Global Patient Monitoring Systems Market

Market Size in USD Billion

USD

56.65 Billion

USD

125.93 Billion

2024

2032

USD

56.65 Billion

USD

125.93 Billion

2024

2032

| 2025 - 2032 | |

| USD 56.65 Billion | |

| USD 125.93 Billion | |

| % | |

|

Patient Monitoring Systems Market Size

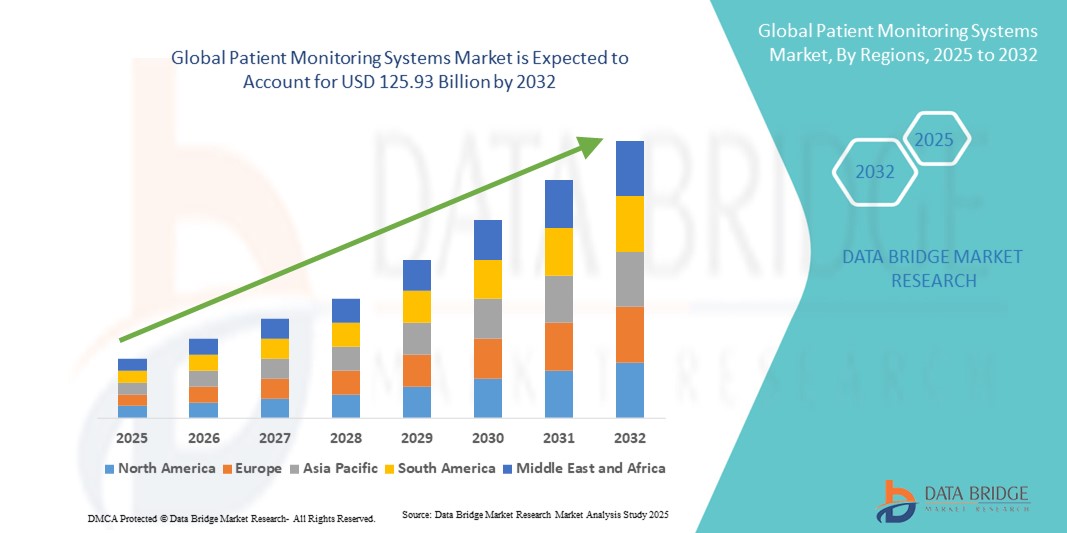

- The global patient monitoring systems market size was valued at USD 56.65 billion in 2024 and is expected to reach USD 125.93 billion by 2032, at a CAGR of 10.50% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced healthcare technologies and increasing emphasis on remote patient care, leading to higher demand for real-time patient monitoring solutions in hospitals, clinics, and home care settings

- Furthermore, rising prevalence of chronic diseases, aging populations, and the need for continuous monitoring of vital signs are driving the adoption of patient monitoring systems

Patient Monitoring Systems Market Analysis

- Patient monitoring systems, offering continuous and real-time tracking of vital signs and health parameters, are increasingly vital components of modern healthcare delivery in hospitals, clinics, and homecare settings due to their enhanced accuracy, timely alerts, and seamless integration with electronic health records and digital health platforms

- The escalating demand for patient monitoring systems is primarily driven by the increasing prevalence of chronic diseases, growing geriatric population, rising need for continuous health monitoring, and the adoption of advanced digital health technologies. Hospitals, clinics, and home healthcare providers are increasingly relying on patient monitoring devices to ensure timely detection of critical health conditions, improve patient outcomes, and reduce hospital readmissions

- North America dominated the patient monitoring systems market with the largest revenue share of 35.02% in 2024, supported by advanced healthcare infrastructure, strong R&D activities, early adoption of innovative monitoring technologies, and favorable reimbursement policies. The U.S. remains the largest contributor within the region, experiencing substantial growth due to widespread deployment of continuous monitoring devices, wearable sensors, and integrated digital health platforms in hospitals, specialty clinics, and home healthcare settings

- Asia-Pacific is expected to be the fastest-growing region in the patient monitoring systems market during the forecast period, driven by increasing urbanization, rising healthcare access, expansion of hospital networks, and growing awareness about chronic disease management in emerging economies such as China, India, and Japan. The region’s rising disposable incomes, government initiatives for digital health adoption, and increasing investments in healthcare infrastructure further accelerate market growth

- The On-Premise segment dominated the patient monitoring systems market with largest market revenue share of 52.1% in 2024, owing to its reliability, secure storage of sensitive patient data, and seamless integration with existing hospital IT infrastructure. Healthcare facilities, particularly in intensive care units and high-risk wards, prefer on-premise systems to ensure uninterrupted monitoring and quick local access to critical patient information

