Global Pediatric Neurology Devices Market

Market Size in USD Billion

USD

2,332.96 Billion

USD

3,774.88 Billion

2025

2033

USD

2,332.96 Billion

USD

3,774.88 Billion

2025

2033

| 2026 - 2033 | |

| USD 2,332.96 Billion | |

| USD 3,774.88 Billion | |

| % | |

|

Pediatric Neurology Devices Market Size

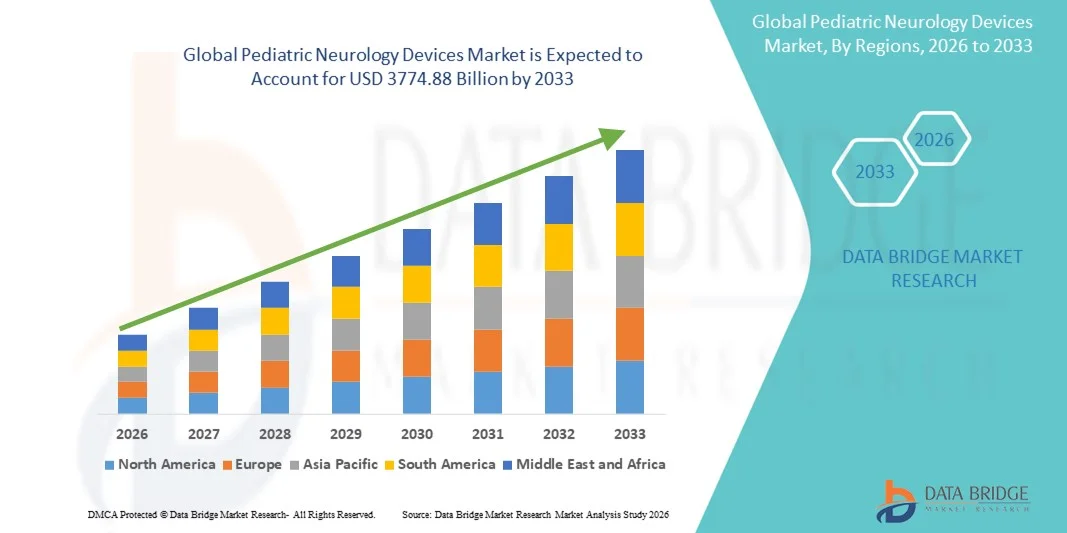

- The global pediatric neurology devices market size was valued at USD 2332.96 billion in 2025 and is expected to reach USD 3774.88 billion by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders among children, rising awareness about early diagnosis and intervention, and technological advancements in pediatric neurology devices, leading to improved diagnostic accuracy, treatment planning, and patient monitoring in both hospital and clinical settings

- Furthermore, growing demand for minimally invasive, non-invasive, and child-friendly neurological devices, coupled with increasing investments in pediatric healthcare infrastructure, is establishing pediatric neurology devices as essential tools for modern pediatric care. These converging factors are accelerating the uptake of Pediatric Neurology Devices solutions, thereby significantly boosting the overall growth of the market

Pediatric Neurology Devices Market Analysis

- Pediatric neurology devices, designed for diagnosing, monitoring, and treating neurological conditions in children, are becoming increasingly vital due to rising incidence of pediatric neurological disorders, improved healthcare access, and technological advancements in child‑specific diagnostic and therapeutic tools

- The escalating demand for pediatric neurology devices is primarily driven by the growing prevalence of conditions such as epilepsy, cerebral palsy, and developmental disorders, combined with increased investment in pediatric healthcare infrastructure and advanced neurodiagnostic technologies. Integration with AI‑enabled imaging and monitoring systems is further supporting market adoption

- North America dominated the pediatric neurology devices market with approximately 44.5% revenue share in 2025, supported by well‑established healthcare infrastructure, high clinical adoption of advanced devices, strong reimbursement policies, and the presence of major industry players

- Asia‑Pacific is expected to be the fastest‑growing region during the forecast period, posting the highest CAGR due to expanding healthcare investments, rising awareness about pediatric neurological care, and increasing diagnosis rates in emerging markets such as China and India

- The neurosurgery devices segment dominated the market with the largest revenue share of 42.5% in 2025, primarily due to the rising prevalence of congenital neurological disorders, brain injuries, and cranial malformations in pediatric patients

Report Scope and Pediatric Neurology Devices Market Segmentation

|

Attributes |

Pediatric Neurology Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Medtronic (Ireland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pediatric Neurology Devices Market Trends

