Global Pharmaceutical Metal Detector Market

Market Size in USD Million

USD

824.00 Million

USD

1,480.55 Million

2025

2033

USD

824.00 Million

USD

1,480.55 Million

2025

2033

| 2026 - 2033 | |

| USD 824.00 Million | |

| USD 1,480.55 Million | |

| % | |

|

Pharmaceutical Metal Detector Market Overview

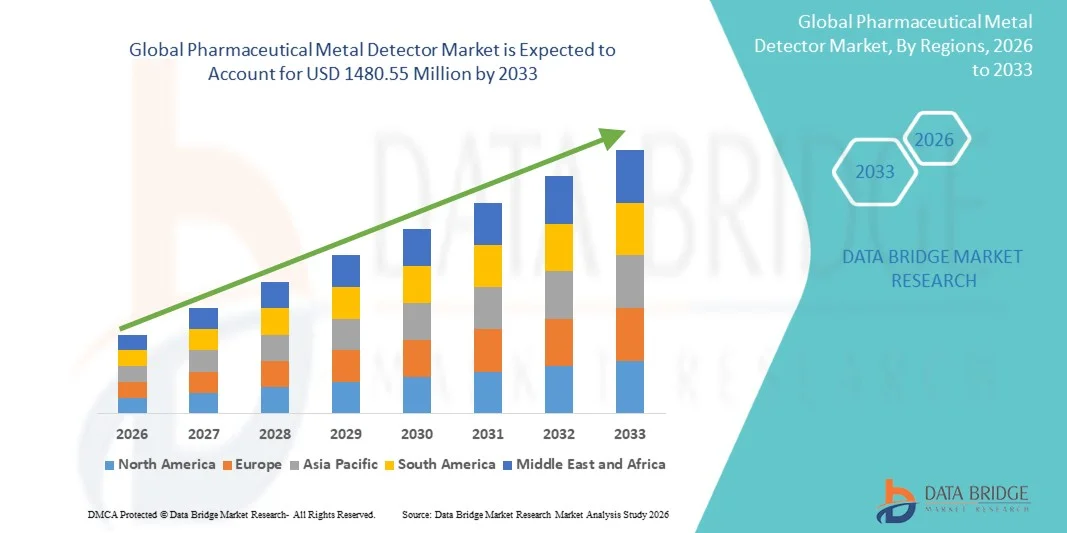

As per Data Bridge Market Research analysis the Pharmaceutical Metal Detector Market was valued at USD 824 Million in 2025 and is projected to reach USD 1480.55 Million by 2033, growing at a CAGR of 7.60% from 2026 to 2033. The market is experiencing steady growth driven by the increasing emphasis on pharmaceutical product quality, stringent regulatory requirements for contamination control, and rising adoption of automated inspection systems across pharmaceutical manufacturing facilities. The widespread use of pharmaceutical metal detectors enables manufacturers to detect and remove ferrous, non-ferrous, and stainless-steel contaminants from tablets, capsules, powders, granules, and packaged medicines, ensuring product safety, regulatory compliance, and consumer protection. Continuous advancements in digital signal processing, multi-frequency detection technology, and high-sensitivity inspection systems are improving detection accuracy while minimizing false rejects and enhancing production efficiency.

The growing production of pharmaceutical products, increasing incidence of product recalls due to foreign particle contamination, and expanding implementation of Good Manufacturing Practices (GMP) and Hazard Analysis and Critical Control Point (HACCP) standards are encouraging pharmaceutical manufacturers, contract manufacturing organizations (CMOs), and packaging companies to invest in advanced pharmaceutical metal detector systems. Modern metal detection solutions are increasingly integrated with automated production lines, serialization systems, Industry 4.0 technologies, and real-time quality monitoring platforms to enhance operational efficiency and ensure compliance with stringent regulations established by agencies such as the U.S. FDA, EMA, and other global regulatory authorities. Furthermore, continuous innovation in conveyor-based inspection systems, pipeline metal detectors, and intelligent inspection technologies is accelerating the adoption of pharmaceutical metal detector solutions across both developed and emerging markets.

