Global Pediatric Heart Failure Market

Market Size in USD Billion

USD

2.78 Billion

USD

4.07 Billion

2024

2032

USD

2.78 Billion

USD

4.07 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.78 Billion | |

| USD 4.07 Billion | |

| % | |

|

Pediatric Heart Failure Market Size

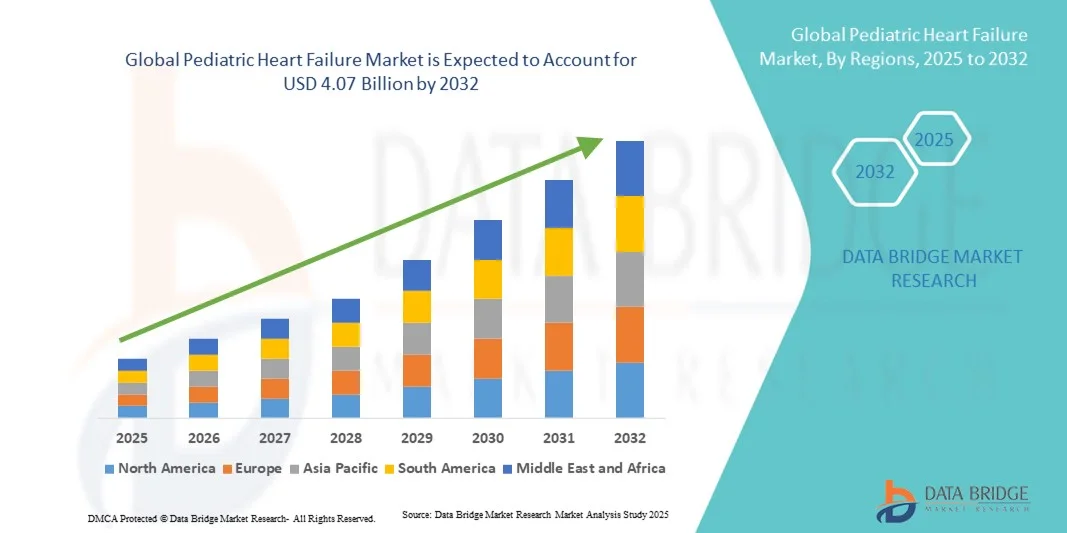

- The global pediatric heart failure market size was valued at USD 2.78 billion in 2024 and is expected to reach USD 4.07 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of congenital heart defects and chronic cardiovascular conditions in children, leading to higher demand for specialized pediatric heart failure management solutions in hospitals and clinics

- Furthermore, advancements in early diagnosis, improved pharmacological therapies, and growing awareness among healthcare professionals and caregivers are driving the adoption of innovative treatment options. These converging factors are accelerating the uptake of Pediatric Heart Failure solutions, thereby significantly boosting the industry's growth

Pediatric Heart Failure Market Analysis

- Pediatric heart failure, a complex clinical syndrome affecting children due to structural or functional cardiac disorders, is increasingly recognized as a critical area in pediatric cardiology, necessitating specialized treatment protocols, early diagnosis, and comprehensive care in both hospital and outpatient settings

- The escalating demand for advanced pediatric heart failure therapies is primarily fueled by rising prevalence of congenital heart diseases, increasing survival rates of pediatric patients with cardiac anomalies, growing awareness among clinicians and caregivers, and advancements in pharmacological and device-based interventions

- North America dominated the pediatric heart failure market with the largest revenue share of 41.8% in 2024, characterized by advanced healthcare infrastructure, high clinical awareness, and a strong presence of leading pharmaceutical and medical device companies. The U.S. experienced substantial growth in pediatric heart failure treatment adoption, driven by hospital protocols for early diagnosis, implementation of evidence-based management guidelines, and innovations in pediatric-specific therapies

- Asia-Pacific is expected to be the fastest-growing region in the pediatric heart failure market during the forecast period, projected to register a CAGR of 10.5%, fueled by rising pediatric cardiovascular disorders, improving healthcare infrastructure, increasing investment in specialized pediatric cardiac centers, and growing accessibility to advanced treatment options in countries such as China and India

- The Over-Circulation Failure segment dominated the pediatric heart failure market with a revenue share of 52% in 2024, due to the higher prevalence of left-to-right shunts and congenital cardiac anomalies leading to volume overload in pediatric patients

