Global Pellagra Market

Market Size in USD Million

USD

450.05 Million

USD

664.93 Million

2024

2032

USD

450.05 Million

USD

664.93 Million

2024

2032

| 2025 - 2032 | |

| USD 450.05 Million | |

| USD 664.93 Million | |

| % | |

|

Pellagra Market Size

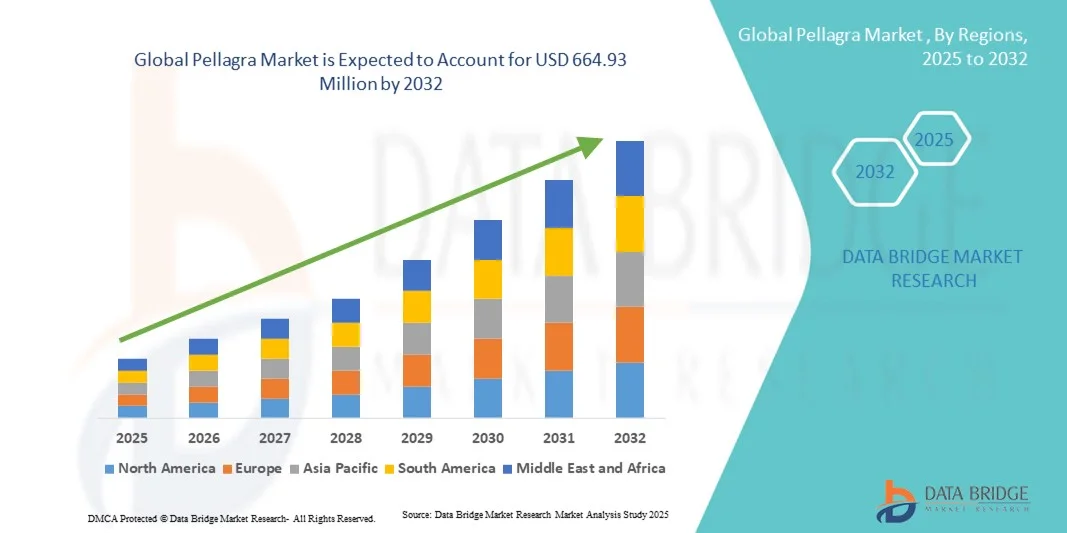

- The global pellagra market size was valued at USD 450.05 million in 2024 and is expected to reach USD 664.93 million by 2032, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of Pellagra, primarily caused by niacin (vitamin B3) deficiency, and growing awareness regarding early diagnosis and management

- Furthermore, rising demand for effective vitamin supplementation, fortified foods, and therapeutic interventions, along with government initiatives to address nutritional deficiencies, is accelerating the adoption of Pellagra treatment solutions, thereby significantly boosting the industry’s growth

Pellagra Market Analysis

- Pellagra, a nutritional disorder caused by niacin (Vitamin B3) deficiency, is increasingly recognized due to its prevalence in regions with poor dietary diversity and malnutrition. The condition can lead to dermatitis, diarrhea, dementia, and if untreated, death. Rising awareness about nutritional deficiencies, public health initiatives, and improved diagnostic capabilities have made pellagra a critical focus in preventive healthcare

- The escalating demand for pellagra prevention and treatment is primarily fueled by growing public health campaigns, government nutrition programs, and increasing efforts to fortify staple foods with niacin. Expanded awareness of early detection and supplementation benefits has driven adoption of therapeutic interventions and enriched diets in affected regions

- North America dominated the pellagra market with the largest revenue share of 38.7% in 2024, attributed to advanced healthcare infrastructure, government-led nutrition programs, and higher public awareness. The U.S. led regional growth, driven by niacin fortification initiatives, clinical interventions for at-risk populations, and research on improving maternal and child nutrition outcomes

- Asia-Pacific is expected to be the fastest-growing region in the pellagra market during the forecast period, with a projected CAGR due to increasing urbanization, rising awareness of nutritional deficiencies, and expanding public health programs in countries like India, China, and Indonesia. Efforts to improve dietary diversity and implement food fortification programs are expected to support rapid growth in the region

