Global Pfas Free Foodservice Packaging Market

Market Size in USD Billion

USD

11.40 Billion

USD

21.75 Billion

2025

2033

USD

11.40 Billion

USD

21.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.40 Billion | |

| USD 21.75 Billion | |

| % | |

|

PFAS-Free Foodservice Packaging Market Overview

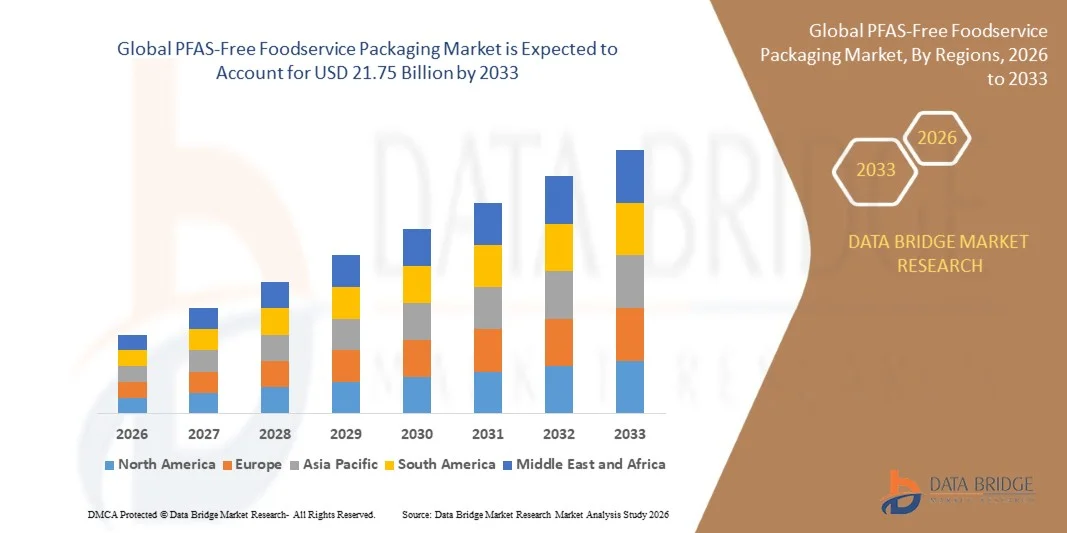

As per Data Bridge Market Research Analysis the PFAS-Free Foodservice Packaging Market was valued at USD 11.4 billion in 2025 and is projected to reach USD 21.75 billion by 2033, growing at a CAGR of 12.30% from 2026 to 2033. This significant growth outpaces broader industry estimates, reflecting the accelerating regulatory crackdown on per- and polyfluoroalkyl substances (PFAS) and the rapid transition by major quick-service restaurant (QSR) chains to safer, more sustainable packaging alternatives . Heightened consumer awareness regarding the health and environmental hazards of "forever chemicals," coupled with aggressive corporate sustainability mandates, is fundamentally reshaping the food packaging landscape .

As jurisdictions worldwide implement bans and restrictions, demand for innovative, high-performance, and cost-competitive PFAS-free solutions is soaring across the global food value chain.

Market Size & Forecast

- Global Market Value (2025): USD 11.4 Billion

- Expected Market Value (2033): USD 21.75 Billion

- Forecast CAGR (2026–2033): 12.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the PFAS-Free Foodservice Packaging Market in 2025, capturing the largest revenue share of 38% . This leadership is driven by early and stringent state-level bans (e.g., California, New York, Washington) and strong corporate commitments from major QSR chains to phase out PFAS .

- Asia-Pacific is the fastest-growing region, with a projected CAGR exceeding 8% through 2030 . Growth is fueled by rapid expansion of the foodservice and QSR sectors, increasing molded-fiber production capacity in countries like China and Malaysia, and a shift in consumer preferences toward sustainable packaging .

- The wraps and liners segment was the leading product type, capturing approximately 34.5% of revenue in 2024, driven by high-volume use in sandwiches, bakery items, and tray liners .