Report Scope and Pediatric Heart Failure Market Segmentation

|

Attributes |

Pediatric Heart Failure Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Pediatric Heart Failure Market Trends

Advances in Innovative Therapies and Monitoring

- A significant and accelerating trend in the global pediatric heart failure market is the growing adoption of advanced therapeutic options and digital monitoring technologies. Innovations such as pediatric-specific ventricular assist devices (VADs), gene therapies, and wearable cardiac monitoring solutions are enhancing patient outcomes and enabling more precise management of chronic heart conditions in children

- Clinicians are increasingly using telemonitoring platforms to track vital signs, cardiac output, and medication adherence in real-time, allowing timely interventions and reducing hospital readmissions

- The integration of AI-based predictive analytics in pediatric cardiology is improving early diagnosis and risk stratification, helping physicians personalize treatment plans for young patients with heart failure

- For instance, in January 2023, Medtronic announced the launch of a next-generation pediatric ventricular assist device in the U.S., designed to provide safer, long-term circulatory support for children with severe heart failure

- Digital platforms are also enabling remote patient education, virtual consultations, and interactive care programs for families, improving adherence to treatment and overall quality of life for pediatric patients

- Growing collaboration between hospitals, medical device companies, and research institutions is fostering rapid innovation in pediatric heart failure therapies, leading to better access to advanced treatment options

Pediatric Heart Failure Market Dynamics

Driver

Rising Prevalence of Pediatric Heart Conditions and Improved Diagnosis

- The increasing prevalence of congenital heart defects, cardiomyopathies, and other chronic cardiovascular conditions among children is a primary driver for the Pediatric Heart Failure market. Early detection and timely intervention are critical for improving survival rates and quality of life

- Advancements in diagnostic imaging, such as echocardiography, cardiac MRI, and 3D modeling, are enabling precise assessment of heart function and better treatment planning for pediatric patients

- For instance, in August 2022, Boston Children’s Hospital implemented an AI-assisted echocardiography platform, which enhanced the accuracy of pediatric heart failure diagnosis and optimized treatment regimens

- Growing awareness among healthcare providers and parents about the importance of early detection and specialized pediatric care is expanding the market

- Increasing government and NGO initiatives focused on child health, pediatric cardiac screening programs, and public health campaigns are boosting early diagnosis and treatment uptake

- The adoption of advanced pharmacological therapies, including pediatric-friendly formulations of ACE inhibitors, beta-blockers, and novel inotropes, is further contributing to market growth

Restraint/Challenge

High Treatment Costs, Limited Specialized Infrastructure, and Regulatory Hurdles

- The relatively high cost of pediatric heart failure therapies, devices, and hospital care can limit access in low- and middle-income regions, affecting overall market growth

- Availability of specialized pediatric cardiac centers and trained cardiologists remains limited in many regions, posing challenges for widespread adoption of advanced therapies

- Regulatory approvals for pediatric-specific devices and drugs often require longer clinical trials and safety validations, delaying market entry

- For instance, in March 2021, a survey across Latin America highlighted that limited availability of pediatric-specific ventricular assist devices led to delays in treatment initiation for several patients

- Concerns about potential adverse effects, long-term safety, and device-related complications may make parents and caregivers hesitant to pursue advanced treatment options

- Inadequate awareness among caregivers regarding disease management, early warning signs, and adherence to prescribed therapies can further hinder treatment effectiveness

- Overcoming these challenges through governmental support, insurance coverage expansion, enhanced infrastructure for pediatric cardiac care, and ongoing medical education will be crucial for sustainable market growth

Pediatric Heart Failure Market Scope

The pediatric heart failure market is segmented on the basis of treatment, type, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the market is segmented into diuretics, digoxin, aldosterone antagonists, ACE inhibitors, beta blockers, and inotropes. The Diuretics segment dominated the market with a revenue share of 44.5% in 2024, driven by its established efficacy in managing fluid overload, reducing hospitalization rates, and improving symptomatic relief in pediatric heart failure patients. Hospitals and clinics widely adopt diuretics as a first-line therapy due to ease of administration, rapid clinical response, and guideline-based recommendations. The segment benefits from strong physician confidence, inclusion in pediatric heart failure protocols, and high availability across major healthcare institutions. Awareness campaigns, clinical training, and inclusion in treatment guidelines further reinforce adoption. Insurance coverage and favorable reimbursement policies in North America and Europe also contribute to dominance. Market penetration is strong in children with both over-circulation and pump failure types. Research studies emphasizing safety and tolerability enhance clinician trust, while emerging combination therapies with diuretics support sustained usage. The segment also benefits from integration into hospital formulary systems and wide availability in both branded and generic forms. Overall, diuretics remain a cornerstone of pediatric heart failure treatment across regions.