Report Scope and Patient Monitoring Systems Market Segmentation

|

Attributes |

Patient Monitoring Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Patient Monitoring Systems Market Trends

Enhanced Patient Care Through Advanced Monitoring Technologies

- A significant and accelerating trend in the global Patient Monitoring Systems market is the increasing adoption of integrated monitoring solutions that combine wearable sensors, continuous monitoring devices, and centralized data platforms. This integration is significantly enhancing patient care, enabling healthcare providers to track vital signs, detect anomalies early, and intervene promptly

- For instance, advanced multi-parameter bedside monitors and wireless wearable sensors allow real-time monitoring of heart rate, oxygen saturation, blood pressure, and other critical parameters, facilitating timely clinical decisions and reducing hospital readmissions. Similarly, remote monitoring platforms provide continuous oversight for patients in homecare settings, supporting chronic disease management and post-discharge care

- Integration of patient monitoring systems with electronic health records (EHR) and hospital information systems enables seamless data flow, improving clinical workflows, enhancing accuracy in diagnosis, and supporting predictive analytics for better patient outcomes. Real-time alerts and automated data visualization features ensure clinicians can prioritize critical cases efficiently

- The centralization of monitoring data through interoperable platforms allows healthcare providers to manage multiple patients across wards, clinics, or remote locations, creating a unified and proactive healthcare management experience. Hospitals and specialty clinics can use these platforms to optimize staff allocation and reduce response times in emergency situations

- This trend towards more intelligent, connected, and patient-centric monitoring systems is fundamentally reshaping expectations for hospital and home healthcare standards. Consequently, companies such as Philips, GE Healthcare, and Medtronic are developing advanced monitoring solutions with integrated analytics, remote monitoring capabilities, and mobile connectivity

- The demand for patient monitoring systems that provide comprehensive, real-time health insights is growing rapidly across both clinical and homecare settings, as healthcare providers increasingly prioritize early detection, continuous patient oversight, and enhanced operational efficiency

Patient Monitoring Systems Market Dynamics

Driver

Growing Need Due to Rising Healthcare Monitoring and Chronic Disease Management

- The increasing prevalence of chronic diseases, coupled with the rising demand for continuous patient monitoring in hospitals and homecare settings, is a significant driver for the heightened adoption of Patient Monitoring Systems

- For instance, in 2024, Philips Healthcare and GE Healthcare announced advancements in remote patient monitoring platforms, integrating wearable sensors and cloud-based data analytics for real-time tracking of vital parameters. Such innovations by key companies are expected to propel the Patient Monitoring Systems industry growth during the forecast period

- As healthcare providers aim to improve patient outcomes and reduce hospital readmissions, Patient Monitoring Systems offer advanced features such as real-time alerts, automated data recording, and trend analysis, providing a compelling upgrade over traditional episodic monitoring

- Furthermore, the growing emphasis on preventive care and telemedicine is making Patient Monitoring Systems an integral component of healthcare delivery, enabling clinicians to remotely track patients’ conditions and intervene proactively

- The convenience of continuous monitoring, remote data accessibility, and integration with electronic health record (EHR) systems are key factors driving the adoption of Patient Monitoring Systems across hospitals, specialty clinics, and home healthcare settings. Increasing awareness among patients and healthcare professionals further supports market expansion

Restraint/Challenge

Concerns Regarding Data Security and High Initial Costs

- Concerns surrounding data privacy and cybersecurity of connected patient monitoring devices pose a significant challenge to broader market penetration. As Patient Monitoring Systems rely on network connectivity and software platforms, they are susceptible to data breaches and unauthorized access, raising concerns among healthcare providers and patients regarding sensitive medical information

- For instance, reports of vulnerabilities in medical IoT devices have made some institutions cautious in adopting fully connected monitoring solutions

- Addressing these concerns through secure encryption, HIPAA-compliant protocols, and regular software updates is crucial for building trust

- In addition, the relatively high initial cost of advanced patient monitoring systems compared to conventional monitoring methods can be a barrier for smaller clinics or budget-conscious healthcare facilities. While entry-level solutions are becoming more affordable, premium systems with integrated analytics, remote connectivity, and wearable sensors often carry higher price points

- While costs are gradually decreasing, the perceived premium for advanced monitoring technology may still hinder widespread adoption, particularly in emerging regions or smaller healthcare establishments

- Overcoming these challenges through enhanced cybersecurity measures, staff training, patient education, and development of cost-effective monitoring solutions will be vital for sustained growth in the global Patient Monitoring Systems market

Patient Monitoring Systems Market Scope

The market is segmented on the basis of product, type, process, deployment, and end use.