- The Niacin segment dominated the pellagra market with the largest market revenue share of 46.1% in 2024, due to its proven efficacy in replenishing niacin levels and reversing pellagra symptoms

Report Scope and Pellagra Market Segmentation

|

Attributes |

Pellagra Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Pellagra Market Trends

Rising Focus on Nutritional Deficiency Awareness and Preventive Healthcare

- A significant and accelerating trend in the global pellagra market is the increasing focus on preventive healthcare and nutritional awareness programs

- Governments, NGOs, and healthcare organizations are emphasizing early detection and management of niacin deficiency through community health campaigns, supplementation programs, and dietary fortification initiatives

- For instance, in 2023, multiple public health campaigns in sub-Saharan Africa and South Asia highlighted the importance of Vitamin B3-rich diets and fortified foods to prevent Pellagra, especially in vulnerable populations such as children and pregnant women

- The trend is also driven by rising interest in maternal and child nutrition, with healthcare providers increasingly recommending niacin supplements as part of routine nutritional care

- Educational initiatives, combined with government-backed supplementation programs, are enabling wider awareness and adoption of preventive measures

- Moreover, fortified foods, multivitamins, and dietary supplements are gaining traction globally, reflecting consumer preference for proactive health management

- This trend towards preventive nutrition and early intervention is reshaping market expectations and encouraging investments in educational and supplement distribution programs

Pellagra Market Dynamics

Driver

Growing Need for Nutritional Deficiency Management and Public Health Awareness

- The increasing prevalence of niacin deficiency and associated health complications is a key driver for the Pellagra market. Rising malnutrition cases in developing countries, coupled with growing awareness regarding the importance of Vitamin B3, are significantly contributing to market growth

- For instance, in March 2023, the World Health Organization highlighted the need for community-level nutritional intervention programs in regions with high niacin deficiency prevalence, encouraging fortified food initiatives and supplementation programs. Such efforts are expected to boost the adoption of Pellagra therapies and preventive measures during the forecast period

- As governments and NGOs intensify awareness campaigns and public health initiatives, demand for dietary supplements, fortified foods, and therapeutic interventions is rising. Educational programs emphasizing maternal and child nutrition, especially in high-risk regions, are further propelling market growth

- Furthermore, the increasing focus on preventive healthcare and wellness, alongside the rise in chronic conditions exacerbated by nutritional deficiencies, is promoting the adoption of both therapeutic and prophylactic interventions for Pellagra

- Growing accessibility to healthcare services, particularly in rural areas, combined with government-supported fortification and supplementation programs, is further expanding the patient pool for Pellagra management

Restraint/Challenge

Limited Awareness, Accessibility Barriers, and Treatment Costs

- Despite growing awareness, limited knowledge about pellagra and its treatment options in several regions remains a key challenge to market penetration. In areas with low health literacy, patients often remain undiagnosed or untreated, constraining market growth

- The affordability and accessibility of niacin-rich supplements, fortified foods, and therapeutic interventions can be limited in low-income regions, particularly in rural areas, hindering widespread adoption

- Addressing these challenges requires stronger government initiatives, community outreach programs, and educational campaigns to improve understanding of Pellagra symptoms, prevention, and treatment options

- In addition, the cost of high-quality supplements and fortified formulations can be a barrier for budget-conscious consumers, even in urbanized regions. While generic and lower-cost alternatives are becoming more widely available, the perceived value of specialized nutritional therapies can still impact uptake

- Ensuring equitable distribution of therapeutic and preventive solutions, improving supply chain efficiency, and raising public awareness through targeted campaigns will be crucial for sustained market growth

Pellagra Market Scope

The market is segmented on the basis of type, drugs, dosage strength, end-users, and distribution channel.

- By Type

On the basis of type, the Pellagra market is segmented into Primary Pellagra and Secondary Pellagra. The Primary Pellagra segment dominated the market with the largest revenue share of 43.8% in 2024, driven by the high prevalence of niacin deficiency due to poor dietary intake in affected populations. Primary Pellagra occurs mainly in regions with insufficient nutrition and is often linked to maize-based diets lacking niacin or tryptophan. Awareness campaigns and public health interventions targeting malnourished communities have strengthened early diagnosis and treatment. Oral supplementation with niacin and niacinamide is widely adopted. Government programs support distribution in high-risk areas. Screening in dermatology and specialty clinics ensures timely detection. Clinical research supports the effectiveness of preventive interventions. Education on dietary diversification helps reduce incidence. Community nutrition programs and fortified food initiatives further strengthen adoption. Hospitals and clinics are primary care points for treatment. Maternal and child health programs often integrate pellagra prevention.

