Global Persistent Mullerian Duct Syndrome Market

Market Size in USD Billion

USD

185.50 Billion

USD

295.65 Billion

2024

2032

USD

185.50 Billion

USD

295.65 Billion

2024

2032

| 2025 - 2032 | |

| USD 185.50 Billion | |

| USD 295.65 Billion | |

| % | |

|

Persistent Mullerian Duct Syndrome Market Size

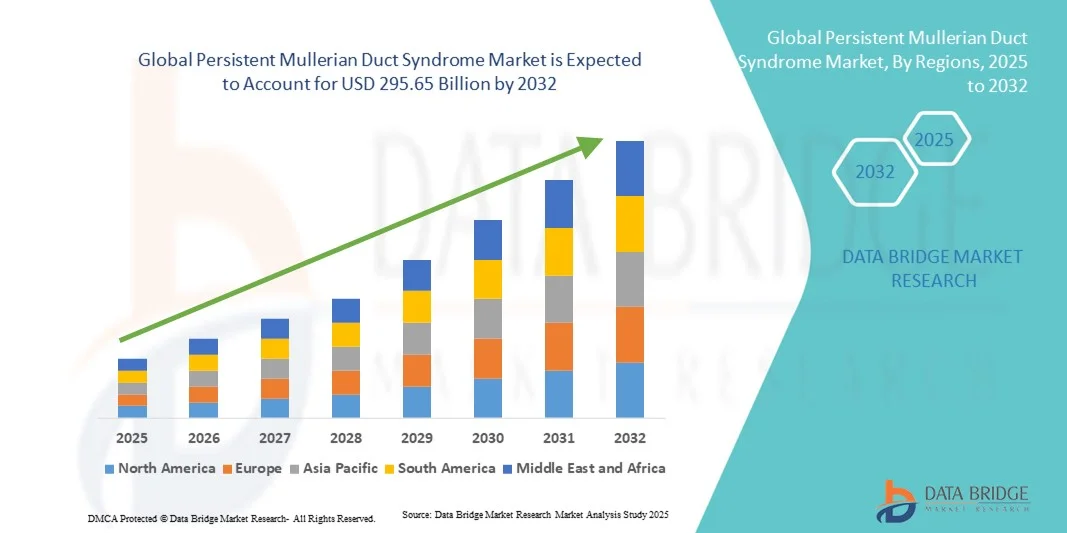

- The global persistent mullerian duct syndrome market size was valued at USD 185.5 billion in 2024 and is expected to reach USD 295.65 billion by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the increasing awareness and early diagnosis of rare genetic disorders, along with advancements in molecular genetics and diagnostic imaging, leading to improved identification and understanding of Persistent Mullerian Duct Syndrome (PMDS) cases

- Furthermore, rising research initiatives focused on gene therapy, hormonal regulation, and surgical management are establishing more effective and personalized treatment approaches for PMDS. These converging factors are accelerating the adoption of novel diagnostic and therapeutic solutions, thereby significantly boosting the industry’s growth

Persistent Mullerian Duct Syndrome Market Analysis

- Persistent Mullerian Duct Syndrome (PMDS), a rare genetic disorder characterized by the presence of Müllerian duct structures in genetically male individuals, is gaining increasing clinical and research attention due to advancements in genetic testing, surgical interventions, and reproductive medicine

- The escalating demand for improved diagnostic techniques, such as next-generation sequencing (NGS) and imaging-based evaluations, along with the rising prevalence of genetic counseling and rare disease awareness programs, are key factors driving the growth of the PMDS market

- North America dominated the persistent mullerian duct syndrome market with the largest revenue share of 41.66% in 2024, driven by robust healthcare infrastructure, advanced genomic research capabilities, and growing investment in rare disease management. The U.S. remains the key contributor to market expansion, supported by increased clinical studies and early diagnosis initiatives

- Asia-Pacific is expected to be the fastest-growing region in the persistent mullerian duct syndrome market during the forecast period, with a projected CAGR, due to expanding healthcare access, growing awareness of genetic disorders, and increasing government funding for rare disease treatment programs

- The Surgery segment dominated the market with the largest revenue share of 57.5% in 2024, as surgical procedures remain the cornerstone for treating PMDS