The Inotropes segment is expected to witness the fastest CAGR of 11.5% from 2025 to 2032, driven by rising adoption in severe pediatric cases, ICU settings, and acute decompensated heart failure. Inotropes improve myocardial contractility, offering immediate hemodynamic benefits, particularly in critical care and post-operative cardiac patients. Increasing availability of pediatric-specific formulations and innovations in infusion devices support growth. Hospitals and ambulatory centers are expanding protocols for inotropic therapy due to positive patient outcomes and shorter recovery times. Rising awareness among cardiologists regarding the role of inotropes in bridging therapy for transplant candidates fuels adoption. Clinical studies highlighting safety, combined with guideline updates, are boosting market confidence. Growth is further supported by improving healthcare infrastructure in Asia-Pacific and Latin America, increasing emergency care access, and rising incidence of congenital heart diseases. Inotropes’ integration into hospital protocols, physician endorsements, and continuous R&D in pediatric formulations make it the fastest-growing treatment segment.

- By Type

On the basis of type, the market is segmented into Over-Circulation Failure and Pump Failure. The Over-Circulation Failure segment dominated with a revenue share of 52% in 2024, due to the higher prevalence of left-to-right shunts and congenital cardiac anomalies leading to volume overload in pediatric patients. Effective management strategies, including diuretics, ACE inhibitors, and beta-blockers, are widely adopted to prevent progression. Hospitals implement structured monitoring and early intervention protocols, driving segment dominance. Increasing clinician awareness, guideline adoption, and focus on preventive management further support growth. Patient education initiatives and insurance coverage for standard therapies enhance market penetration. The segment benefits from strong hospital-based infrastructure and specialist pediatric cardiology units in North America and Europe. Research highlighting improved outcomes with timely intervention strengthens adoption. High physician familiarity and standardized treatment protocols make Over-Circulation Failure the preferred focus of pediatric heart failure management programs.

The Pump Failure segment is expected to witness the fastest CAGR of 10.8% from 2025 to 2032, fueled by rising cases of myocardial dysfunction due to congenital defects, cardiomyopathies, and post-operative complications. Growing adoption of inotropes, beta-blockers, and device-assisted therapy drives the segment. Hospitals and clinics increasingly implement intensive monitoring, early intervention, and advanced care pathways. Awareness campaigns, physician training, and increasing pediatric cardiac ICU facilities support growth. Market expansion in emerging regions with improved healthcare access further accelerates adoption. Increasing integration of pharmacological and non-pharmacological interventions enhances outcomes, driving demand. Technological advancements in pediatric cardiac care, combined with R&D in pump failure-specific therapies, are further contributing to the segment’s rapid growth.

- By End-Users

On the basis of end-users, the market is segmented into Clinics, Hospitals, Ambulatory Surgical Centers, and Others. The Hospitals segment dominated with a revenue share of 59% in 2024, owing to specialized pediatric cardiology departments, access to advanced treatment modalities, and capability to manage acute and chronic heart failure cases. Hospitals serve as primary centers for diagnosis, monitoring, and long-term management, benefiting from structured care pathways. The segment also benefits from strong clinician presence, trained pediatric cardiologists, and availability of ICU facilities. Reimbursement policies, hospital partnerships with pharmaceutical companies, and widespread adoption of standardized treatment guidelines further strengthen the segment’s dominance. High patient inflow, adoption of evidence-based protocols, and comprehensive care offerings make hospitals the primary choice for pediatric heart failure management.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 11% from 2025 to 2032, fueled by rising outpatient procedures, minimally invasive interventions, and demand for short-stay management of stabilized heart failure patients. Growth is supported by increased adoption of day-care cardiac procedures, improving healthcare infrastructure, and rising investments in specialized centers. Flexibility, lower costs, and patient convenience further drive adoption. Training programs, clinician awareness, and supportive reimbursement policies also contribute to growth. Expansion of ASCs in emerging regions such as Asia-Pacific and Latin America enhances market access.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated with a revenue share of 62% in 2024, due to direct procurement by hospitals for inpatient and outpatient care, ensuring consistent supply of essential pediatric heart failure medications. Integration with hospital formulary systems, bulk procurement advantages, and regulatory compliance drive dominance. Hospitals prioritize stock availability, quality assurance, and physician-preferred branded medications. The segment benefits from structured logistics, hospital networks, and strong supplier relationships. Patient trust and insurance coverage further reinforce preference for hospital pharmacy distribution.