- The quick-service restaurants (QSR) segment is the largest end-user, holding over 41% of the market share in 2024. Major chains like McDonald's, Subway, and Chipotle are implementing global PFAS-free mandates, fundamentally reshaping the entire supply chain .

- Bioplastics are emerging as the fastest-growing material segment, with a projected CAGR of 8.6% from 2025 to 2030, driven by their enhanced barrier properties, compostability, and ability to meet stringent food-contact regulations .

Report Scope and PFAS-Free Foodservice Packaging Market Segmentation

|

Attributes |

PFAS-Free Foodservice Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

PFAS-Free Foodservice Packaging Market Trends

Trend: Rapid Commercialization of Bio-Based Barrier Coatings

The market is witnessing a significant shift from pilot projects to industrial-scale production of bio-based and water-based barrier coatings . Materials derived from seaweed, plant proteins (e.g., Xampla), chitosan, and starch are providing grease and moisture resistance comparable to PFAS while meeting stringent environmental criteria like home compostability and marine safety . These coatings are now being deployed by major QSR chains across North America and Europe . Innovations in application methods, including in-line flexographic printing, are allowing converters to apply these barriers cost-effectively without major capital investment .

PFAS-Free Foodservice Packaging Market Dynamics

Key Market Driver: Stricter Global and State-Level PFAS Bans

Aggressive regulatory action is the primary driver, creating an irreversible push away from fluorinated chemistries . The EU's Packaging and Packaging Waste Regulation (PPWR) is set to introduce a full ban on PFAS in food packaging starting in August 2026, with strict concentration limits . In the U.S., several states including Maine, New York, Washington, and California have passed legislation restricting PFAS . The FDA's ruling in March 2025 that 35 prior food-contact notifications are no longer effective set a firm sell-through deadline for existing PFAS packaging, compelling an industry-wide pivot .

Key Restraint/Challenge: 15-30% Cost Premium and Performance Gaps

Despite progress, a significant challenge is the 15-30% higher cost of PFAS-free options compared to legacy fluorinated packaging . Specialty resins, modified production lines, and lower economies of scale drive up unit costs, impacting price-sensitive segments like independent restaurants and institutional caterers . Furthermore, in extreme conditions—such as high-humidity or hot-grease applications like fried food containers—current bio-barrier systems only achieve 70-85% of the grease resistance offered by PFAS, limiting their immediate suitability for all use cases .

Key Market Opportunity: Sustainable Foodservice Packaging Expansion

The rapid growth of the sustainable foodservice packaging sector, driven by the rise of food delivery, takeaway, and QSRs, presents a massive market opportunity . As global food delivery and takeout consumption continue to surge, the demand for packaging that is both oil-resistant and environmentally safe is increasing . This creates a fertile ground for innovation in paper containers, molded fiber trays, and barrier-coated packaging that can meet the rigorous performance and sustainability standards for a wide range of foodservice applications .

PFAS-Free Foodservice Packaging Market Scope

The PFAS-free foodservice packaging market is segmented on the basis of material type, product type, end-user, and region.

- By Material Type

On the basis of material type, the market is segmented into paper & paperboard, bioplastics & bio-derived polymers, molded fiber/pulp, aluminum, and others. Paper & Paperboard is the leading material segment, valued at over 45% of the market in 2024, due to its sustainability, cost-effectiveness, and adaptability to PFAS-free coatings . The Bioplastics segment is projected to grow at the fastest CAGR (8.6% through 2030), driven by its compostability and improved barrier performance . Molded Fiber is also gaining significant traction, especially in Asia-Pacific, driven by capacity expansion and cost competitiveness for foodservice trays and bowls .