Report Scope and Persistent Mullerian Duct Syndrome Market Segmentation

|

Attributes |

Persistent Mullerian Duct Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Persistent Mullerian Duct Syndrome Market Trends

Advancements in Genetic Research and Precision Medicine

- A key and rapidly accelerating trend in the global persistent mullerian duct syndrome (PMDS) market is the growing focus on genetic and molecular research aimed at improving diagnosis, understanding disease mechanisms, and developing targeted treatment options. The increasing adoption of advanced genomic sequencing and molecular diagnostic tools is transforming PMDS detection and management

- For instance, next-generation sequencing (NGS) platforms are enabling early identification of mutations in the AMH and AMHR2 genes, which are responsible for the condition. This precision-based approach supports more accurate diagnosis and personalized patient management

- Academic and clinical research institutions are increasingly collaborating to map genetic variations across populations, improving insights into PMDS inheritance patterns and phenotypic diversity

- Moreover, the growing integration of bioinformatics and AI-driven analysis in genetic testing facilitates faster interpretation of genetic variants, allowing clinicians to make more informed treatment decisions

- Biotech companies and research organizations are also investing in novel gene-editing technologies, such as CRISPR-Cas9, to explore the potential of correcting genetic defects associated with PMDS. This shift toward precision medicine and molecular therapy is expected to reshape the long-term management and potential curative approaches for the disorder

- As awareness and accessibility of advanced diagnostics increase globally, especially in developing healthcare systems, the focus on early genetic screening and patient-specific interventions is anticipated to expand significantly, positioning PMDS research at the forefront of rare disease innovation

Persistent Mullerian Duct Syndrome Market Dynamics

Driver

Rising Awareness, Improved Diagnostics, and Growing Research Investments

- The global PMDS market is being strongly driven by growing awareness among healthcare professionals and patients, coupled with advancements in diagnostic technologies and genetic testing capabilities

- For instance, in March 2023, multiple academic studies emphasized the use of advanced imaging modalities such as MRI and laparoscopy in confirming the diagnosis of PMDS, helping clinicians differentiate the condition from other intersex disorders more effectively

- Government and private sector investments in rare disease research have also increased, supporting the identification and documentation of PMDS cases through national genetic disorder registries

- Organizations promoting genetic counseling and early diagnosis are expanding outreach programs, especially in countries with high rates of consanguineous marriages, where autosomal recessive disorders like PMDS are more prevalent

- Furthermore, ongoing collaborative studies between endocrinology and genetics departments across global medical institutions are driving the discovery of novel gene variants and their correlation with reproductive health outcome

- The increasing availability of specialized reproductive and urological care centers with access to genetic testing facilities is also enhancing early detection rates, leading to improved patient outcomes

- Collectively, these factors are accelerating clinical recognition, boosting diagnosis rates, and strengthening the market growth trajectory for PMDS

Restraint/Challenge

Limited Treatment Options and Diagnostic Challenges in Developing Regions

- Despite growing research efforts, the PMDS market continues to face challenges due to limited treatment options and insufficient diagnostic infrastructure, particularly in low- and middle-income countries

- The rarity of the condition often results in underdiagnosis or misdiagnosis, as clinical symptoms may overlap with other disorders of sexual development (DSDs). This diagnostic ambiguity hampers timely intervention and appropriate management

- In addition, the lack of specialized genetic laboratories and limited access to advanced molecular testing technologies pose significant obstacles to accurate detection in resource-constrained settings

- For instance, while developed countries have integrated genetic panels for DSDs into clinical practice, many regions still rely on basic karyotyping and hormonal testing, which may fail to identify subtle AMH or AMHR2 mutations

- High diagnostic costs, limited awareness among clinicians, and cultural stigmas surrounding genetic and reproductive disorders further restrict patient outreach and case reporting

- Furthermore, there are currently no approved curative therapies for PMDS, with treatment primarily focused on surgical management of retained Müllerian structures and fertility preservation strategies

- Overcoming these barriers will require increased international collaboration, investment in rare disease registries, and the development of low-cost, accessible genetic testing solutions. Enhancing awareness among healthcare professionals through continued education and cross-disciplinary training will also be crucial for early diagnosis and improved patient care outcomes

Persistent Mullerian Duct Syndrome Market Scope

The market is segmented on the basis of Symptoms, Diagnostic Test, Treatment, and End User.