Market Size & Forecast

- Market Value (2025): USD 824 Million

- Expected Market Value (2033): USD 1480.55 Million

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Pharmaceutical Metal Detector Market with the largest revenue share of approximately 35.0% in 2025, supported by stringent FDA and Health Canada regulations, the strong presence of pharmaceutical manufacturers and contract manufacturing organizations (CMOs), widespread adoption of automated quality inspection systems, and increasing investments in contamination detection technologies. The region's advanced pharmaceutical manufacturing infrastructure and growing implementation of Industry 4.0 practices continue to strengthen market leadership.

- The solutions segment dominated the market with an estimated 14% share in 2025 owing to the increasing adoption of AI-powered skin analysis software, facial imaging platforms, personalized skincare recommendation engines, virtual beauty assistants, and cloud-based digital skincare applications.

- Asia-Pacific is expected to be the fastest-growing regional market during the forecast period (2026–2033), driven by rapid expansion of pharmaceutical manufacturing capacities, increasing investments in automated production lines, rising generic drug production across China and India, strengthening regulatory compliance requirements, and growing adoption of advanced quality inspection technologies. Expanding pharmaceutical exports and modernization of manufacturing facilities across China, India, Japan, South Korea, and Southeast Asia are expected to further accelerate regional market growth.

- The retail & e-commerce platforms segment is projected to witness the fastest CAGR of 3% from 2026 to 2033, driven by the rapid growth of online beauty retail, increasing smartphone penetration, and expanding adoption of AI-powered virtual consultations and digital skincare assistants.

- The cloud-based segment dominated the market with an estimated 81% share in 2025 owing to its scalability, cost efficiency, real-time data processing capabilities, and seamless software updates

Report Scope and Pharmaceutical Metal Detector Market Segmentation

|

Attributes |

Pharmaceutical Metal Detector Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Pharmaceutical Metal Detector Market Trends

Trend: Increasing Adoption of Advanced Multi-Frequency Metal Detection Systems for Pharmaceutical Quality Control

Pharmaceutical manufacturers are increasingly adopting advanced multi-frequency and high-sensitivity metal detection systems to strengthen contamination control, comply with stringent Good Manufacturing Practices (GMP), and improve product quality. Modern pharmaceutical metal detectors are capable of detecting ferrous, non-ferrous, and stainless-steel contaminants in tablets, capsules, powders, and granules without affecting production throughput. The growing emphasis on product safety, increasing regulatory inspections, and rising pharmaceutical exports are encouraging manufacturers to upgrade conventional inspection systems with digital, automated solutions. Integration with Industry 4.0 technologies, real-time production monitoring, and automated reject mechanisms is further enhancing manufacturing efficiency and traceability. For instance, in May 2024, METTLER TOLEDO highlighted its advanced Safeline pharmaceutical metal detection systems designed for high-speed tablet and capsule inspection, offering enhanced sensitivity and compliance with FDA and GMP requirements for pharmaceutical manufacturing. This reflects the growing industry trend toward automated contamination detection and advanced product inspection technologies across pharmaceutical production facilities.

Pharmaceutical Metal Detector Market Dynamics

Key Market Driver: Stringent Pharmaceutical Quality Regulations and Growing Adoption of Automated Inspection Systems

Stringent regulatory requirements governing pharmaceutical manufacturing are a major driver of the Pharmaceutical Metal Detector Market. Regulatory authorities, including the U.S. FDA, EMA, and other global agencies, require pharmaceutical manufacturers to implement robust foreign-body detection systems to comply with Good Manufacturing Practices (GMP) and protect patient safety. Rising production of tablets, capsules, powders, and sterile medicines is increasing demand for highly sensitive metal detection technologies capable of identifying ferrous, non-ferrous, and stainless-steel contaminants. Pharmaceutical companies are also investing in automated inspection systems to reduce recalls, improve traceability, and support continuous manufacturing. For instance, in September 2024, Minebea Intec announced its participation at Pharma Pro & Pack Expo 2024, showcasing pharmaceutical inspection solutions including the CoSynus combination system, Flexus checkweigher, and advanced metal detection technologies designed to help pharmaceutical manufacturers meet stringent quality and regulatory requirements while reducing contamination risks. This reflects the growing industry investment in automated inspection technologies for pharmaceutical production.

