Global Pessary Market

Market Size in USD Million

USD

409.17 Million

USD

788.75 Million

2025

2033

USD

409.17 Million

USD

788.75 Million

2025

2033

| 2026 - 2033 | |

| USD 409.17 Million | |

| USD 788.75 Million | |

| % | |

|

Pessary Market Overview

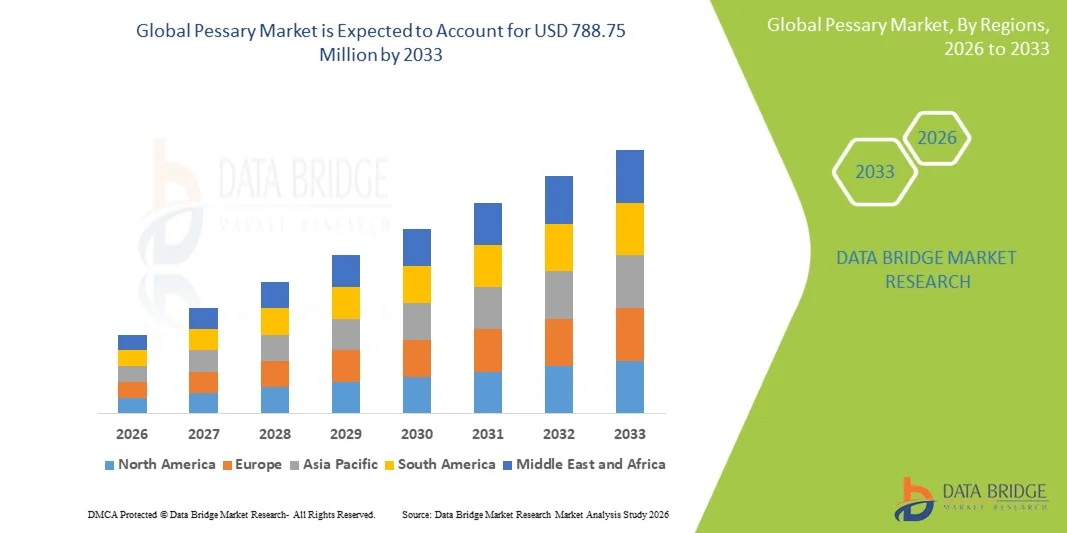

The Pessary Market was valued at USD 409.17 million in 2025 and is projected to reach USD 788.75 million by 2033, growing at a CAGR of 8.55% from 2026 to 2033. Market growth is supported by the rising prevalence of pelvic organ prolapse and stress urinary incontinence among the aging female population, alongside the growing preference for non-surgical treatment options.

The excellent efficacy rates connected to pessary therapy, combined with lower procedural risks and improved quality of life compared to surgical interventions, are driving increased adoption among both patients and healthcare providers. Ongoing advancements in pessary design and materials, including silicone-based devices with enhanced comfort, durability, and antimicrobial properties, are expanding the clinical applicability of pessaries across urogynecology and primary care settings. In addition, growing awareness of pelvic floor disorders, expanding women's health initiatives, and the increasing availability of pessary fitting services in ambulatory surgical centers and clinics are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Pessary Market with the largest revenue share of 38.6% in 2025, supported by high awareness of pelvic floor disorders, established urogynecology specialty care, and favorable reimbursement frameworks.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 10.45% from 2026 to 2033, driven by expanding healthcare infrastructure, rising geriatric female population, and increasing awareness of non-surgical treatment options.

- The Ring segment led the market with a 44.8% market share in 2025, reflecting its established position as the most commonly prescribed pessary type due to ease of insertion, patient comfort, and broad clinical applicability.

- The Donut segment is anticipated to be the fastest-growing type category, driven by increasing adoption for moderate to severe pelvic organ prolapse cases and technological advancements in device design.

- The Mild Pelvic Organ Prolapse segment dominated the products category with a 46.2% market share in 2025, supported by early diagnosis trends, growing awareness campaigns, and patient preference for conservative management.

- The Severe Pelvic Organ Prolapse segment is expected to witness strong growth during the forecast period, driven by aging population demographics and increasing referrals for non-surgical management in patients unfit for surgery.