Rising Adoption of Advanced Pediatric Neurology Devices

- A significant and accelerating trend in the global pediatric neurology devices market is the growing adoption of advanced diagnostic and monitoring tools specifically designed for neurological disorders in children. These devices facilitate early detection, accurate diagnosis, and effective treatment planning for conditions such as epilepsy, cerebral palsy, and developmental delays

- For instance, in 2024, Nihon Kohden launched a pediatric-focused EEG system with enhanced sensitivity and real-time monitoring capabilities, enabling clinicians to accurately diagnose seizures in infants and young children

- The integration of multimodal imaging and neurophysiological monitoring within pediatric neurology devices is improving the precision of diagnoses and allowing for more personalized treatment plans

- Increasing awareness among parents and healthcare providers regarding early intervention and neurological health in children is driving adoption of these devices

- The trend toward minimally invasive monitoring and portable devices is enhancing patient comfort and enabling broader use in both clinical and home settings

- Overall, the adoption of advanced, child-specific neurological devices is reshaping pediatric care by improving diagnostic accuracy and treatment outcomes

Pediatric Neurology Devices Market Dynamics

Driver

Increasing Prevalence of Pediatric Neurological Disorders

- The rising incidence of neurological disorders among children, including epilepsy, cerebral palsy, and attention deficit disorders, is a major driver for the Pediatric Neurology Devices market. Early diagnosis and monitoring are critical to improving patient outcomes and reducing long-term healthcare costs

- For instance, in 2023, Boston Children’s Hospital adopted advanced pediatric EEG and neuroimaging devices, leading to faster detection and improved management of pediatric seizure disorders

- Growing parental awareness, coupled with the push for preventive pediatric healthcare, is further boosting market demand

- Expansion of pediatric neurology departments in hospitals and specialty clinics worldwide is supporting the adoption of these devices

- Government initiatives and funding for pediatric neurological research and treatment programs are also contributing to market growth

Restraint/Challenge

High Cost and Limited Accessibility in Emerging Regions

- Despite growing demand, the high cost of pediatric neurology devices and limited accessibility in developing regions remain significant barriers to adoption. These devices often require specialized training, calibration, and maintenance, which can limit their availability in smaller clinics or rural areas

- For instance, several community hospitals in Southeast Asia reported challenges in acquiring pediatric EEG machines due to high costs and supply chain limitations

- Limited reimbursement coverage, complex regulatory requirements, and the need for trained personnel can further slow adoption

- In addition, the high cost of advanced neuroimaging equipment and monitoring tools may restrict widespread use to larger healthcare centers

- Addressing these challenges through cost-effective devices, regional manufacturing, training programs, and government support will be essential for sustained growth in the Pediatric Neurology Devices market

Pediatric Neurology Devices Market Scope

The market is segmented on the basis of type, service and treatment, neurological subspecialties, age group, and end user.

- By Type

On the basis of type, the Pediatric Neurology Devices market is segmented into neurosurgery devices, neurostimulator, and cerebrospinal fluid (CSF) management devices. The neurosurgery devices segment dominated the market with the largest revenue share of 42.5% in 2025, primarily due to the rising prevalence of congenital neurological disorders, brain injuries, and cranial malformations in pediatric patients. Neurosurgery devices are crucial for precision surgeries and minimally invasive interventions, which reduces surgical risks and enhances recovery outcomes. Hospitals and specialized neurological centers continue to adopt these devices due to their proven clinical efficacy and high reliability. Technological advancements, including pediatric-specific surgical tools and robotic-assisted devices, further strengthen their market position. The segment benefits from increasing awareness among caregivers and healthcare professionals about early surgical interventions. Well-established manufacturers offering comprehensive portfolios enhance accessibility. Compatibility with advanced imaging and navigation systems drives adoption. Government and private hospital investments in pediatric neurology also support revenue growth. Continuous innovation in device safety, ergonomics, and minimally invasive techniques further strengthens dominance.

The CSF management devices segment is expected to witness the fastest CAGR of 20.3% from 2026 to 2033, driven by the rising incidence of hydrocephalus and other cerebrospinal fluid disorders in neonates and children. Advances such as programmable shunts, minimally invasive implantation methods, and homecare-compatible systems are fueling adoption. Hospitals are increasingly investing in specialized pediatric neurology units equipped with advanced CSF management devices. The segment also benefits from awareness campaigns emphasizing early diagnosis and treatment. Reduced procedure time, improved post-surgical outcomes, and cost-effectiveness further drive adoption. Regulatory approvals for pediatric-specific devices and reimbursement schemes in developed countries support rapid growth. Manufacturers are introducing innovative products with enhanced monitoring and remote adjustability features. Expanding clinical research and trials for novel CSF management technologies contribute to market acceleration. Integration with digital health platforms allows remote patient monitoring, enhancing appeal. Additionally, emerging markets are witnessing increased accessibility due to growing healthcare infrastructure. Pediatric caregivers and clinicians increasingly prefer these devices for long-term therapeutic benefits.

