Global Pet Ct Scanners Market

Market Size in USD Billion

USD

2.60 Billion

USD

4.40 Billion

2025

2033

USD

2.60 Billion

USD

4.40 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.60 Billion | |

| USD 4.40 Billion | |

| % | |

|

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Overview

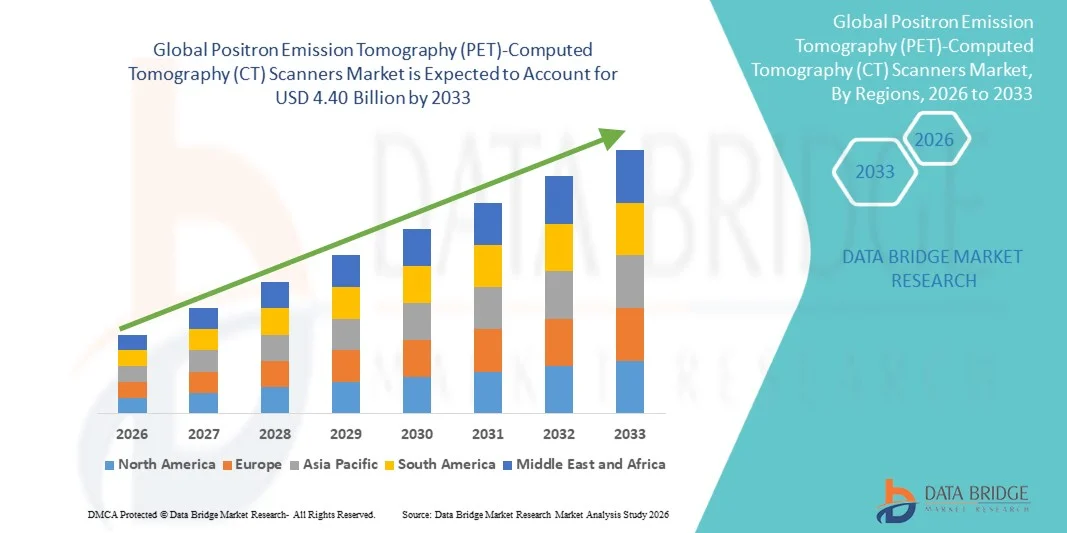

As per Data Bridge Market Research analysis the Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market was valued at USD 2.60 billion in 2025 and is projected to reach USD 4.40 billion by 2033, growing at a CAGR of 6.80% from 2026 to 2033. The market is witnessing steady expansion driven by rising prevalence of cancer and cardiovascular diseases, increasing demand for advanced hybrid imaging modalities, and continuous technological advancements in nuclear medicine imaging systems. Growing emphasis on early and precise disease diagnosis, along with expanding applications in oncology, neurology, and cardiology, is further supporting market growth.

The increasing adoption of PET-CT systems in hospitals, diagnostic imaging centers, and research institutions is being fueled by the growing burden of chronic diseases and the need for highly accurate functional and anatomical imaging in a single scan. In addition, integration of artificial intelligence for image reconstruction and analysis, development of digital PET detectors, and improving reimbursement frameworks in developed markets are accelerating adoption. However, high equipment and operational costs remain a key challenge, particularly in emerging economies, despite rising investments in healthcare infrastructure and expanding access to advanced diagnostic technologies.

Key Market Trends & Insights

- North America dominated the Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market with the largest revenue share of 36.28% in 2025, supported by strong healthcare infrastructure, high adoption of advanced imaging technologies, and favorable reimbursement policies.

- The Lutetium Oxyorthosilicate segment led the market with a 42.6% share in 2025, driven by its strong scintillation efficiency, high light yield, and faster decay time compared to conventional crystal materials.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by expanding healthcare infrastructure, growing cancer burden, and increasing investments in nuclear medicine and diagnostic imaging centers in China, India, and Japan.

- Gadolinium Oxyorthosilicate are the fastest-growing detector type, projected to register a CAGR of 7.2%, reflecting the surge in improved energy resolution and stable performance in specific clinical imaging environments.

