Global Perforating Disorder Treatment Market

Market Size in USD Billion

USD

7.22 Billion

USD

10.58 Billion

2024

2032

USD

7.22 Billion

USD

10.58 Billion

2024

2032

| 2025 - 2032 | |

| USD 7.22 Billion | |

| USD 10.58 Billion | |

| % | |

|

Perforating Disorder Treatment Market Size

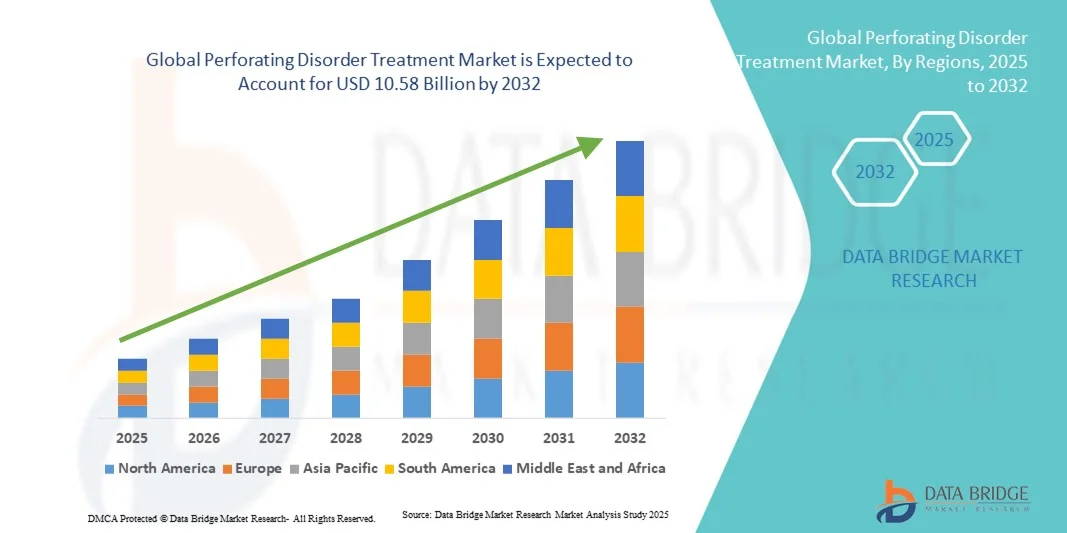

- The global perforating disorder treatment market size was valued at USD 7.22 billion in 2024 and is expected to reach USD 10.58 billion by 2032, at a CAGR of 4.90% during the forecast period

- The market growth is largely fueled by the growing advancement in dermatological research, coupled with the rising prevalence of chronic kidney disease, diabetes, and other systemic conditions that contribute to the development of perforating disorders. Increasing awareness among healthcare professionals and patients about early diagnosis and treatment options is further propelling market expansion globally

- Furthermore, the rising demand for effective and minimally invasive treatment solutions such as laser therapy, topical retinoids, and phototherapy is establishing modern dermatological care as the preferred approach for managing perforating disorders. These converging factors are accelerating the uptake of Perforating Disorder Treatment solutions, thereby significantly boosting the industry's growth

Perforating Disorder Treatment Market Analysis

- Perforating disorder treatment options, including topical therapies, systemic medications, and advanced dermatological procedures such as laser therapy and cryotherapy, are increasingly vital components of modern dermatology practice due to their effectiveness in managing chronic skin manifestations and preventing secondary infections in both hospital and outpatient settings. The growing emphasis on patient comfort, minimally invasive techniques, and targeted therapies has significantly enhanced treatment outcomes and adoption rates across healthcare systems

- The escalating demand for perforating disorder treatments is primarily fueled by the rising prevalence of chronic diseases such as diabetes mellitus and chronic kidney disease, which are major underlying causes of acquired perforating dermatoses. Furthermore, increasing awareness about early dermatological intervention and advancements in topical drug delivery systems are driving greater patient compliance and clinical success

- North America dominated the perforating disorder treatment market with the largest revenue share of 41.3% in 2024, characterized by advanced healthcare infrastructure, high diagnosis rates, and a strong presence of leading pharmaceutical and dermatological research companies. The U.S. continues to lead in clinical trials and adoption of biologics and innovative topical agents, supported by favorable reimbursement frameworks and increased dermatologist engagement in rare skin disorder management

- Asia-Pacific is expected to be the fastest growing region in the perforating disorder treatment market during the forecast period, projected to grow at a CAGR from 2025 to 2032, driven by improving healthcare access, rising disposable incomes, and growing awareness of dermatological conditions. Countries like India, China, and Japan are witnessing increased adoption of advanced skin treatments and government initiatives aimed at chronic disease management, further fueling market growth

