Global Patient Temperature Management Market

Market Size in USD Billion

USD

3.72 Billion

USD

8.09 Billion

2025

2033

USD

3.72 Billion

USD

8.09 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.72 Billion | |

| USD 8.09 Billion | |

| % | |

|

Patient Temperature Management Market Size

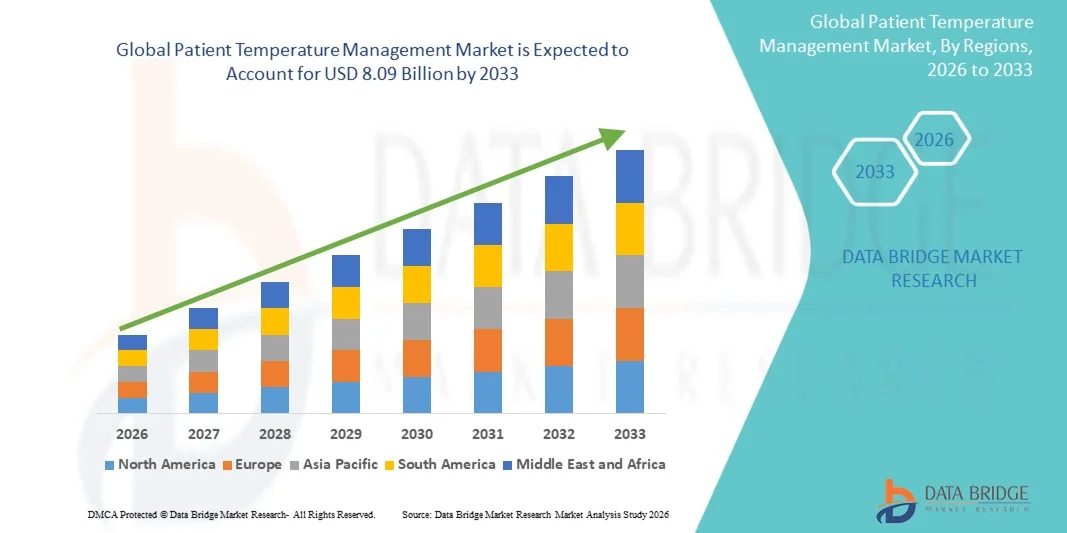

- The global patient temperature management market size was valued at USD 3.72 billion in 2025 and is expected to reach USD 8.09 billion by 2033, at a CAGR of 10.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, rising number of surgical procedures, and growing focus on maintaining optimal patient body temperature during critical care, leading to higher adoption of temperature management systems in hospitals and healthcare facilities

- Furthermore, increasing awareness regarding patient safety, advancements in temperature management technologies, and rising demand for efficient and non-invasive solutions are establishing patient temperature management systems as essential tools in modern healthcare. These converging factors are accelerating the uptake of patient temperature management solutions, thereby significantly boosting the market’s growth

Patient Temperature Management Market Analysis

- Patient temperature management systems, including warming and cooling devices, are increasingly vital in modern healthcare due to their role in maintaining normothermia, reducing surgical complications, and improving patient outcomes in critical care and perioperative settings

- The escalating demand for patient temperature management solutions is primarily driven by the rising number of surgical procedures, increasing prevalence of chronic conditions, and growing awareness regarding patient safety and temperature regulation in hospitals and intensive care units

- North America dominated the patient temperature management market with the largest revenue share of approximately 39.4% in 2025, supported by advanced healthcare infrastructure, high adoption of medical technologies, and strong presence of key market players

- Asia-Pacific is expected to be the fastest-growing region in the patient temperature management market during the forecast period, with a projected CAGR of 8.8%, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing surgical volumes in countries such as China, India, and Japan

- The patient warming system segment dominated the largest market revenue share of 61.8% in 2025, driven by its widespread use in surgical procedures and critical care settings to prevent hypothermia

Report Scope and Patient Temperature Management Market Segmentation

|

Attributes |

Patient Temperature Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• 3M Company (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Patient Temperature Management Market Trends

“Increasing Adoption of Advanced Temperature Control Technologies”

- A significant and accelerating trend in the global patient temperature management market is the growing adoption of advanced temperature regulation systems designed to maintain normothermia and improve clinical outcomes across surgical and critical care settings