- By Product Type

On the basis of product type, the market is segmented into wraps & liners, clamshells & hinged containers, plates, bowls & trays, cups & lids, bags & pouches, and others. Wraps & Liners held the largest market share (34.5%) in 2024, driven by high-volume, high-turnover items like sandwich wraps and bakery sheets . The Clamshells and Hinged Containers segment is expected to grow robustly at a CAGR of 8.3%, fueled by rising demand from food delivery, ghost kitchens, and takeaway services that require grease-resistant packaging for hot entrees .

- By End-User

On the basis of end-user, the market is segmented into quick-service restaurants (QSR), retail & supermarkets, cafes & bakeries, institutional catering, and others. The QSR segment dominated the market in 2024, accounting for over 41% of revenue, due to corporate policies mandating sub-100 ppm total organic fluorine thresholds . The Retail and Supermarkets segment is the fastest-growing end-user, with an 8.67% CAGR, as grocery chains transition their deli, bakery, and meat tray packaging to comply with impending local bans .

PFAS-Free Foodservice Packaging Market Regional Analysis

North America dominated the PFAS-Free Foodservice Packaging Market with a 36.7% revenue share in 2024 . The region's leadership is driven by early state-level bans, voluntary FDA phase-out guidance, and aggressive QSR mandates . The U.S. market alone was valued at USD 11.14 billion in 2025, accounting for over 30% of global sales . Europe is the second-largest market, leveraging a unified PPWR framework that standardizes PFAS caps and creates predictable demand signals . Asia-Pacific is the fastest-growing region, with an 8.27% CAGR through 2030, driven by massive molded-fiber line installations in China and Malaysia and the rapid expansion of QSR and food delivery sectors .

United States PFAS-Free Foodservice Packaging Market Insight

The U.S. market is witnessing exceptional growth, fueled by an aggressive regulatory landscape (e.g., California, New York, Washington bans) and significant federal and state-level policy drivers . The FDA's phase-out guidance and the establishment of firm sell-through deadlines in 2025 forced a rapid industry-wide reformulation . Major QSR chains and retailers are actively switching to PFAS-free options, creating strong demand for certified alternatives and driving innovation in bio-based and water-based barrier coatings .

China PFAS-Free Foodservice Packaging Market Insight

China is emerging as a key growth market and cost-efficient production hub for PFAS-free packaging. Chinese molded-fiber capacity surged by 40% in 2024 as domestic delivery giants shifted to sustainable alternatives . Domestic manufacturing facilities are adding over 100,000 tons of fiber packaging capacity annually, exporting to U.S. and EU buyers . This scale-up is helping to narrow delivered-cost gaps for Western buyers, making PFAS-free options more affordable globally .

PFAS-Free Foodservice Packaging Market Share

The PFAS-free foodservice packaging industry features a moderately fragmented competitive landscape, blending global incumbents with specialized innovators. Key players including:

- Huhtamaki Oyj (Finland)

- Stora Enso Oyj (Finland)

- Smurfit WestRock plc (U.S.)

- Footprint LLC (U.S.)

- Novolex Holdings (U.S.)

- Georgia-Pacific LLC (U.S.)

- UPM Specialty Papers (Finland)

- Ahlstrom Oyj (Finland)

- Duni Group AB (Sweden)

- Vegware Ltd (U.K.)

- Biopak Pty Ltd (Australia)

- Genpak LLC (U.S.)

Latest Developments in PFAS-Free Foodservice Packaging Market

- In October 2024, Huhtamaki announced a strategic partnership with Xampla to develop protein-based barrier coatings for food packaging applications .

- In September 2024, Stora Enso completed a EUR 50 million (USD 55 million) investment in barrier-coating technology at its Oulu mill in Finland .

- In September 2024, Huhtamaki launched a new line of PFAS-free molded fiber foodservice packaging designed for QSRs and takeaway .

- In January 2024, Genpak launched its "Harvest Fiber" product line, a new molded fiber packaging line designed without intentionally added PFAS .

- In August 2024, AkzoNobel launched its Interpon Terra coating system for food-contact metal packaging after receiving FDA approval .

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Pfas Free Foodservice Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Pfas Free Foodservice Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Pfas Free Foodservice Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.