The Secondary Pellagra segment is expected to witness the fastest CAGR of 7.5% from 2025 to 2032, driven by increasing awareness of pellagra caused by chronic illnesses, alcoholism, or malabsorption disorders. Secondary Pellagra patients often require targeted medical interventions. Hospitals and specialty clinics provide personalized treatment plans. Rising prevalence of gastrointestinal disorders that impair nutrient absorption fuels demand. Adoption of niacinamide therapy is increasing due to high effectiveness and low side effects. Nutrition counseling complements treatment in clinical settings. Telemedicine platforms support follow-up care and monitoring. Awareness programs for at-risk populations improve early detection. Research on combination therapies enhances patient outcomes. Hospital-based interventions are expanding in emerging markets. Public health campaigns emphasize screening for secondary causes. Clinical studies continue to optimize therapeutic protocols.

- By Drugs

On the basis of drugs, the Pellagra market is segmented into Niacin and Niacinamide. The Niacin segment held the largest market revenue share of 46.1% in 2024, due to its proven efficacy in replenishing niacin levels and reversing pellagra symptoms. Niacin is widely available in oral tablet form and integrated into public health supplementation programs. Hospitals and specialty clinics favor niacin for its rapid therapeutic effect. Government nutrition initiatives distribute niacin supplements in high-risk regions. Clinical research supports its safety profile and effectiveness. Niacin is often combined with dietary counseling to ensure sustained recovery. Educational campaigns reinforce the importance of niacin intake. Patients show high compliance due to low side effects and convenience. Maternal and child nutrition programs often incorporate niacin. Hospitals ensure proper dosing and monitoring. Community health workers aid in supplementation distribution.

The Niacinamide segment is projected to witness the fastest CAGR of 8.0% from 2025 to 2032, driven by increasing adoption in patients with secondary pellagra and those with comorbidities. Niacinamide has lower flushing side effects compared to niacin, improving patient compliance. Specialty clinics and dermatology centers favor niacinamide for long-term management. Awareness programs targeting clinicians emphasize its effectiveness in diverse patient groups. Telemedicine services are promoting adherence to niacinamide therapy. Rising incidence of malabsorption and chronic conditions boosts demand. Hospitals implement combination therapy protocols including niacinamide. Patient education and counseling improve clinical outcomes. Research on optimized dosing supports better bioavailability. Nutrition programs in developing regions integrate niacinamide. Pharmaceutical companies are expanding production and distribution.

- By Dosage Strength

On the basis of dosage strength, the Pellagra market is segmented into 50mg, 100mg, 250mg, and 500mg. The 100mg dosage strength segment dominated the market with a share of 42.7% in 2024, as it provides an optimal balance between therapeutic efficacy and patient tolerance. Widely used in oral tablets and fortified foods, this strength ensures rapid replenishment of niacin without significant side effects. Hospitals and clinics prescribe it for both preventive and treatment purposes. Government-supported supplementation programs often include the 100mg formulation. Educational campaigns on correct dosage promote safe usage. Maternal and child health programs adopt this strength in routine supplementation. Clinical studies confirm its effectiveness for symptom reversal. Nutritional counseling improves adherence. Community health workers distribute this dosage in high-risk areas. Availability in retail pharmacies supports easy access. Research continues to validate its efficacy in diverse populations.

The 250mg dosage strength segment is projected to witness the fastest CAGR of 7.8% from 2025 to 2032, driven by increasing demand in severe pellagra cases and secondary deficiency patients. Hospitals and specialty clinics prefer this higher dosage for acute symptom management. Clinicians recommend 250mg formulations in treatment protocols for malnourished populations. Rising prevalence of secondary pellagra due to chronic illnesses supports adoption. Combination therapy with niacin and supportive nutrients enhances recovery. Telemedicine follow-ups encourage adherence. Clinical trials support safety and efficacy at this strength. Government programs in high-risk regions distribute higher-dose formulations. Patient education promotes proper usage. Specialty clinics in urban areas increasingly adopt the 250mg dosage. Research on bioavailability improvements supports growth.