- For instance, surface warming systems and intravascular temperature management devices are increasingly being utilized in hospitals to prevent perioperative hypothermia, with studies indicating that effective temperature control can reduce surgical complications by nearly 20–30%

- The integration of automated temperature monitoring and feedback-controlled systems is enhancing precision in patient care, enabling real-time adjustments based on patient condition

- In addition, the rising use of minimally invasive surgical procedures is increasing the demand for efficient temperature management solutions to ensure patient stability

- Technological advancements such as portable and user-friendly devices are improving accessibility across ambulatory surgical centers and emergency care units

- The increasing adoption of targeted temperature management (TTM) in post-cardiac arrest care is further strengthening market growth

- Growing awareness among healthcare professionals regarding the importance of maintaining optimal body temperature is driving consistent adoption

- Furthermore, the expansion of healthcare infrastructure in emerging markets is supporting the deployment of advanced temperature management systems

- The rising incidence of chronic diseases and surgical procedures globally is also contributing to the demand for these solutions

- Overall, this trend is significantly enhancing patient safety, treatment outcomes, and operational efficiency in healthcare settings

Patient Temperature Management Market Dynamics

Driver

“Rising Surgical Procedures and Critical Care Demand”

- The increasing number of surgical procedures and critical care admissions globally is a major driver for the Patient Temperature Management market, with over 300 million surgeries performed annually worldwide, necessitating effective temperature control solutions

- For instance, the growing prevalence of cardiovascular diseases has led to a rise in cardiac surgeries, where maintaining patient temperature is critical, with temperature management systems helping reduce post-operative complications by approximately 25%

- The expanding geriatric population, which is more susceptible to hypothermia during surgeries, is further driving demand for these systems

- Increasing incidence of trauma and emergency cases is also contributing to the need for rapid and efficient temperature management solutions

- Hospitals are increasingly adopting advanced systems to comply with clinical guidelines for perioperative temperature maintenance

- In addition, the growing number of intensive care units (ICUs) and advancements in critical care infrastructure are supporting market expansion

- The rise in chronic conditions such as cancer and neurological disorders requiring complex procedures is further fueling demand

- Healthcare providers are focusing on improving patient outcomes and reducing hospital stays, which is boosting adoption

- Government initiatives and healthcare investments aimed at improving surgical care are also supporting growth

- Collectively, these factors are significantly accelerating the adoption of patient temperature management systems across healthcare facilities globally

Restraint/Challenge

“High Equipment Costs and Limited Accessibility in Developing Regions”

- The high cost associated with advanced patient temperature management systems remains a significant challenge, particularly for small healthcare facilities and hospitals in developing regions, were budget constraints limit adoption

- For instance, advanced intravascular temperature management systems can cost significantly more than conventional warming methods, making them less accessible in low- and middle-income countries despite their clinical benefits

- Limited awareness and lack of trained professionals in certain regions further restrict the effective utilization of these systems

- In addition, inadequate healthcare infrastructure in developing economies hampers the widespread deployment of advanced technologies

- Maintenance and operational costs associated with these devices also add to the financial burden for healthcare providers

- Variability in reimbursement policies across countries can impact purchasing decisions and slow market growth

- The complexity of certain systems may require specialized training, creating additional barriers to adoption

- Concerns regarding device-related complications or improper usage can also hinder acceptance among healthcare professionals

- Furthermore, supply chain disruptions and limited availability of advanced devices in remote areas can restrict market penetration

- Addressing these challenges through cost-effective innovations, training programs, and improved healthcare access will be essential for sustaining long-term market growth

Patient Temperature Management Market Scope

The market is segmented on the basis of product type, component, application, medical speciality, and end user.

• By Product Type

On the basis of product type, the Patient Temperature Management market is segmented into Patient Warming System and Patient Cooling System. The patient warming system segment dominated the largest market revenue share of 61.8% in 2025, driven by its widespread use in surgical procedures and critical care settings to prevent hypothermia. Maintaining normothermia during surgeries is crucial to avoid complications such as infections and prolonged hospital stays, thereby increasing the adoption of warming systems. The segment benefits from rising surgical volumes globally and increasing awareness regarding perioperative temperature management. In addition, technological advancements such as forced-air warming systems and conductive warming devices are enhancing efficiency and patient safety. Hospitals and healthcare providers are increasingly incorporating warming systems into standard protocols. The growing geriatric population, which is more prone to hypothermia, further drives demand. Increasing healthcare expenditure and improved infrastructure also support segment growth. The segment is further strengthened by strong clinical evidence supporting its effectiveness. Rising adoption in neonatal and ICU settings contributes significantly. These factors collectively reinforce the segment’s leading position.