- By Product

On the basis of product, the patient monitoring systems market is segmented into hemodynamic, neuro monitoring, cardiac, fetal and neonatal, respiratory, multi parameter, remote patient, weight, temperature, and urine output monitoring devices. The multi parameter monitoring devices segment dominated the largest market revenue share of 38.7% in 2024, driven by its ability to monitor multiple vital signs simultaneously, reducing the need for separate devices and enhancing clinical efficiency. Hospitals and critical care units rely on these systems for continuous patient monitoring, early detection of complications, and streamlined workflow. Integration with hospital IT systems, advanced data analytics, and bedside automation further strengthens the segment’s leadership.

The Remote Patient Monitoring Devices segment is expected to witness the fastest CAGR of 19.5% from 2025 to 2032, fueled by the increasing adoption of telemedicine, home healthcare, and chronic disease management solutions. Remote monitoring devices enable continuous vital sign tracking, reduce hospital readmissions, and allow real-time communication with clinicians. Technological advancements in wearable sensors, mobile applications, and cloud-based platforms further accelerate adoption. Patient preference for home-based care and the growing geriatric population also support rapid market growth.

- By Type

On the basis of type, the patient monitoring systems market is segmented into vibration, thermal, motor current, alarm, and GPS. The Alarm-based monitoring systems segment dominated the largest market revenue share of 41.2% in 2024, owing to its ability to provide immediate alerts in case of abnormal patient conditions, enabling rapid clinical intervention. Hospitals and intensive care units heavily depend on these systems to enhance patient safety, reduce response time, and prevent critical events. Integration with electronic health records, real-time monitoring, and central nurse stations strengthens its market presence.

The Vibration-based monitoring segment is expected to witness the fastest CAGR of 18.8% from 2025 to 2032, driven by the growing demand for non-invasive, continuous monitoring in home and ambulatory care. Vibration-based devices track vital signs like respiration and heart rate without causing patient discomfort. Wearable and portable solutions, coupled with enhanced mobility and ease-of-use, are key factors contributing to this segment’s rapid adoption. Increasing awareness among patients and healthcare providers about the benefits of continuous, real-time monitoring further supports market growth. In addition, advancements in sensor accuracy and battery life are enhancing the reliability and convenience of vibration-based monitoring systems.

- By Process

On the basis of process, the patient monitoring systems market is segmented into online and portable. The Online process segment dominated the largest market revenue share of 44.5% in 2024, as it allows real-time monitoring and centralized data management. Hospitals and ICUs benefit from online monitoring for continuous assessment of patient conditions, predictive analytics, and timely interventions. Integration with hospital IT infrastructure, cloud connectivity, and high-throughput monitoring platforms enhances clinical efficiency and operational workflow.

The portable segment is expected to witness the fastest CAGR of 17.9% from 2025 to 2032, fueled by the growing demand for bedside, mobile, and home-based monitoring solutions. These portable devices offer significant flexibility, allowing seamless patient transfers, rapid response in emergency care, and effective at-home health monitoring. Their compact design, combined with wireless connectivity and extended battery life, enables continuous and reliable patient monitoring across diverse healthcare settings. Healthcare providers increasingly favor portable systems for their ease of use, quick deployment, and ability to deliver real-time data. Moreover, the rising adoption of mobile and wearable health technologies further supports the expansion of this segment.

- By Deployment Type

On the basis of deployment type, the patient monitoring systems market is segmented into on-premise and cloud. The on-premise segment dominated the largest market revenue share of 52.1% in 2024, owing to its reliability, secure storage of sensitive patient data, and seamless integration with existing hospital IT infrastructure. Healthcare facilities, particularly in intensive care units and high-risk wards, prefer on-premise systems to ensure uninterrupted monitoring and quick local access to critical patient information. Strong compliance with regulatory standards, robust data protection, and real-time monitoring capabilities further reinforce the segment’s dominance. In addition, hospitals and clinics rely on on-premise solutions for handling complex multi-parameter monitoring, ensuring accurate and timely interventions. The ability to customize and control system configurations locally also adds to its appeal among large healthcare providers.

The cloud segment is expected to witness the fastest CAGR of 20.2% from 2025 to 2032, driven by the rising adoption of telehealth, remote patient monitoring, and centralized data analytics. Cloud-based systems provide clinicians with the flexibility to access patient data from multiple locations, enabling better collaboration across departments and healthcare networks. The integration of AI-driven insights, predictive analytics, and mobile device compatibility enhances patient care and operational efficiency. Scalability, cost-effectiveness, and simplified maintenance make cloud solutions attractive for hospitals, home healthcare providers, and ambulatory care settings. The increasing trend of remote consultations and hospital-at-home initiatives further accelerates the adoption of cloud-based patient monitoring systems.