Key Restraint/Challenge:High Validation Costs and Complex Integration with Existing Manufacturing Lines

A major challenge facing the Pharmaceutical Metal Detector Market is the high cost and complexity associated with integrating advanced inspection equipment into existing pharmaceutical production facilities. Metal detection systems must undergo Installation Qualification (IQ), Operational Qualification (OQ), and Performance Qualification (PQ) while complying with FDA 21 CFR Part 11, GMP, and other regulatory requirements. These validation activities increase implementation costs and can temporarily interrupt production during equipment installation and qualification. For instance, Mettler-Toledo states that pharmaceutical product inspection systems—including metal detectors—must be validated and integrated into existing production lines to comply with regulatory requirements while maintaining production efficiency, making implementation particularly challenging for manufacturers upgrading legacy facilities. This increases capital expenditure and extends project timelines, particularly for small and medium-sized pharmaceutical manufacturers

Key Market Opportunity: Industry 4.0 and Next-Generation Combination Inspection Systems

The growing adoption of Industry 4.0 technologies and integrated inspection solutions presents a significant opportunity for the Pharmaceutical Metal Detector Market. Pharmaceutical manufacturers are increasingly seeking combination systems that integrate metal detection, checkweighing, x-ray inspection, and digital monitoring to improve production efficiency while reducing equipment footprint. These smart inspection platforms enable real-time process monitoring, centralized data management, predictive maintenance, and improved regulatory compliance. For instance, in September 2024, Mettler-Toledo Product Inspection launched its new CM and CX Combination Systems, integrating next-generation M30 R-Series metal detectors with high-precision checkweighers and x-ray inspection technologies to provide flexible contamination detection and quality inspection for regulated manufacturing industries, including pharmaceuticals. The launch demonstrates the industry's transition toward fully integrated digital inspection systems capable of improving product safety and operational efficiency.

Pharmaceutical Metal Detector Market Scope

The pharmaceutical metal detector market is segmented on the basis of product type, technology, application, and end user.

- By Component

On the basis of component, the global AI-personalized skincare market is segmented into solutions and services. The solutions segment dominated the market with an estimated 69.14% share in 2025 owing to the increasing adoption of AI-powered skin analysis software, facial imaging platforms, personalized skincare recommendation engines, virtual beauty assistants, and cloud-based digital skincare applications. Beauty brands, dermatology clinics, cosmetic retailers, and aesthetic centers are increasingly deploying AI solutions to analyze skin conditions such as acne, wrinkles, pigmentation, pores, hydration, redness, and UV damage with high accuracy. These platforms enable real-time personalized product recommendations while improving customer engagement and treatment effectiveness. The growing commercialization of computer vision, machine learning, and generative AI technologies is further strengthening solution adoption across online and offline beauty channels. Continuous investments by cosmetic manufacturers in AI-driven digital beauty ecosystems, coupled with expanding smartphone-based skincare applications, are reinforcing the dominance of the solutions segment. Furthermore, ongoing innovation in AI software capabilities and personalized consumer experiences is expected to sustain its leading market position throughout the forecast period.