The patient cooling system segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing demand for therapeutic hypothermia in cardiac arrest and neurological conditions. Cooling systems are gaining traction for their role in improving patient outcomes in critical care. The segment benefits from rising prevalence of cardiovascular and neurological disorders. In addition, advancements in non-invasive cooling technologies are enhancing adoption. Increasing awareness among healthcare professionals regarding temperature modulation therapies is boosting demand. The segment is also supported by growing ICU admissions globally. Expanding applications in trauma and stroke management further contribute to growth. Technological innovations such as automated temperature control systems enhance precision. Government initiatives to improve critical care infrastructure also support adoption. Rising investments in healthcare technology further accelerate growth. These factors collectively drive the rapid expansion of the cooling systems segment.

• By Component

On the basis of component, the Patient Temperature Management market is segmented into Warming and Cooling. The warming segment dominated the largest market revenue share of 58.9% in 2025, driven by its extensive application across surgical and postoperative care. Warming components are essential in preventing hypothermia during anesthesia and recovery phases. The segment benefits from high adoption in operating rooms and ICUs. Increasing number of surgeries globally significantly contributes to demand. In addition, growing awareness regarding patient safety protocols supports widespread usage. The availability of advanced warming blankets and systems enhances efficiency. Hospitals are increasingly integrating warming components into routine care practices. The segment is also supported by favorable reimbursement policies in developed regions. Rising geriatric population further boosts demand. Continuous innovation in warming technologies strengthens market presence. These factors collectively maintain the segment’s dominance.

The cooling segment is projected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by increasing use in emergency and critical care settings. Cooling components are essential in managing fever and reducing metabolic activity in critical patients. The segment benefits from rising cases of stroke and cardiac arrest. Technological advancements in cooling devices improve patient outcomes. Increasing adoption of targeted temperature management therapies further drives growth. The segment is also supported by expanding ICU infrastructure globally. Growing awareness among clinicians enhances utilization. In addition, increasing research in hypothermia therapy contributes to innovation. Rising healthcare investments in emerging economies support expansion. These factors collectively accelerate the segment’s growth trajectory.

• By Application

On the basis of application, the Patient Temperature Management market is segmented into Preoperative Care, Operating Room, Postoperative Care, Acute Care, Intensive Care Unit, Emergency Rooms, Neonatal Intensive Care Units and Other Applications. The operating room segment dominated the largest market revenue share of 36.5% in 2025, driven by the critical need to maintain patient temperature during surgical procedures. Temperature regulation in operating rooms is essential to prevent complications and ensure better surgical outcomes. The segment benefits from increasing global surgical volumes. In addition, strict clinical guidelines mandate temperature management during operations. Technological advancements in intraoperative warming systems enhance efficiency. Hospitals are prioritizing patient safety, boosting adoption. The segment also benefits from increased healthcare spending. Growing prevalence of chronic diseases requiring surgery further supports demand. Integration of advanced monitoring systems enhances usage. Rising awareness among surgeons contributes to growth. These factors collectively ensure segment dominance.

The intensive care unit (ICU) segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing critical care admissions. ICU patients often require precise temperature control for optimal recovery. The segment benefits from rising prevalence of severe infections and chronic conditions. Technological advancements in automated temperature management systems support adoption. Increasing investment in ICU infrastructure globally boosts growth. In addition, growing awareness of targeted temperature management enhances demand. The segment is also supported by rising geriatric population. Expansion of critical care facilities in emerging markets contributes significantly. Continuous monitoring capabilities improve treatment outcomes. These factors collectively drive rapid growth of the ICU segment.

• By Medical Speciality

On the basis of medical speciality, the Patient Temperature Management market is segmented into General Surgery, Cardiology, Neurology, Pediatrics, Thoracic Surgery, Orthopedic Surgery and Other Medical Specialties. The general surgery segment dominated the largest market revenue share of 28.4% in 2025, driven by the high volume of surgical procedures performed globally. Temperature management is a standard requirement in general surgeries to prevent complications. The segment benefits from increasing surgical interventions due to rising chronic diseases. In addition, advancements in surgical techniques enhance demand for temperature management devices. Hospitals are increasingly adopting standardized perioperative care protocols. The segment also benefits from strong healthcare infrastructure in developed regions. Rising awareness regarding patient safety further supports growth. Increasing adoption in outpatient surgical centers contributes to demand. Continuous innovation in surgical equipment enhances efficiency. These factors collectively maintain segment dominance.