- The acetaminophen segment dominated the largest market revenue share of 43.1% in 2024, driven by its extensive usage for pain and fever management in patients suffering from tympanic membrane perforations

Report Scope and Perforating Disorder Treatment Market Segmentation

|

Attributes |

Perforating Disorder Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Perforating Disorder Treatment Market Trends

Enhanced Convenience Through AI and Precision-Based Diagnosis

- A significant and accelerating trend in the global perforating disorder treatment market is the integration of artificial intelligence (AI), digital pathology, and precision-based diagnostic platforms. This combination is revolutionizing the identification and monitoring of perforating disorders by enabling faster, more accurate diagnosis and individualized treatment approaches

- For instance, in 2024, researchers developed AI-based dermatological imaging software capable of detecting perforating dermatoses such as Kyrle’s disease and perforating folliculitis with enhanced accuracy using automated lesion mapping and image analytics. Similarly, the use of digital pathology combined with machine learning models has allowed for high-resolution visualization of collagen and elastic fiber extrusion in affected tissues

- AI integration in dermatological and histopathological workflows enables clinicians to predict disease progression, assess treatment efficacy, and identify optimal therapeutic combinations for patients. For example, ongoing AI-driven clinical studies are leveraging algorithmic models to differentiate acquired perforating disorders from secondary skin manifestations linked to diabetes or renal dysfunction, improving treatment precision. Furthermore, AI-assisted systems support remote dermatology consultations, allowing experts to evaluate chronic perforating lesions more efficiently and consistently

- The seamless integration of AI-based analytics with electronic health records (EHR) and digital pathology platforms also facilitates centralized patient data management, allowing dermatologists and researchers to track treatment responses and identify recurrence patterns in real time. Through a single digital interface, clinicians can review clinical photographs, histopathology data, and therapeutic outcomes, supporting a holistic and data-driven approach to care

- This trend toward more intelligent, data-supported, and technology-enabled care pathways is fundamentally transforming how clinicians manage perforating disorders. Consequently, companies and research institutes are investing in AI-assisted diagnostics and treatment monitoring tools to enhance early detection and personalized management of chronic perforating dermatoses

- The demand for AI-integrated diagnostic and therapeutic solutions is increasing rapidly across hospitals, dermatology clinics, and research laboratories, as medical professionals seek to improve treatment outcomes, minimize diagnostic delays, and enhance clinical efficiency in managing perforating disorders

Perforating Disorder Treatment Market Dynamics

Driver

Growing Need Due to Rising Prevalence of Chronic Skin Conditions and Advancements in Dermatological Therapies

- The rising prevalence of chronic skin conditions such as diabetes mellitus, chronic renal failure, and autoimmune disorders—which are commonly associated with perforating dermatoses—is a key driver for the growth of the global perforating disorder treatment market

- For instance, in March 2024, a multinational clinical collaboration led by the Mayo Clinic and University of Tokyo launched a multicenter study exploring the efficacy of advanced retinoid formulations and biologic therapies in treating acquired perforating dermatoses. Such ongoing initiatives by key medical research organizations are expected to propel market expansion during the forecast period

- As healthcare professionals increasingly recognize the connection between systemic diseases and perforating disorders, there is growing demand for targeted therapies, including topical retinoids, keratolytic agents, and biologics that modulate immune response. These treatment options offer improved skin regeneration and reduced lesion recurrence rates compared to traditional symptomatic therapies

- Furthermore, advancements in molecular dermatology, combined with the development of minimally invasive drug delivery systems such as microneedle-based transdermal formulations, are revolutionizing treatment approaches for perforating disorders by enhancing drug absorption and patient compliance

- The growing awareness among dermatologists about perforating disorders, coupled with expanding diagnostic accessibility and pharmaceutical R&D investments, is boosting the overall growth of this therapeutic market segment. In addition, the rising availability of patient support programs and the inclusion of rare dermatological conditions in orphan disease frameworks are expected to further drive market expansion over the coming years

Restraint/Challenge

Limited Awareness, Diagnostic Challenges, and High Treatment Costs

- One of the major challenges restraining the growth of the perforating disorder treatment market is the limited awareness among both patients and healthcare providers, often leading to delayed or incorrect diagnosis. As perforating dermatoses frequently mimic other pruritic or inflammatory skin diseases, misdiagnosis can hinder appropriate therapeutic interventions

- For instance, multiple clinical reports have highlighted diagnostic delays exceeding six months in patients presenting with acquired perforating dermatoses secondary to chronic kidney disease, underscoring the need for improved dermatological screening protocols