The Online Pharmacy segment is expected to witness the fastest CAGR of 12% from 2025 to 2032, driven by rising e-pharmacy adoption, convenience of home delivery, and increased awareness among caregivers. Growth is further supported by telemedicine adoption, digital prescription platforms, and expanding internet penetration. Caregivers increasingly rely on online pharmacies for routine refills, branded and generic options, and timely access to medications. Marketing initiatives, partnerships with healthcare providers, and discount programs enhance uptake. The segment benefits from rapid expansion in urban and semi-urban regions globally.

Pediatric Heart Failure Market Regional Analysis

- North America dominated the pediatric heart failure market with the largest revenue share of 41.8% in 2024, driven by advanced healthcare infrastructure, high clinical awareness, and a strong presence of leading pharmaceutical and medical device companies

- The region has witnessed substantial adoption of pediatric heart failure therapies due to well-established hospital protocols for early diagnosis and the implementation of evidence-based management guidelines. Increasing investments in specialized pediatric cardiac centers, expansion of outpatient care facilities, and the rising focus on personalized treatment options have further fueled market growth

- The prevalence of congenital heart defects and chronic pediatric cardiovascular disorders is high in North America, which has encouraged clinicians to adopt innovative pharmacological and device-based therapies. Moreover, government initiatives supporting pediatric healthcare research, continuous clinical trials, and enhanced reimbursement policies are facilitating widespread access to advanced treatment options, driving further market expansion

U.S. Pediatric Heart Failure Market Insight

The U.S. pediatric heart failure market captured the largest revenue share within North America in 2024. This growth is fueled by high awareness of pediatric cardiovascular disorders among healthcare professionals, widespread adoption of early diagnostic procedures, and the implementation of hospital-based treatment protocols. The U.S. market benefits from extensive clinical research, robust healthcare infrastructure, and access to cutting-edge pharmacological treatments such as ACE inhibitors, beta blockers, and inotropes tailored for pediatric patients. Furthermore, increasing awareness among caregivers and parents regarding early symptom recognition, coupled with supportive insurance and reimbursement policies, is driving treatment uptake. The market is also boosted by collaborations between hospitals, research institutions, and pharmaceutical companies aimed at developing innovative, pediatric-specific therapies and improving clinical outcomes.

Europe Pediatric Heart Failure Market Insight

The Europe pediatric heart failure market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing awareness of pediatric cardiovascular conditions and increasing availability of advanced treatment options. European countries are witnessing rising investment in specialized pediatric cardiac centers, hospitals, and outpatient care facilities. National healthcare initiatives promoting early diagnosis, preventive care, and multidisciplinary management approaches are encouraging the adoption of evidence-based therapies. The market growth is further supported by increasing participation in clinical trials, the availability of pediatric-specific medications and medical devices, and a rising emphasis on improving treatment accessibility and quality of care across the region.

U.K. Pediatric Heart Failure Market Insight

The U.K. pediatric heart failure market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by a combination of increasing public and clinical awareness regarding pediatric cardiovascular disorders and substantial investments in healthcare infrastructure. Hospitals and specialized cardiac centers are expanding capacity to meet the rising demand for pediatric-specific therapies. Early detection programs, nationwide screening initiatives, and enhanced training for healthcare professionals are improving patient outcomes. In addition, the U.K.’s strong regulatory framework and access to innovative therapies encourage clinicians to adopt advanced treatment protocols, contributing to overall market growth.