The cardiology segment is anticipated to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing prevalence of cardiovascular diseases. Temperature management plays a crucial role in cardiac surgeries and post-cardiac arrest care. The segment benefits from advancements in cardiac care technologies. Increasing number of cardiac procedures globally supports growth. In addition, rising awareness of therapeutic hypothermia enhances adoption. The segment is also supported by expanding specialized cardiac centers. Government initiatives to improve cardiac care infrastructure contribute to growth. Increasing geriatric population further drives demand. Continuous research in cardiac treatment enhances innovation. These factors collectively accelerate segment expansion.

• By End User

On the basis of end user, the Patient Temperature Management market is segmented into Hospitals, Specialized Clinics, Ambulatory Surgical Centres and Others. The hospitals segment dominated the largest market revenue share of 64.7% in 2025, driven by the high patient volume and availability of advanced medical infrastructure. Hospitals are primary centers for surgeries and critical care, increasing demand for temperature management systems. The segment benefits from strong financial capabilities and access to advanced technologies. In addition, increasing number of hospital admissions supports growth. Hospitals are increasingly adopting comprehensive patient care protocols. The segment is also supported by favorable reimbursement policies. Rising investments in healthcare infrastructure further boost demand. Increasing prevalence of chronic diseases contributes to higher patient inflow. Continuous technological upgrades enhance efficiency. These factors collectively ensure segment dominance.

The ambulatory surgical centres segment is expected to witness the fastest CAGR of 8.4% from 2026 to 2033, driven by the growing shift towards outpatient surgeries. These centers offer cost-effective and efficient surgical procedures, increasing demand for temperature management systems. The segment benefits from shorter hospital stays and faster recovery times. Increasing preference for minimally invasive procedures supports growth. In addition, expanding number of ASCs globally contributes significantly. The segment is also supported by advancements in portable temperature management devices. Rising healthcare cost containment measures drive adoption. Growing patient preference for convenient care settings enhances demand. Continuous innovation in outpatient care technologies supports expansion. These factors collectively drive rapid growth of the segment.

Patient Temperature Management Market Regional Analysis

- North America dominated the patient temperature management market with the largest revenue share of approximately 39.4% in 2025, supported by advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and the strong presence of leading market players across the region

- The region benefits from a high volume of surgical procedures and well-established clinical protocols that emphasize perioperative temperature management, thereby driving consistent demand for these systems

- This widespread adoption is further reinforced by strong healthcare spending, increasing awareness among healthcare professionals, and the availability of advanced critical care facilities, establishing patient temperature management systems as an essential component in hospitals and surgical centers

U.S. Patient Temperature Management Market Insight

The U.S. patient temperature management market captured the largest revenue share in 2025 within North America, driven by a high number of surgical procedures, strong healthcare infrastructure, and early adoption of advanced medical technologies. The country continues to lead in the implementation of targeted temperature management systems, particularly in critical care and post-operative settings. Additionally, the presence of major medical device manufacturers, ongoing clinical research, and increasing focus on improving patient outcomes are significantly contributing to market growth. The rising prevalence of chronic diseases and the growing geriatric population further support the demand for efficient temperature management solutions in the U.S.

Europe Patient Temperature Management Market Insight

The Europe patient temperature management market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare investments, stringent clinical guidelines for patient safety, and rising awareness regarding perioperative hypothermia management. The region is witnessing growing adoption of advanced warming and cooling systems across hospitals and ambulatory surgical centers. Additionally, the presence of well-established healthcare systems and increasing focus on improving surgical outcomes are contributing to market expansion across European countries.

U.K. Patient Temperature Management Market Insight

The U.K. patient temperature management market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising number of surgical procedures and strong emphasis on patient safety within the healthcare system. Increasing adoption of advanced medical technologies, along with government initiatives aimed at improving healthcare services, is supporting market growth. Furthermore, the presence of well-developed hospital infrastructure and increasing awareness regarding temperature management in critical care are contributing to the expansion of the market in the U.K.