- High treatment costs also pose a significant barrier, particularly in developing regions where advanced biologic or retinoid-based therapies remain inaccessible. The specialized diagnostic tools required for histopathological confirmation—such as high-resolution dermoscopy and digital biopsy imaging—add to the financial burden on healthcare systems and patients alike

- Moreover, the lack of standardized treatment guidelines and limited clinical trial data hinder uniform therapeutic practices across regions, affecting market consistency. While newer therapies show promise, reimbursement limitations for rare dermatologic diseases remain a critical obstacle to widespread adoption

- Addressing these challenges through public health awareness programs, clinician education, and the introduction of cost-effective treatment formulations will be crucial for overcoming barriers to diagnosis and care

- Continued collaboration between dermatology research centers, pharmaceutical developers, and healthcare policymakers is expected to mitigate these constraints and support sustainable growth in the perforating disorder treatment market

Perforating Disorder Treatment Market Scope

The market is segmented on the basis of drug class, treatment, diagnosis, distribution channel, and end user.

- By Drug Class

On the basis of drug class, the Perforating Disorder Treatment market is segmented into acetaminophen, ibuprofen, and others. The acetaminophen segment dominated the largest market revenue share of 43.1% in 2024, driven by its extensive usage for pain and fever management in patients suffering from tympanic membrane perforations. It remains the preferred choice due to its proven safety, low cost, and minimal gastrointestinal side effects compared to NSAIDs. The availability of multiple formulations including oral, intravenous, and pediatric variants boosts its accessibility across different patient demographics. Widespread prescription by ENT specialists and growing OTC consumption contribute to its continued market leadership. Moreover, increased awareness regarding safe self-medication practices and strong distribution channels further strengthen its dominance across both developed and developing markets.

The ibuprofen segment is expected to witness the fastest CAGR of 8.9% from 2025 to 2032, attributed to its superior anti-inflammatory properties that aid in reducing ear pain and swelling caused by infections. Rising adoption of combination therapies that include ibuprofen as a key component for managing middle ear inflammation drives the segment’s rapid growth. Pharmaceutical manufacturers are increasingly focusing on extended-release formulations to improve patient compliance. Growing online availability and rising acceptance of self-care medication trends in developed countries also fuel expansion. Moreover, awareness regarding the therapeutic advantages of ibuprofen in ENT conditions supports strong future demand globally.

- By Treatment

On the basis of treatment, the Perforating Disorder Treatment market is segmented into eardrum patch, surgery, drugs, and others. The eardrum patch segment dominated the largest revenue share of 39.4% in 2024, primarily due to its minimally invasive nature and high success rate in treating small tympanic membrane perforations. This treatment offers quick recovery and lower risk of complications, making it highly preferred among patients and ENT specialists. Advancements in bioresorbable materials and regenerative tissue technologies have further improved patch adhesion and healing outcomes. Hospitals and specialty clinics continue to adopt patch techniques as a first-line treatment option due to their cost-effectiveness. Supportive insurance coverage and government initiatives promoting minimally invasive ENT procedures have also reinforced the segment’s market position globally.

The surgery segment is expected to grow at the fastest CAGR of 9.5% from 2025 to 2032, supported by technological advancements in tympanoplasty and myringoplasty procedures. The rise in chronic perforation cases requiring reconstructive surgical interventions drives significant demand. Increasing adoption of endoscopic ear surgery and laser-assisted techniques enhances precision and reduces postoperative complications. Hospitals with advanced surgical infrastructure are witnessing increased patient footfall for complex cases. Growing healthcare spending and improved access to skilled ENT surgeons in developing regions are expected to further accelerate the segment’s growth trajectory over the forecast period.

- By Diagnosis

On the basis of diagnosis, the Perforating Disorder Treatment market is segmented into laboratory tests, tuning fork evaluation, tympanometry, and audiology exam. The audiology exam segment held the largest market revenue share of 38.7% in 2024, driven by its ability to accurately assess hearing impairment levels associated with tympanic membrane damage. The growing integration of digital audiometers and automated hearing evaluation devices across hospitals and clinics enhances diagnostic accuracy. Increasing awareness programs related to early detection of hearing loss also contribute to higher diagnostic rates. Moreover, expanding geriatric population and the prevalence of chronic otitis media are strengthening the demand for audiometric evaluations. Continuous technological advancements in audiology software and devices further sustain the segment’s leadership globally.