- The Hospitals segment dominated the end-user category with a 52.4% market share in 2025, supported by access to specialized urogynecology services, comprehensive patient evaluation infrastructure, and multidisciplinary care teams.

- The Ambulatory Surgical Centers segment is expected to witness the fastest growth during the forecast period, driven by cost-effective service delivery, shorter patient wait times, and expanding outpatient pelvic floor disorder management programs.

Market Size & Forecast

- Global Market Value (2025): USD 409.17 Million

- Expected Market Value (2033): USD 788.75 Million

- Forecast CAGR (2026–2033): 8.55%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Pessary Market Segmentation

|

Attributes |

Pessary Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· CooperSurgical Inc. (U.S.) · Coloplast A/S (Denmark) · Integra LifeSciences Corporation (U.S.) · Thomas Medical (U.S.) · Panpac Medical Corp. (U.S.) · Personal Medical Corp. (U.S.) · Medgyn Products Inc. (U.S.) · Bioteque America Inc. (U.S.) · Arabin GmbH & Co. KG (Germany) · Gyneas (France) |

|

Market Opportunities |

· Expansion of pessary fitting services into primary care and community health settings with growing pelvic floor disorder awareness · Development of innovative pessary designs with enhanced biocompatibility, antimicrobial coatings, and patient self-management capabilities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pessary Market Trends

Trend: Technological Advancements Enhancing Patient Comfort and Self-Management

Clinical adoption of pessary devices continues to accelerate as technological innovations improve patient comfort, device durability, and ease of use. Advanced silicone-based pessaries with antimicrobial properties, softer materials, and ergonomic designs enable patients to experience reduced irritation and improved long-term compliance. Self-insertion pessaries and patient-friendly designs are empowering women to manage their pelvic floor conditions independently, reducing healthcare visit frequency and improving quality of life.

For instance,

The introduction of the Uresta self-positioning bladder support device has gained significant market traction due to its patient-controlled design, eliminating the need for professional fitting and enabling women to manage stress urinary incontinence independently at home.

In addition, research demonstrates that modern silicone pessaries have significantly lower rates of vaginal erosion and discharge compared to older rubber-based devices, supporting broader clinical adoption and improved patient satisfaction across urogynecology practices. These technological advancements are expected to strengthen market growth by improving patient adherence and expanding the eligible patient population for pessary therapy.

Pessary Market Dynamics

Key Market Driver: Rising Prevalence of Pelvic Floor Disorders Among Aging Female Population

The growing prevalence of pelvic organ prolapse and stress urinary incontinence among aging women is a primary driver of market growth. Pessary devices offer an effective, non-surgical treatment option for managing these conditions, particularly for elderly patients who may be poor candidates for surgical intervention due to comorbidities or patient preference. The increasing life expectancy of the global female population is expanding the patient pool requiring pelvic floor disorder management.

For instance,

According to epidemiological studies, approximately 50% of parous women experience some degree of pelvic organ prolapse, with prevalence increasing significantly after menopause and reaching peak incidence among women aged 70 to 79 years. The growing geriatric female population globally is expected to strengthen adoption of pessary devices as a first-line conservative treatment option.

Key Restraint/Challenge: Limited Patient Awareness and Access to Specialized Fitting Services

The lack of patient awareness regarding pessary therapy as a viable treatment option for pelvic floor disorders, combined with limited access to specialized urogynecology services in underserved regions, presents a significant barrier to market expansion. Many women remain unaware that non-surgical options exist, and healthcare providers in primary care settings may lack training in pessary fitting and management.

For instance,

Studies indicate that fewer than 20% of women with symptomatic pelvic organ prolapse are offered pessary therapy as a first-line treatment option, with surgical intervention often being recommended without adequate counseling on conservative alternatives. Limited awareness and provider training may constrain market growth, particularly in emerging markets with developing urogynecology infrastructure.

Key Market Opportunity: Expansion of Pessary Services into Primary Care and Community Health Settings

The development of simplified pessary designs suitable for primary care fitting, combined with expanding training programs for general practitioners and nurse practitioners, is creating opportunities for adoption beyond traditional urogynecology specialty settings. Community health centers and primary care practices are increasingly incorporating pessary fitting services, improving access for women in rural and underserved areas.