The services segment is projected to witness the fastest CAGR of 18.4% from 2026 to 2033, driven by increasing demand for AI implementation, cloud deployment, software integration, consulting, algorithm optimization, cybersecurity, and continuous platform maintenance services. As beauty companies and dermatology providers continue expanding AI-enabled skincare platforms, demand for professional implementation and managed services is growing significantly. Service providers assist organizations with AI model customization, cloud migration, consumer data management, regulatory compliance, and ongoing software upgrades. Growing partnerships between AI technology companies, skincare brands, and healthcare providers are accelerating demand for consulting and support services. In addition, the rapid expansion of subscription-based digital skincare platforms and teledermatology solutions is creating substantial opportunities for AI service providers. Continuous advancements in cloud computing, generative AI, and digital healthcare infrastructure are expected to further accelerate the growth of the services segment during the forecast period.

- By Technology

On the basis of technology, the global AI-personalized skincare market is segmented into computer vision & image recognition, machine learning & predictive analytics, generative AI & large language models (LLMs), and cloud & edge AI solutions. The computer vision & image recognition segment dominated the market with an estimated 38.62% share in 2025 owing to its extensive adoption in AI-powered facial analysis applications capable of accurately evaluating wrinkles, acne, pigmentation, pores, redness, hydration levels, dark spots, skin elasticity, and texture through high-resolution facial imaging. Beauty brands, dermatology clinics, and digital skincare platforms increasingly rely on computer vision algorithms to generate personalized skincare recommendations based on real-time facial analysis. Continuous improvements in smartphone camera technology, deep learning algorithms, and facial recognition software have significantly enhanced diagnostic precision and customer experience. The technology is also being integrated into mobile applications, smart mirrors, beauty kiosks, and e-commerce platforms to deliver seamless digital skincare experiences. Rising investments in AI-powered skin diagnostic technologies continue to reinforce the leadership of the computer vision & image recognition segment across the global market.

The generative AI & large language models (LLMs) segment is anticipated to witness the fastest CAGR of 20.1% from 2026 to 2033, driven by the growing integration of conversational AI, intelligent beauty assistants, personalized skincare coaching, and AI-generated skincare recommendations. Generative AI enables consumers to receive customized skincare routines, product education, ingredient explanations, and continuous beauty consultations through interactive digital platforms. Cosmetic companies are increasingly utilizing LLM-powered virtual assistants to improve customer engagement, product discovery, and personalized shopping experiences. Growing advancements in multimodal AI, natural language processing, and predictive analytics are further enhancing the accuracy of personalized skincare recommendations. In addition, increasing investments in generative AI platforms and digital beauty ecosystems are expected to create significant growth opportunities across cosmetic brands, dermatology providers, and online beauty retailers. These technological innovations are expected to drive robust expansion of the generative AI & large language models segment throughout the forecast period.

- By Application Area

On the basis of application area, the global AI-personalized skincare market is segmented into skin analysis & diagnostics, personalized skincare recommendations, product formulation & R&D, and virtual try-on & AR experiences. The skin analysis & diagnostics segment dominated the market with an estimated 40.36% share in 2025 owing to the growing adoption of AI-powered facial analysis platforms capable of accurately evaluating acne, wrinkles, pigmentation, dark spots, pores, redness, hydration, skin texture, elasticity, and UV damage through high-resolution facial imaging. Beauty brands, dermatology clinics, medical spas, and cosmetic retailers increasingly utilize AI-driven skin diagnostics to provide personalized consultations and product recommendations. The rapid expansion of smartphone-based skin analysis applications and AI-enabled smart beauty devices has significantly improved consumer access to professional-grade skincare assessments. In addition, growing consumer awareness regarding preventive skincare, increasing demand for science-backed beauty solutions, and continuous advancements in computer vision and predictive analytics are reinforcing the dominance of this segment. Continuous innovation in AI-powered diagnostic technologies is expected to sustain its market leadership throughout the forecast period.