- By Service and Treatment

On the basis of service and treatment, the market is segmented into electroencephalogram (EEG), intrathecal baclofen therapy, neurological evaluations, and vagal nerve stimulation (VNS). The EEG segment held the largest market revenue share of 38.9% in 2025, owing to its essential role in diagnosing epilepsy, seizure disorders, and other neurological abnormalities in children. EEG is a non-invasive, cost-effective diagnostic tool widely adopted across hospitals, neurological centers, and research facilities. Technological advancements such as digital EEG systems, AI-assisted signal interpretation, and telemonitoring improve diagnostic accuracy and efficiency. Hospitals increasingly deploy portable EEG devices for bedside monitoring and neonatal care units. The segment benefits from clinical guidelines recommending routine monitoring and early diagnosis of pediatric neurological disorders. The rising prevalence of epilepsy and other chronic neurological conditions fuels consistent demand. Integration with electronic medical records and telemedicine platforms enhances workflow efficiency. Reimbursement policies in developed regions support adoption. Educational programs and training for healthcare professionals improve utilization. Manufacturers focus on innovation to reduce noise interference, improve sensitivity, and enhance data management. Parents and caregivers are becoming more aware of early neurological assessments, increasing market penetration.

The vagal nerve stimulation (VNS) therapy segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, due to its growing application in drug-resistant epilepsy and neurodevelopmental disorders. Technological improvements such as minimally invasive implantable devices, remote programmability, and longer battery life are driving adoption. Increased hospital investments in specialized pediatric neurology departments and government funding for advanced treatment options accelerate growth. Rising awareness of therapeutic alternatives for refractory epilepsy and neurobehavioral conditions contributes significantly. Manufacturers are innovating devices with adaptive stimulation and remote monitoring capabilities. Clinical research and trials supporting long-term efficacy reinforce adoption. Training programs for physicians enhance implementation. Hospitals and research centers are expanding pediatric VNS therapy availability. The segment benefits from favorable reimbursement policies in developed countries. Continuous product improvements, including MRI-safe implants and non-invasive stimulation options, drive market expansion. Awareness campaigns targeting caregivers and healthcare professionals further stimulate adoption. Emerging markets show growing uptake due to healthcare infrastructure development and affordability of devices.

- By Neurological Subspecialties

On the basis of neurological subspecialties, the market is segmented into neuro-oncology, neuromuscular, neonatal neurology, neuro-immunology, and stroke. The neonatal neurology segment dominated with a 35.4% revenue share in 2025, fueled by the rising focus on premature births, congenital neurological disorders, and neonatal intensive care unit (NICU) monitoring. Hospitals are investing heavily in advanced neonatal neurology devices to ensure early diagnosis and intervention, which improves survival rates and developmental outcomes. Technological advancements such as non-invasive monitoring, continuous vital sign tracking, and AI-assisted diagnostics further support adoption. Research initiatives and collaborations between hospitals and academic institutions promote the development and usage of neonatal-specific neurology devices. Government policies supporting neonatal healthcare and reimbursement programs drive further adoption. Integration with neonatal ICU monitoring systems enhances device utility. Caregivers increasingly seek early intervention tools, boosting demand. Specialized training for clinicians improves adoption rates. Hospitals aim to reduce long-term neurological complications, which reinforces market dominance. Innovations in portable neonatal devices provide additional flexibility for homecare or remote monitoring.

The neuro-immunology segment is expected to witness the fastest CAGR of 18.8% from 2026 to 2033, due to the increasing prevalence of autoimmune and inflammatory neurological disorders among children. Advancements in diagnostics and therapeutic devices, along with improved access to specialty care centers, drive adoption. Pediatric neuro-immunology centers are expanding globally, supported by increasing government and private funding. Early diagnosis and management programs for conditions such as pediatric multiple sclerosis and autoimmune encephalitis promote rapid adoption. Integration of devices with digital health platforms and patient monitoring tools enhances clinical utility. Research and clinical trials for innovative therapies reinforce device deployment. Caregiver awareness initiatives and advocacy campaigns further drive adoption. Technological innovations in portable and minimally invasive devices support wider use. Hospitals and specialized clinics increasingly prefer these devices for accurate monitoring and therapeutic interventions. Insurance coverage and reimbursement improvements facilitate accessibility in developed markets.