- By Symptoms

On the basis of symptoms, the Persistent Mullerian Duct Syndrome market is segmented into Cryptorchidism, Inguinal Hernias, and Others. The Cryptorchidism segment dominated the market with the largest revenue share of 46.8% in 2024, driven by its high prevalence in PMDS patients. Cryptorchidism, or undescended testes, is the most frequent manifestation leading to diagnosis. The segment’s dominance is supported by increasing awareness among pediatricians, advancements in diagnostic imaging, and improved early screening in newborn males. Surgical correction like orchiopexy and long-term hormonal management further drive demand. Hospitals prioritize surgical treatment for these patients to prevent infertility and malignancy. Rising healthcare spending and growing prevalence of congenital anomalies also strengthen this segment’s revenue position.

The Inguinal Hernias segment is projected to register the fastest CAGR of 9.4% from 2025 to 2032, driven by higher recognition of hernias as a common secondary symptom in PMDS. The rise in laparoscopic hernia repair procedures and the growing use of advanced imaging for early identification enhance adoption. Increased surgical precision, shorter recovery time, and reduced hospital stay further accelerate growth. The growing collaboration between urology and pediatric surgery departments for dual management of hernias and Müllerian structures adds momentum. The segment benefits from technological innovations in minimally invasive procedures and increasing government support for congenital disorder management.

- By Diagnostic Test

On the basis of diagnostic test, the Persistent Mullerian Duct Syndrome market is segmented into Physical Examination, Imaging Test, and Genetic Testing. The Imaging Test segment dominated the market with the largest share of 51.2% in 2024, owing to its vital role in accurately detecting internal Müllerian structures. Advanced modalities such as MRI, CT scan, and ultrasound are increasingly used to confirm PMDS diagnosis. Hospitals rely heavily on imaging for pre-surgical planning and identifying associated anomalies. The availability of cost-effective imaging solutions and increased diagnostic accuracy contribute to its dominance. Rapid integration of AI-assisted image interpretation and improved reimbursement policies further boost segmental strength. Growing adoption of imaging tests in tertiary healthcare centers globally supports long-term market leadership.

The Genetic Testing segment is anticipated to record the fastest CAGR of 10.2% from 2025 to 2032, driven by the rising application of molecular diagnostics and genetic counseling. Identification of AMH and AMHR2 gene mutations provides precise diagnostic outcomes, reducing misdiagnosis. The increasing use of next-generation sequencing (NGS) and PCR-based testing promotes early and family-level detection. Growing research initiatives in reproductive genetics and affordable genetic test kits are enhancing accessibility. Hospitals are expanding their genetic testing capabilities to support precision treatment. Rising awareness about the hereditary nature of PMDS also drives faster adoption of genetic testing among at-risk families globally.

- By Treatment

On the basis of treatment, the Persistent Mullerian Duct Syndrome market is segmented into Surgery, Laparoscopy, and Others. The Surgery segment dominated the market with the largest revenue share of 57.5% in 2024, as surgical procedures remain the cornerstone for treating PMDS. Surgeries such as orchiectomy, hysterectomy, and hernia repair are frequently performed to address anatomical complications. The increasing prevalence of cryptorchidism and hernia cases enhances the need for operative management. Technological advancements in microsurgical tools and intraoperative imaging have improved success rates. Hospitals with dedicated pediatric surgery units drive higher patient inflow. Post-surgical follow-ups and long-term fertility management further contribute to revenue. The availability of trained surgeons and favorable reimbursement policies reinforce this segment’s leadership.

The Laparoscopy segment is estimated to grow at the fastest CAGR of 11.6% from 2025 to 2032, owing to its minimally invasive advantages. Laparoscopy allows simultaneous diagnosis and correction of Müllerian structures with smaller incisions and faster recovery. Surgeons prefer it for its high accuracy and reduced risk of postoperative complications. The rising adoption of 3D and robotic-assisted laparoscopic systems boosts efficiency and precision. Growing patient preference for minimally invasive surgery and reduced hospital stays supports strong market expansion. Training programs promoting advanced laparoscopic skills in developing countries also encourage widespread acceptance. Increased integration of imaging-guided techniques during laparoscopic interventions enhances procedural outcomes and drives robust segmental growth.