For instance,

The American College of Obstetricians and Gynecologists has published updated guidelines encouraging primary care providers to offer pessary therapy as a first-line treatment for pelvic organ prolapse, expanding the clinical settings where patients can access non-surgical management options. The expansion of pessary services into primary care settings is expected to significantly broaden market reach and improve patient access to conservative treatment options.

Pessary Market Scope

The pessary market is segmented on the basis of type, products, and end-use.

By Type

On the basis of type, the Pessary Market is segmented into Gellhorn, Ring, Donut, and Others. The Ring segment dominated the market with a 44.8% market share in 2025, reflecting its established position as the most commonly prescribed pessary type. Ring pessaries are widely preferred due to their ease of insertion and removal, patient comfort, and broad clinical applicability across mild to moderate pelvic organ prolapse and stress urinary incontinence cases. The simple design enables patient self-management, reducing healthcare visit frequency and improving treatment adherence.

The Donut segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing adoption for moderate to severe pelvic organ prolapse cases and technological advancements in device design. Donut pessaries offer excellent support for posterior vaginal wall defects and are increasingly prescribed for patients who have not achieved adequate symptom relief with ring pessaries.

By Products

On the basis of products, the Pessary Market is segmented into mild pelvic organ prolapse, stress urinary incontinence, and severe pelvic organ prolapse. The mild pelvic organ prolapse segment dominated the market with a 46.2% market share in 2025, supported by early diagnosis trends, growing awareness campaigns, and patient preference for conservative management before considering surgical options. Pessary therapy is increasingly recommended as first-line treatment for stage I and stage II pelvic organ prolapse, enabling symptom relief without surgical intervention.

The Severe Pelvic Organ Prolapse segment is expected to witness strong growth during the forecast period, driven by aging population demographics and increasing referrals for non-surgical management in patients unfit for surgery due to advanced age, comorbidities, or patient preference. Gellhorn, cube, and donut pessaries are commonly prescribed for stage III and stage IV pelvic organ prolapse cases requiring robust mechanical support.

By End-use

On the basis of end-use, the Pessary Market is segmented into hospitals, ambulatory surgical centers, and clinics. The hospitals segment dominated the market with a market share of 52.4% in 2025, driven by access to specialized urogynecology services, comprehensive patient evaluation infrastructure, and multidisciplinary care teams. Hospitals serve as primary centers for initial pessary fitting, particularly for complex cases requiring thorough pelvic examination, imaging studies, and specialist consultation.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth from 2026 to 2033, driven by cost-effective service delivery, shorter patient wait times, and expanding outpatient pelvic floor disorder management programs. Ambulatory surgical centers are increasingly incorporating pessary fitting services as part of comprehensive women's health programs, improving patient access and reducing healthcare costs.

Pessary Market Regional Analysis

North America dominated the pessary market with a revenue share of 38.6% in 2025, supported by high awareness of pelvic floor disorders, established urogynecology specialty care, and favorable reimbursement frameworks. Strong clinical practice guidelines, comprehensive provider training programs, and extensive patient education initiatives contribute to regional market leadership.

U.S. Pessary Market Insight

The U.S. pessary market benefits from the highest awareness levels of pelvic floor disorders globally, extensive urogynecology specialty services, and strong professional society guidelines supporting pessary therapy as first-line treatment. Academic medical centers, urogynecology practices, and women's health clinics continue to expand pessary fitting programs across urban and rural settings. Favorable Medicare and commercial payer reimbursement supports patient access and provider adoption. The U.S. held a dominant market share of 78.4% within North America in 2025, reflecting its leadership position in the regional market.

Europe Pessary Market Insight

The Europe pessary market remains a major contributor, with strong urogynecology services across Germany, the U.K., France, and the Netherlands. Growing adoption of modern silicone pessaries, expanding primary care training programs, and favorable national health service coverage are improving patient access to pessary therapy. Cross-disciplinary guidelines and structured care pathways are standardizing treatment approaches and improving clinical outcomes.