- The Full Ring PET Scanner segment dominated the product type category with a 63.5% revenue share in 2025, led by its superior detector coverage, high sensitivity, and ability to deliver uniform and high-resolution imaging.

- High Slice Scanner accounted for 51.2% of the market, preferred by its superior image resolution, faster scanning speed, and enhanced ability to detect small lesions.

- The Portable segment is the fastest-growing setting category, with a CAGR of 7.1%, driven by the increasing demand for flexible and point-of-care diagnostic imaging solutions.

Market Size & Forecast

- Global Market Value (2025): USD 2.60 Billion

- Expected Market Value (2033): USD 4.40 Billion

- Forecast CAGR (2026–2033): 6.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Segmentation

|

Attributes |

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· GE HealthCare (U.S.) · Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · United Imaging Healthcare Co., Ltd. (China) · Shimadzu Corporation (Japan) · FUJIFILM Healthcare Corporation (Japan) · Mediso Ltd. (Hungary) · Neusoft Medical Systems Co., Ltd. (China) · Positron Corporation (U.S.) · Spectrum Dynamics Medical (Israel) · MR Solutions Ltd. (U.K.) · Time Medical Systems (Hong Kong) · SurgicEye GmbH (Germany) · Bruker Corporation (U.S.) · Hitachi Medical Systems (Japan) · Carestream Health (U.S.) · Digirad Corporation (U.S.) · Eckert & Ziegler Radiopharma GmbH (Germany) |

|

Market Opportunities |

· Expansion of PET-CT adoption in emerging economies · Growing integration of PET-CT systems with AI-powered diagnostic platforms · Rising demand for theranostics applications, combining PET-CT imaging with targeted radiopharmaceutical therapies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Trends

Trend: Expansion of AI-Enhanced Image Reconstruction and Digital PET Systems

Healthcare providers across developed and emerging markets are increasingly transitioning toward AI-integrated PET-CT platforms to significantly enhance diagnostic precision and workflow efficiency. These systems leverage deep learning algorithms to improve image reconstruction quality, reduce noise levels, and shorten scan acquisition times, which is particularly critical in high-patient-load hospitals. The ongoing shift from conventional photomultiplier-based PET systems to digital detector technology (digital PET) is further improving spatial resolution and sensitivity, enabling earlier detection of small lesions and subtle metabolic changes. In addition, hybrid imaging ecosystems are evolving into fully integrated diagnostic platforms where PET and CT data are automatically fused, allowing radiologists to interpret anatomical and functional information simultaneously with greater accuracy.

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Dynamics

Key Market Driver: Rising Burden of Cancer and Demand for Early Diagnostic Imaging

The global increase in cancer incidence, along with rising cases of neurological and cardiovascular disorders, is one of the strongest drivers of PET-CT adoption worldwide. PET-CT scanners play a critical role in early-stage cancer detection, tumor staging, metastasis evaluation, and treatment response monitoring, making them indispensable in modern oncology workflows. As healthcare systems shift toward value-based care, early and accurate diagnosis is becoming a priority to reduce long-term treatment costs and improve survival outcomes. Moreover, governments and healthcare organizations are expanding national cancer screening programs, while awareness among clinicians regarding molecular imaging benefits continues to grow. Improvements in healthcare infrastructure, especially in Asia-Pacific and Latin America, are also increasing accessibility to advanced diagnostic imaging. For instance, large tertiary care hospitals are increasingly incorporating PET-CT systems into standard oncology protocols for lung, breast, and colorectal cancer management to improve diagnostic accuracy and treatment planning efficiency.

