly durable fireproofing solutions in heavy industrial environments. These materials are extensively used in oil & gas plants, refineries, tunnels, and power generation facilities where extreme fire exposure conditions exist. Their high thermal stability and ability to provide thick passive protection make them ideal for high-risk infrastructure applications. Increasing investment in industrial expansion and energy infrastructure in emerging economies is significantly supporting adoption. In addition, improvements in spray application techniques are enhancing installation speed and reducing labor costs. For instance, large-scale refinery and petrochemical projects are increasingly deploying cementitious systems for structural fireproofing in high-temperature zones.

- By Technology

On the basis of technology, the Passive Fire Protection Coatings Market is segmented into water-based protection coating and solvent-based protection coating. The Solvent-Based Protection Coating segment dominated the market with a 57.36% share in 2025, owing to its superior adhesion properties, high durability, and strong resistance under extreme environmental and fire exposure conditions. These coatings are widely used in offshore oil platforms, heavy industrial facilities, and infrastructure projects where long-term performance and harsh operating conditions are critical. Their ability to form dense protective films ensures enhanced fire resistance and structural stability. Despite environmental concerns, they remain widely adopted in applications requiring maximum performance reliability. Established supply chains and proven field performance further reinforce their dominance. Continuous formulation improvements are also enhancing their compliance with evolving safety standards.

The Water-Based Protection Coating segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing environmental regulations and demand for low-VOC, sustainable fire protection solutions. These coatings are gaining traction in commercial construction, residential projects, and green-certified buildings due to their reduced environmental impact and safer application process. Rapid advancements in polymer technology are improving their fire resistance and durability, narrowing the performance gap with solvent-based systems. Governments and regulatory bodies are promoting eco-friendly construction materials, further accelerating adoption. For instance, water-based intumescent coatings are increasingly being used in modern commercial complexes and public infrastructure projects targeting sustainability certifications.

- By Application

On the basis of application, the Passive Fire Protection Coatings Market is segmented into oil & gas, construction, aerospace, electrical and electronics, automotive, textile, furniture, warehousing, and others. The Construction segment dominated the market with a 44.85% share in 2025, driven by rapid urbanization, expansion of high-rise infrastructure, and stringent fire safety regulations in commercial and residential buildings. Passive fire protection coatings are extensively used on structural steel to enhance fire resistance and ensure occupant safety during fire incidents. Increasing investments in smart cities, metro rail systems, and commercial real estate development are further strengthening demand. The segment benefits from mandatory building codes requiring certified fireproofing systems. Continuous infrastructure modernization in emerging economies also supports long-term growth.

The Oil & Gas segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing safety requirements in high-risk exploration, refining, and offshore operations. These environments demand advanced fire protection systems capable of withstanding hydrocarbon fire scenarios and extreme temperatures. Rising global energy demand and expansion of LNG terminals, refineries, and petrochemical plants are significantly boosting adoption. Regulatory frameworks are becoming more stringent, requiring certified passive fire protection systems across critical assets. For instance, offshore drilling platforms and LNG storage facilities are increasingly integrating high-performance coatings to ensure structural integrity during fire emergencies.

- By End User

On the basis of end user, the Passive Fire Protection Coatings Market is segmented into building & construction, oil & gas, transportation, and others. The Building & Construction segment dominated the market with a 46.92% share in 2025, driven by large-scale infrastructure development, increasing fire safety compliance, and widespread adoption of steel-framed structures in modern architecture. Passive fire protection coatings are essential for ensuring structural stability and meeting regulatory fire resistance requirements in commercial and residential buildings. Growing investments in urban infrastructure, including skyscrapers, airports, and public facilities, further reinforce demand. The segment benefits from continuous modernization of building codes across major economies.

The Transportation segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by rising investments in railways, metro systems, aviation infrastructure, and marine transport safety. These systems require advanced fire protection solutions to ensure passenger safety and asset protection in confined and high-risk environments. Increasing adoption of lightweight steel structures in transport infrastructure is further boosting coating usage. Governments are strengthening safety standards across transport networks, accelerating demand for certified fireproofing systems. For instance, metro rail tunnels and airport terminals are increasingly integrating advanced passive fire protection coatings for enhanced emergency resilience.

Passive Fire Protection Coatings Market Regional Analysis

North America dominated the Passive Fire Protection Coatings Market with the largest revenue share of 35.62% in 2025, supported by strict fire safety regulations, large-scale industrial infrastructure, and strong adoption across oil & gas and commercial construction sectors. The region also benefits from high adoption of intumescent and epoxy-based fireproofing systems across commercial buildings, offshore platforms, and critical energy facilities. Increasing investments in infrastructure modernization and stringent insurance compliance requirements continue to drive large-scale deployment of certified passive fire protection solutions. Growing emphasis on safety-driven design practices and retrofitting of aging infrastructure further strengthens North America’s leadership position in the global market.

U.S. Passive Fire Protection Coatings Market Insight

The U.S. passive fire protection coatings market is expanding steadily due to stringent fire safety regulations, large-scale construction activities, and strong presence of oil, gas, and industrial manufacturing sectors. Increasing adoption of high-performance intumescent coatings in skyscrapers, commercial complexes, and energy facilities is driving market growth. The country’s strong focus on workplace safety standards and disaster risk mitigation is further accelerating demand. Moreover, continuous investments in infrastructure resilience and modernization of existing buildings are reinforcing the use of advanced passive fire protection systems.

Europe Passive Fire Protection Coatings Market Insight

The Europe passive fire protection coatings market holds a significant share globally, supported by strict regulatory frameworks, advanced construction practices, and strong emphasis on sustainability and building safety. Widespread use of fire-resistant coatings in commercial infrastructure, industrial plants, and transport facilities is driving regional demand. Increasing investments in green buildings and energy-efficient infrastructure are also supporting adoption of low-emission coating systems. Furthermore, continuous technological advancements and strong enforcement of fire safety standards continue to strengthen Europe’s market position.