- By Age Group

On the basis of age group, the market is segmented into neonates, infants, children, and adolescents. The children segment held the largest market share of 40.2% in 2025, driven by the high prevalence of epilepsy, neuromuscular disorders, and cranial malformations in this age group. Pediatric neurology devices are widely used for both diagnostic and therapeutic purposes in children due to their critical role in early intervention. Hospitals and research centers increasingly adopt child-friendly, non-invasive, and minimally invasive devices. Continuous innovations in device ergonomics, safety, and usability strengthen adoption. Awareness campaigns targeting parents and healthcare providers encourage early diagnosis and treatment. Reimbursement policies and government support in developed regions also support growth. Training programs for clinicians enhance efficient use. Devices integrated with telemedicine and digital platforms improve monitoring and care. Increasing hospital investments in pediatric neurology departments drive higher device uptake. Hospitals and specialty clinics prefer advanced devices to reduce long-term neurological complications.

The neonates segment is projected to grow at the fastest CAGR of 20.1% from 2026 to 2033, driven by premature birth rates, congenital disorder prevalence, and increasing NICU admissions. Technological advancements in neonatal monitoring, portable devices, and homecare-compatible systems support rapid growth. Hospitals are investing in specialized neonatal neurology units. Awareness programs for early intervention and caregiver education accelerate adoption. Integration of neonatal neurology devices with advanced ICU monitoring systems enhances clinical workflow. Manufacturers are introducing minimally invasive and non-invasive devices suitable for neonates. Expanding healthcare infrastructure in emerging markets further drives market penetration. Favorable reimbursement policies in developed countries facilitate adoption. Research and clinical trials validate new device efficacy. Digital health integration for remote monitoring is contributing to growth.

- By End User

On the basis of end user, the market is segmented into hospitals, healthcare centers, and neurological research centers. The hospitals segment dominated with a 45.7% revenue share in 2025, driven by high pediatric neurology procedure volumes, advanced infrastructure, and availability of skilled healthcare professionals. Hospitals are investing in cutting-edge neurology devices for both diagnostic and therapeutic interventions. Government healthcare initiatives and reimbursement schemes further support adoption. Hospitals prioritize minimally invasive and non-invasive devices to improve patient outcomes. Integration with electronic medical records and telemedicine platforms enhances operational efficiency. Specialized pediatric neurology departments in hospitals contribute to consistent demand. Training and certification programs for clinicians ensure efficient device utilization. Collaborations with manufacturers for device customization strengthen hospital adoption. Hospitals seek devices that reduce long-term neurological complications and hospitalization costs. Awareness campaigns targeting parents and caregivers encourage hospital visits for early intervention.

The neurological research centers segment is expected to witness the fastest CAGR of 19.3% from 2026 to 2033, fueled by increasing government and private funding for pediatric neurology research and clinical trials. Research centers are expanding their infrastructure and adopting innovative devices for experimental and diagnostic purposes. Collaborative research programs with hospitals and academic institutions accelerate adoption. Funding for studies on neurological disorders and device efficacy promotes growth. Research centers focus on advanced technologies such as AI-assisted monitoring, remote patient tracking, and minimally invasive interventions. Technological advancements and early access to prototypes drive device adoption. Publications and research outcomes contribute to credibility and further expansion. Emerging markets show rising investment in research infrastructure. Digital integration for remote trials and monitoring supports growth. Research centers are increasingly preferred for training and development of new device protocols.

Pediatric Neurology Devices Market Regional Analysis

- North America dominated the pediatric neurology devices market with the largest revenue share of approximately 44.5% in 2025

- Supported by a well‑established healthcare infrastructure, high clinical adoption of advanced devices, strong reimbursement policies, and the presence of major industry players

- The market accounted for the majority of regional demand, driven by widespread adoption of diagnostic and therapeutic pediatric neurology devices in hospitals, specialty clinics, and academic medical centers

U.S. Pediatric Neurology Devices Market Insight

The U.S. pediatric neurology devices market captured the largest share within North America, fueled by increasing prevalence of neurological disorders in children, adoption of advanced EEG, neuroimaging, and neurostimulation devices, and strong R&D initiatives. The integration of innovative monitoring and diagnostic technologies, coupled with reimbursement support and awareness programs, is significantly contributing to the market’s expansion.

Europe Pediatric Neurology Devices Market Insight

The Europe Pediatric Neurology Devices market is projected to expand at a substantial CAGR during the forecast period, driven by government initiatives promoting pediatric healthcare, increasing awareness of neurological disorders, and the adoption of advanced clinical technologies. The region is experiencing growth across hospitals, rehabilitation centers, and specialty pediatric clinics, with ongoing incorporation of neurodiagnostic and therapeutic devices into routine care.