Key Restraint/Challenge: High Cost and Limited Accessibility of PET-CT Infrastructure

Despite strong clinical demand, the PET-CT scanners market faces significant barriers due to the high capital investment required for equipment procurement, installation, and maintenance. These systems also require specialized infrastructure such as radiation-shielded imaging rooms, cyclotron access for radiotracer production, and highly trained nuclear medicine professionals, all of which substantially increase operational complexity and cost. In addition, regulatory constraints surrounding radioactive materials and radiopharmaceutical handling further limit deployment, especially in low- and middle-income countries. Reimbursement challenges in several regions also restrict widespread adoption, as insurance coverage for PET-CT scans is not uniformly available or fully adequate. For instance, many smaller diagnostic centers in emerging economies continue to rely on CT or MRI alone due to the prohibitive cost of PET-CT systems and the lack of supporting nuclear medicine infrastructure required for routine operations.

Key Market Opportunity: Expansion of Theranostics and Personalized Nuclear Medicine Applications

The major growth opportunity in the PET-CT scanners market lies in the rapid expansion of theranostics, which combines diagnostic imaging with targeted radiopharmaceutical therapy for personalized disease management. PET-CT imaging enables precise identification of molecular targets, allowing clinicians to tailor treatment strategies based on individual tumor biology, significantly improving therapeutic outcomes. Advancements in radiotracer development, particularly in oncology, are expanding the use of PET-CT beyond diagnosis into real-time treatment monitoring and therapy guidance. The increasing adoption of precision medicine is further strengthening demand for imaging modalities that provide both functional and molecular insights. For instance, PET-CT guided radioligand therapies in prostate cancer are increasingly being used to not only detect metastatic disease but also monitor treatment response and adjust therapeutic dosing for improved patient-specific outcomes.

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Scope

The Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is segmented on the basis of detector type, product type, slice count, setting, application, and end user.

- By Detector Type

On the basis of detector type, the global PET-CT scanners market is segmented into Bismuth Germanium Oxide (BGO), Lutetium Oxyorthosilicate (LSO), Gadolinium Oxyorthosilicate (GSO), Lutetium Fine Silicate (LFS), and Lutetium Yttrium Orthosilicate (LYSO). The LSO segment dominated the market with a 42.6% share in 2025, owing to its strong scintillation efficiency, high light yield, and faster decay time compared to conventional crystal materials. These characteristics enable superior spatial resolution and faster imaging workflows, which are critical in oncology and neurology diagnostics. LSO-based systems are widely deployed in hospital PET-CT installations due to their proven clinical reliability and compatibility with time-of-flight imaging. The segment also benefits from established manufacturing maturity and widespread regulatory approvals. Continuous improvements in digital PET integration further strengthen its market leadership.

The GSO segment is the fastest growing, expected to register a CAGR of 7.2% from 2026 to 2033, driven by its improved energy resolution and stable performance in specific clinical imaging environments. GSO crystals offer lower afterglow and better image uniformity in certain neurological and cardiac imaging applications. Increasing adoption in specialized diagnostic centers and research institutions is accelerating demand. The segment is gaining traction in cost-sensitive regions where balanced performance and affordability are important. Expanding use in hybrid imaging research and prototype PET systems is further supporting growth. For instance, several academic research hospitals are increasingly using GSO-based PET-CT systems for advanced neuroimaging studies and tracer development research.

- By Product Type

On the basis of product type, the market is segmented into Full Ring PET Scanner and Partial Ring PET Scanner. The Full Ring PET Scanner segment dominated the market with a 63.5% share in 2025, due to its superior detector coverage, high sensitivity, and ability to deliver uniform and high-resolution imaging. These systems provide faster acquisition times and better signal-to-noise ratio, making them highly suitable for oncology, neurology, and advanced clinical research. Full ring systems are widely used in tertiary hospitals and diagnostic centers handling high patient volumes. Integration with CT and AI-based reconstruction further improves diagnostic precision. Their capability to support dynamic imaging studies strengthens clinical adoption across complex disease evaluations.

The Partial Ring PET Scanner segment is the fastest growing, projected to register a CAGR of 6.8% from 2026 to 2033, driven by lower cost, easier installation, and growing demand in emerging healthcare markets. These systems are increasingly adopted in mid-sized diagnostic centers and developing regions where full ring systems may be financially restrictive. Technological improvements are enhancing image reconstruction quality even in partial coverage systems. Expanding use in mobile imaging units and outpatient diagnostic setups is further supporting growth. For instance, several regional diagnostic clinics are adopting partial ring PET-CT systems to expand access to nuclear imaging services at lower capital investment levels.