Germany Patient Temperature Management Market Insight

The Germany patient temperature management market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s strong healthcare infrastructure, high healthcare expenditure, and focus on technological innovation. Germany’s well-established hospital network and increasing adoption of advanced patient monitoring and temperature regulation systems are driving market growth. Additionally, the emphasis on improving clinical outcomes and reducing surgical complications is further promoting the use of patient temperature management solutions.

Asia-Pacific Patient Temperature Management Market Insight

The Asia-Pacific patient temperature management market is poised to grow at the fastest CAGR of approximately 8.8% during the forecast period, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing surgical volumes in countries such as China, Japan, and India. The region is witnessing significant investments in hospital development and modernization, which is facilitating the adoption of advanced temperature management systems. Furthermore, the growing awareness regarding patient safety and increasing access to healthcare services are supporting market growth across the region.

Japan Patient Temperature Management Market Insight

The Japan patient temperature management market is gaining momentum due to the country’s advanced healthcare system, aging population, and high demand for quality medical care. The increasing number of surgical procedures and the strong focus on patient safety are driving the adoption of temperature management systems. Additionally, Japan’s emphasis on technological innovation and the integration of advanced medical devices in healthcare facilities are contributing to market growth.

China Patient Temperature Management Market Insight

The China patient temperature management market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid healthcare infrastructure development, increasing healthcare investments, and a growing patient population. The country is experiencing a rise in surgical procedures and hospital admissions, which is driving demand for temperature management systems. Additionally, government initiatives aimed at improving healthcare access and the expansion of domestic medical device manufacturing are key factors propelling market growth in China.

Patient Temperature Management Market Share

The Patient Temperature Management industry is primarily led by well-established companies, including:

• 3M Company (U.S.)

• Stryker Corporation (U.S.)

• BD (U.S.)

• GE HealthCare Technologies Inc. (U.S.)

• Medtronic (Ireland)

• Smiths Medical (U.K.)

• ZOLL Medical Corporation (U.S.)

• Drägerwerk AG & Co. KGaA (Germany)

• Inspiration Healthcare Group plc (U.K.)

• Gentherm Medical (U.S.)

• Atom Medical Corporation (Japan)

• The Surgical Company (Netherlands)

• Geratherm Medical AG (Germany)

• Stihler Electronic GmbH (Germany)

• Biegler GmbH (Austria)

• EMIT Corporation (U.S.)

• Inditherm plc (U.K.)

• Belmont Medical Technologies (U.S.)

• Enthermics Medical Systems (U.S.)

• Innocare Medical (China)

Latest Developments in Global Patient Temperature Management Market

- In January 2021, Medtronic announced that the U.S. Food and Drug Administration approved its DiamondTemp Ablation System, a temperature-controlled radiofrequency system designed to precisely manage tissue temperature during cardiac ablation procedures, improving procedural safety and expanding its temperature-management portfolio

- In June 2023, Drägerwerk AG & Co. KGaA launched the Babyroo TN300 patient warming system, specifically designed for neonatal care, providing stable temperature regulation and respiratory support for newborns, thereby addressing critical care needs in neonatal intensive care units

- In July 2023, Asahi Kasei Corporation entered into an agreement with BrainCool for exclusive distribution of the BrainCool System and IQool System in the U.S. and Europe, expanding access to advanced temperature management solutions for therapeutic hypothermia and neurological care

- In January 2024, ZOLL Medical Corporation (an Asahi Kasei company) received both FDA clearance and CE mark approval for an upgraded Thermogard Temperature Management System, enabling combined core and surface temperature management with enhanced analytics, improving precision and flexibility in critical care settings

- In July 2025, Medline Industries announced the launch of the ComfortTemp Patient Warming System in select Asia-Pacific hospitals, featuring disposable warming blankets and advanced connector designs to improve perioperative temperature control and patient comfort during surgical procedures

- In August 2025, Arctx Medical announced progress toward FDA authorization for its Cool Catheter Kit designed for body temperature regulation, representing a novel minimally invasive approach to therapeutic cooling in acute care settings

- In November 2025, Arctx Medical received FDA marketing authorization for its Cool Catheter Set, a thermal regulation device designed to control patient temperature while also enabling gastric decompression and fluid administration, highlighting innovation in integrated temperature management solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.