- By End User

On the basis of end user, the Persistent Mullerian Duct Syndrome market is segmented into Hospitals and Clinics, Ambulatory Surgical Centers, and Others. The Hospitals and Clinics segment dominated the market with the largest revenue share of 63.1% in 2024, attributed to the concentration of advanced diagnostic and surgical capabilities. Hospitals serve as referral centers for PMDS cases, offering multidisciplinary management involving endocrinology, genetics, and surgery. High patient admissions, infrastructure for imaging and testing, and government-funded treatment programs strengthen this dominance. Hospitals also facilitate early diagnosis through newborn screening and genetic counseling. Increasing hospital-based research in congenital reproductive disorders supports long-term market leadership. Collaboration between global pediatric and urology specialists further enhances treatment outcomes.

The Ambulatory Surgical Centers (ASCs) segment is projected to record the fastest CAGR of 10.9% from 2025 to 2032, due to the increasing shift toward outpatient and minimally invasive procedures. ASCs offer cost-effective surgeries, reduced wait times, and quicker patient recovery. Rising preference for same-day laparoscopic interventions supports strong adoption. Technological advancements enabling safe and efficient outpatient treatments further strengthen growth. Government incentives for reducing hospital burden by promoting ambulatory care also contribute. Surgeons favor ASCs for performing routine and low-risk PMDS-related procedures. The growing expansion of specialized pediatric ASCs and partnerships with hospital systems enhance accessibility and patient satisfaction.

Persistent Mullerian Duct Syndrome Market Regional Analysis

- North America dominated the persistent mullerian duct syndrome (PMDS) market with the largest revenue share of 41.66% in 2024, driven by robust healthcare infrastructure, advanced genomic research capabilities, and growing investments in rare disease management

- The region benefits from the presence of leading biotechnology and genetic testing companies, alongside strong clinical research networks dedicated to rare congenital disorders

- Increased awareness among healthcare providers and parents regarding early genetic screening for disorders of sexual development (DSDs) is further supporting market growth

U.S. Persistent Mullerian Duct Syndrome Market Insight

The U.S. persistent mullerian duct syndrome (PMDS) market captured the largest revenue share in 2024 within North America, supported by increasing adoption of advanced genetic testing and a growing focus on rare disease registries. The presence of key academic institutions such as the NIH and Mayo Clinic actively conducting clinical studies on intersex conditions, including PMDS, is accelerating diagnostic improvements. Government-funded genomics programs and public-private partnerships are also promoting early identification and research on AMH and AMHR2 gene mutations. Furthermore, favorable healthcare reimbursement policies and the availability of specialized centers for reproductive genetics and urology make the U.S. the leading contributor to regional market growth.

Europe Persistent Mullerian Duct Syndrome Market Insight

The Europe persistent mullerian duct syndrome (PMDS) market is projected to expand at a steady CAGR during the forecast period, primarily driven by strong healthcare frameworks, increasing focus on genetic research, and the presence of collaborative research networks across the EU. Growing government initiatives toward rare disease identification under programs such as EU4Health and Orphanet are strengthening diagnostic rates. Increased awareness among clinicians about disorders of sexual development and advancements in molecular diagnostics are fostering the adoption of genetic testing. In addition, supportive regulatory frameworks for orphan drugs and research funding through European rare disease consortia are enhancing the continent’s PMDS research capacity.

U.K. Persistent Mullerian Duct Syndrome Market Insight

The U.K. persistent mullerian duct syndrome (PMDS) market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by early adoption of genomic screening and government support for precision medicine initiatives. Institutions such as the National Health Service (NHS) and Genomics England are integrating rare disease diagnostics into clinical care, improving PMDS detection and reporting rates. Rising collaboration between academic centers and genetic laboratories, coupled with increased awareness through national rare disease strategies, is supporting sustainable market growth.