- By End Use

On the basis of end use, the patient monitoring systems market is segmented into hospitals and clinics, home setting, and ambulatory surgical centres. The hospitals and clinics segment dominated the largest market revenue share of 61.3% in 2024, attributed to advanced healthcare infrastructure, high patient throughput, and the critical need for continuous monitoring in intensive and critical care units. Hospitals rely on these systems to optimize patient management, enable early detection of complications, and improve overall operational efficiency. Integration with hospital IT systems, electronic medical records, and bedside monitoring devices further strengthens the segment’s leadership. In addition, healthcare facilities use these systems to support specialized departments such as cardiology, neurology, and neonatal care, ensuring precise and timely interventions.

The home setting segment is expected to witness the fastest CAGR of 21.5% from 2025 to 2032, fueled by the growing preference for home healthcare, telemedicine, and remote patient monitoring solutions. Wearable devices, connected health apps, and cloud-based platforms enable continuous monitoring of chronic conditions while providing real-time clinician access for timely intervention. Factors such as the increasing geriatric population, convenience for patients, and the expansion of hospital-at-home programs are major drivers. Remote monitoring also supports reduced hospital readmissions, cost savings, and enhanced patient engagement, making this segment a key growth area in the patient monitoring systems market.

Patient Monitoring Systems Market Regional Analysis

- North America dominated the patient monitoring systems market with the largest revenue share of 35.02% in 2024, supported by advanced healthcare infrastructure, strong R&D activities, early adoption of innovative monitoring technologies, and favorable reimbursement policies

- Hospitals, specialty clinics, and home healthcare providers are increasingly deploying continuous monitoring devices, wearable sensors, and integrated digital health platforms

- This trend is driven by the growing need for real-time patient monitoring, early detection of critical conditions, and improved chronic disease management, which collectively enhance patient outcomes and reduce hospital readmissions. The region’s technologically inclined population, combined with strong government initiatives promoting digital health, further strengthens market adoption

U.S. Patient Monitoring Systems Market Insight

The U.S. patient monitoring systems market captured the largest revenue share within North America in 2024, fueled by the widespread deployment of wearable devices, wireless monitoring platforms, and integrated digital health solutions across hospitals and homecare settings. Increasing prevalence of chronic diseases, rising geriatric population, and the growing focus on remote patient monitoring are driving demand for advanced patient monitoring systems. The country’s well-established healthcare ecosystem, coupled with favorable reimbursement policies and strong technology adoption, further supports market growth. Continuous innovation in monitoring devices and analytics platforms is enabling more accurate and timelier patient care, positioning the U.S. as the dominant contributor in the region.

Europe Patient Monitoring Systems Market Insight

The Europe patient monitoring systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing focus on high-quality healthcare services and growing adoption of digital health technologies. Hospitals and clinics across the region are investing in continuous monitoring solutions to enhance operational efficiency, improve patient outcomes, and reduce healthcare costs. Rising urbanization, expansion of hospital networks, and government initiatives promoting telemedicine and remote monitoring are further supporting market growth. In addition, the emphasis on chronic disease management, aging population, and increasing awareness of health monitoring solutions are driving demand across both residential and institutional settings.

U.K. Patient Monitoring Systems Market Insight

The U.K. patient monitoring systems market is expected to grow at a noteworthy CAGR during the forecast period, driven by rising chronic disease prevalence, increasing patient awareness, and the need for efficient hospital management. Healthcare providers are increasingly leveraging advanced monitoring systems to track vital signs, enable early detection of complications, and provide personalized care. Government policies supporting digital healthcare adoption, coupled with the expansion of hospital and clinic networks, are encouraging investment in patient monitoring technologies. Furthermore, the growing demand for home-based monitoring solutions for elderly and chronic care patients supports steady market growth.

Germany Patient Monitoring Systems Market Insight

The Germany patient monitoring systems market is anticipated to expand at a significant CAGR during the forecast period, fueled by increasing healthcare expenditures, technological advancements in monitoring devices, and strong emphasis on patient-centric care. Hospitals and specialty clinics are implementing continuous monitoring solutions and wearable devices to ensure accurate, real-time patient data collection. The country’s well-developed healthcare infrastructure, along with initiatives promoting smart hospital systems and telemedicine, is further encouraging the adoption of advanced monitoring solutions. Growing awareness among patients and healthcare professionals regarding early intervention and chronic disease management also contributes to market expansion.