- By Slice Count

On the basis of slice count, the market is segmented into Low Slice Scanner, Medium Slice Scanner, and High Slice Scanner. The High Slice Scanner segment dominated the market with a 51.2% share in 2025, driven by its superior image resolution, faster scanning speed, and enhanced ability to detect small lesions. These systems are widely used in oncology and cardiology for detailed anatomical and functional imaging. High slice scanners significantly reduce scan time while improving diagnostic accuracy. Integration with AI-based reconstruction tools further enhances imaging efficiency and reduces radiation exposure. Strong adoption in advanced hospitals supports segment dominance.

The Medium Slice Scanner segment is the fastest growing, expected to register a CAGR of 7.3% from 2026 to 2033, driven by its balanced performance, affordability, and suitability for mid-tier healthcare facilities. These systems provide adequate image quality for routine oncology and neurology applications without the high cost of advanced high-slice systems. Increasing demand from emerging economies and regional hospitals is boosting adoption. Continuous improvements in detector efficiency are narrowing the performance gap with high slice systems. For instance, several secondary care hospitals are upgrading to medium slice PET-CT scanners to expand diagnostic capabilities while maintaining cost efficiency.

- By Setting

On the basis of setting, the market is segmented into Fixed and Portable PET-CT systems. The Fixed segment dominated the market with a 92.4% share in 2025, as PET-CT imaging requires controlled environments, radiation shielding, and integrated radiotracer handling systems. Fixed installations are widely used in hospitals, diagnostic centers, and research institutions with high patient volumes. These systems provide stable imaging performance, high accuracy, and seamless workflow integration. They are essential for oncology departments where continuous imaging demand exists. Strong infrastructure investment in nuclear medicine further reinforces dominance.

The Portable segment is the fastest growing, projected to register a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for flexible and point-of-care diagnostic imaging solutions. Portable systems are gaining traction in emergency care, remote healthcare facilities, and mobile diagnostic units. Advancements in compact detector technology and shielding systems are improving feasibility. Growing need for decentralized healthcare delivery is further accelerating adoption. For instance, mobile diagnostic initiatives in rural healthcare programs are increasingly using portable PET-CT solutions for early cancer screening and outreach diagnostics.

- By Application

On the basis of application, the market is segmented into Cardiology, Neurology, Oncology, and Others. The Oncology segment dominated the market with a 48.9% share in 2025, driven by the high global burden of cancer and the critical role of PET-CT in tumor detection, staging, and therapy monitoring. PET-CT enables precise metabolic and anatomical imaging, making it essential for cancer diagnosis and treatment planning. Increasing adoption of personalized oncology approaches is further strengthening demand. Hospitals and cancer centers rely heavily on PET-CT for clinical decision-making.

The Neurology segment is the fastest growing, projected to register a CAGR of 7.5% from 2026 to 2033, driven by rising prevalence of Alzheimer’s disease, epilepsy, and other neurodegenerative disorders. PET-CT is increasingly used for early brain function assessment and neurological disorder diagnosis. Growing awareness of early detection benefits is boosting demand for advanced neuroimaging. Technological advancements are improving brain imaging resolution and tracer specificity. For instance, PET-CT is increasingly used in dementia research centers to identify early biomarkers of Alzheimer’s disease progression.

- By End User

On the basis of end user, the market is segmented into Hospitals, Diagnostic Centers, and Research Institutes. The Hospitals segment dominated the market with a 52.7% share in 2025, due to high patient inflow, advanced imaging infrastructure, and integration of PET-CT systems into oncology and neurology departments. Hospitals serve as primary centers for complex diagnostic procedures and multidisciplinary cancer care. Strong reimbursement support and infrastructure investment further strengthen dominance.