Germany Persistent Mullerian Duct Syndrome Market Insight

The Germany persistent mullerian duct syndrome (PMDS) market is expected to expand at a considerable CAGR, supported by the country’s strong biomedical research ecosystem and focus on advanced diagnostic infrastructure. Germany’s emphasis on innovation and clinical excellence has led to the establishment of multiple rare disease reference centers offering multidisciplinary diagnosis and treatment for PMDS and related conditions. In addition, public funding through the Federal Ministry of Education and Research (BMBF) for genetic and endocrine disorder studies enhances the nation’s role in advancing PMDS research.

Asia-Pacific Persistent Mullerian Duct Syndrome Market Insight

The Asia-Pacific persistent mullerian duct syndrome (PMDS) market region is expected to be the fastest-growing market for Persistent Mullerian Duct Syndrome during the forecast period, with a projected CAGR from 2025 to 2032, driven by improving healthcare access, growing awareness of genetic disorders, and increasing government funding for rare disease treatment programs.

Countries such as China, Japan, and India are witnessing rapid development in genetic testing infrastructure and higher adoption of molecular diagnostics. Rising investments in biotechnology research, coupled with awareness campaigns promoting early screening for congenital disorders, are further propelling regional market growth. The expansion of healthcare insurance coverage and cross-border collaborations in genomics are also creating favorable conditions for market development across Asia-Pacific.

Japan Persistent Mullerian Duct Syndrome Market Insight

The Japan persistent mullerian duct syndrome (PMDS) market is gaining momentum due to advancements in medical genetics, early implementation of population-based genetic screening, and a growing focus on personalized healthcare. Japan’s healthcare system emphasizes early diagnosis of hereditary and developmental disorders, supported by government initiatives under the Rare/Intractable Diseases Program (Nanbyo). The integration of advanced sequencing technologies and hospital-based genetic counseling services is improving detection accuracy and patient outcomes for PMDS.

China Persistent Mullerian Duct Syndrome Market Insight

The China persistent mullerian duct syndrome (PMDS) market accounted for the largest revenue share within Asia-Pacific in 2024, supported by an expanding middle-class population, increasing healthcare expenditure, and a surge in dermatological and genetic R&D initiatives. The country’s growing number of genomic laboratories, along with national strategies such as the Healthy China 2030 Plan, is promoting early diagnosis and research into rare genetic conditions. Increased domestic production of molecular diagnostic kits and collaborations with international genomics firms are strengthening China’s capacity in rare disease management and contributing significantly to regional market expansion.

Persistent Mullerian Duct Syndrome Market Share

The Persistent Mullerian Duct Syndrome industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sanofi S.A. (France)

- GSK plc (U.K.)

- AbbVie Inc. (U.S.)

- Bayer AG (Germany)

- Merck & Co., Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Takeda Pharmaceutical Company Limited (Japan)

- Boston Scientific Corporation (U.S.)

- Medtronic plc (Ireland)

- Sun Pharmaceutical Industries Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

Latest Developments in Global Persistent Mullerian Duct Syndrome Market

- In March 2022, a comprehensive case-and-literature report described several adult PMDS presentations discovered incidentally during inguinal hernia or cryptorchidism surgery and emphasized the need for molecular testing (AMH / AMHR2 sequencing) to confirm diagnosis and guide management

- In May 2022, a clinical review of diagnostic imaging and surgical management consolidated evidence showing that pelvic imaging (US/CT/MRI) plus genetic testing now forms the standard diagnostic pathway for suspected PMDS, improving pre-operative planning and reducing intraoperative surprises

- In September 2023, multiple published case reports and short series highlighted seminoma and other germ-cell tumor risks in some PMDS patients, renewing calls for long-term surveillance protocols in males with retained gonads and for individualized management plans

- In May 2024, groups publishing on DSD genetics reported broader adoption of targeted next-generation sequencing (NGS) panels / whole-exome approaches for 46,XY DSDs (including PMDS), demonstrating higher diagnostic yield and allowing identification of novel AMH / AMHR2 variants — leading to more precise genetic counselling and family testing

- In July 2024, a multinational case report series (peer-reviewed) described newly identified pathogenic AMH/AMHR2 variants in diverse populations, underlining that novel, population-specific mutations continue to be reported and that expanded genetic testing is uncovering previously unrecognized cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.