The personalized skincare recommendations segment is projected to witness the fastest CAGR of 19.4% from 2026 to 2033, driven by increasing consumer demand for individualized skincare routines based on skin condition, age, genetics, environmental exposure, climate, and lifestyle habits. AI-powered recommendation engines continuously analyze facial imaging data and consumer preferences to suggest customized cleansers, serums, moisturizers, sunscreens, and treatment regimens. Cosmetic companies are increasingly integrating AI recommendation platforms into mobile applications, e-commerce websites, and digital beauty ecosystems to improve customer retention and purchasing decisions. Growing collaborations between AI technology providers, dermatologists, and beauty manufacturers are accelerating innovation in personalized skincare solutions. Furthermore, continuous advancements in generative AI, predictive analytics, and digital health technologies are expected to significantly accelerate the adoption of personalized skincare recommendations during the forecast period.

- By Deployment Mode

On the basis of deployment mode, the global AI-personalized skincare market is segmented into cloud-based, on-premises, and hybrid. The cloud-based segment dominated the market with an estimated 58.81% share in 2025 owing to its scalability, cost efficiency, real-time data processing capabilities, and seamless software updates. Cloud platforms enable beauty companies and dermatology providers to process large volumes of facial images while continuously improving AI algorithms using centralized machine learning models. Cloud deployment also facilitates integration with mobile applications, e-commerce platforms, CRM systems, and teledermatology services, enabling consumers to access personalized skincare recommendations from virtually anywhere. The increasing adoption of Software-as-a-Service (SaaS) business models, digital beauty ecosystems, and subscription-based skincare platforms is further strengthening demand. Continuous investments in secure cloud infrastructure, AI computing capabilities, and consumer data management are expected to maintain the dominance of the cloud-based deployment segment throughout the forecast period.

The hybrid segment is anticipated to witness the fastest CAGR of 18.8% from 2026 to 2033, driven by increasing demand for flexible deployment models that combine the scalability of cloud computing with the security and performance advantages of on-premises infrastructure. Large cosmetic manufacturers, dermatology networks, and beauty technology providers are increasingly adopting hybrid AI environments to protect sensitive consumer skin data while maintaining high-speed AI processing capabilities. Hybrid deployment also supports regulatory compliance, improved cybersecurity, business continuity, and seamless integration with existing enterprise systems. Growing investments in enterprise AI platforms, secure cloud architecture, and digital healthcare technologies are expected to accelerate the adoption of hybrid deployment solutions during the forecast period.

- By End User

On the basis of end user, the global AI-personalized skincare market is segmented into beauty & cosmetic brands, dermatology clinics, medical spas & aesthetic centers, retail & e-commerce platforms, and direct-to-consumer (DTC) consumers. The beauty & cosmetic brands segment dominated the market with an estimated 35.72% share in 2025 owing to increasing investments by global skincare manufacturers in AI-powered beauty technologies that improve customer engagement, product personalization, and digital commerce. Cosmetic brands are integrating AI-driven skin analysis, virtual beauty advisors, and personalized recommendation engines into their websites, mobile applications, smart mirrors, and retail stores to deliver customized skincare experiences. The growing adoption of digital beauty platforms, increasing consumer preference for personalized products, and continuous innovation in AI-powered skincare solutions are further supporting market expansion. Rising investments in generative AI, predictive analytics, and omnichannel beauty experiences continue to strengthen the leadership of the beauty & cosmetic brands segment throughout the forecast period.

The retail & e-commerce platforms segment is projected to witness the fastest CAGR of 20.3% from 2026 to 2033, driven by the rapid growth of online beauty retail, increasing smartphone penetration, and expanding adoption of AI-powered virtual consultations and digital skincare assistants. E-commerce companies are increasingly integrating AI-powered facial analysis, personalized recommendation engines, and virtual skincare advisors into online shopping platforms to improve customer experience and increase conversion rates. The growing popularity of direct-to-consumer beauty brands, subscription-based skincare services, and AI-enabled product discovery platforms is further accelerating market growth. Furthermore, continuous advancements in generative AI, cloud computing, augmented reality, and digital commerce technologies are expected to significantly expand the adoption of AI-personalized skincare solutions across retail and e-commerce platforms during the forecast period.