- By End-Users

On the basis of end-users, the Pellagra market is segmented into Dermatology Clinics, Specialty Clinics, Hospitals, and Others. The Hospitals segment accounted for the largest revenue share of 48.3% in 2024, due to the availability of diagnostic and treatment facilities for severe pellagra cases. Hospitals provide oral and injectable niacin and niacinamide therapies. High patient volumes in dermatology and nutrition departments support segment dominance. Hospitals implement standardized treatment protocols. Government-supported supplementation programs are distributed through hospitals. Clinical monitoring ensures safe and effective dosing. Patient education enhances adherence. Maternal and child health initiatives are integrated into hospital programs. Telemedicine services help track patient outcomes. Hospitals collaborate with specialty clinics for follow-up care. Community outreach programs utilize hospitals as distribution hubs. Pharmaceutical partnerships ensure supply reliability.

The Specialty Clinics segment is expected to witness the fastest CAGR of 7.6% from 2025 to 2032, fueled by rising demand for outpatient management of mild to moderate pellagra cases. Clinics provide targeted counseling, supplementation, and follow-up care. Telehealth platforms support adherence monitoring. Clinics in urban areas expand access to patients seeking convenience. Rising awareness among clinicians encourages early detection and treatment. Education on dietary supplementation complements therapy. Clinics often coordinate with hospitals for complex cases. Public health initiatives use clinics to reach high-risk populations. Specialty clinics adopt niacinamide therapy for better patient tolerance. Private healthcare expansion supports rapid segment growth. Research programs in clinics promote optimal dosing strategies. Patient-centric care models drive adoption.

- By Distribution Channel

On the basis of distribution channel, the Pellagra market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated the market with a share of 45.9% in 2024, due to centralized procurement and direct distribution of niacin and niacinamide supplements. Hospital pharmacies ensure accurate dosing and regulatory compliance. Integration with maternal and child nutrition programs strengthens adoption. Hospitals manage both inpatient and outpatient cases. Bulk procurement agreements secure consistent supply. Clinical staff provide counseling and monitor adherence. Hospitals serve as distribution hubs for surrounding clinics and communities. Government programs often channel supplements through hospital pharmacies. Trusted supply chains and pharmaceutical partnerships ensure product quality. Telehealth integration allows monitoring of supplement use. Hospitals also distribute fortified foods in community programs.

The Online Pharmacy segment is projected to witness the fastest CAGR of 8.3% from 2025 to 2032, fueled by rising digital adoption and demand for home delivery of supplements. Patients can conveniently order niacin and niacinamide online. Telemedicine services ensure prescription verification and adherence. Delivery in remote areas improves access. E-commerce growth and internet penetration support expansion. Subscription and auto-refill services enhance compliance. Patient education and support resources are available online. Partnerships with logistics providers ensure safe delivery. Digital platforms allow personalized nutrition guidance. Private healthcare networks promote online pharmacy adoption. Rising awareness of convenient access drives growth. Online channels complement hospital and retail distribution.

Pellagra Market Regional Analysis

- North America dominated the pellagra market with the largest revenue share of 38.7% in 2024, attributed to advanced healthcare infrastructure, government-led nutrition programs, and higher public awareness

- The market led regional growth, driven by niacin fortification initiatives, clinical interventions for at-risk populations, and research on improving maternal and child nutrition outcomes

- Programs targeting maternal nutrition, pediatric care, and high-risk communities have further strengthened the market, ensuring widespread access to preventive measures and treatments

U.S. Pellagra Market Insight

The U.S. pellagra market captured the largest revenue share within North America in 2024, fueled by nationwide nutrition surveillance programs, strong government policies on vitamin fortification, and high public health spending. The country has witnessed extensive adoption of niacin-enriched food products and supplements, supported by federal nutrition assistance schemes and clinical outreach for low-income populations. Continuous research into micronutrient deficiency management and the integration of digital health tools for dietary monitoring are further contributing to market expansion. Additionally, growing awareness among consumers regarding balanced nutrition and preventive healthcare continues to enhance the country’s market outlook.