Germany Pediatric Heart Failure Market Insight

The Germany pediatric heart failure market is expected to expand at a considerable CAGR during the forecast period, owing to its well-established healthcare infrastructure, strong clinical expertise, and high patient awareness. Hospitals and specialized pediatric cardiac centers in Germany are increasingly integrating advanced monitoring systems, personalized treatment plans, and evidence-based therapies. Government support for pediatric health initiatives, coupled with ongoing clinical research and adoption of innovative medications and devices, is driving growth. Furthermore, patient advocacy programs and caregiver education initiatives are creating awareness of early diagnosis and adherence to treatment protocols, supporting market expansion.

Asia-Pacific Pediatric Heart Failure Market Insight

The Asia-Pacific is expected to be the fastest-growing region in the pediatric heart failure market during the forecast period, projected to register a CAGR of 10.5%. Growth is fueled by rising prevalence of pediatric cardiovascular disorders, improving healthcare infrastructure, increasing investment in specialized pediatric cardiac centers, and growing accessibility to advanced treatment options in countries such as China and India. Rapid urbanization, rising disposable incomes, and expansion of private healthcare services are improving treatment availability. Government initiatives focused on pediatric health, combined with increasing awareness among parents and caregivers regarding early diagnosis and treatment, are contributing to market growth. The adoption of modern treatment protocols, improved access to pharmacological therapies, and expansion of outpatient and telemedicine services are further accelerating the market.

Japan Pediatric Heart Failure Market InsightThe Japan pediatric heart failure market is witnessing steady growth, supported by a high level of clinical expertise, advanced healthcare infrastructure, and an increasing focus on early detection and management of pediatric cardiovascular conditions. The market benefits from government-led healthcare programs, advanced diagnostic facilities, and the presence of specialized cardiac centers. Furthermore, Japan’s aging population has spurred interest in preventive pediatric care, increasing the emphasis on early treatment and long-term disease management strategies.

China Pediatric Heart Failure Market Insight

The China pediatric heart failure market accounted for a significant revenue share in Asia-Pacific in 2024, driven by expanding pediatric cardiac care facilities, rising awareness of pediatric cardiovascular disorders, and increasing accessibility to innovative treatment options. Rapid urbanization, government initiatives to enhance pediatric healthcare, and the availability of advanced pharmacological therapies have propelled market growth. In addition, China’s growing middle class, improved insurance coverage, and private healthcare investments are supporting wider adoption of pediatric heart failure therapies. Expansion of telemedicine services and collaboration between hospitals and medical device manufacturers are further facilitating market growth.

Pediatric Heart Failure Market Share

The Pediatric Heart Failure industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson and its affiliates (U.S.)

- Bayer AG (Germany)

- Abbott (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi S.A. (France)

- Bristol-Myers Squibb Company (U.S.)

- GSK plc (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Hikma Pharmaceuticals PLC (U.K.)

Latest Developments in Global Pediatric Heart Failure Market

- In April 2023, an international symposium titled “Advances in Pediatric Heart Failure: Congenital Disease and Cardiomyopathies” was held in Florence, Italy. The event brought together leading experts to discuss state-of-the-art management strategies for children and adolescents with heart failure, focusing on the latest research and clinical practices in the field

- In March 2025, a keynote presentation titled “A Journey Through Time: Enhancing Care of Pediatric Heart Failure Patients” was delivered at the American College of Cardiology (ACC) conference. The session highlighted advancements in the care and treatment of pediatric heart failure, emphasizing the importance of early diagnosis, personalized treatment plans, and the integration of new therapeutic approaches to improve patient outcomes

- In January 2025, Eli Lilly and Company announced encouraging topline findings from the Phase 3 SUMMIT clinical study, assessing the safety and effectiveness of tirzepatide injection in adults suffering from heart failure with preserved ejection fraction (HFpEF) and obesity. This dual agonist targets glucose-dependent insulinotropic polypeptide (GIP) and glucagon-like peptide-1 (GLP-1) receptors, offering a new potential therapy for advanced heart failure

- In May 2025, Cohen Children's Medical Center in New Hyde Park, New York, conducted its first pediatric heart transplant. This milestone followed the program's approval by New York State in February 2025, marking the establishment of Long Island's first pediatric heart transplant program. The transplant was performed by Dr. Timothy Martens and his team, providing a critical service to children in the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.