Pharmaceutical Metal Detector Market Regional Analysis

North America dominated the pharmaceutical metal detector market and accounted for the largest revenue share of approximately 35.00% in 2025, supported by stringent regulatory requirements enforced by the U.S. Food and Drug Administration (FDA) and Health Canada, the strong presence of leading pharmaceutical manufacturers and contract manufacturing organizations (CMOs), and widespread adoption of advanced contamination detection technologies. The region benefits from highly automated pharmaceutical production facilities, strict implementation of Good Manufacturing Practices (GMP), and increasing investments in Industry 4.0-enabled manufacturing systems. Pharmaceutical manufacturers are increasingly integrating high-sensitivity metal detectors into tablet, capsule, powder, and packaging lines to improve product quality and ensure regulatory compliance. Continuous investments in automated inspection systems and digital quality assurance technologies continue to reinforce North America's leadership in the Pharmaceutical Metal Detector Market.

U.S. Pharmaceutical Metal Detector Market Insight

The U.S. pharmaceutical metal detector market is witnessing robust growth owing to the country's large pharmaceutical manufacturing base, increasing implementation of FDA quality standards, and rising investments in automated inspection and contamination detection systems. Pharmaceutical companies and CDMOs are increasingly deploying high-performance metal detectors to detect ferrous, non-ferrous, and stainless-steel contaminants throughout manufacturing and packaging operations. The growing adoption of Industry 4.0 technologies, real-time quality monitoring systems, and automated production lines is further improving operational efficiency and product safety. Furthermore, increasing pharmaceutical exports, expanding biologics manufacturing, and continuous modernization of production facilities are accelerating market growth across the United States.

Europe Pharmaceutical Metal Detector Market Insight

The Europe pharmaceutical metal detector market is experiencing significant growth due to stringent pharmaceutical quality regulations, increasing pharmaceutical manufacturing activities, and growing investments in automated inspection technologies. Pharmaceutical companies across Europe are increasingly adopting high-precision metal detection systems to comply with European Medicines Agency (EMA) regulations and Good Manufacturing Practices (GMP). Rising investments in pharmaceutical automation, contamination prevention, and smart manufacturing technologies are strengthening market demand. In addition, expanding contract manufacturing services and increasing production of high-value pharmaceutical products continue to support regional market growth.

U.K. Pharmaceutical Metal Detector Market Insight

The U.K. pharmaceutical metal detector market is expanding steadily, supported by increasing investments in pharmaceutical manufacturing, rising implementation of automated quality control systems, and growing demand for contamination-free pharmaceutical products. Pharmaceutical manufacturers are increasingly integrating advanced inspection technologies into production and packaging operations to improve product safety and regulatory compliance. Furthermore, increasing adoption of digital manufacturing technologies, continuous investments in life sciences infrastructure, and expansion of pharmaceutical exports are contributing to sustained market growth.

Germany Pharmaceutical Metal Detector Market Insight

The Germany pharmaceutical metal detector market is witnessing steady expansion due to the country's strong pharmaceutical manufacturing sector, advanced industrial automation capabilities, and increasing investments in precision quality inspection technologies. German pharmaceutical companies are increasingly deploying high-sensitivity metal detection systems across solid dosage, injectable, and packaging production lines to ensure compliance with EU regulatory standards. Furthermore, continuous investments in smart factories, pharmaceutical process automation, and digital manufacturing technologies continue to strengthen market growth across Germany.

Asia-Pacific Pharmaceutical Metal Detector Market Insight

The Asia-Pacific pharmaceutical metal detector market is expected to witness the fastest growth during the forecast period, driven by rapid expansion of pharmaceutical manufacturing capacities, increasing investments in automated production lines, rising generic drug production across China and India, strengthening regulatory compliance requirements, and growing adoption of advanced quality inspection technologies. Expanding pharmaceutical exports, increasing healthcare expenditure, and modernization of pharmaceutical manufacturing facilities are accelerating the demand for contamination detection systems throughout the region. Furthermore, continuous investments in smart manufacturing, industrial automation, and GMP-compliant production infrastructure are expected to support the highest CAGR from 2026 to 2033, positioning Asia-Pacific as the fastest-growing regional market.