Asia-Pacific Patient Monitoring Systems Market Insight

The Asia-Pacific patient monitoring systems market is poised to grow at the fastest CAGR during the forecast period, driven by rapid urbanization, increasing healthcare access, and rising awareness about chronic disease management in emerging economies such as China, India, and Japan. Expansion of hospital networks, increasing investment in digital health infrastructure, and rising disposable incomes are accelerating the adoption of continuous and wearable monitoring devices. Government initiatives promoting telemedicine, remote monitoring, and digital health adoption further support market growth. In addition , increasing prevalence of cardiovascular diseases, diabetes, and other chronic conditions is prompting healthcare providers to implement advanced patient monitoring systems across both hospital and homecare settings.

Japan Patient Monitoring Systems Market Insight

The Japan patient monitoring systems market is gaining momentum due to the country’s advanced healthcare system, rapidly aging population, and high adoption of digital health solutions. Continuous and wearable monitoring devices are increasingly deployed in hospitals, nursing homes, and homecare settings to provide real-time patient data and proactive healthcare management. Government support for telemedicine and remote monitoring initiatives further accelerates adoption. The emphasis on improving quality of life for elderly patients, combined with rising chronic disease prevalence, is driving market expansion in both clinical and homecare environments.

China Patient Monitoring Systems Market Insight

The China patient monitoring systems market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, increasing healthcare awareness, and growing investments in healthcare infrastructure. Expansion of hospital networks, adoption of continuous and wearable monitoring devices, and government initiatives for chronic disease management are key factors driving market growth. The rising prevalence of lifestyle-related diseases and the push toward digital healthcare systems, combined with increasing consumer disposable income, further enhance market adoption across both urban and semi-urban regions. Continuous technological advancements and increasing collaboration between healthcare providers and technology companies are reinforcing China’s dominant position in the Asia-Pacific market.

Patient Monitoring Systems Market Share

The patient monitoring systems industry is primarily led by well-established companies, including:

- Honeywell International Inc. (U.S.)

- Verily (U.S.)

- Medtronic (Ireland)

- Compumedics Limited (Australia)

- NIHON KOHDEN CORPORATION (Japan)

- Natus Medical Incorporated (U.S.)

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- OMRON Corporation (Japan)

- Johnson & Johnson and its affiliates (U.S.)

- Care Innovations, LLC (U.S.)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Drägerwerk AG and Co. KGaA (Germany)

- CONTEC MEDICAL SYSTEMS CO., LTD (China)

- PRÜFTECHNIK Dieter Busch GmbH (Germany)

- Analog Devices, Inc. (U.S.)

Latest Developments in Global Patient Monitoring Systems Market

- In December 2021, Accuhealth launched its enhanced Remote Patient Monitoring (RPM) platform, Evelyn 3.0. This upgraded system incorporates advanced Artificial Intelligence capabilities, setting a new benchmark in RPM technology. The platform aims to improve patient outcomes by offering more accurate monitoring and predictive analytics, thereby reducing hospitalizations and enhancing care efficiency

- In June 2025, Cardinal Health introduced the Kendall DL Multi System, a multi-parameter, single-patient use monitoring cable and lead wire system. This innovative device enables continuous monitoring of cardiac activity, blood oxygen levels, and temperature through a single connection point. Designed for seamless patient transport from admission to discharge, it aims to streamline clinical workflows and reduce alarm fatigue among healthcare providers

- In June 2025, Philips expanded its longstanding partnership with Medtronic through a new multi-year agreement. This collaboration focuses on enhancing access to advanced patient monitoring technologies and delivering high-quality care. Building on a relationship that began in 1992, this next phase reflects both companies' shared commitment to providing comprehensive and validated monitoring solutions that support better patient outcomes

- In July 2025, AliveCor launched the Kardia 12L ECG System in India, marking a significant advancement in portable cardiac care. This AI-powered device offers 12-lead ECG capabilities, enabling healthcare providers to diagnose heart conditions more accurately and efficiently in outpatient settings. The launch underscores AliveCor's commitment to expanding access to advanced cardiac monitoring in emerging markets

- In April 2025, Health Recovery Solutions (HRS) was named the "Best in KLAS" provider of Remote Patient Monitoring solutions for the fourth consecutive year. This recognition highlights HRS's commitment to delivering high-quality RPM services that improve patient outcomes and reduce hospital readmissions. The company's platform is widely adopted across healthcare systems in the United States

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.