U.K. Pessary Market Insight

The U.K. pessary market is characterized by expanding pessary fitting services within NHS hospitals, community clinics, and general practitioner practices. Investment in pelvic floor disorder awareness campaigns and provider training is improving access to conservative treatment options and reducing surgical waiting lists. The U.K. is expected to grow at a CAGR of 8.95% from 2026 to 2033, driven by expanding NHS pelvic floor disorder services.

Germany Pessary Market Insight

Germany's robust healthcare infrastructure and established urogynecology specialty services support comprehensive pessary fitting programs across hospitals and private practices. Strong clinical training networks and favorable statutory health insurance coverage contribute to high patient access and treatment adherence.

Asia-Pacific Pessary Market Insight

The Asia-Pacific pessary market is poised for rapid growth with a CAGR of 10.45% during the forecast period, driven by expanding healthcare infrastructure, rising geriatric female population, and increasing awareness of non-surgical treatment options. Private healthcare systems and women's health clinics in China, Japan, India, and Australia are investing in urogynecology capabilities to meet growing patient demand for pelvic floor disorder management.

Japan Pessary Market Insight

The Japan pessary market benefits from advanced healthcare infrastructure, strong obstetrics and gynecology services, and increasing awareness of pelvic floor disorders among aging women. Pessary therapy is increasingly recommended as first-line treatment, with expanding provider training programs improving access to fitting services. Japan held the largest market share of 26.8% within Asia-Pacific in 2025.

China Pessary Market Insight

The China pessary market is experiencing rapid growth driven by healthcare modernization initiatives, expanding women's health programs, and increasing patient demand for non-surgical treatment options. Growing awareness of pelvic floor disorders through public health campaigns and expanding urogynecology services in tertiary hospitals are driving market expansion. China is expected to be the fastest-growing country within Asia-Pacific at a CAGR of 11.85% from 2026 to 2033.

Pessary Market Share

The pessary industry is primarily led by well-established companies, including:

- CooperSurgical Inc. (U.S.)

- Coloplast A/S (Denmark)

- Integra LifeSciences Corporation (U.S.)

- Thomas Medical (U.S.)

- Panpac Medical Corp. (U.S.)

- Personal Medical Corp. (U.S.)

- Medgyn Products Inc. (U.S.)

- Bioteque America Inc. (U.S.)

- Arabin GmbH & Co. KG (Germany)

- Gyneas (France)

Latest Developments in Pessary Market

- In February 2026, CooperSurgical Inc. announced the expansion of its Milex pessary portfolio with the introduction of new sizing options for ring and Gellhorn pessaries, designed to improve patient fit and comfort across a broader range of anatomies. The expanded product line supports the company's commitment to providing comprehensive pelvic floor disorder management solutions.

- In November 2025, Coloplast A/S launched its next-generation silicone pessary line featuring enhanced antimicrobial properties and improved surface smoothness, designed to reduce vaginal irritation and improve long-term patient compliance. The launch underscores Coloplast's focus on advancing patient comfort in conservative pelvic floor disorder treatment.

- In August 2025, Integra LifeSciences Corporation announced a strategic partnership with leading urogynecology training centers across North America to expand provider education programs for pessary fitting and management. The initiative aims to increase primary care provider competency and improve patient access to pessary therapy.

- In May 2025, Bioteque America Inc. received FDA 510(k) clearance for its new self-positioning bladder support pessary designed for patient self-management of stress urinary incontinence. The device enables women to independently insert and remove the pessary, reducing healthcare visit frequency and improving treatment adherence.

- In January 2025, Thomas Medical announced the expansion of its pessary manufacturing capacity at its U.S. production facility to meet growing global demand for silicone pessary devices. The expansion supports the company's strategy to strengthen its market position in the pelvic floor disorder management segment.

- In September 2024, Arabin GmbH & Co. KG introduced its updated pessary product line featuring new designs for cervical support during pregnancy, expanding the company's portfolio beyond traditional pelvic organ prolapse indications.

- In June 2024, CooperSurgical Inc. announced the acquisition of a leading pelvic floor health education platform, strengthening its patient and provider education capabilities and supporting broader adoption of pessary therapy as first-line treatment.

- In March 2024, Personal Medical Corp. launched its educational video series for healthcare providers on pessary fitting techniques, available through its online training portal. The initiative aims to expand provider competency and improve patient outcomes in pessary therapy.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.