Japan Pharmaceutical Metal Detector Market Insight

The Japan pharmaceutical metal detector market is witnessing consistent growth due to the country's advanced pharmaceutical manufacturing infrastructure, stringent quality assurance standards, and increasing adoption of automated inspection technologies. Pharmaceutical manufacturers are investing in high-performance contamination detection systems to improve manufacturing efficiency, comply with regulatory requirements, and enhance product quality. In addition, continuous innovation in pharmaceutical production technologies and increasing exports of high-value pharmaceutical products are contributing to market expansion.

China Pharmaceutical Metal Detector Market Insight

The China pharmaceutical metal detector market is growing rapidly owing to the country's rapidly expanding pharmaceutical manufacturing industry, increasing production of generic medicines and active pharmaceutical ingredients (APIs), and rising investments in automated quality inspection systems. Pharmaceutical manufacturers are increasingly deploying advanced metal detection solutions to comply with international quality standards and support export-oriented manufacturing. In addition, government initiatives promoting pharmaceutical modernization, expansion of contract manufacturing organizations (CMOs), and growing implementation of Industry 4.0 technologies are positioning China as one of the fastest-growing markets for pharmaceutical metal detector systems globally.

Pharmaceutical Metal Detector Market Share

The pharmaceutical metal detector industry is primarily led by well-established companies, including:

- METTLER TOLEDO (U.S./Switzerland)

- ANRITSU CORPORATION (Japan)

- Thermo Fisher Scientific Inc. (U.S.)

- Minebea Intec GmbH (Germany)

- Bizerba (Germany)

- Loma Systems (U.K.)

- CEIA S.p.A. (Italy)

- Cassel Messtechnik GmbH (Germany)

- Sesotec GmbH (Germany)

- Fortress Technology Inc. (Canada)

- Eriez Manufacturing Co. (U.S.)

- Nikka Densok Limited (Japan)

- COSO Electronic Tech Co., Ltd. (China)

- Shanghai Techik Instrument Co., Ltd. (China)

- Mesutronic Gerätebau GmbH (Germany)

- Yamato Scale Co., Ltd. (Japan)

- Mekitec Group (Finland)

- Wipotec GmbH (Germany)

- Ishida Co., Ltd. (Japan)

Latest Developments in Pharmaceutical Metal Detector Market

- In September 2024, Mettler-Toledo Product Inspection announced the launch of its new CM (checkweighing and metal detection) and CX (checkweighing and X-ray) Combination Systems. The new systems integrate the M30 R-Series metal detectors with C-Series checkweighers and X2 Series X-ray inspection systems, providing pharmaceutical manufacturers with enhanced contaminant detection, higher sensitivity, improved regulatory compliance, and a space-saving integrated inspection solution. The launch reflects the growing adoption of automated quality inspection technologies across pharmaceutical manufacturing

- In September 2024, Minebea Intec announced its participation at Pharma Pro & Pack Expo 2024 and showcased its pharmaceutical inspection portfolio, including the CoSynus combination system, Flexus checkweigher, Vistus metal detector, and advanced weighing solutions. The company highlighted these technologies to help pharmaceutical manufacturers improve contamination detection, comply with GMP requirements, and enhance product quality and patient safety

- In September 2024, Mettler-Toledo Product Inspection announced that it would demonstrate its latest combination inspection systems, metal detectors, X-ray inspection systems, and ProdX™ data management software at PACK EXPO International 2024. The company showcased integrated inspection technologies designed to improve contamination detection, digital quality management, regulatory compliance, and production efficiency for pharmaceutical and other highly regulated industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.