Europe Pellagra Market Insight

The Europe pellagra market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of nutritional deficiencies and government-led public health initiatives. Rising urbanization, coupled with strong focus on preventive healthcare, is fostering early detection and treatment of niacin deficiency across the region. Significant growth is expected in both residential and institutional healthcare settings, supported by dietary fortification programs and education campaigns targeting at-risk populations.

U.K. Pellagra Market Insight

The U.K. pellagra market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by growing awareness of maternal and child nutrition and increased healthcare outreach programs. Initiatives promoting balanced diets, supplementation, and early diagnosis of niacin deficiency are expected to drive market growth. Government programs and collaborations with healthcare providers are enhancing access to preventive and therapeutic interventions for vulnerable populations.

Germany Pellagra Market Insight

The Germany pellagra market is expected to expand at a considerable CAGR during the forecast period, supported by increasing awareness of nutritional disorders and public health campaigns. Well-developed healthcare infrastructure, coupled with government-backed fortification and supplementation programs, is driving early detection and treatment of Pellagra. The region emphasizes preventive nutrition measures, particularly for children, pregnant women, and the elderly, contributing to steady market growth.

Asia-Pacific Pellagra Market Insight

The Asia-Pacific pellagra market is expected to grow at the fastest CAGR during the forecast period, driven by increasing urbanization, rising awareness of nutritional deficiencies, and expanding public health programs in countries such as India, China, and Indonesia. Efforts to improve dietary diversity, implement niacin fortification programs, and promote maternal and child health initiatives are expected to support rapid market growth. The growing emphasis on preventive healthcare, combined with expanding healthcare access in urban and rural areas, is facilitating widespread adoption of interventions and supplementation strategies.

Japan Pellagra Market Insight

The Japan pellagra market is gaining momentum due to rising awareness of nutritional deficiencies and government-supported dietary programs. Emphasis on maternal and child nutrition, along with preventive health initiatives, is driving adoption of niacin supplementation and fortified foods. Educational campaigns targeting at-risk populations and collaborations between public health agencies and healthcare providers are contributing to steady market growth.

China Pellagra Market Insight

The China pellagra market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to expanding healthcare infrastructure, increasing awareness of nutritional deficiencies, and growing government-led fortification programs. National initiatives promoting dietary diversification, food fortification, and maternal-child nutrition programs are key factors supporting market expansion. Improved access to healthcare services and community-level education programs are facilitating early detection, preventive interventions, and treatment of Pellagra.

Pellagra Market Share

The Pellagra industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- GSK Plc. (U.K.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Bayer AG (Germany)

- Abbott (U.S.)

- Cipla Limited (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Aurobindo Pharma Limited (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Natco Pharma Limited (India)

- Fresenius Kabi AG (Germany

Latest Developments in Global Pellagra Market

- In February 2024, a case report titled “Pellagra presentation with dermatitis and dysphagia” was published in Frontiers in Medicine. The report describes a patient in rural Ethiopia who presented primarily with photosensitive dermatitis and progressive difficulty swallowing (dysphagia), without the full classical triad of symptoms (i.e. no diarrhea or neurologic symptoms). Niacin supplementation led to clinical recovery. This case highlights the need for clinicians to consider pellagra even when only partial symptoms appear

- In November 2024, a clinical article on “Alcoholic Pellagrous Encephalopathy” was published, documenting a rare neurological manifestation of pellagra in a chronic alcohol user. The patient exhibited delirium without the typical rash, making the diagnosis challenging. The case emphasized the importance of considering pellagra in differential diagnosis of encephalopathy in alcoholics. Niacin therapy contributed to recovery

- In August 2025, a case in Cureus documented a patient with a history of bariatric surgery, Whipple procedure, and alcohol use disorder developing pellagra. The complexity of the patient’s medical history made diagnosis difficult, but treatment with niacin supplementation led to symptom improvement. This case underscores that surgical and metabolic conditions can precipitate pellagra even in patients with ostensibly adequate diets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.