U.K. Pediatric Neurology Devices Market Insight

The U.K. pediatric neurology devices market is expected to grow at a noteworthy CAGR, supported by increased healthcare expenditure, rising clinical adoption of advanced pediatric neurology devices, and growing awareness of neurological conditions in children. The country’s strong healthcare network and emphasis on pediatric care are fostering market growth.

Germany Pediatric Neurology Devices Market Insight

Germany’s pediatric neurology devices market is anticipated to expand at a considerable CAGR, owing to advanced healthcare infrastructure, government initiatives supporting pediatric care, and increasing adoption of diagnostic and monitoring devices. Focus on innovation, research, and technologically advanced solutions is driving the integration of pediatric neurology devices across hospitals and specialty clinics.

Asia-Pacific Pediatric Neurology Devices Market Insight

The Asia-Pacific pediatric neurology devices market is expected to grow at the fastest CAGR during the forecast period, driven by expanding healthcare investments, rising awareness of pediatric neurological care, and increasing diagnosis rates in emerging markets such as China and India. Government programs, improved hospital infrastructure, and growing adoption of advanced pediatric neurodiagnostic and therapeutic devices are further propelling market growth.

Japan Pediatric Neurology Devices Market Insight

Japan’s pediatric neurology devices market is gaining momentum due to high healthcare standards, advanced medical technology adoption, and strong focus on pediatric care. The market is benefiting from increasing prevalence of neurological disorders in children and widespread use of EEG, imaging, and neurostimulation devices across hospitals and clinics.

China Pediatric Neurology Devices Market Insight

The China pediatric neurology devices market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising healthcare spending, growing awareness about pediatric neurological disorders, and expanding hospital infrastructure. Strong domestic manufacturing, supportive government initiatives, and increasing diagnosis rates are key factors driving market growth.

Pediatric Neurology Devices Market Share

The Pediatric Neurology Devices industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• Boston Scientific Corporation (U.S.)

• Abbott (U.S.)

• Stryker (U.S.)

• Integra LifeSciences Holdings Corporation (U.S.)

• Zimmer Biomet Holdings, Inc. (U.S.)

• NeuroPace, Inc. (U.S.)

• LivaNova PLC (U.K.)

• Natus Medical Incorporated (U.S.)

• GE Healthcare (U.S.)

• Philips Healthcare (Netherlands)

• B. Braun Melsungen AG (Germany)

• Fisher & Paykel Healthcare (New Zealand)

• Canon Medical Systems Corporation (Japan)

Latest Developments in Global Pediatric Neurology Devices Market

- In February 2023, Natus Medical Incorporated launched an advanced pediatric EEG monitoring device with cutting‑edge algorithms for improved seizure detection and real‑time monitoring, designed specifically to enhance diagnostic accuracy and treatment planning for children with neurological disorders. This updated device integrates sophisticated analytics to help clinicians quickly detect and monitor abnormal brain activity in pediatric patients, reflecting a broader trend of integrating digital technologies into pediatric neurology diagnostics. The launch underscores the emphasis on improving early diagnosis and individualized care for children suffering from epilepsy and other neurological conditions

- In May 2023, Nihon Kohden Corporation received regulatory approval for a novel EEG device tailored specifically for pediatric patients with epilepsy, following rigorous safety and performance evaluations. This approval highlights the company’s commitment to pediatric neurology care and addresses a critical unmet need for specialized diagnostic equipment for young patients, where accurate EEG readings are essential for effective seizure management and treatment customization

- In July 2023, Anuncia Medical Inc. announced the U.S. commercial launch of its ReFlow Mini Flusher device, an FDA‑cleared cerebrospinal fluid (CSF) management system designed to help manage hydrocephalus and similar conditions across broader age groups, including infants. With its reduced size and streamlined profile, the device supports more versatile use in pediatric neurological care and expands treatment options for conditions requiring CSF diversion therapies

- In November 2023, Allied Market Research published a major market outlook report projecting that the global pediatric neurology devices market would reach USD 5.84 billion by 2031, growing at about 7.8% CAGR from 2022 to 2031. This forecast underscores significant growth prospects and reflects ongoing advancements in pediatric neurology technologies driving demand in diagnosis and treatment tools

- In April 2025, Ceribell, Inc. announced that the U.S. FDA granted 510(k) clearance for its next‑generation Clarity algorithm specifically for pediatric patients aged 1 year and older, making it the first FDA‑cleared AI‑enabled technology for rapid bedside detection and diagnosis of electrographic (non‑convulsive) seizures in young children. The clearance supports faster clinical decision‑making in emergency and critical care settings, enhancing pediatric neurologic emergency response and patient outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.