U.K. Passive Fire Protection Coatings Market Insight

The U.K. passive fire protection coatings market is growing steadily, driven by stringent building regulations, increasing construction of high-rise buildings, and strong focus on fire safety compliance. Rising adoption of intumescent coatings in commercial and residential infrastructure is supporting market expansion. In addition, growing renovation and retrofitting activities in older buildings are increasing demand for modern fire protection solutions. Integration of advanced coating technologies and strong emphasis on sustainable construction practices are further enhancing market growth in the country.

Germany Passive Fire Protection Coatings Market Insight

The Germany passive fire protection coatings market is expanding due to strong industrial infrastructure, advanced engineering capabilities, and strict enforcement of fire safety regulations. The automotive, manufacturing, and construction sectors are key end users driving demand for high-performance coating systems. Increasing focus on sustainable construction and energy-efficient buildings is also supporting adoption of eco-friendly fire protection coatings. Continuous innovation in material science and strong emphasis on industrial safety standards further strengthen market growth in Germany.

Asia-Pacific Passive Fire Protection Coatings Market Insight

The Asia-Pacific passive fire protection coatings market is expected to witness rapid growth, driven by large-scale infrastructure development, urbanization, and increasing industrial expansion across emerging economies. Rising awareness of fire safety standards and growing investments in commercial construction, oil & gas, and transportation infrastructure are supporting regional demand. Adoption of advanced coating technologies is increasing due to stricter government regulations and modernization of building codes. In addition, expanding industrial bases in countries such as China and India are significantly boosting market growth.

Japan Passive Fire Protection Coatings Market Insight

The Japan passive fire protection coatings market is experiencing steady growth due to strong emphasis on disaster prevention, advanced construction practices, and high safety standards. Increasing adoption of fire-resistant coatings in commercial buildings, industrial facilities, and transportation infrastructure is driving demand. The country’s focus on earthquake and fire-resilient infrastructure further supports market expansion. In addition, continuous technological innovation and use of high-performance materials are strengthening the adoption of advanced passive fire protection systems in Japan.

China Passive Fire Protection Coatings Market Insight

The China passive fire protection coatings market is growing rapidly, supported by large-scale urban development, expanding industrial infrastructure, and strict government fire safety regulations. Rising construction of high-rise buildings, commercial complexes, and energy facilities is significantly boosting demand for fire-resistant coatings. Increasing investment in oil & gas, petrochemical, and transportation infrastructure is further accelerating market growth. In addition, growing adoption of advanced, cost-effective coating solutions and strong focus on public safety are positioning China as a key growth market globally.

Passive Fire Protection Coatings Market Share

The passive fire protection coatings industry is primarily led by well-established companies, including:

- Akzo Nobel N.V., (Netherlands)

- Jotun A/S, (Norway)

- Hempel A/S, (Denmark)

- The Sherwin-Williams Company, (U.S.)

- PPG Industries, Inc., (U.S.)

- RPM International Inc., (U.S.)

- Carboline Company, (U.S.)

- Sika AG, (Switzerland)

- BASF SE, (Germany)

- 3M (U.S.)

- Hilti Aktiengesellschaft, (Liechtenstein)

- Fosroc International Limited, (U.K.)

- Promat International N.V. (Belgium)

- Etex Group NV, (Belgium)

- Isolatek International, (U.S.)

- Contego International Inc., (U.S.)

- Nullifire (Tremco CPG), (U.K.)

- Tremco CPG Inc., (U.S.)

- Teknos Group Oy, (Finland)

- Flame Control Coatings LLC, (U.S.)

Latest Developments in Passive Fire Protection Coatings Market

- In March 2025, Sherwin-Williams announced continued expansion of its Firetex intumescent coatings portfolio, strengthening its passive fire protection offering for steel structures used in commercial and energy infrastructure projects. The development focuses on improving fire resistance performance, application efficiency, and compliance with evolving global safety standards, particularly for offshore and high-rise applications. This update reinforces the company’s strategy to enhance protective coatings for critical infrastructure resilience

- In September 2024, AkzoNobel highlighted advancements in its International® passive fire protection coatings range, including improved durability and extended fire protection performance for hydrocarbon and cellulosic fire scenarios. The development supports broader use in oil & gas facilities, industrial plants, and marine infrastructure, where high-performance fire resistance is essential. The innovation also aligns with the company’s sustainability goals through improved coating efficiency and lifecycle performance

- In June 2023, Hempel expanded its Hempafire passive fire protection product line, enhancing its water-based intumescent coatings designed for structural steel protection in commercial buildings and industrial environments. The update focuses on reducing environmental impact while maintaining high fire resistance ratings and improving application flexibility. This development reflects increasing demand for sustainable fire protection solutions in modern construction projects

- In November 2022, Jotun strengthened its SteelMaster passive fire protection portfolio, supporting increased demand for high-performance coatings in offshore, energy, and infrastructure sectors. The enhancement focuses on improving fire resistance efficiency, faster application, and long-term durability under extreme environmental conditions. This development reinforces Jotun’s position in critical fire safety applications across industrial assets

- In May 2021, PPG announced developments in its fire protection coatings business unit, focusing on improved intumescent coating technologies designed for structural steel protection in commercial and industrial construction. The initiative emphasizes enhanced fire resistance performance, easier application processes, and compliance with global fire safety regulations. This development supports increasing global demand for certified passive fire protection systems in high-risk infrastructure

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Passive Fire Protection Coating Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Passive Fire Protection Coating Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Passive Fire Protection Coating Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.