The tympanometry segment is expected to witness the fastest CAGR of 10.4% from 2025 to 2032, driven by the growing preference for non-invasive diagnostic tools that assess middle ear function effectively. Tympanometry provides rapid and reliable results, making it an essential test in ENT clinics and primary healthcare centers. Portable tympanometers and digital impedance systems are gaining popularity for pediatric ear screening programs. The rising availability of advanced diagnostic equipment and increasing government focus on preventive ear care further support the segment’s strong growth outlook.

- By Distribution Channel

On the basis of distribution channel, the Perforating Disorder Treatment market is segmented into hospital pharmacies and retail & online pharmacies. The hospital pharmacies segment accounted for the largest market revenue share of 46.9% in 2024, owing to the centralized distribution of prescription-based ENT medications and postoperative drugs. Hospitals ensure higher patient compliance due to direct physician prescriptions and controlled supply chains. Increasing inpatient admissions for surgical and patch procedures also enhance pharmaceutical demand through hospital pharmacies. Partnerships between hospitals and pharmaceutical firms ensure consistent product availability. Moreover, favorable government regulations and insurance reimbursements for hospital-based treatments further reinforce the segment’s leading position across major markets.

The retail & online pharmacies segment is expected to grow at the fastest CAGR of 11.2% from 2025 to 2032, propelled by digitalization in healthcare and rising preference for convenient, doorstep delivery of medications. Online platforms offer competitive pricing, wider product availability, and fast order fulfillment, encouraging consumers to shift toward e-pharmacies. Moreover, strategic collaborations between pharmaceutical manufacturers and e-commerce providers are enhancing visibility for ENT medications. Growing internet penetration, favorable regulatory reforms for online drug distribution, and increasing patient reliance on telemedicine platforms are expected to drive significant growth in this channel.

- By End User

On the basis of end user, the Perforating Disorder Treatment market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the largest revenue share of 45.6% in 2024, primarily due to their advanced surgical infrastructure, availability of skilled ENT specialists, and comprehensive postoperative care facilities. Hospitals serve as the key treatment centers for complex perforation cases requiring surgical intervention. Increasing government investments in healthcare infrastructure, coupled with the expansion of tertiary care ENT departments, have enhanced hospital capacities globally. High patient inflow, advanced diagnostic support, and availability of emergency ENT services further strengthen the segment’s dominance throughout the forecast period.

The specialty clinics segment is projected to grow at the fastest CAGR of 10.9% from 2025 to 2032, driven by the growing number of outpatient ENT facilities offering personalized treatment options. Specialty clinics provide focused diagnosis and cost-effective treatment procedures with shorter waiting times. The adoption of advanced diagnostic tools such as otoendoscopes and portable tympanometers enhances operational efficiency. Increasing awareness regarding early ENT care and the expansion of independent ENT clinics in urban areas support segmental growth. Furthermore, rising demand for personalized care and improved patient satisfaction levels continue to drive strong growth for this segment across developed markets.

Perforating Disorder Treatment Market Scope

- North America dominated the perforating disorder treatment market with the largest revenue share of 41.3% in 2024, characterized by advanced healthcare infrastructure, high diagnosis rates, and a strong presence of leading pharmaceutical and dermatological research companies

- The region’s dominance is also supported by growing awareness of rare dermatological disorders, the presence of specialty dermatology centers, and increased adoption of biologic and topical therapies

- The market continues to lead in clinical trials and approval of innovative treatment modalities, such as retinoid-based topical agents and immune-modulating therapies. Moreover, the region benefits from favorable reimbursement frameworks, high patient awareness, and growing dermatologist engagement in chronic perforating dermatosis management

U.S. Perforating Disorder Treatment Market Insight

The U.S. perforating disorder treatment market captured the largest revenue share in 2024 within North America, driven by robust investments in rare disease research and the expansion of dermatology-focused biotechnology companies. Increasing patient awareness, availability of specialized dermatologic services, and broad access to advanced diagnostic tools such as dermoscopy and histopathological imaging are major contributors to market dominance. Moreover, the rise in clinical research evaluating novel biologic agents, combined with the U.S. Food and Drug Administration’s (FDA) support for orphan disease programs, continues to stimulate innovation and accelerate therapeutic development in the country.

Europe Perforating Disorder Treatment Market Insight

The Europe perforating disorder treatment market is projected to grow steadily during the forecast period, supported by increasing prevalence of chronic kidney and diabetic-associated skin conditions and the availability of specialized dermatology centers across major countries such as Germany, France, and the U.K. European nations have implemented strong regulatory frameworks encouraging rare disease drug development, leading to growing interest from pharmaceutical and biotech firms. Moreover, collaborations between academic dermatology departments and clinical research networks are improving early diagnosis rates and patient management outcomes, contributing to sustained market expansion across the continent.