The Diagnostic Centers segment is the fastest growing, projected to register a CAGR of 7.2% from 2026 to 2033, driven by rising demand for outpatient imaging services and rapid expansion of standalone diagnostic chains. These centers offer faster access, lower costs, and reduced hospital dependency. Increasing outsourcing of imaging services from hospitals is supporting growth. Technological advancements are enabling compact and efficient PET-CT installations in diagnostic labs. For instance, independent diagnostic chains are increasingly installing PET-CT systems to expand oncology imaging services and improve patient accessibility in urban and semi-urban regions.

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Regional Analysis

North America dominated the Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market with the largest revenue share of 36.28% in 2025, supported by strong healthcare infrastructure, high adoption of advanced imaging technologies, and favorable reimbursement policies. The region also benefits from favorable reimbursement frameworks, high cancer prevalence, and widespread integration of PET-CT systems in oncology and cardiology diagnostics. Increasing use of digital PET systems, AI-based image reconstruction, and theranostic applications continues to strengthen North America’s leadership position in the global market.

U.S. Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The United States Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is witnessing strong growth due to rising cancer prevalence, advanced healthcare infrastructure, and high adoption of digital imaging technologies. The country’s well-established hospital network, strong reimbursement policies, and presence of leading medical imaging companies are driving demand across oncology, cardiology, and neurology applications. Increasing integration of AI-powered diagnostics, radiopharmaceutical innovations, and theranostic approaches is further accelerating PET-CT adoption across clinical and research settings. In addition, growing focus on early disease detection and precision medicine is strengthening market expansion across hospitals and diagnostic centers.

Europe Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The Europe Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market remains a key contributor to global revenue, driven by strong healthcare systems, government-supported cancer screening programs, and high adoption of advanced diagnostic imaging technologies. The widespread use of PET-CT systems in oncology and neurology diagnostics is supporting regional market expansion. Increasing investments in digital PET systems, hybrid imaging platforms, and nuclear medicine infrastructure are further enhancing adoption. In addition, strict clinical standards, growing emphasis on early diagnosis, and rising demand for precision imaging continue to strengthen Europe’s position in the global PET-CT scanners market.

United Kingdom Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The United Kingdom Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is experiencing steady growth, supported by expanding cancer diagnostic programs, strong NHS infrastructure, and increasing adoption of advanced imaging modalities. Rising demand for early cancer detection and improved treatment monitoring is driving PET-CT utilization across major hospitals. Integration of AI-based imaging analysis, digital PET systems, and radiopharmaceutical advancements is further improving diagnostic efficiency. Moreover, growing investments in nuclear medicine facilities and research collaborations are positioning the United Kingdom as an important innovation hub in the PET-CT imaging landscape.

Germany Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The Germany Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is expanding steadily due to strong healthcare infrastructure, advanced medical research capabilities, and high adoption of precision imaging technologies. Hospitals and diagnostic centers are increasingly using PET-CT systems for oncology, cardiology, and neurology applications. Continuous advancements in digital PET technology, hybrid imaging systems, and AI-enabled diagnostics are further driving market growth. In addition, Germany’s strong focus on medical innovation, cancer research, and nuclear medicine development is supporting widespread adoption of advanced PET-CT scanners across clinical environments.

Asia-Pacific Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The Asia-Pacific Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is expected to witness rapid growth, driven by rising cancer burden, expanding healthcare infrastructure, and increasing investments in advanced diagnostic imaging. Growing adoption of digital PET systems and hybrid imaging technologies across China, India, and Japan is significantly boosting market demand. Increasing awareness of early disease detection, improving reimbursement scenarios, and expansion of tertiary care hospitals are further supporting regional growth. In addition, rising government initiatives in cancer screening and nuclear medicine development are accelerating PET-CT adoption across clinical settings.

Japan Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The Japan Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is witnessing consistent growth due to advanced healthcare infrastructure, strong focus on early disease detection, and high adoption of nuclear medicine technologies. The country’s aging population and rising prevalence of cancer are key factors driving demand for PET-CT imaging. Continuous innovation in digital PET systems, AI-based diagnostics, and radiotracer development is further enhancing imaging accuracy. Moreover, Japan’s strong research ecosystem and integration of precision medicine approaches are supporting sustained market expansion in clinical and academic settings.

China Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Insight

The China Positron Emission Tomography (PET)-Computed Tomography (CT) scanners market is growing rapidly, driven by increasing cancer incidence, expanding healthcare infrastructure, and strong government support for advanced medical imaging technologies. Rising investments in hospital modernization, nuclear medicine facilities, and radiopharmaceutical production are significantly boosting PET-CT adoption. The growing presence of domestic manufacturing capabilities and increasing accessibility of digital PET systems are further supporting market expansion. In addition, rising awareness of early cancer detection and rapid technological advancements are positioning China as one of the fastest-growing PET-CT markets globally.

Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market Share

The Positron Emission Tomography (PET)-Computed Tomography (CT) scanners industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- United Imaging Healthcare Co., Ltd. (China)

- Shimadzu Corporation (Japan)

- FUJIFILM Healthcare Corporation (Japan)

- Mediso Ltd. (Hungary)

- Neusoft Medical Systems Co., Ltd. (China)

- Positron Corporation (U.S.)

- Spectrum Dynamics Medical (Israel)

- MR Solutions Ltd. (U.K.)

- Time Medical Systems (Hong Kong)

- SurgicEye GmbH (Germany)

- Bruker Corporation (U.S.)

- Hitachi Medical Systems (Japan)

- Carestream Health (U.S.)

- Digirad Corporation (U.S.)

- Eckert & Ziegler Radiopharma GmbH (Germany)

Latest Developments in Positron Emission Tomography (PET)-Computed Tomography (CT) Scanners Market

- In February 2024, Canon Medical Systems, a leading manufacturer of diagnostic imaging equipment, announced advancements in its PET/CT imaging portfolio with enhanced AI-driven reconstruction and workflow optimization technologies. These improvements are aimed at improving image clarity, reducing scan noise, and increasing diagnostic confidence in complex cases. The updates support faster clinical decision-making in oncology and neurology applications. This development reflects the increasing integration of AI in hybrid nuclear imaging systems

- In March 2023, GE HealthCare, a leading provider of medical imaging and diagnostics solutions, announced the launch of its Omni Legend PET/CT system designed to enhance digital PET imaging performance in clinical environments. The system integrates advanced digital detector technology and AI-powered image reconstruction to improve lesion detectability, reduce scan times, and lower radiation dose for patients. It is particularly focused on oncology applications, enabling more precise tumor detection and treatment monitoring. The launch strengthens GE HealthCare’s position in next-generation molecular imaging and precision diagnostics

- In September 2022, United Imaging Healthcare, a global medical imaging company, expanded the clinical adoption of its uEXPLORER total-body PET/CT system across leading hospitals and research institutions. The system offers an ultra-long axial field of view, enabling ultra-low-dose and high-speed whole-body imaging. It significantly enhances imaging sensitivity for oncology, cardiovascular, and pediatric diagnostics. The development highlights growing global acceptance of total-body PET technology in advanced clinical practice

- In November 2021, Koninklijke Philips N.V., a global health technology company, introduced enhancements to its PET/CT imaging ecosystem focused on AI-enabled reconstruction and advanced analytics integration. The upgrades are designed to improve diagnostic accuracy, optimize scanning workflows, and reduce examination time in clinical settings. It also supports better imaging consistency across oncology and cardiology applications. This advancement reinforces Philips’ strategy toward intelligent and connected diagnostic imaging solutions

- In May 2021, Siemens Healthineers, a global leader in medical technology, introduced the Biograph Vision Quadra total-body PET/CT system to advance ultra-high sensitivity imaging capabilities. The system enables full-body dynamic imaging in a single scan, significantly improving tracer distribution analysis and diagnostic accuracy. It is designed for advanced research applications, including oncology, cardiology, and drug development studies. This innovation marked a major milestone in expanding total-body PET imaging technology for precision medicine

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.