U.K. Perforating Disorder Treatment Market Insight

The U.K. perforating disorder treatment market is anticipated to grow at a notable CAGR during the forecast period, driven by national programs aimed at improving dermatologic care pathways and chronic disease management. Government initiatives supporting precision medicine and clinical registries for rare dermatologic conditions are enhancing visibility and therapeutic intervention for perforating dermatoses. In addition, the country’s strong academic base and investment in biologic research are expected to further strengthen its position as a key contributor to the regional market.

Germany Perforating Disorder Treatment Market Insight

The Germany perforating disorder treatment market is expected to expand at a significant CAGR during the forecast period, fueled by the nation’s focus on innovative dermatology research, biotechnology integration, and patient-centered healthcare models. Germany’s well-established clinical infrastructure, coupled with rising awareness of chronic skin disorders associated with systemic diseases, supports the adoption of advanced topical and biologic therapies. In addition, the country’s emphasis on sustainable healthcare and continuous R&D funding for dermatologic innovation reinforces its strong presence in the European market.

Asia-Pacific Perforating Disorder Treatment Market Insight

The Asia-Pacific perforating disorder treatment market is projected to grow at the fastest CAGR from 2025 to 2032, driven by improving healthcare access, rising disposable incomes, and increasing public awareness of dermatological health. The region’s expansion is supported by government-led initiatives promoting chronic disease management and the establishment of dermatology research institutes in countries such as China, Japan, and India. Rapid advances in clinical dermatology, coupled with expanding pharmaceutical distribution networks, are improving access to both conventional and novel treatment options. Furthermore, multinational pharmaceutical companies are increasingly partnering with regional firms to conduct clinical trials and distribute advanced therapies, broadening the availability of perforating disorder treatments across Asia-Pacific.

Japan Perforating Disorder Treatment Market Insight

The Japan perforating disorder treatment market is gaining momentum owing to the country’s robust dermatology infrastructure, advanced research in rare skin diseases, and patient awareness of personalized therapies. Japanese research centers are actively participating in international collaborations focusing on genetic and immune-mediated mechanisms of perforating dermatoses. The adoption of topical retinoids and biologic immunomodulators is growing rapidly, and government initiatives supporting rare disease treatment are fostering steady market growth throughout the forecast period.

China Perforating Disorder Treatment Market Insight

The China perforating disorder treatment market accounted for the largest revenue share within Asia-Pacific in 2024, supported by an expanding middle-class population, increasing healthcare expenditure, and a surge in dermatological R&D initiatives. Growing awareness about chronic skin conditions, combined with national healthcare reforms encouraging early diagnosis, is driving patient engagement in specialized treatment programs. Furthermore, domestic pharmaceutical companies are investing heavily in dermatology-focused product development and clinical trials. These factors, along with expanding access to hospital-based dermatology services and improved drug affordability, are positioning China as one of the key high-growth markets in Asia-Pacific.

Perforating Disorder Treatment Market Share

The Perforating Disorder Treatment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Johnson & Johnson and its affiliates (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

- Hoffmann-La Roche Ltd. (Switzerland)

- Cipla Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Bausch Health Companies Inc. (Canada)

- Glenmark Pharmaceuticals Ltd. (India)

- Otonomy Inc. (U.S.)

- Aurobindo Pharma Ltd. (India)

Latest Developments in Global Perforating Disorder Treatment Market

- In February 2022, a peer-reviewed case report described the successful use of Dupilumab in treating a patient with acquired perforating dermatosis (APD) associated with atopic dermatitis, marking a novel biologic therapy application beyond conventional topical or retinoid treatments

- In June 2023, a multicenter retrospective analysis of 37 APD cases provided new insights into treatment patterns and referenced narrow-band UV-B therapy as a recommended first-line treatment for reactive perforating collagenosis (RPC)

- In August 2024, a case report highlighted the successful management of a severe “giant” variant of acquired reactive perforating collagenosis (ARPC) using Allopurinol, demonstrating the potential repurposing of a xanthine-oxidase inhibitor for dermatologic conditions

- In September 2024, another case study detailed the use of Upadacitinib (a JAK-1 inhibitor) in a patient with APD, suggesting that immunomodulatory therapies could offer promising new treatment options for perforating disorders

- In January 2025, a comprehensive literature-based review of 189 patients across 124 studies on ARPC reaffirmed the importance of multimodal therapy—combining topical treatments, phototherapy, and systemic agents—as the most effective approach to manage perforating disorders

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.